Market Overview

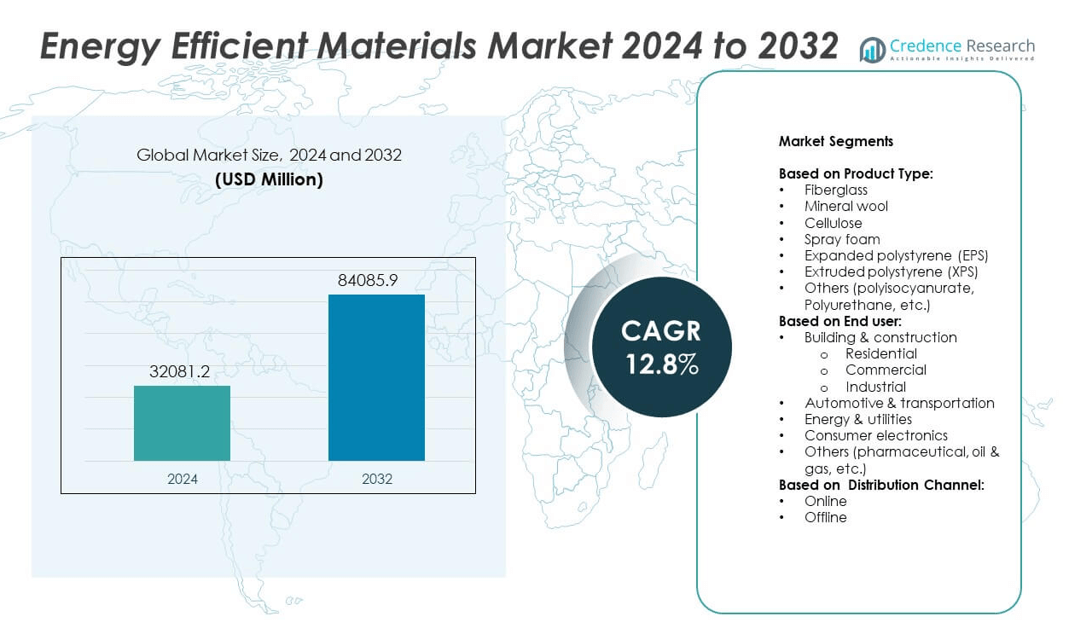

The Energy Efficient Materials market size was valued at USD 32,081.2 million in 2024 and is anticipated to reach USD 84,085.9 million by 2032, growing at a CAGR of 12.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Energy Efficient Materials Market Size 2024 |

USD 32,081.2 million |

| Energy Efficient Materials Market, CAGR |

12.8% |

| Energy Efficient Materials Market Size 2032 |

USD 84,085.9 million |

The Energy Efficient Materials market grows rapidly due to increasing regulatory support and government initiatives promoting sustainability and carbon reduction. Rising demand from the construction sector for green buildings and energy-saving solutions further fuels adoption. Technological advancements introduce innovative materials with enhanced thermal performance and multifunctional properties, expanding applications across industries. Consumer awareness about reducing energy costs also drives market demand. Simultaneously, trends such as integration of smart materials, emphasis on lightweight composites in automotive, and adoption of circular economy principles shape the market’s evolution. These factors collectively stimulate robust growth and continuous innovation.

The Energy Efficient Materials market demonstrates strong growth across North America, Europe, and Asia Pacific, driven by regulatory support, urbanization, and sustainability initiatives. North America and Europe lead with advanced infrastructure and stringent energy efficiency standards, while Asia Pacific experiences rapid demand due to industrial expansion and urban development. Key players shaping the market include Rockwool International, Owens Corning, Kingspan Group, and Saint-Gobain. These companies focus on innovation, expanding product portfolios, and strategic partnerships to meet diverse end-user needs and capitalize on emerging opportunities across global regions.

Market Insights

- The Energy Efficient Materials market was valued at USD 32,081.2 million in 2024 and is projected to reach USD 84,085.9 million by 2032, growing at a CAGR of 12.8% during the forecast period.

- Increasing government regulations and incentives aimed at reducing carbon emissions significantly drive market growth by encouraging the adoption of energy-efficient materials across industries.

- Technological advancements, including the development of smart, multifunctional, and lightweight materials, shape market trends by enhancing energy conservation and expanding application areas.

- Major companies such as Rockwool International, Owens Corning, Kingspan Group, and Saint-Gobain lead the market with a strong focus on innovation, product diversification, and global expansion.

- High initial costs and complex manufacturing processes restrain market growth, limiting adoption especially among small and medium enterprises and cost-sensitive projects.

