Market Overview

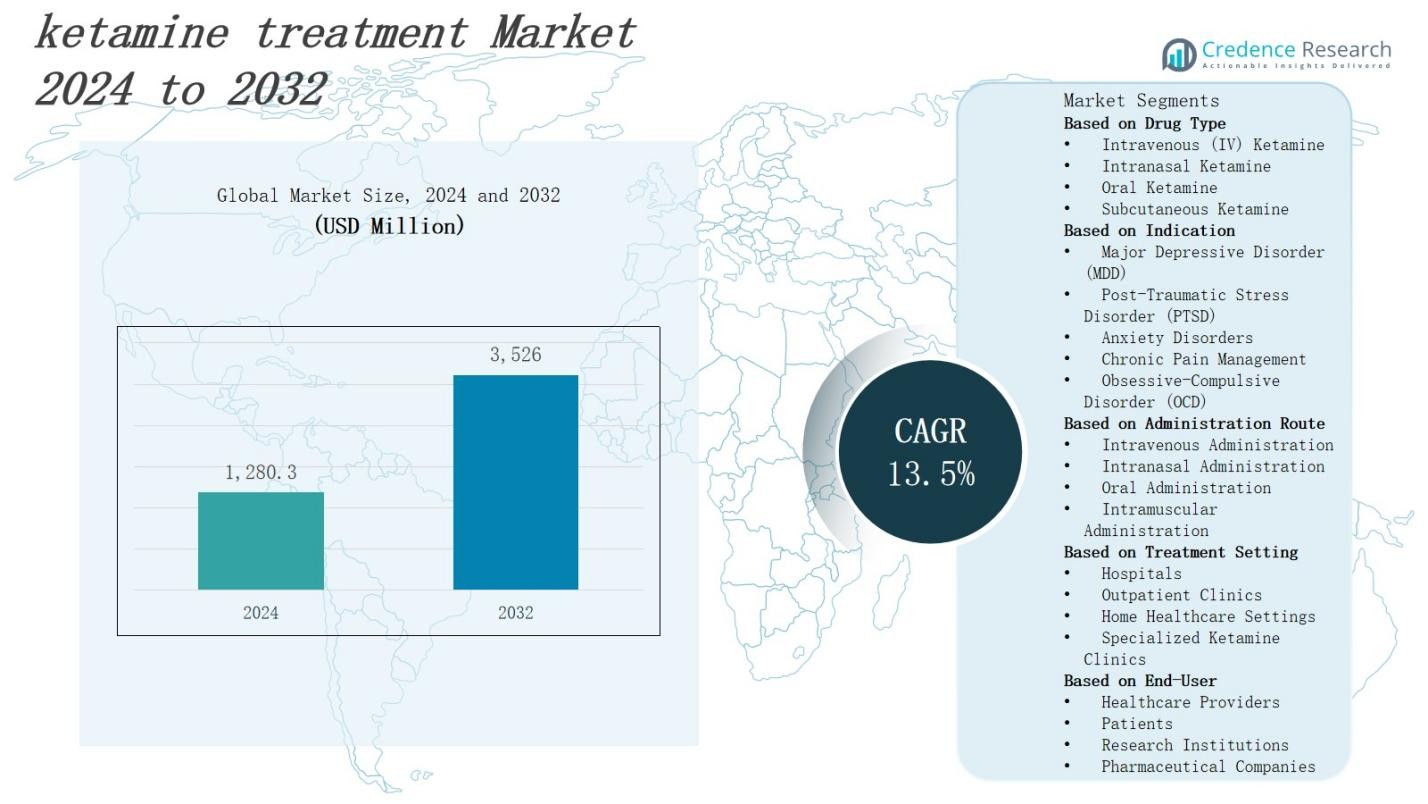

The ketamine treatment market is projected to grow from USD 1,280.3 million in 2024 to USD 3,526 million by 2032, registering a CAGR of 13.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ketamine Treatment Market Size 2024 |

USD 1,280.3 Million |

| Ketamine Treatment Market, CAGR |

13.5% |

| Ketamine Treatment Market Size 2032 |

USD 3,526 Million |

Market growth in the ketamine treatment sector is driven by the rising prevalence of depression, anxiety disorders, and treatment-resistant mental health conditions, coupled with increasing acceptance of ketamine-assisted therapy among healthcare providers. Advancements in delivery methods, such as nasal sprays and infusion therapies, are enhancing patient accessibility and treatment efficacy. Expanding research into ketamine’s therapeutic potential beyond psychiatric applications, including chronic pain management, is broadening its market scope. Growing investments in mental health infrastructure, supportive regulatory frameworks, and the entry of specialized clinics are further accelerating adoption, while heightened public awareness continues to strengthen demand across global healthcare markets.

