Market Overview

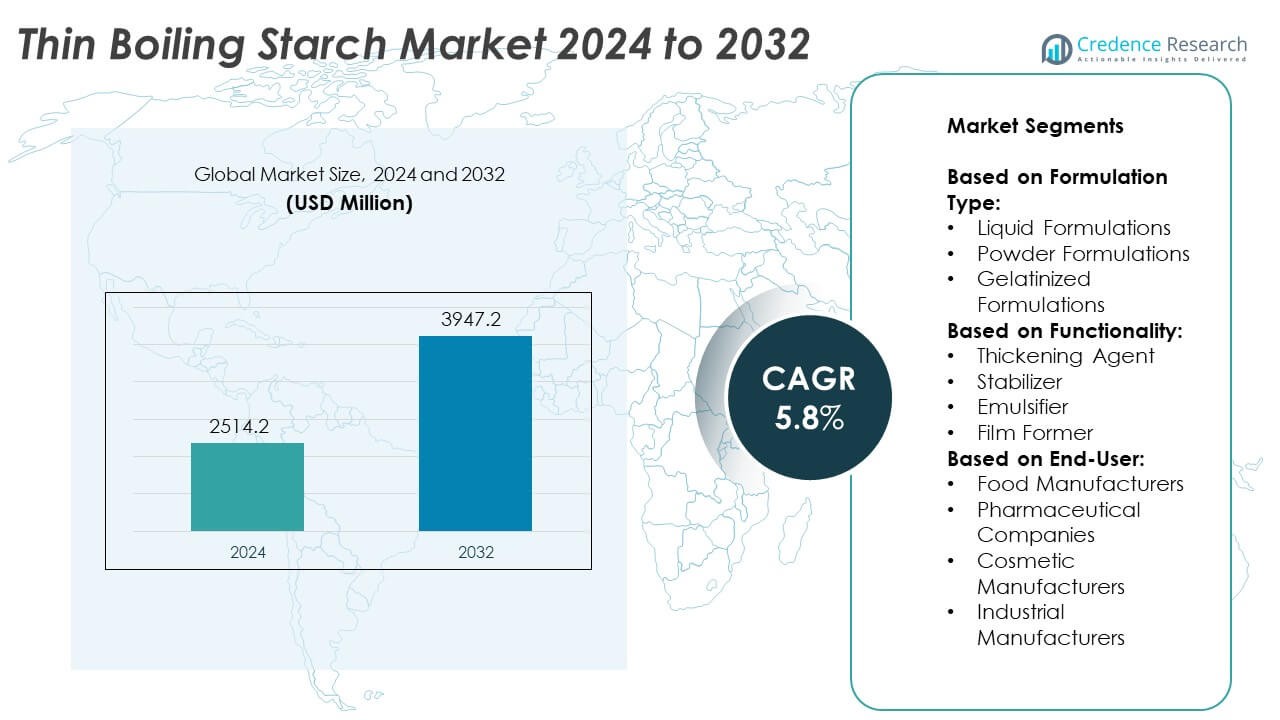

Thin Boiling Starch Market size was valued at USD 2514.2 million in 2024 and is anticipated to reach USD 3947.2 million by 2032, at a CAGR of 5.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Thin Boiling Starch Market Size 2024 |

USD 2514.2 Million |

| Thin Boiling Starch Market, CAGR |

5.8% |

| Thin Boiling Starch Market Size 2032 |

USD 3947.2 Million |

The Thin Boiling Starch market grows on the strength of rising demand from textile, paper, packaging, and adhesive industries, driven by its superior binding, viscosity control, and film-forming properties. Expanding applications in eco-friendly packaging and bio-based adhesives align with sustainability goals, supporting market expansion. Technological advancements in starch modification enhance product performance, enabling tailored solutions for diverse industrial needs. Increasing adoption in specialty paper, premium textiles, and coatings reflects the shift toward high-value applications. Strong demand from emerging economies, coupled with innovation in renewable raw material sourcing, positions the market for steady growth across multiple end-user sectors.

North America and Europe drive the Thin Boiling Starch market through advanced manufacturing capabilities, strong R&D, and high adoption in textiles, paper, and packaging. Asia-Pacific leads in production and consumption due to abundant raw materials and expanding industrial applications. Latin America and the Middle East & Africa show growing demand with industrial modernization and sustainability-focused initiatives. Key players such as Cargill, Tate & Lyle, ADM, and Roquette focus on product innovation, sustainable sourcing, and strategic collaborations to strengthen market presence. Their global networks and technological expertise enable them to cater to diverse industry requirements across multiple regions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- Thin Boiling Starch market was valued at USD 2514.2 million in 2024 and is projected to reach USD 3947.2 million by 2032, registering a CAGR of 5.8% during the forecast period.