- North America, Europe, and Asia Pacific dominate the market due to stringent regulations, advanced infrastructure, and rapid urbanization, with emerging economies in Asia Pacific presenting significant growth opportunities.

- Market challenges include lack of standardized regulations and limited awareness in certain regions, which affect confidence in product performance and slow down widespread acceptance

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Growing Regulatory Support and Government Initiatives Accelerate Adoption of Energy Efficient Materials

Strict regulations and government policies aimed at reducing carbon emissions and enhancing energy conservation significantly drive the Energy Efficient Materials market. Governments worldwide implement mandatory standards for building codes and industrial processes, encouraging the use of materials that minimize energy loss. Incentives such as tax rebates and subsidies further promote investment in energy-efficient technologies. These regulatory frameworks push manufacturers and end-users to adopt materials that comply with environmental targets. It also creates opportunities for innovation and development of advanced materials that meet stringent criteria. Increasing global focus on sustainability reinforces the market’s steady expansion.

- For instance, Kingspan Group has installed over 4 million square meters of insulated panels globally that improve building energy performance, supporting green building initiatives.

Rising Demand for Sustainable Construction and Green Building Projects Boost Market Growth

The construction sector’s shift towards sustainability plays a pivotal role in expanding the Energy Efficient Materials market. Builders and developers prioritize materials that reduce energy consumption in residential and commercial buildings to achieve certifications like LEED and BREEAM. It contributes to enhanced insulation, thermal regulation, and reduced operational costs. Consumers increasingly demand buildings with lower environmental impact, encouraging widespread adoption of energy-saving materials. This trend supports market growth by driving higher volumes of material usage. The emphasis on long-term energy cost savings motivates stakeholders to invest in energy-efficient solutions.

- For instance, Owens Corning developed a spray foam insulation product with a global installed base exceeding 1 billion square feet, offering superior R-value per inch compared to traditional materials.

Technological Advancements Enable Development of Innovative Energy Efficient Materials

Technological progress drives the introduction of novel materials with improved thermal performance, durability, and cost-effectiveness in the Energy Efficient Materials market. Research and development efforts focus on enhancing material properties to meet evolving industry demands. Innovations include phase change materials, advanced coatings, and high-performance insulation products that optimize energy efficiency. Manufacturers leverage cutting-edge production techniques to reduce costs and increase scalability. These advancements open new applications across sectors such as construction, automotive, and electronics. Continuous innovation ensures the market remains dynamic and competitive.

Increasing Consumer Awareness and Focus on Reducing Energy Costs Stimulate Market Demand

Consumers and businesses actively seek ways to lower energy expenses, which directly influences the Energy Efficient Materials market. Awareness regarding environmental impacts and rising utility prices prompt investment in materials that improve energy conservation. It creates strong demand for products that deliver tangible cost benefits through enhanced efficiency. End-users prioritize solutions that extend lifecycle performance and reduce maintenance costs. This shift in consumer behavior encourages manufacturers to develop user-friendly, high-performance energy-efficient materials. The market benefits from growing recognition of the economic and environmental advantages these materials offer.

Market Trends

Increasing Integration of Smart and Multifunctional Energy Efficient Materials in Construction and Industry

The Energy Efficient Materials market experiences a significant shift towards smart and multifunctional materials that enhance energy conservation while offering additional benefits. These materials incorporate sensors or responsive properties to adapt to environmental changes such as temperature and humidity. It allows buildings and industrial systems to optimize energy use dynamically, reducing waste. The adoption of these advanced materials improves overall system performance and supports predictive maintenance strategies. Growing interest in intelligent solutions drives research and commercialization efforts. This trend reflects a move beyond traditional insulation and coatings toward more interactive energy management tools.

- For instance, Toray Industries supplied over 50,000 carbon fiber composite components annually to aerospace manufacturers, contributing to a significant weight reduction of commercial aircraft.

Expansion of Lightweight and High-Performance Materials for Automotive and Aerospace Sectors

Lightweight energy efficient materials gain traction within the automotive and aerospace industries due to their ability to reduce fuel consumption and emissions. The Energy Efficient Materials market sees increased demand for composites, carbon fiber, and advanced polymers that deliver strength without added weight. Manufacturers prioritize these materials to meet stringent regulatory standards on emissions and enhance vehicle efficiency. It supports the development of electric and hybrid vehicles by improving battery life and overall performance. The trend toward sustainability in transport accelerates adoption across global markets. Growing collaborations between material scientists and industry stakeholders fuel continuous improvements.