The ketamine treatment market spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with North America holding the largest share due to advanced infrastructure and widespread clinical adoption. Europe follows with strong regulatory frameworks and mental health initiatives, while Asia-Pacific shows rapid growth from rising healthcare investments. Latin America sees expanding private psychiatric services, and the Middle East & Africa benefit from urban-centered adoption. Key players include Better U, Klarisana, Numinus Wellness, Nushama, Interpersonal Psychiatry, Journey Clinical, Mindbloom, Save Minds, Ember Health, Nue Life Health, and Field Trip Health.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The ketamine treatment market is projected to grow from USD 1,280.3 million in 2024 to USD 3,526 million by 2032, registering a CAGR of 13.5% during the forecast period.

- Rising prevalence of depression, anxiety disorders, PTSD, and treatment-resistant cases is increasing demand, supported by growing acceptance of ketamine-assisted therapy among healthcare providers.

- Advancements in delivery methods, including nasal sprays, oral formulations, and intravenous infusions, are improving accessibility, treatment compliance, and clinical outcomes.

- Expansion into chronic pain management, migraines, and neurological disorders is broadening therapeutic applications and attracting a wider patient base.

- Regulatory scrutiny, licensing challenges, and limited insurance coverage remain significant barriers to market expansion across multiple regions.

- North America holds 42% of the market, Europe 28%, Asia-Pacific 20%, Latin America 6%, and the Middle East & Africa 4%, reflecting diverse adoption rates and healthcare infrastructure levels.

- Key players include Better U, Klarisana, Numinus Wellness, Nushama, Interpersonal Psychiatry, Journey Clinical, Mindbloom, Save Minds, Ember Health, Nue Life Health, and Field Trip Health.

Market Drivers

Rising Prevalence of Mental Health Disorders

The ketamine treatment market is gaining traction due to the increasing global burden of depression, anxiety, and post-traumatic stress disorder, particularly among populations resistant to conventional antidepressants. Growing awareness about treatment alternatives is driving patient interest in ketamine therapy. It is viewed as a viable solution for individuals requiring rapid relief from severe symptoms. Healthcare providers are expanding service offerings to include ketamine-based options, supported by favorable clinical outcomes and patient satisfaction levels.

Advancements in Drug Delivery Methods

Innovations in drug delivery, such as nasal sprays, oral formulations, and refined intravenous infusion protocols, are expanding accessibility and improving treatment compliance. The ketamine treatment market benefits from technology that allows precise dosing and minimizes side effects. It supports faster onset of therapeutic benefits, making it an attractive choice for both patients and practitioners. Regulatory approvals for new administration formats are encouraging wider adoption, improving scalability in clinical and outpatient settings.

- For instance, Johnson & Johnson’s FDA-approved esketamine nasal spray Spravato provides rapid relief for treatment-resistant depression by delivering precise doses through a non-invasive nasal spray, allowing for quicker symptom onset and minimized side effects.

Expansion Beyond Psychiatric Applications

Clinical research is uncovering ketamine’s potential in treating chronic pain, migraines, and certain neurological disorders. This diversification of therapeutic use strengthens the ketamine treatment market by attracting a broader patient base and increasing long-term demand. It provides healthcare facilities with opportunities to integrate ketamine into multidisciplinary care programs. Positive trial results and ongoing studies are enhancing credibility, driving further investment in specialized treatment centers equipped to deliver multiple indications.

Growing Investment and Supportive Infrastructure

Rising private and institutional investment in mental health infrastructure is creating a strong foundation for ketamine therapy expansion. The ketamine treatment market is supported by dedicated clinics, trained professionals, and integrated telehealth services. Supportive policies and updated treatment guidelines are improving operational viability. It fosters greater patient outreach, reduces access barriers, and encourages new entrants into the sector. Strategic partnerships among pharmaceutical companies and clinics are also accelerating service availability across regions.

- For instance, Athena Behavioural Health secured ₹10 crore in 2025 to scale its mental health and digital care infrastructure nationwide, improving access and telehealth integration.