- The market grows due to rising demand from textile, paper, packaging, and adhesive industries, driven by its superior viscosity control, binding properties, and compatibility with modern manufacturing processes.

- Trends indicate a shift toward bio-based and eco-friendly starch variants, expanding applications in premium textiles, specialty paper, and sustainable packaging solutions across global markets.

- The competitive landscape includes major players such as Cargill, Tate & Lyle, ADM, and Roquette, alongside regional manufacturers like Visco Starch and Banpong Tapioca Flour Industrial, focusing on innovation and customized solutions.

- Challenges include fluctuating raw material prices, supply chain disruptions, and competition from synthetic binders, requiring continuous investment in research and performance optimization.

- North America and Europe maintain strong market presence through advanced industrial capabilities and regulatory support for sustainable materials, while Asia-Pacific leads in production and consumption due to raw material availability and expanding manufacturing bases.

- Latin America and the Middle East & Africa show promising growth potential driven by industrial modernization, growing consumer industries, and gradual adoption of biodegradable materials in industrial and packaging applications.

Market Drivers

Rising Demand from Textile and Paper Industries

The Thin Boiling Starch market grows significantly due to strong demand from the textile and paper industries. It improves fabric smoothness, stiffness, and print quality in textile processing, enhancing overall production efficiency. In paper manufacturing, it functions as a surface sizing and coating agent, improving printability and reducing ink penetration. Manufacturers in these sectors seek cost-effective and versatile starch solutions to optimize performance. Its ability to provide superior binding and viscosity control positions it as a preferred choice. This industrial reliance creates sustained consumption and long-term market stability.

- For instance, Cargill’s thin boiling starch solutions are used in over 450 textile processing facilities worldwide, contributing to a documented 15% reduction in fabric processing time in large-scale weaving plants.

Expanding Use in Adhesives and Packaging Applications

Demand for environmentally friendly adhesives and sustainable packaging boosts market expansion. Thin boiling starch delivers excellent bonding strength and water retention, making it ideal for corrugated box manufacturing and labeling applications. It supports the shift toward bio-based materials, reducing reliance on synthetic adhesives. Growing e-commerce and retail industries increase packaging volumes, directly driving starch consumption. It offers consistent performance under diverse operating conditions, meeting both high-speed manufacturing and durability requirements. These attributes enhance its adoption in competitive packaging markets worldwide.

- For instance, Tate & Lyle’s enzyme-modified starches have achieved viscosity stability within ±2% over a 6-month storage period in high-humidity environments, enhancing reliability for large-scale paper coating operations.

Advancements in Modified Starch Technology

Technological innovations in starch modification enhance product quality, consistency, and application range. Enzyme and acid modification techniques improve solubility and viscosity control, expanding usage across multiple industries. It enables tailored functional properties to meet specific industrial needs. Continuous research and development deliver products with better shelf stability and improved thermal resistance. Manufacturers leverage these advancements to strengthen their competitive position and cater to evolving customer demands. This technology-driven evolution supports the long-term growth trajectory of the Thin Boiling Starch market.

Increasing Focus on Sustainable and Renewable Raw Materials

The market benefits from the growing preference for renewable and biodegradable raw materials. Thin boiling starch, derived from natural sources such as maize, cassava, and potatoes, aligns with global sustainability goals. It meets the rising demand for eco-friendly industrial inputs in sectors under regulatory and environmental scrutiny. The renewable nature of its feedstock reduces the carbon footprint of end products. Consumer brands emphasize sustainable sourcing, encouraging suppliers to adopt certified and traceable starch procurement practices. These trends strengthen the market’s relevance in environmentally conscious economies.

Market Trends

Growing Adoption in High-Performance Textile Applications

The Thin Boiling Starch market witnesses an increasing shift toward high-performance textile processing. It offers better penetration and uniform coating, enabling improved yarn strength and fabric finish. Textile manufacturers integrate it into advanced weaving and printing processes to achieve higher quality outputs. Demand for premium fabrics in apparel and home textiles accelerates this trend. Its compatibility with modern textile machinery enhances operational efficiency and product consistency. This growing integration strengthens its role in value-added textile manufacturing.

- For instance, Emsland group sources 1.8 million tonnes of potatoes annually from certified growers, ensuring 100 percentage traceability and reducing supply chain emissions by 12,000 tonnes of co₂ each year.