- For instance, BASF’s bio-based insulation foam production has reached over 25,000 tons annually, supporting lower environmental footprints with fully recyclable materials.

Growing Focus on Circular Economy Principles and Recyclable Energy Efficient Materials

Sustainability trends drive the Energy Efficient Materials market toward circular economy principles, emphasizing reuse and recyclability. Companies increasingly develop materials that minimize environmental impact throughout their lifecycle, including manufacturing, use, and disposal phases. It encourages design approaches that allow materials to be recovered and repurposed effectively. This focus reduces waste generation and conserves natural resources, aligning with corporate social responsibility goals. Demand rises for bio-based and eco-friendly materials that meet energy efficiency requirements without compromising sustainability. The integration of circular economy concepts strengthens market resilience and consumer appeal.

Rising Adoption of Digital Technologies to Enhance Material Development and Performance

Digital tools, including simulation, artificial intelligence, and data analytics, transform how energy efficient materials are designed and optimized. The Energy Efficient Materials market benefits from faster development cycles and improved material properties driven by predictive modeling. It enables manufacturers to tailor materials precisely to application needs, reducing trial-and-error processes. Digital twins and real-time monitoring contribute to better quality control and performance validation. This technological trend reduces costs and accelerates innovation within the sector. It fosters a more agile and responsive market environment that meets evolving industry demands.

Market Challenges Analysis

High Initial Costs and Complex Manufacturing Processes Limit Adoption of Energy Efficient Materials

The Energy Efficient Materials market faces challenges related to the high upfront costs associated with advanced materials and their production techniques. Many energy-efficient materials require specialized raw materials and manufacturing processes that increase expenses compared to conventional alternatives. It creates barriers for small and medium-sized enterprises and cost-sensitive projects, limiting widespread adoption. Manufacturers must balance quality and performance with cost efficiency to remain competitive. The complexity of scaling production while maintaining consistency further complicates market expansion. These factors slow down integration in industries focused on short-term financial returns. Overcoming cost-related hurdles remains critical for broader market penetration.

Lack of Standardization and Limited Awareness Hinder Market Growth and Product Acceptance

The absence of universally accepted standards and certifications for energy efficient materials poses a significant challenge within the market. It leads to confusion among end-users and reduces confidence in product performance claims. Variability in testing methods and performance benchmarks limits comparability across different materials and suppliers. The Energy Efficient Materials market also suffers from limited awareness among some stakeholders regarding the long-term benefits and potential savings. It requires targeted education and outreach to improve understanding and drive demand. Without clear regulatory frameworks and consistent quality assurance, adoption rates may remain subdued. Addressing these challenges is essential to unlock the full market potential.

Market Opportunities

Expansion into Emerging Markets with Growing Infrastructure and Sustainability Initiatives

Emerging economies present significant opportunities for the Energy Efficient Materials market due to rapid urbanization and increasing investments in sustainable infrastructure. Governments in these regions prioritize energy efficiency to manage rising energy demand and reduce environmental impact. It creates a strong demand for cost-effective and high-performance materials suitable for new construction and retrofitting projects. Expanding middle-class populations further drive residential and commercial building activities, increasing market penetration potential. Companies that tailor their products to meet local regulations and affordability can capture substantial growth. Strategic partnerships and localized manufacturing may enhance competitiveness in these markets. The rising focus on green buildings offers a platform for accelerated adoption of energy efficient materials.

Advancements in Research and Development Unlock New Applications and Material Innovations

Ongoing innovation in material science offers promising opportunities for the Energy Efficient Materials market to diversify its applications across various industries. Breakthroughs in nanotechnology, bio-based composites, and phase change materials enable the creation of products with superior energy-saving properties. It allows manufacturers to target sectors such as automotive, electronics, and aerospace, expanding beyond traditional construction uses. The market benefits from developing lightweight, durable, and multifunctional materials that address specific energy efficiency challenges. Collaborations between research institutions and industry players accelerate product development and commercialization. Leveraging cutting-edge technology enhances competitiveness and drives sustained market growth.

Market Segmentation Analysis:

By Product Type:

Fiberglass and mineral wool dominate due to their excellent thermal insulation properties and cost-effectiveness. Cellulose gains traction for its eco-friendly nature, appealing to sustainability-focused projects. Spray foam, expanded polystyrene (EPS), and extruded polystyrene (XPS) serve specific insulation needs in construction and industrial sectors, offering superior energy retention and moisture resistance. Other materials like polyisocyanurate and polyurethane address specialized requirements with high-performance thermal barriers. The variety in product types enables the market to cater to a wide range of efficiency and durability demands.

