Market Overview

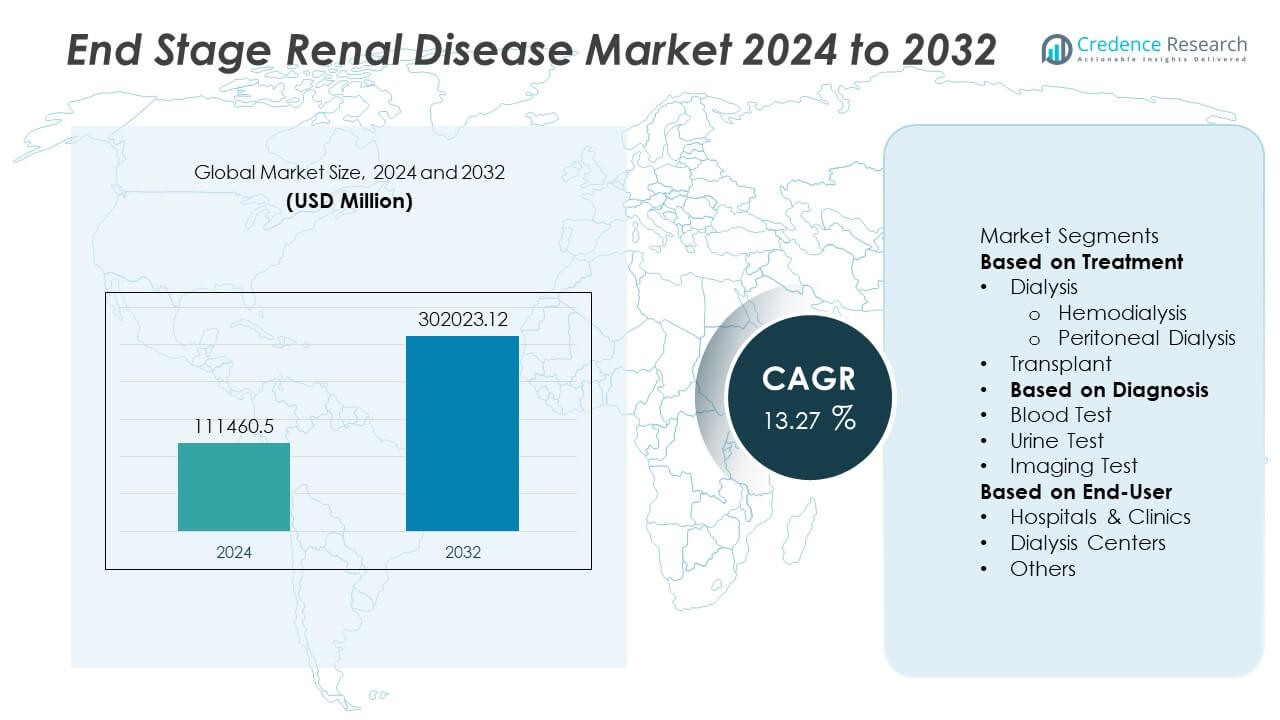

The End Stage Renal Disease (ESRD) market was valued at approximately USD 111,460.5 million in 2024. It is projected to grow significantly, reaching around USD 302,023.12 million by 2032, reflecting a compound annual growth rate (CAGR) of 13.27% over the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| End Stage Renal Disease (ESRD) market Size 2024 |

USD 111,460.5Million |

| End Stage Renal Disease (ESRD) market, CAGR |

13.27% |

| End Stage Renal Disease (ESRD) market Size 2032 |

USD 302,023.12 Million |

The End Stage Renal Disease Market experiences robust growth driven by rising prevalence of chronic kidney conditions, increasing geriatric populations, and advances in dialysis and transplantation technologies. Growing awareness and early diagnosis programs enhance patient access to treatment. Market trends emphasize personalized therapies, adoption of home-based and wearable dialysis devices, and integration of digital health solutions for remote monitoring.

The End Stage Renal Disease Market exhibits significant growth across key regions including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America leads due to advanced healthcare infrastructure and strong government support, while Asia Pacific shows rapid expansion fueled by rising chronic disease prevalence and improving medical access. Europe focuses on home dialysis and transplantation programs, whereas Latin America and the Middle East & Africa work on expanding healthcare facilities and awareness. Prominent players driving innovation and competition in this market include Abbott, Amgen Inc., AstraZeneca, and Hoffmann-La Roche Limited. These companies invest heavily in research and development to introduce advanced dialysis devices, novel drug therapies, and digital health platforms.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The End Stage Renal Disease Market was valued at USD 111,460.5 million in 2024 and is projected to reach USD 302,023.12 million by 2032, growing at a CAGR of 13.27% during the forecast period.