Market Trends

Integration of Ketamine Therapy into Mainstream Mental Health Care

The ketamine treatment market is witnessing a steady shift toward inclusion in standard mental health protocols, driven by its rapid antidepressant effects. Hospitals and psychiatric clinics are incorporating ketamine therapy into treatment plans for patients unresponsive to traditional medications. It is gaining clinical acceptance through evidence-based outcomes and peer-reviewed studies. This integration is fostering broader insurance coverage, encouraging patient participation, and enhancing trust in ketamine as a viable medical intervention for mental health.

Emergence of Specialized Ketamine Clinics and Telemedicine Platforms

A growing number of dedicated ketamine therapy clinics are being established, offering tailored treatment plans and patient monitoring. The ketamine treatment market benefits from telemedicine platforms that provide remote consultations, follow-up care, and symptom tracking. It improves access for patients in underserved or rural areas while maintaining treatment quality. These hybrid care models are enabling scalability, optimizing resource utilization, and fostering strong patient-provider engagement in both physical and digital environments.

- For instance, the Sterling Institute of Neuropsychiatry & Behavioral Medicine offers intranasal ketamine therapy through both in-person and telehealth services across multiple states, providing expert clinician care and secure remote consultations globally.

Expansion of Research into Novel Therapeutic Indications

Clinical trials are exploring ketamine’s potential for neurological conditions, substance use disorders, and chronic pain syndromes. The ketamine treatment market is diversifying as these studies reveal promising results, expanding its relevance beyond psychiatric care. It supports long-term market sustainability by attracting investment and fostering pharmaceutical innovation. Multidisciplinary research collaborations are accelerating the development of new dosing regimens, delivery systems, and combination therapies, strengthening ketamine’s position in modern medicine.

- For instance, Pharmather is advancing a ketamine-based treatment for Parkinson’s disease, with FDA approval decision expected in August 2025, focusing on symptom relief such as tremors and involuntary movements under the brand name Ketarx.

Focus on Personalized and Precision-Based Treatment Protocols

Healthcare providers are moving toward personalized ketamine therapy, tailoring dosages, frequency, and delivery methods to individual patient profiles. The ketamine treatment market is benefiting from advances in genetic testing, biomarker analysis, and AI-driven treatment optimization. It enables clinicians to predict patient response more accurately, improving outcomes and reducing adverse effects. This trend aligns with the broader shift in healthcare toward patient-centric approaches, ensuring higher satisfaction and better long-term adherence to therapy plans.

Market Challenges Analysis

Regulatory and Compliance Barriers

The ketamine treatment market faces stringent regulatory scrutiny due to ketamine’s classification as a controlled substance in many countries. It creates challenges for clinics and healthcare providers in securing necessary licenses and ensuring compliance with storage, handling, and administration protocols. Varying regional regulations complicate market expansion, particularly for cross-border operations. Limited inclusion in public healthcare systems and insurance plans restricts affordability and patient access. These regulatory constraints slow down adoption rates despite growing clinical evidence of ketamine’s therapeutic potential.

Concerns Over Safety, Efficacy, and Misuse Potential

Public and medical community concerns regarding the long-term safety of ketamine therapy present a significant challenge. The ketamine treatment market must address risks of dissociation, abuse, and dependency through strict patient screening and monitoring. It is critical to establish robust clinical guidelines and standardized treatment protocols to enhance safety and build trust. Limited large-scale longitudinal studies create uncertainty about long-term outcomes. These factors contribute to cautious adoption, especially in regions with heightened substance abuse concerns.

Market Opportunities

Expansion into Emerging Markets and Untapped Regions

The ketamine treatment market holds significant potential in emerging economies where mental health infrastructure is developing rapidly. Rising awareness about innovative psychiatric treatments, combined with increasing healthcare expenditure, creates fertile ground for adoption. It can benefit from partnerships with local healthcare providers to establish clinics and training programs. Government mental health initiatives and NGO collaborations can further support outreach. These regions offer opportunities to introduce affordable delivery models tailored to local economic conditions, expanding market penetration.

Innovation in Formulations and Delivery Technologies

Ongoing advancements in pharmaceutical formulations and administration methods are opening new revenue streams for the ketamine treatment market. It can leverage intranasal sprays, oral tablets, and controlled-release systems to improve patient convenience and adherence. Research into combination therapies and personalized protocols enhances efficacy and broadens the range of treatable conditions. Collaborations between biotech firms and healthcare institutions are accelerating innovation. These developments create opportunities for differentiation and long-term growth in a competitive therapeutic landscape.