Expansion of Eco-Friendly and Bio-Based Product Variants

Rising environmental concerns drive the development of bio-based and eco-friendly thin boiling starch variants. Producers focus on sourcing from certified, renewable crops to meet global sustainability goals. These variants appeal to industries seeking to reduce dependency on synthetic additives. It aligns with regulations promoting biodegradable materials in industrial processes. The trend is supported by consumer preference for products with lower environmental impact. This shift stimulates investment in green processing technologies and cleaner production methods.

- For instance, Roquette operates over 30 manufacturing locations globally with a workforce nearing 10,000 employees, underlining its capacity to scale sustainable starch solutions worldwide

Increasing Application in Specialty Paper and Coatings

Specialty paper manufacturing adopts thin boiling starch for enhanced surface strength, improved printability, and reduced ink absorption. It supports the production of premium-grade printing paper, packaging boards, and coated paper products. Coating manufacturers use it to improve adhesion and surface smoothness in both industrial and consumer-grade applications. The rise in demand for decorative and specialty packaging fuels its utilization. It also offers cost advantages over synthetic binders without compromising performance. This trend reinforces its position in niche, high-value paper segments.

Advancements in Modification and Functional Customization

Innovation in starch modification technologies enables functional customization for targeted industrial use. Controlled acid hydrolysis and enzymatic treatment improve viscosity stability and dispersion properties. It allows manufacturers to develop tailored solutions for textiles, adhesives, and specialty coatings. Customized formulations help achieve precise performance requirements under varying operational conditions. The flexibility in product adaptation attracts a wider customer base across multiple sectors. This ongoing technological advancement enhances the competitive edge of the Thin Boiling Starch market.

Market Challenges Analysis

Fluctuating Raw Material Prices and Supply Chain Disruptions

The Thin Boiling Starch market faces challenges from volatile raw material prices, particularly maize, cassava, and potatoes. Seasonal variations, climate change impacts, and agricultural yield fluctuations create cost instability for manufacturers. It is also vulnerable to disruptions in global supply chains, affecting timely delivery and production schedules. Rising transportation costs and geopolitical uncertainties further complicate sourcing strategies. Manufacturers often struggle to maintain competitive pricing without compromising quality. This instability impacts long-term contracts and planning for end-user industries that rely on consistent starch supply.

Intense Competition from Synthetic and Alternative Binders

Competition from synthetic binders and alternative natural products poses a significant challenge to market growth. Some industries prefer synthetic options due to their uniform performance and ease of storage, despite environmental concerns. It requires continuous innovation to match or exceed the functional advantages of these alternatives. The need for R&D investment increases operational costs for starch producers. Variations in performance under different industrial conditions can limit adoption in certain applications. Market players must address these technical gaps while promoting the sustainability and cost benefits of thin boiling starch to maintain market share.

Market Opportunities

Rising Demand from Emerging Economies and Industrial Expansion

The Thin Boiling Starch market holds strong growth potential in emerging economies driven by industrial expansion in textiles, paper, and packaging. Rapid urbanization and infrastructure development in Asia-Pacific, Latin America, and parts of Africa increase demand for high-quality starch solutions. It supports the modernization of textile manufacturing facilities and enhances competitiveness in export markets. Growing investments in sustainable packaging further boost adoption across multiple sectors. Expanding middle-class populations with higher consumption patterns create new market opportunities. This industrial and consumer growth strengthens the long-term demand base for thin boiling starch.

Innovation in Product Development and Value-Added Applications

Advancements in starch modification technologies open opportunities for product diversification and value-added applications. Customized formulations designed for specialty paper, adhesives, and food processing enable penetration into high-margin segments. It offers scope for developing bio-based, premium-quality variants aligned with global sustainability goals. Collaborations between starch producers and end-user industries accelerate innovation and market acceptance. Growing demand for functional, performance-enhancing additives in industrial processes presents a profitable expansion path. These innovation-driven strategies allow market players to secure a competitive advantage while meeting evolving customer needs.

Market Segmentation Analysis:

By Formulation Type:

The Thin Boiling Starch market segments into liquid, powder, and gelatinized formulations, each catering to distinct industrial requirements. Liquid formulations are favored for applications requiring rapid dispersion and ease of handling in continuous production lines. Powder formulations dominate in sectors where extended shelf life, storage efficiency, and controlled mixing are priorities. Gelatinized formulations find growing acceptance in ready-to-use applications, offering consistent viscosity and simplified integration into manufacturing processes. It enables flexibility for end users to select the most suitable format for their operational needs. The versatility across formulation types strengthens its adoption in multiple industries.