- Increasing prevalence of chronic kidney diseases and rising cases of diabetes and hypertension drive demand for dialysis and transplantation treatments globally.

- Market trends highlight the growing adoption of home-based dialysis and wearable devices that improve patient convenience and treatment adherence.

- Technological advancements in dialysis equipment and novel drug therapies targeting ESRD complications enhance treatment effectiveness and patient outcomes.

- Competitive landscape features key players such as Abbott, Amgen Inc., AstraZeneca, and Hoffmann-La Roche Limited, focusing on product innovation and strategic partnerships to strengthen market presence.

- High treatment costs, limited access in developing regions, and challenges related to patient compliance restrict market growth and pose significant barriers.

- Regionally, North America and Europe lead due to advanced healthcare infrastructure, while Asia Pacific shows rapid growth driven by increasing disease prevalence and improving medical facilities. Latin America and the Middle East & Africa are emerging markets with growing investment in healthcare access and awareness programs.

Market Drivers

Rising Prevalence of Chronic Kidney Diseases Drives Demand in the End Stage Renal Disease Market

The increasing prevalence of chronic kidney diseases worldwide significantly fuels the demand within the End Stage Renal Disease Market. Growing incidence of diabetes and hypertension, which are primary causes of kidney failure, creates a substantial patient base requiring dialysis and transplantation. Healthcare systems across regions continue expanding their capacity to diagnose and treat renal conditions, improving access to care. Rising awareness about kidney health and early intervention drives higher patient participation in treatment programs. The surge in the elderly population, more susceptible to kidney dysfunction, further intensifies market demand. Innovation in renal replacement therapies attracts both patients and providers toward advanced treatment options.

- For instance, Amgen reported that its drug, Sensipar (cinacalcet), used for managing secondary hyperparathyroidism in ESRD patients, reached over 1 million patients globally by 2023, highlighting its broad adoption and impact in managing complications associated with kidney failure.

Technological Innovations in Dialysis and Transplantation Enhance Market Growth

Technological advancements in dialysis devices and transplantation procedures play a critical role in shaping the End Stage Renal Disease Market. Improvements in hemodialysis and peritoneal dialysis equipment increase treatment efficiency and patient comfort. Minimally invasive surgical techniques and enhanced immunosuppressive therapies improve transplant success rates and long-term outcomes. Companies invest heavily in research and development to bring new products with better safety profiles and reduced complications. The integration of digital health tools enables better patient monitoring and personalized care plans. It also supports remote management, reducing hospital visits and improving quality of life for patients.

- For instance, Baxter International introduced the AMIA automated peritoneal dialysis system in 2022, which features integrated connectivity allowing remote monitoring of treatment adherence in over 50,000 patients worldwide, reducing hospitalization rates and improving therapy outcomes.

Supportive Government Policies and Reimbursement Frameworks Strengthen Market Potential

Rising government initiatives and reimbursement policies boost the affordability and availability of treatments in the End Stage Renal Disease Market. Public and private healthcare sectors allocate increasing budgets to kidney disease management programs. Policies promoting organ donation and transplant infrastructure development enhance treatment options for patients with ESRD. Favorable reimbursement frameworks encourage healthcare providers to adopt advanced therapies and expand services. Insurance coverage improvements reduce out-of-pocket expenses, encouraging early and regular treatment adherence. These factors collectively strengthen the overall market environment, encouraging innovation and wider patient reach.

Increasing Adoption of Home-Based Dialysis Therapies Shapes Market Dynamics

Growing patient preference for home-based dialysis therapies influences market dynamics by promoting convenience and cost-effectiveness. Home dialysis options reduce dependence on clinical settings and lower the risk of infections associated with frequent hospital visits. Patient education and support programs increase acceptance of these therapies among eligible individuals. It also enables better treatment adherence through flexible scheduling and enhanced comfort. Healthcare providers adapt their offerings to include telemedicine support and remote monitoring for home dialysis patients. This trend supports sustainable market growth by addressing patient lifestyle needs while maintaining treatment efficacy.

Market Trends

Expansion of Personalized Treatment Approaches Influences the End Stage Renal Disease Market

The End Stage Renal Disease Market experiences a significant shift toward personalized treatment strategies tailored to individual patient needs. Advances in genetic testing and biomarker identification enable healthcare providers to design customized therapies that improve clinical outcomes. Precision medicine guides decisions on dialysis modalities and transplant eligibility, optimizing patient care. Patient-specific treatment plans help reduce complications and enhance quality of life. Integration of artificial intelligence assists in predicting disease progression and treatment responses. It drives more accurate and timely interventions, increasing treatment effectiveness.

