Market Overview

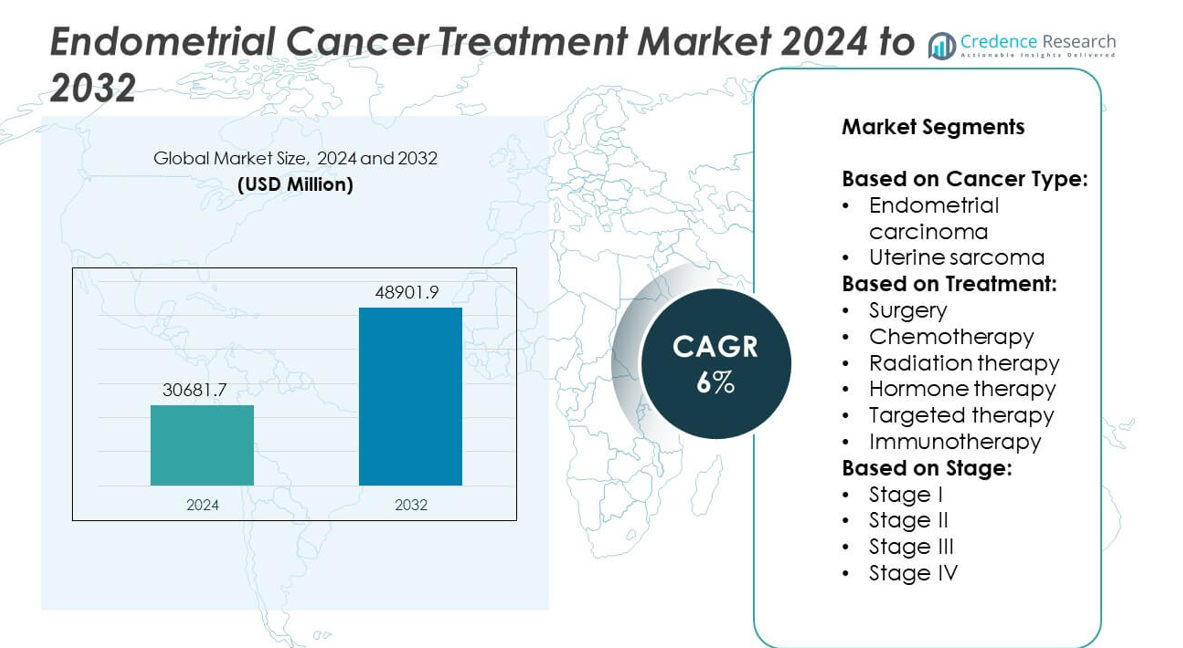

The Endometrial Cancer Treatment Market size was valued at USD 30,681.7 million in 2024 and is anticipated to reach USD 48,901.9 million by 2032, growing at a compound annual growth rate (CAGR) of 6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Endometrial Cancer Treatment Market Size 2024 |

USD 30,681.7 million |

| Endometrial Cancer Treatment Market , CAGR |

6% |

| Endometrial Cancer Treatment Market Size 2032 |

USD 48,901.9 million |

The Endometrial Cancer Treatment market grows due to rising incidence rates and increased awareness of early diagnosis benefits. Advances in targeted therapies, immunotherapy, and personalized medicine improve treatment effectiveness and patient outcomes. Minimally invasive surgical techniques gain traction for their precision and faster recovery times. Expansion of healthcare infrastructure and supportive government initiatives enhance treatment accessibility worldwide. Innovations in diagnostic technologies enable earlier detection, driving demand for comprehensive care. Patient-centered approaches focusing on quality of life further influence treatment choices, collectively propelling market growth and encouraging ongoing research and development efforts.