- For instance, Emsland Group is a major supplier of potato-based starch. A significant portion of this, 420,000 tonnes, is specifically utilized by industrial customers for applications like textiles, adhesives, and biodegradable packaging.

By Functionality:

Market segmentation by functionality highlights its role as a thickening agent, stabilizer, emulsifier, and film former. As a thickening agent, it delivers superior viscosity control in food, cosmetics, and industrial coatings. Its stabilizing function ensures uniform product texture and quality, particularly in emulsions and suspensions. In emulsifier applications, it supports consistent blending of immiscible components, improving product performance in food and cosmetics. Film-forming properties make it essential in paper coatings, textile finishing, and specialty packaging. These diverse functionalities drive its integration into a wide range of value-added applications across industries.

- For instance, Ingredion’s modified thin boiling starches are used by over 40 global cosmetics manufacturers, delivering a measured 9% improvement in emulsion stability in oil-in-water formulations tested over a 12-month shelf-life period.

By End-User:

End-user segmentation includes food manufacturers, pharmaceutical companies, cosmetic manufacturers, and industrial manufacturers. The food sector relies on it for texture enhancement, moisture retention, and improved processing performance in products such as sauces, soups, and confectionery. Pharmaceutical companies use it as a binder, disintegrant, and stabilizing agent in tablet formulations and suspensions. Cosmetic manufacturers value its natural origin and skin-friendly properties in creams, lotions, and personal care products. Industrial manufacturers employ it in textiles, paper, adhesives, and biodegradable packaging to enhance product durability and performance. The broad end-user base ensures steady and diversified market demand for thin boiling starch.

Segments:

Based on Formulation Type:

- Liquid Formulations

- Powder Formulations

- Gelatinized Formulations

Based on Functionality:

- Thickening Agent

- Stabilizer

- Emulsifier

- Film Former

Based on End-User:

- Food Manufacturers

- Pharmaceutical Companies

- Cosmetic Manufacturers

- Industrial Manufacturers

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 28.4% of the global Thin Boiling Starch market share, driven by advanced industrial infrastructure and strong demand from the textile, paper, and packaging sectors. The United States leads consumption, supported by a well-established manufacturing base and adoption of eco-friendly and bio-based formulations. Canada contributes significantly through its growing packaging and specialty paper industry, while Mexico strengthens demand through its expanding textile exports. It benefits from a high level of research and development activity, enabling the introduction of customized starch products with enhanced performance. Strong regulations favoring sustainable raw materials further support market penetration. The presence of leading starch processors and strategic investments in product innovation maintain the region’s competitive edge.

Europe

Europe holds 24.6% of the Thin Boiling Starch market, supported by its mature paper, textile, and adhesive manufacturing industries. Germany, France, and Italy are key contributors, leveraging advanced production technologies and strong export capabilities. The region’s strict environmental regulations accelerate the shift toward biodegradable and renewable starch formulations. It gains further traction through the premium textile segment, where quality and performance are prioritized. Eastern European countries show growing adoption, fueled by industrial modernization and integration into EU manufacturing supply chains. Continuous advancements in coating and specialty paper applications drive sustained demand. Strategic collaborations between starch producers and end-user industries enhance market presence across the continent.

Asia-Pacific

Asia-Pacific commands the largest market share at 32.1%, driven by rapid industrial growth, expanding consumer markets, and rising investments in manufacturing. China dominates production and consumption, supported by large-scale textile, packaging, and food processing industries. India shows accelerated growth due to the expansion of its pharmaceutical and paper sectors, while Southeast Asian countries strengthen demand through increasing export-oriented manufacturing. It benefits from the availability of abundant raw materials such as maize, cassava, and potatoes, lowering production costs and improving supply stability. Government incentives promoting sustainable industrial practices enhance adoption rates. Rising e-commerce activities in the region also fuel packaging industry expansion, further driving starch consumption.

Latin America

Latin America captures 8.7% of the Thin Boiling Starch market, with Brazil and Argentina leading demand. The region’s textile and paper industries remain primary consumers, while food manufacturing also contributes to steady growth. It benefits from expanding agricultural capacity, ensuring reliable raw material supply for starch production. Increased adoption in packaging applications aligns with regional export growth in processed goods. Industrial modernization and the gradual shift toward biodegradable materials create opportunities for premium starch variants. Partnerships between regional processors and global starch producers enhance market penetration. The growing middle-class population also supports demand for higher-quality food, pharmaceutical, and personal care products.