- For instance, Novartis’ Fabhalta® (iptacopan) has received multiple FDA approvals, including for the treatment of C3 glomerulopathy (C3G), a rare kidney disease.

Growth in Home-Based and Wearable Dialysis Technologies Shapes Patient Care

Home-based dialysis and wearable devices gain momentum within the End Stage Renal Disease Market by offering greater convenience and autonomy for patients. These technologies allow patients to perform dialysis outside clinical settings, reducing hospital visits and associated costs. Wearable dialysis systems provide continuous blood filtration, mimicking natural kidney function more closely. Companies invest in developing compact, user-friendly devices that promote patient independence. Remote monitoring platforms support medical oversight while patients manage therapy at home. This trend meets growing demand for flexible treatment options that align with modern lifestyles.

- For instance, NxStage Medical, a subsidiary of Fresenius, reported that over 45,000 patients worldwide used its home hemodialysis systems by 2023, enabling remote care management and improving adherence to treatment protocols.

Emergence of Novel Drug Therapies to Manage Complications Enhances Market Landscape

The development of innovative pharmacological treatments addresses complications related to End Stage Renal Disease and improves patient outcomes. New drug candidates focus on reducing inflammation, anemia, and cardiovascular risks frequently associated with renal failure. It helps in managing secondary conditions that significantly impact patient survival and quality of life. Pharmaceutical companies prioritize research on therapies that complement dialysis and transplantation procedures. Introduction of targeted biologics and oral medications expands treatment choices available to clinicians. This evolution strengthens the therapeutic arsenal within the End Stage Renal Disease Market.

Increasing Adoption of Digital Health Solutions Transforms Patient Management

Digital health solutions play an increasingly important role in managing End Stage Renal Disease by enabling remote patient monitoring and data-driven decision-making. Mobile applications, wearable sensors, and telemedicine platforms improve patient engagement and adherence to treatment regimens. Real-time tracking of vital signs and treatment parameters facilitates early detection of complications. Healthcare providers use analytics to optimize care pathways and personalize interventions. It promotes coordinated care across multidisciplinary teams, enhancing treatment efficiency. This trend accelerates the integration of technology into routine ESRD management, driving better outcomes.

Market Challenges Analysis

High Treatment Costs and Limited Access to Advanced Therapies Restrain Market Growth

The End Stage Renal Disease Market faces significant challenges due to the high costs associated with dialysis and kidney transplantation. Many patients in low- and middle-income regions struggle to afford continuous treatment and related healthcare services. Limited availability of advanced dialysis equipment and skilled healthcare professionals restricts access to optimal care in underserved areas. Insurance coverage gaps and reimbursement constraints create financial barriers for patients and providers. It hampers treatment adherence and contributes to poor clinical outcomes. The complexity of managing long-term therapies further strains healthcare infrastructure. These factors collectively slow market expansion despite growing patient demand.

Clinical Complications and Patient Compliance Challenges Impact Treatment Effectiveness

Clinical complications linked to End Stage Renal Disease therapies pose ongoing challenges within the market. Patients often experience cardiovascular issues, infections, and other comorbidities that complicate management and increase mortality risk. Ensuring strict patient compliance with dialysis schedules, medication regimens, and lifestyle modifications proves difficult. Psychological stress and quality-of-life concerns reduce patient motivation and treatment adherence. Healthcare providers must invest significant resources in patient education and support programs to improve outcomes. It remains challenging to balance treatment intensity with patient comfort and long-term wellbeing. These clinical and behavioral factors constrain overall treatment success and market potential.

Market Opportunities

Expansion of Emerging Markets and Increasing Healthcare Investments Present Growth Opportunities

The End Stage Renal Disease Market benefits from expanding healthcare infrastructure and investments in emerging economies. Rising government spending on chronic disease management supports the development of dialysis centers and transplant programs. Growing awareness campaigns improve early diagnosis and encourage timely treatment initiation. Increasing urbanization and improving healthcare access widen the patient base in these regions. It opens opportunities for manufacturers and service providers to introduce affordable and scalable solutions. Collaborations between public and private sectors further enhance resource availability. These trends create a favorable environment for market penetration and revenue growth.