- For instance, Dow Inc.’s phase change materials achieved thermal energy storage capacity of 120 kJ/kg, enhancing thermal regulation in electronic devices.

By End User:

The building and construction sector remains the largest consumer within the Energy Efficient Materials market. Residential, commercial, and industrial buildings increasingly adopt energy-efficient solutions to reduce operational costs and meet regulatory standards. The automotive and transportation segment exhibits growing demand for lightweight and thermally efficient materials to improve fuel economy and reduce emissions. Energy and utilities leverage these materials to enhance infrastructure efficiency and reliability. Consumer electronics also contribute to market growth by incorporating energy-saving materials to manage heat and improve device longevity. Other sectors, including pharmaceuticals and oil & gas, apply energy efficient materials to optimize energy consumption and maintain regulatory compliance.

- For instance, BASF reported that the production cost of its advanced insulation materials is up to 25% higher than traditional foams, impacting pricing strategies for smaller manufacturers.

By Distribution Channel:

Segment splits into online and offline channels, each serving different customer preferences and market dynamics. Offline distribution remains dominant due to established supply chains, direct customer relationships, and the need for technical consultation, especially in construction and industrial applications. It supports bulk purchases and complex project requirements through specialized vendors and distributors. Online channels gain importance with increasing digitalization, offering convenience and wider accessibility to smaller customers and emerging markets. It allows manufacturers to expand their reach and provide detailed product information, facilitating informed purchase decisions. Both channels complement each other to enhance market penetration and customer engagement.

Segments:

Based on Product Type:

- Fiberglass

- Mineral wool

- Cellulose

- Spray foam

- Expanded polystyrene (EPS)

- Extruded polystyrene (XPS)

- Others (polyisocyanurate, Polyurethane, etc.)

Based on End user:

- Building & construction

- Residential

- Commercial

- Industrial

- Automotive & transportation

- Energy & utilities

- Consumer electronics

- Others (pharmaceutical, oil & gas, etc.)

Based on Distribution Channel:

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds a commanding share of approximately 28% in the Energy Efficient Materials market, driven by strong regulatory frameworks and widespread adoption across construction, automotive, and energy sectors. The United States and Canada lead the region due to stringent energy codes and government incentives encouraging energy efficiency in residential and commercial buildings. Market participants benefit from advanced research facilities and established supply chains that foster innovation in material development. The automotive industry’s transition to lightweight and energy-saving materials further propels growth. Increasing awareness among consumers about energy costs and environmental impact also stimulates demand. Continuous investments in smart infrastructure projects sustain market momentum in this region.

Europe

Europe accounts for roughly 26% of the global Energy Efficient Materials market, supported by progressive environmental policies and strong emphasis on green building certifications such as BREEAM and LEED. The European Union’s focus on achieving carbon neutrality by 2050 drives adoption across member countries. Germany, France, and the UK serve as key markets due to their robust construction industries and technological advancements. The region exhibits a growing preference for recyclable and bio-based materials aligned with circular economy principles. Energy-efficient retrofitting of aging infrastructure presents ongoing opportunities. Europe’s well-established manufacturing base and R&D capabilities support continuous innovation and product diversification.

Asia Pacific

The Asia Pacific region leads with an estimated 32% market share, fueled by rapid urbanization, infrastructure development, and expanding industrial activities. Countries such as China, India, Japan, and South Korea invest heavily in sustainable construction and energy-efficient manufacturing processes. Rising population and expanding middle class drive demand for residential and commercial buildings incorporating energy-saving materials. Government initiatives focused on reducing carbon emissions and improving energy security boost market growth. The region also witnesses increased adoption of lightweight materials in automotive and electronics sectors. Growth in digital infrastructure and smart city projects further enhances market potential. Asia Pacific presents substantial opportunities for manufacturers targeting emerging economies.

Latin America, Middle East and Africa

The Rest of the World segment, including Latin America, Middle East, and Africa, holds around 14% of the Energy Efficient Materials market. The region demonstrates growing interest in sustainable building practices and energy conservation driven by rising energy costs and environmental concerns. Brazil, South Africa, and the Gulf countries emerge as important markets due to investments in infrastructure modernization and renewable energy projects. Challenges such as limited awareness and less stringent regulations slow penetration but create room for growth through targeted initiatives. Increasing international collaborations and technology transfer support market expansion. The RoW region shows promising prospects for energy efficient materials driven by economic development and urban growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Schneider Electric

- ArcelorMittal

- Rockwool International

- BASF

- Owens Corning

- Johnson Controls

- LG Chem

- Saint-Gobain

- Dow Inc.