Market Segmentation Analysis:

By Drug Type

The ketamine treatment market encompasses intravenous (IV) ketamine, intranasal ketamine, oral ketamine, and subcutaneous ketamine. IV ketamine remains the most widely used form due to its rapid onset and proven efficacy in treatment-resistant depression. Intranasal formulations, supported by regulatory approvals, are gaining traction for their convenience and non-invasive nature. Oral and subcutaneous forms are emerging as alternatives for maintenance therapy. It benefits from ongoing formulation research aimed at enhancing bioavailability and reducing side effects.

- For instance, Johnson & Johnson’s Spravato (esketamine) nasal spray is FDA-approved for treatment-resistant depression and has shown rapid symptom improvement in clinical trials, making it a groundbreaking non-invasive option.

By Indication

Major depressive disorder (MDD) leads the market due to the urgent need for rapid-acting therapies in severe cases. The ketamine treatment market also serves patients with post-traumatic stress disorder (PTSD), anxiety disorders, chronic pain, and obsessive-compulsive disorder (OCD). It is experiencing growth from expanded clinical trials supporting efficacy across these conditions. Chronic pain management is becoming a key application, attracting multidisciplinary treatment centers. Broader adoption is expected as evidence solidifies for psychiatric and pain-related uses.

By Administration Route

Intravenous administration dominates due to its predictable dosing and immediate therapeutic response. Intranasal administration is expanding quickly, driven by ease of use in outpatient settings. Oral administration provides an accessible option for long-term maintenance, while intramuscular administration is used selectively for targeted cases. The ketamine treatment market benefits from innovations in delivery methods that prioritize patient comfort, optimize clinical efficiency, and expand reach to diverse healthcare environments. It continues to evolve with advances in administration technology.

- For instance, Mindbloom, Inc. launched in 2023 its Mastermind Series, an expert-led psychedelic therapy program integrating ketamine treatment with specialized mental health education targeting burnout and heartbreak.

Segments:

Based on Drug Type

- Intravenous (IV) Ketamine

- Intranasal Ketamine

- Oral Ketamine

- Subcutaneous Ketamine

Based on Indication

- Major Depressive Disorder (MDD)

- Post-Traumatic Stress Disorder (PTSD)

- Anxiety Disorders

- Chronic Pain Management

- Obsessive-Compulsive Disorder (OCD)

Based on Administration Route

- Intravenous Administration

- Intranasal Administration

- Oral Administration

- Intramuscular Administration

Based on Treatment Setting

- Hospitals

- Outpatient Clinics

- Home Healthcare Settings

- Specialized Ketamine Clinics

Based on End-User

- Healthcare Providers

- Patients

- Research Institutions

- Pharmaceutical Companies

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the largest share of the ketamine treatment market at 42%, supported by advanced healthcare infrastructure, high awareness of mental health therapies, and widespread availability of specialized clinics. It benefits from favorable regulatory environments in the United States and Canada, enabling easier integration of ketamine therapy into psychiatric and pain management practices. High prevalence of depression, PTSD, and anxiety disorders fuels demand. Strong insurance coverage and ongoing clinical trials further drive adoption. Strategic collaborations between healthcare providers and pharmaceutical companies strengthen service delivery across urban and rural areas.

Europe

Europe accounts for 28% of the ketamine treatment market, driven by rising acceptance of ketamine-based therapies and a growing focus on mental health awareness. It is supported by robust healthcare systems and strict clinical guidelines that ensure safe administration. Countries such as the United Kingdom, Germany, and France lead adoption, with specialized clinics expanding across the region. Research initiatives exploring ketamine’s broader therapeutic applications attract funding. Public health campaigns and government-backed mental wellness programs contribute to increasing demand.

Asia-Pacific

Asia-Pacific holds 20% of the ketamine treatment market, fueled by growing mental health challenges and increasing healthcare investments. It is experiencing rapid infrastructure development in countries like Australia, Japan, China, and India, where awareness of innovative psychiatric treatments is rising. Expanding private healthcare networks and telemedicine platforms improve access in urban and semi-urban regions. Government initiatives addressing mental health stigma encourage adoption. Rising middle-class populations and healthcare spending create strong growth potential for ketamine therapy services.

Latin America

Latin America represents 6% of the ketamine treatment market, with Brazil, Mexico, and Argentina leading adoption. It benefits from the expansion of private psychiatric care facilities and growing awareness of treatment-resistant depression. Limited public healthcare coverage for ketamine therapy remains a challenge, but private sector initiatives are filling the gap. Partnerships with global ketamine providers are introducing standardized treatment protocols. Expanding mental health advocacy and NGO-led outreach programs are helping overcome stigma and increase accessibility.