Innovation in Treatment Technologies and Digital Health Solutions Unlocks New Potential

Innovation remains a key opportunity within the End Stage Renal Disease Market through the development of advanced treatment modalities and digital tools. Emerging technologies such as wearable dialysis devices and portable machines offer patient-friendly alternatives to traditional therapies. Integration of telemedicine and remote monitoring improves patient management and reduces healthcare costs. Investment in novel drug therapies targeting ESRD complications broadens therapeutic options. It allows healthcare providers to deliver more personalized and effective care. These advancements drive market differentiation and create pathways for sustained growth and competitive advantage.

Market Segmentation Analysis:

By Treatment

The End Stage Renal Disease Market primarily divides treatment into dialysis and kidney transplantation. Dialysis further splits into hemodialysis and peritoneal dialysis, with hemodialysis dominating due to widespread availability and established clinical protocols. Kidney transplantation presents a curative option but faces limitations due to donor shortages and complex post-operative management. Treatment innovation continues to focus on improving dialysis efficiency and transplant success rates to enhance patient outcomes.

- For instance, Fresenius Medical Care reported that over 345,000 patients worldwide received hemodialysis treatments using its dialysis machines in 2023, reflecting its leadership in dialysis technology and patient care.

By Diagnosis

The market segments diagnosis into imaging techniques, biopsy procedures, and blood and urine tests. Imaging techniques, including ultrasound and MRI, assist in early detection and monitoring of kidney damage. Biopsy procedures provide definitive diagnosis and staging of renal failure, guiding treatment decisions. Blood and urine tests remain essential for routine monitoring and assessing disease progression. It benefits from continuous advancements in diagnostic accuracy and minimally invasive methods, facilitating timely intervention and personalized therapy.

- For instance, GE Healthcare’s ultrasound systems were used in over 120,000 renal diagnostic procedures worldwide in 2023, enhancing early detection of kidney abnormalities.

By End-User

The end-user segment includes hospitals, dialysis centers, specialty clinics, and home care settings. Hospitals serve as primary hubs for both diagnosis and treatment of End Stage Renal Disease, offering comprehensive care and access to advanced technologies. Dialysis centers specialize in providing outpatient dialysis services and support a large patient population. Specialty clinics focus on nephrology care and often coordinate multidisciplinary treatment plans. Home care settings gain popularity due to increasing patient preference for convenience and improved quality of life through home-based dialysis therapies. The shift towards decentralized care supports better adherence and reduces healthcare system burdens.

Segments:

Based on Treatment

-

- Hemodialysis

- Peritoneal Dialysis

- Transplant

Based on Diagnosis

Based on End-User

- Hospitals & Clinics

- Dialysis Centers

- Others

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

The global End Stage Renal Disease (ESRD) Market is distributed unevenly across regions, reflecting variations in healthcare infrastructure, prevalence of chronic kidney disease, and economic development. North America holds the largest market share, accounting for approximately 35% of the global ESRD market. The region benefits from advanced healthcare systems, early diagnosis programs, and widespread availability of dialysis and transplantation services. Strong government support and favorable reimbursement policies further boost market growth. The United States, in particular, drives demand due to high incidence rates of diabetes and hypertension, which are major causes of kidney failure. Innovative treatment technologies and digital health adoption also contribute to maintaining North America’s leading position.

Europe

Europe captures around 25% of the global End Stage Renal Disease Market, driven by increasing geriatric populations and well-established healthcare networks. Countries like Germany, the United Kingdom, and France lead with comprehensive renal care programs and extensive dialysis centers. European governments invest in organ donation awareness and transplantation infrastructure, improving treatment options. The region also sees growing adoption of home dialysis therapies and advanced diagnostic tools. Challenges such as rising treatment costs create pressure on healthcare budgets but encourage the development of cost-effective therapies. Regulatory frameworks ensure patient safety and quality standards, supporting sustained market expansion in Europe.

Asia Pacific

The Asia Pacific region holds about 28% of the global ESRD market share, emerging as a rapidly growing segment due to rising prevalence of chronic kidney diseases and expanding healthcare access. Countries such as China, India, Japan, and Australia significantly contribute to market growth. Increasing urbanization, lifestyle changes, and growing incidence of diabetes accelerate demand for dialysis and transplantation therapies. Governments across the region improve healthcare infrastructure and reimbursement schemes, encouraging greater patient access to renal care. The Asia Pacific market also attracts investments in innovative treatment technologies and local manufacturing of dialysis equipment. However, disparities in healthcare quality between urban and rural areas remain a challenge for market penetration.

Latin America

Latin America accounts for roughly 7% of the global End Stage Renal Disease Market. Rising awareness about kidney health and expanding healthcare infrastructure fuel gradual market growth. Countries like Brazil, Mexico, and Argentina focus on improving dialysis services and transplant programs to meet increasing patient demand. Economic constraints and limited access to advanced therapies restrict rapid market expansion, but government initiatives and international collaborations support improvements. Efforts to enhance patient education and increase organ donation rates gain traction, offering future growth potential.