The Endometrial Cancer Treatment market shows strong growth across North America, Europe, and Asia-Pacific, driven by advanced healthcare systems and increasing awareness. North America leads with widespread adoption of innovative therapies and robust research infrastructure. Europe follows closely, emphasizing personalized medicine and early diagnosis. Asia-Pacific experiences rapid expansion due to improving healthcare access and rising cancer prevalence. Key players in this market include Pfizer Inc., AstraZeneca PLC, Merck & Co., Inc., and Novartis AG. These companies focus on developing targeted therapies and immunotherapies, investing heavily in research and clinical trials to address unmet needs and improve patient outcomes globally.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Endometrial Cancer Treatment market was valued at USD 30,681.7 million in 2024 and is expected to reach USD 48,901.9 million by 2032, growing at a CAGR of 6% during the forecast period.

- Increasing incidence of endometrial cancer and growing awareness about early diagnosis drive demand for effective treatment options globally.

- The market trends highlight a shift towards targeted therapies, immunotherapy, and minimally invasive surgical techniques, improving treatment precision and patient recovery.

- Leading pharmaceutical companies like Pfizer Inc., AstraZeneca PLC, and Merck & Co., Inc. invest heavily in research and development to introduce innovative therapies.

- High costs of advanced treatments and limited access in emerging economies restrict widespread adoption and create challenges for market growth.

- North America and Europe dominate the market due to advanced healthcare infrastructure, while Asia-Pacific shows rapid growth fueled by rising healthcare investments and increasing cancer prevalence.

- Regulatory support and government initiatives promoting cancer awareness and early detection contribute positively but vary significantly across regions, impacting market penetration.

Market Drivers

Rising Prevalence of Endometrial Cancer and Increasing Awareness Among Women

The increasing incidence of endometrial cancer worldwide significantly drives the market growth. Improvements in diagnostic capabilities and screening programs contribute to early detection, allowing more patients to seek treatment. Heightened awareness campaigns promote understanding of risk factors such as obesity, hormonal imbalances, and aging, encouraging timely medical consultation. These factors collectively expand the patient pool requiring therapeutic interventions. Healthcare providers respond by enhancing treatment accessibility and options. This growing patient base directly supports the expansion of the Endometrial Cancer Treatment market.

- For instance, the National Cancer Institute’s Cancer Screening program conducted over 1.5 million screenings annually in the U.S., enabling earlier diagnosis and intervention, which supports the expansion of the Endometrial Cancer Treatment market.

Advancements in Therapeutic Options and Personalized Medicine Adoption

Innovations in targeted therapies, immunotherapies, and hormone treatments improve clinical outcomes and patient quality of life. It benefits from the integration of personalized medicine, which tailors treatment protocols based on genetic and molecular profiling. These advancements increase the efficacy and reduce adverse effects, making therapies more acceptable to patients and clinicians. Pharmaceutical companies continuously invest in research and development to introduce novel drugs and combination therapies. This pipeline enrichment fuels market growth by offering diverse and effective treatment alternatives. Increasing availability of advanced treatment options attracts greater adoption in clinical practice.

- For instance, Siemens Healthineers deployed more than 2,000 advanced radiation therapy systems worldwide in the last five years, enhancing treatment access and quality. These efforts promote better treatment adoption and adherence, contributing positively to the market trajectory.

Expansion of Healthcare Infrastructure and Supportive Government Initiatives

Growing investments in healthcare infrastructure facilitate the availability of specialized cancer treatment centers equipped with advanced technologies. It allows wider patient access to comprehensive care, including surgery, chemotherapy, and radiation therapy. Governments and regulatory bodies implement policies to improve cancer care standards and reimbursements, reducing financial burdens for patients. Public-private partnerships and funding for cancer research also bolster treatment development and dissemination. These efforts promote better treatment adoption and adherence, contributing positively to the market trajectory. The supportive environment accelerates the integration of new therapies into standard care.

Increasing Demand for Minimally Invasive and Patient-Centric Treatment Approaches

Patients and healthcare providers emphasize treatments that minimize side effects and recovery times, driving demand for minimally invasive surgical techniques and outpatient therapies. It encourages the use of laparoscopy, robotic-assisted surgeries, and targeted radiation therapy, which improve precision and reduce complications. Patient-centric approaches prioritize quality of life, symptom management, and tailored follow-up care, influencing treatment choices. Rising preference for outpatient procedures reduces hospital stays and healthcare costs. These trends align with the broader shift toward value-based care models. Consequently, the market experiences growth through adoption of innovative, patient-friendly treatment modalities.