Middle East & Africa

The Middle East & Africa region accounts for 4% of the ketamine treatment market, driven by a gradual rise in mental health awareness and private healthcare investments. It sees adoption primarily in urban centers of Gulf countries and South Africa. Limited specialist availability and infrastructure gaps slow broader expansion. Growing medical tourism, especially in the UAE, presents opportunities for ketamine therapy. Training programs for healthcare professionals are emerging to support safe and effective treatment delivery.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Better U (U.S.)

- Klarisana (U.S.)

- Numinus Wellness (Canada)

- Nushama (U.S.)

- Interpersonal Psychiatry (U.S.)

- Journey Clinical (U.S.)

- Mindbloom (U.S.)

- Save Minds (U.S.)

- Ember Health (U.S.)

- Nue Life Health (U.S.)

- Field Trip Health (Canada)

Competitive Analysis

The ketamine treatment market is highly competitive, with a mix of specialized clinics, wellness centers, and integrated healthcare providers focusing on mental health and pain management. Leading players include Better U, Klarisana, Numinus Wellness, Nushama, Interpersonal Psychiatry, Journey Clinical, Mindbloom, Save Minds, Ember Health, Nue Life Health, and Field Trip Health. It is characterized by rapid service expansion, innovation in treatment protocols, and investment in patient-centric care models. Companies are emphasizing clinical expertise, safety standards, and personalized therapy plans to differentiate offerings. Strategic partnerships with research institutions and pharmaceutical companies are enabling access to advanced formulations and delivery systems. Marketing efforts target both patients and referring healthcare professionals, enhancing brand visibility. The competitive landscape is also shaped by regional presence, with North America hosting the largest concentration of providers, while international expansion remains a key growth focus. Players are leveraging technology, such as telemedicine platforms, to extend reach and improve patient engagement.

Recent Developments

- On June 23, 2025, NRx Pharmaceuticals advanced NRX-100 (a preservative-free IV ketamine) through the FDA’s fast-track review for treating suicidal depression and PTSD, following the submission of an Abbreviated New Drug Application earlier that month.

- In May 2025, PharmaTher Holdings introduced the KetaVault™ portal to assist ketamine therapy providers and launched innovative delivery systems, including microneedle patches and on-body pumps for sustained ketamine release.

- In January 2025, Hope Therapeutics revealed plans to acquire Kadima Neuropsychiatry Institute, making it the flagship for their expanding network of ketamine-focused psychiatric clinics.

- In February 2024, Innerwell (KBS, Inc.) entered in-network agreements with four major California insurers and two in New York to improve access to ketamine and mental health services.

Market Concentration & Characteristics

The ketamine treatment market is moderately fragmented, with a mix of specialized clinics, wellness centers, and integrated healthcare providers competing for market share. It features both established players with strong regional networks and emerging providers targeting niche patient segments. Competition is driven by service quality, clinical expertise, delivery methods, and patient experience. Providers focus on personalized treatment protocols, regulatory compliance, and integration of telemedicine to extend reach. Strategic partnerships between clinics, pharmaceutical companies, and research institutions support innovation and expand service capabilities. Market growth is influenced by regional regulatory frameworks, infrastructure maturity, and mental health awareness levels. While North America dominates, other regions are gaining traction through targeted investments and expanding healthcare accessibility.

Report Coverage

The research report offers an in-depth analysis based on Drug Type, Indication, Administartion Rule, Treatmnet Setting, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Rising awareness will drive higher demand for ketamine therapy in mental health care.

- Broader adoption will occur across psychiatric disorders and chronic pain management treatment settings.

- Growth in specialized ketamine clinics will improve access in urban and semi-urban regions.

- Integration of telemedicine will expand patient monitoring capabilities and improve treatment accessibility globally.

- Development of innovative formulations and delivery systems will enhance safety and patient compliance.

- Standardized clinical guidelines will ensure consistent treatment quality across different healthcare service providers.

- Ongoing research will identify new therapeutic uses beyond depression and anxiety-related disorders.

- Strategic partnerships between providers and pharmaceutical companies will accelerate innovation and adoption.

- Awareness initiatives will help reduce stigma and encourage earlier treatment for eligible patients.

- Global market expansion will be supported by investment in advanced mental health infrastructure.