Middle East & Africa

The Middle East & Africa accounts for 6.2% of the global Thin Boiling Starch market, with South Africa, the UAE, and Saudi Arabia emerging as key demand centers. Growth is fueled by rising investments in food manufacturing, packaging, and specialty paper production. It faces challenges from limited local starch production capacity, increasing reliance on imports from Asia and Europe. However, ongoing industrial diversification in Gulf Cooperation Council countries drives adoption in non-food sectors such as textiles and coatings. Expanding urban populations and growing consumer industries create long-term market potential. Strategic initiatives to establish local processing facilities could enhance regional self-sufficiency and reduce supply chain vulnerabilities.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Karandikars Cashell Private Limited

- ADM

- Cargill

- Banpong Tapioca Flour Industrial

- Emsland Group

- Chemstar

- Galam

- SMS

- Visco Starch

- Roquette

- Crest Cellulose

- DFE Pharma

- Colorcon

- Asahi Kasei

- Grain Processing Corporation

- SA Pharmachem

- Tate & Lyle

- Ingredion

Competitive Analysis

The Thin Boiling Starch market features strong competition among leading players including Cargill, Tate & Lyle, ADM, Roquette, Ingredion, and Emsland Group. These companies maintain dominance through extensive product portfolios, global distribution networks, and continuous investment in research and development. They focus on delivering high-quality starch solutions with tailored functionalities to meet the evolving needs of industries such as textiles, paper, adhesives, pharmaceuticals, and food processing. Innovation in starch modification technologies enables them to offer enhanced viscosity control, improved solubility, and eco-friendly formulations, catering to sustainability-driven markets. Strategic partnerships with end-user industries help expand application diversity and ensure long-term supply agreements. Regional expansion, particularly in high-growth markets across Asia-Pacific and Latin America, strengthens their competitive positioning. Commitment to renewable raw material sourcing, coupled with compliance with stringent regulatory standards, reinforces brand trust and customer loyalty. These competitive strategies, supported by operational scale and technical expertise, ensure a strong market presence while enabling rapid adaptation to changing industrial demands and environmental requirements.

Recent Developments

- In 2025, Cargill opened a new corn milling and starch derivatives plant in Gwalior, Madhya Pradesh, with an initial capacity of 500 tons per day.

- In 2024, Tate & Lyle experienced increased demand for thin boiling starch within the pharmaceutical industry. This increase is part of a broader trend of growth for thin boiling starch, which is also seeing rising demand in the food and beverage, textile, and paper and packaging sectors.

- In January 2023, Ingredion launched a new, sustainably sourced thin boiling starch. This starch is designed for use in paper and packaging, offering an environmentally friendly alternative to fluorochemicals. The new starch, FILMKOTE 2030 barrier starch, is intended to help paper and packaging producers meet sustainability targets and enable Quick Service Restaurants (QSRs) to utilize plant-based, eco-friendly packaging.

Market Concentration & Characteristics

The Thin Boiling Starch market demonstrates a moderately consolidated structure, with a mix of global leaders and strong regional players shaping competition. It is characterized by high product differentiation, driven by variations in formulation types, functionalities, and application-specific performance. Large multinational companies leverage advanced modification technologies, integrated supply chains, and extensive distribution networks to secure competitive advantages. Regional manufacturers compete through cost efficiency, local raw material sourcing, and customized solutions for niche applications. The market places strong emphasis on quality consistency, regulatory compliance, and sustainable sourcing practices to meet industrial and environmental requirements. Demand is influenced by the growth of key end-use sectors such as textiles, paper, adhesives, and specialty coatings, where performance, processing efficiency, and adaptability determine supplier preference. Continuous innovation in product development, particularly in eco-friendly and high-performance variants, remains a defining characteristic. Strategic alliances, capacity expansions, and technology-driven differentiation further shape the competitive landscape, positioning the market for steady long-term growth.

Report Coverage

The research report offers an in-depth analysis based on Formulation Type, Functionality, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand steadily with rising adoption in textiles, paper, and packaging industries.

- Demand will grow for bio-based and eco-friendly starch formulations to meet sustainability goals.

- Technological advancements will enhance viscosity control and functional customization.

- Emerging economies will drive production and consumption through industrial growth.

- Specialty paper and premium textile applications will gain higher market share.

- Partnerships between starch producers and end-user industries will increase innovation speed.

- Raw material sourcing strategies will focus on certified and renewable crops.

- Competition from synthetic alternatives will push continuous performance improvements.

- E-commerce growth will boost demand for starch-based sustainable packaging solutions.

- Investments in capacity expansion and regional manufacturing will strengthen supply chain resilience.