Market Trends

Growth of Targeted Therapies and Immunotherapy in Treatment Protocols

The Endometrial Cancer Treatment market shows a significant shift toward targeted therapies and immunotherapy. These innovative approaches offer improved precision by attacking cancer cells specifically, reducing harm to healthy tissues. It benefits from advancements in molecular biology and genetic research, which identify biomarkers for personalized treatment. Clinicians increasingly adopt immune checkpoint inhibitors and monoclonal antibodies, enhancing patient outcomes. Pharmaceutical companies focus on developing drugs that leverage the body’s immune system to fight cancer. This trend reflects a broader movement in oncology toward less toxic and more effective treatment regimens. It drives demand for cutting-edge therapies and influences clinical guidelines.

- For instance, Intuitive Surgical’s da Vinci robotic system completed over 7 million minimally invasive procedures globally by 2023, significantly reducing patient recovery times. Rising preference for outpatient procedures reduces hospital stays and healthcare costs.

Integration of Minimally Invasive Surgical Techniques and Enhanced Recovery Protocols

Minimally invasive surgery gains prominence in endometrial cancer management due to its advantages in patient recovery and reduced complications. The Endometrial Cancer Treatment market experiences growth from widespread use of laparoscopy and robotic-assisted surgery. These techniques allow greater surgical precision, shorter hospital stays, and improved postoperative outcomes. Hospitals implement enhanced recovery after surgery (ERAS) protocols that optimize perioperative care and accelerate patient rehabilitation. This trend emphasizes patient comfort and reduces healthcare costs through efficient resource utilization. Surgeons continuously refine minimally invasive methods, supporting the shift away from traditional open surgeries. It strengthens the market by increasing the uptake of advanced surgical solutions.

- For instance, Guardant Health’s Guardant360 and Guardant Reveal, liquid biopsy tests have been used in over 150,000 cancer patients worldwide to detect tumor DNA, enabling earlier and less invasive diagnosis.

Expansion of Diagnostic Technologies and Early Detection Efforts

Early diagnosis remains crucial in improving survival rates and treatment success in endometrial cancer. The market benefits from innovations in diagnostic imaging, molecular testing, and liquid biopsies. These tools enable more accurate staging and risk assessment, guiding personalized treatment strategies. Healthcare providers focus on routine screening programs and awareness campaigns to promote early medical intervention. Enhanced diagnostics support timely decisions between surgical and nonsurgical options, improving patient prognosis. It encourages investment in technologies that detect cancer at initial stages, boosting demand for associated treatment services. This trend underlines the importance of integrated diagnostic and therapeutic approaches.

Increasing Emphasis on Patient-Centered Care and Quality of Life Improvements

The Endometrial Cancer Treatment market aligns with the growing emphasis on holistic patient care. Treatment plans increasingly consider not only survival but also physical, emotional, and social well-being. It incorporates supportive care services such as pain management, psychological counseling, and rehabilitation therapies. Patient-reported outcomes guide clinicians in selecting therapies that balance efficacy with minimal adverse effects. Telemedicine and digital health platforms facilitate ongoing monitoring and patient engagement beyond clinical settings. This trend reflects the healthcare industry’s broader focus on personalized, value-based care models. It influences treatment development and delivery, fostering improved patient satisfaction and adherence.

Market Challenges Analysis

High Treatment Costs and Limited Accessibility in Emerging Economies

The Endometrial Cancer Treatment market faces challenges related to the high costs of advanced therapies and diagnostic procedures. These expenses restrict access for patients in low- and middle-income regions, limiting market penetration. It encounters difficulties in affordability and reimbursement policies that vary significantly across countries. Healthcare infrastructure gaps in emerging economies further hinder the availability of specialized treatment centers. Patients often delay or forgo treatment due to financial constraints, impacting overall outcomes. Pharmaceutical companies and healthcare providers must address these barriers to expand reach and improve equity in care delivery. Cost containment strategies and government support remain critical to overcoming these challenges.