- Thermo Fisher Scientific

- 3M

- Kingspan Group

- Nippon Steel

- Knauf Insulation

- Alcoa

Competitive Analysis

Key players in the Energy Efficient Materials market include Rockwool International, Owens Corning, Kingspan Group, Saint-Gobain, BASF, Dow Inc., Johnson Controls, and Knauf Insulation. These companies maintain competitive advantages through continuous innovation, expanding product portfolios, and investing in advanced manufacturing technologies. They focus on developing materials with improved thermal performance, sustainability, and cost-effectiveness to meet diverse industry needs. Strategic collaborations and acquisitions enable them to strengthen their global footprint and access emerging markets. Leading players emphasize research and development to create multifunctional and smart materials that enhance energy efficiency across applications. Additionally, they invest in sustainability initiatives aligned with global environmental regulations, appealing to eco-conscious consumers and businesses. Strong distribution networks and customer support systems further differentiate these companies, ensuring timely delivery and technical assistance. By prioritizing quality, compliance, and innovation, these market leaders successfully address evolving regulatory demands and end-user preferences. Their aggressive marketing strategies and partnerships with construction, automotive, and energy sectors bolster market penetration. Overall, the competitive landscape remains dynamic, driven by technological advancement and shifting market requirements, with these companies positioned to capitalize on future growth opportunities in the Energy Efficient Materials market.

Recent Developments

- In February 2025, Schneider Electric reported strong sustainability milestones in 2025, including exceeding its goal of training 1 million people in energy management worldwide as part of its Schneider Sustainability Impact program. The program operates in over 60 countries.

- In February 2025, at ELECRAMA 2025 in New Delhi, Schneider Electric showcased advanced energy management and automation technologies advancing India’s energy transition and industrial digitization. The company emphasized sustainability, energy efficiency, and digital transformation.

- In 2025, LG Chem unveiled a breakthrough precursor-free cathode technology for batteries, which reduces development time by about 40% and enhances environmental sustainability by cutting chemical waste and CO2 emissions. Production of these cathodes is planned to start in the first half of 2025.

- In May 2024, Knauf Insulation, Inc., a leading, family-owned global manufacturer of fiberglass insulation, today announced the launch of its new HVAC fiberglass insulation product line, Knauf Performance+. This product line is the first of its kind to be CERTIFIED asthma & allergy friendly® and the only HVAC fiberglass insulation line that is formaldehyde-free.

Market Concentration & Characteristics

The Energy Efficient Materials market exhibits a moderately concentrated competitive landscape dominated by several key global players who command significant market shares through strong brand presence and extensive product portfolios. It features a mix of established multinational corporations and specialized regional manufacturers, fostering innovation and diversity in material offerings. Market leaders focus heavily on research and development to enhance material performance, sustainability, and cost efficiency, responding to stringent regulatory requirements and evolving customer demands. The industry’s characteristics include high capital intensity and the need for advanced manufacturing capabilities, which pose barriers to entry for smaller firms. Despite this, niche players find opportunities by catering to specific applications or regional needs with tailored solutions. The market also displays dynamic collaboration trends, including partnerships and acquisitions, which help companies expand their technological capabilities and geographic reach. It relies heavily on evolving regulatory frameworks and sustainability goals to drive product development and adoption. Customer preference shifts towards eco-friendly, recyclable, and multifunctional materials shape product innovation. The distribution model balances between traditional offline channels favored for bulk sales and increasing online platforms providing accessibility and detailed product information. Overall, the market combines innovation, regulatory influence, and strategic competition to drive steady growth while maintaining moderate concentration among leading players.

Report Coverage

The research report offers an in-depth analysis based on Product Type, End User, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Energy Efficient Materials market will continue to grow driven by stricter environmental regulations worldwide.

- Increasing urbanization and infrastructure development will expand demand for energy-efficient construction materials.

- Technological innovation will focus on developing smarter and multifunctional materials with improved energy performance.

- Lightweight materials will gain prominence, especially in automotive and aerospace industries, to enhance fuel efficiency.

- Circular economy principles will influence material design, emphasizing recyclability and sustainability.

- Rising consumer awareness about energy costs and environmental impact will boost market adoption.

- Emerging economies will present new growth opportunities due to expanding industrial and residential sectors.

- Digital technologies like AI and simulation will accelerate material research and optimize production processes.

- Collaboration between industry players and research institutions will drive faster commercialization of advanced materials.

- The market will face ongoing challenges related to cost reduction and standardization, requiring innovative solutions to maintain momentum.