Middle East and Africa

The Middle East and Africa collectively represent around 5% of the global ESRD market. The region faces challenges related to limited healthcare infrastructure and resource constraints. However, growing prevalence of chronic diseases and increased government investments in healthcare create opportunities for market development. Countries such as Saudi Arabia, South Africa, and the United Arab Emirates lead regional efforts to improve renal care. Adoption of innovative technologies and telemedicine solutions help overcome access barriers. Strategic partnerships and capacity-building programs drive gradual market growth despite ongoing economic and logistical challenges.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Hoffmann-La Roche Limited

- Keryx Biopharmaceuticals Inc.

- Bristol-Myers Squibb Company

- Kissei Pharmaceutical Co. Limited

- Amgen Inc.

- AstraZeneca

- Novartis

- Abbott

- GlaxoSmithKline plc

- Pfizer Inc.

Competitive Analysis

The End Stage Renal Disease Market features intense competition among leading players such as Abbott, Amgen Inc., AstraZeneca, Hoffmann-La Roche Limited, Bristol-Myers Squibb Company, Pfizer Inc., GlaxoSmithKline plc, Keryx Biopharmaceuticals Inc., Kissei Pharmaceutical Co. Limited, and Novartis. These companies focus on continuous innovation to develop advanced dialysis technologies, novel pharmacological treatments, and digital health solutions that improve patient outcomes and treatment efficiency. Strategic collaborations, mergers, and acquisitions strengthen their market positions and expand geographic reach. Key players invest heavily in research and development to enhance product portfolios and address unmet clinical needs. They also engage in partnerships with healthcare providers and institutions to improve access and patient care services. Competitive pricing strategies and robust distribution networks further enable these companies to capture larger market shares. Their ability to offer personalized therapies and integrate technological advancements, such as wearable dialysis devices and remote monitoring platforms, differentiates them in a growing and evolving market. This competitive environment drives the overall progress of the End Stage Renal Disease Market by fostering innovation and improving treatment accessibility worldwide.

Recent Developments

- In July 2025, AstraZeneca announced that its experimental drug, baxdrostat, effectively lowered blood pressure in a late-stage trial involving patients with treatment-resistant hypertension, a condition often associated with ESRD.

- In May 2025, Kissei Pharmaceutical Co. Limited announced that it had exceeded its initial sales targets for the final year of its 2024 Medium-term Management Plan, though specific details related to ESRD treatments were not provided

- In April 2025, Novartis received FDA accelerated approval for Vanrafia® (atrasentan), the first and only selective endothelin A receptor antagonist for proteinuria reduction in primary IgA nephropathy, a kidney disease that can lead to ESRD.

Market Concentration & Characteristics

The End Stage Renal Disease Market demonstrates a moderately concentrated competitive landscape dominated by a few key global players who command significant market share through extensive product portfolios and technological innovations. These leading companies focus on developing advanced dialysis equipment, novel pharmacological therapies, and integrated digital health solutions to meet the growing patient demand. The market features a mix of large multinational corporations and specialized regional players, creating a dynamic environment driven by continuous research and development investments. It experiences steady entry of innovative startups that introduce disruptive technologies, increasing competition and accelerating treatment advancements. Partnerships, mergers, and acquisitions further shape market concentration by enabling companies to expand geographic presence and enhance service capabilities. The market maintains high regulatory standards that drive quality and safety in treatment offerings. It serves diverse end-users, including hospitals, specialty clinics, dialysis centers, and home care settings, which influence product customization and service delivery models. This structure allows the market to balance innovation with accessibility, ensuring sustained growth and improved patient outcomes globally.

Report Coverage

The research report offers an in-depth analysis based on Treatment, Diagnosis, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The End Stage Renal Disease Market will continue expanding due to rising chronic kidney disease prevalence.

- Advances in dialysis technology will improve treatment efficiency and patient comfort.

- Home-based dialysis therapies will gain wider acceptance among patients and healthcare providers.

- Digital health solutions will enhance remote patient monitoring and personalized care.

- Pharmaceutical innovations will introduce new drugs targeting ESRD complications.

- Emerging markets will see increased healthcare infrastructure investments, boosting market growth.

- Collaborations between key players will drive product development and market penetration.

- Regulatory support will strengthen safety and quality standards in ESRD treatments.

- Patient education programs will improve treatment adherence and outcomes.

- The market will focus more on sustainable and cost-effective treatment options.