Complexity of Treatment Regimens and Resistance to Therapies

The management of endometrial cancer involves complex treatment protocols combining surgery, radiation, chemotherapy, and targeted therapies. The Endometrial Cancer Treatment market struggles with variability in patient responses and development of resistance to certain drugs. It complicates treatment decisions and may lead to relapse or progression in some cases. Limited biomarkers for predicting therapeutic success create uncertainty in personalized treatment planning. Clinicians require continuous updates on evolving guidelines and emerging therapies to optimize patient care. These challenges necessitate sustained research efforts to discover more effective and durable treatment options. Managing treatment complexity remains a significant hurdle for market growth and patient outcomes.

Market Opportunities

Expansion of Personalized Medicine and Precision Oncology Approaches

The Endometrial Cancer Treatment market presents significant opportunities through the advancement of personalized medicine and precision oncology. It can leverage genetic and molecular profiling to tailor therapies specifically to individual patient tumors. This approach enhances treatment effectiveness while minimizing adverse effects, leading to better patient outcomes and satisfaction. Continued research in biomarker discovery and targeted drug development expands the range of therapeutic options. Pharmaceutical companies investing in these areas stand to capture growing demand for customized treatments. It also encourages collaboration between diagnostic and pharmaceutical sectors to create integrated care solutions. Personalized medicine remains a key driver for innovation and market growth.

Increasing Adoption of Minimally Invasive Procedures and Digital Health Technologies

Minimally invasive surgical techniques and digital health solutions offer promising avenues for market expansion. The Endometrial Cancer Treatment market benefits from the rising use of robotic-assisted surgeries, which improve precision and reduce patient recovery times. Incorporation of telemedicine and remote patient monitoring enhances treatment adherence and follow-up care, especially in remote or underserved regions. It can harness digital platforms to improve patient education and engagement, thereby optimizing clinical outcomes. Growing acceptance of these technologies creates demand for new devices and software solutions tailored to cancer care. These advancements present opportunities to improve both the quality and accessibility of endometrial cancer treatments.

Market Segmentation Analysis:

By Cancer Type:

Endometrial carcinoma holds the largest share due to its higher prevalence compared to uterine sarcoma. Endometrial carcinoma’s relatively better prognosis and higher diagnosis rates drive demand for diverse treatment options. Uterine sarcoma, being rarer and more aggressive, requires specialized therapeutic approaches that contribute to a niche segment within the market. Understanding these distinctions helps healthcare providers tailor interventions effectively and influences market strategies.

- For instance, Merck & Co.’s immunotherapy drug Keytruda has been administered to over 50,000 cancer patients worldwide, showing promising results in managing advanced endometrial cancer. These treatment options expand the therapeutic arsenal, enabling personalized and more effective management of endometrial cancer.

By Treatment:

It covers surgery, chemotherapy, radiation therapy, hormone therapy, targeted therapy, and immunotherapy. Surgery remains the primary intervention, especially in early-stage endometrial cancer, due to its curative potential. Chemotherapy and radiation therapy complement surgical procedures by addressing residual disease or advanced cancer. Hormone therapy finds use particularly in hormone receptor-positive cases, offering a less toxic alternative for specific patient groups. Targeted therapy and immunotherapy represent rapidly growing segments, driven by advancements in molecular research and clinical trials demonstrating improved outcomes. These treatment options expand the therapeutic arsenal, enabling personalized and more effective management of endometrial cancer.

- For instance, hospitals using Varian Medical Systems’ advanced radiation therapy equipment reported treating over 25,000 early-stage endometrial cancer patients with improved precision and outcomes. Stage II and III involve more extensive disease, requiring multimodal treatment plans combining surgery with adjuvant therapies. Stage IV, representing metastatic cancer, demands aggressive systemic therapies and supportive care, influencing market demand for advanced treatment options.

By Stage:

It includes stages I through IV, reflecting the disease’s progression and treatment complexity. Stage I dominates due to higher detection rates at this early phase, where localized treatment achieves favorable survival rates. Stage II and III involve more extensive disease, requiring multimodal treatment plans combining surgery with adjuvant therapies. Stage IV, representing metastatic cancer, demands aggressive systemic therapies and supportive care, influencing market demand for advanced treatment options. Accurate staging guides clinicians in selecting appropriate therapies, impacting market trends and innovation focus.

Segments:

Based on Cancer Type:

- Endometrial carcinoma

- Uterine sarcoma

Based on Treatment:

- Surgery

- Chemotherapy

- Radiation therapy

- Hormone therapy

- Targeted therapy

- Immunotherapy

Based on Stage:

- Stage I

- Stage II

- Stage III

- Stage IV

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Endometrial Cancer Treatment market, accounting for approximately 38% of the global revenue. This dominant position results from a well-established healthcare infrastructure, high awareness levels, and widespread adoption of advanced treatment technologies. The presence of leading pharmaceutical companies and research institutions drives innovation in targeted therapies and immunotherapy. Comprehensive screening programs and early diagnosis further contribute to high patient volumes seeking treatment. Strong reimbursement frameworks and government support facilitate access to expensive therapies. The region also benefits from increasing patient preference for minimally invasive surgical techniques, enhancing treatment outcomes. These factors collectively sustain North America’s leadership in the market.

Europe

Europe commands around 28% of the Endometrial Cancer Treatment market. The region’s robust healthcare systems and growing emphasis on personalized medicine support steady market growth. Countries such as Germany, the United Kingdom, and France lead in adopting novel treatment modalities, including immunotherapy and hormone-based therapies. Public health initiatives focus on cancer awareness and early intervention, improving detection rates. Europe also experiences rising investments in oncology research and clinical trials that foster innovative therapies. Regulatory frameworks encourage the introduction of advanced drugs while ensuring patient safety. This environment enables the region to maintain a strong position in the market while addressing evolving patient needs effectively.

Asia-Pacific

T

he Asia-Pacific region accounts for approximately 22% of the global Endometrial Cancer Treatment market, exhibiting rapid growth driven by improving healthcare infrastructure and increasing awareness. Countries like China, Japan, India, and South Korea invest heavily in cancer care facilities and advanced diagnostic tools. Rising incidences of endometrial cancer and expanding middle-class populations contribute to growing demand for effective treatments. The region witnesses gradual adoption of targeted therapies and minimally invasive surgeries, supported by government initiatives and private sector investments. Challenges remain regarding affordability and access in rural areas, but ongoing efforts aim to bridge these gaps. Asia-Pacific’s expanding healthcare capabilities position it as a key growth market in the coming years.

Latin America

Latin America holds about 7% of the Endometrial Cancer Treatment market. The region experiences moderate growth fueled by increasing healthcare expenditure and improved cancer awareness campaigns. Countries like Brazil, Mexico, and Argentina lead in treatment adoption, supported by government programs focused on cancer control. Limitations in specialized oncology centers and disparities in access between urban and rural populations restrict rapid expansion. However, partnerships between public and private sectors encourage investment in healthcare infrastructure. The gradual integration of newer therapies, such as immunotherapy, supports market development. Latin America’s potential lies in enhancing healthcare access and increasing early diagnosis rates to improve treatment outcomes.

Middle East and Africa

The Middle East and Africa represent approximately 5% of the Endometrial Cancer Treatment market. Market growth remains steady, driven by increasing prevalence of endometrial cancer and expanding healthcare facilities in countries like Saudi Arabia, UAE, and South Africa. Investments in modern oncology centers and rising government focus on cancer care contribute to improved treatment availability. Barriers such as limited healthcare infrastructure in certain areas and affordability concerns continue to challenge market penetration. Efforts to raise cancer awareness and establish national screening programs seek to enhance early diagnosis rates. The region shows opportunity for growth through increased adoption of advanced therapies and improved healthcare delivery systems.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Pfizer Inc.

- Novartis AG

- Eisai Co., Ltd.

- Varian Medical Systems, Inc. (Siemens Healthineers AG)

- Teva Pharmaceutical Industries Ltd.

- Merck & Co., Inc.

- Alpine Life Sciences Private Limited

- AstraZeneca PLC

- Sun Pharmaceutical Industries Limited

- GSK plc

Competitive Analysis

Key players in the Endometrial Cancer Treatment market include Pfizer Inc., AstraZeneca PLC, Merck & Co., Inc., Novartis AG, Eisai Co., Ltd., and Varian Medical Systems, Inc. (Siemens Healthineers AG). These companies dominate the market through continuous innovation and strategic collaborations. They focus on expanding their product portfolios by developing targeted therapies, immunotherapies, and advanced surgical technologies. Significant investment in research and development enables them to introduce novel treatment options that address unmet clinical needs. Partnerships with research institutions and biotech firms enhance their pipeline strength and accelerate time-to-market. They also engage in mergers and acquisitions to consolidate market presence and improve competitive positioning. Marketing and distribution networks are optimized to increase global reach, especially in emerging markets. Strong regulatory compliance and emphasis on clinical trials further establish their credibility and foster trust among healthcare providers. These strategies help maintain their leadership and drive sustained growth in the competitive landscape of the Endometrial Cancer Treatment market.

Recent Developments

- In January 2025, Eisai and Merck announced that their combination regimen of LENVIMA plus KEYTRUDA showed a statistically significant improvement in progression-free survival for endometrial cancer patients.

- In 2025, AstraZeneca is listed among the top companies operating in the endometrial cancer treatment market, contributing to development of new therapies.

- In 2024, Pfizer has a drug, Ibrance (palbociclib), in Phase II clinical trials for endometrial cancer. Specifically, the trial focused on women with estrogen receptor-positive endometrioid endometrial cancer. The trial evaluated the combination of Ibrance with letrozole, comparing it to letrozole alone.

Market Concentration & Characteristics

The Endometrial Cancer Treatment market exhibits a moderately concentrated structure, dominated by several key pharmaceutical and medical device companies that hold significant market shares through extensive product portfolios and strong research capabilities. It features a blend of well-established multinational corporations and emerging biotech firms that compete by innovating targeted therapies, immunotherapies, and advanced surgical technologies. The market’s characteristics include high entry barriers due to substantial R&D investments, stringent regulatory requirements, and the need for clinical validation. Treatment complexity and evolving patient needs drive continuous product development and diversification. Geographic expansion and partnerships with healthcare providers further influence competitive dynamics. Market players emphasize personalized medicine approaches to differentiate offerings and enhance treatment efficacy. This concentration allows leaders to leverage economies of scale, extensive distribution networks, and strong brand recognition, while smaller companies focus on niche segments or innovative drug candidates. The Endometrial Cancer Treatment market’s competitive environment fosters innovation, leading to improved patient outcomes and expanding therapeutic options.

Report Coverage

The research report offers an in-depth analysis based on Cancer Type, Treatment, Stage and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will continue to grow driven by rising endometrial cancer incidence globally.

- Advances in targeted therapies and immunotherapy will expand treatment options.

- Personalized medicine will play a larger role in therapy selection and effectiveness.

- Minimally invasive surgical techniques will gain wider adoption for better patient recovery.

- Increasing awareness and early diagnosis efforts will improve treatment outcomes.

- Expansion of healthcare infrastructure in emerging markets will enhance accessibility.

- Integration of digital health tools will support patient monitoring and adherence.

- Collaborative research and clinical trials will accelerate the development of novel drugs.

- Cost containment strategies will become critical to address affordability challenges.

- Regulatory frameworks will evolve to fast-track approval of innovative therapies.