Market Overview

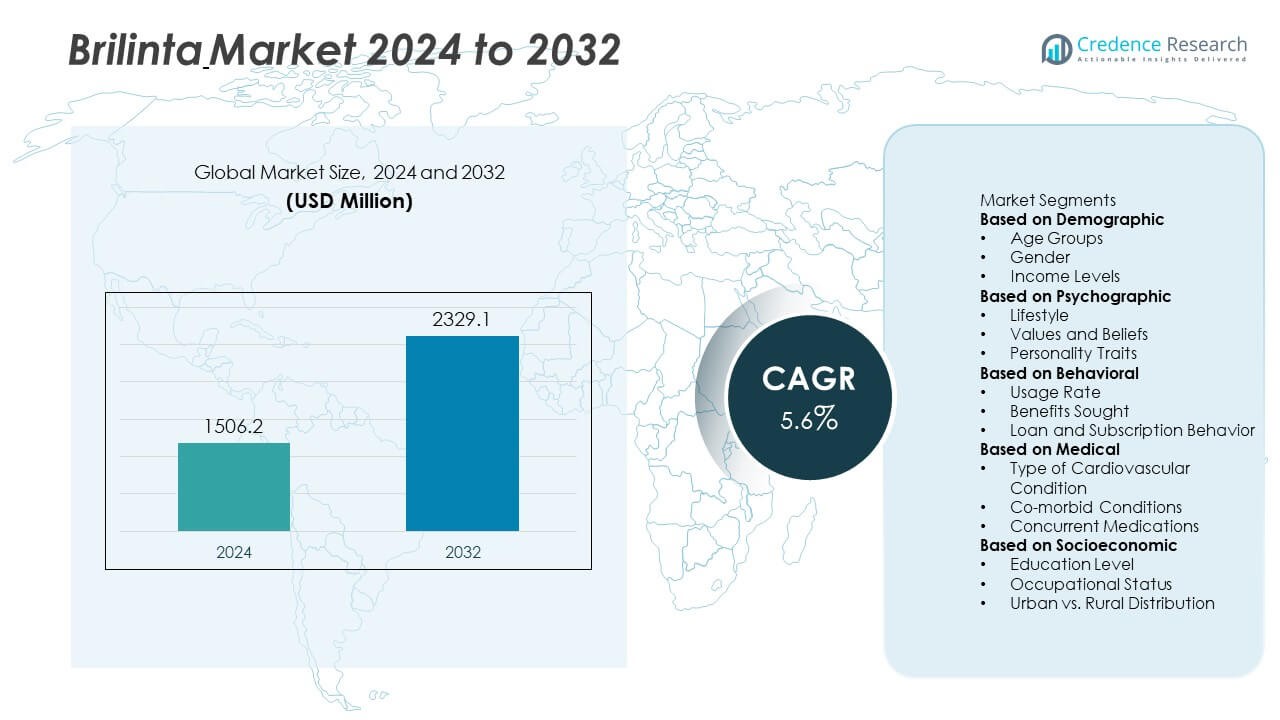

The Brilinta Market was valued at USD 1,506.2 million in 2024 and is projected to reach USD 2,329.1 million by 2032, growing at a CAGR of 5.6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Brilinta Market Size 2024 |

USD 1,506.2 Million |

| Brilinta Market, CAGR |

5.6% |

| Brilinta Market Size 2032 |

USD 2,329.1 Million |

The Brilinta Market is driven by the rising prevalence of cardiovascular diseases, growing adoption of advanced antiplatelet therapies, and strong clinical evidence supporting its efficacy in reducing recurrent thrombotic events. Expanding indications, including long-term secondary prevention and potential stroke prevention, enhance its clinical relevance.

The Brilinta Market spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, each demonstrating distinct adoption patterns influenced by healthcare infrastructure, treatment guidelines, and disease prevalence. North America leads adoption due to strong integration of Brilinta into cardiovascular care protocols and broad insurance coverage. Europe maintains high prescription rates supported by established clinical guidelines and centralized healthcare systems. Asia-Pacific shows rapid growth with expanding cardiac care facilities and improving access to advanced therapies in urban centers. Latin America and the Middle East & Africa are gradually increasing uptake through hospital modernization and physician education. Key players influencing the market include AstraZeneca, the manufacturer of Brilinta; Pfizer, with extensive cardiovascular therapy portfolios; Amgen, focusing on innovative cardiovascular solutions; and Merck, leveraging its global distribution and research capabilities to strengthen therapeutic reach in antiplatelet treatments.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Brilinta Market was valued at USD 1,506.2 million in 2024 and is projected to reach USD 2,329.1 million by 2032, growing at a CAGR of 5.6% during the forecast period.

- Rising prevalence of cardiovascular diseases, an aging population, and updated clinical guidelines are driving adoption of Brilinta for acute coronary syndrome and long-term secondary prevention.

- Expanding use in stroke prevention trials, patient-centric dosing strategies, and integration into extended treatment protocols are shaping current market trends.

- The market is influenced by strong competition among major pharmaceutical companies that invest in clinical trials, regulatory approvals, and physician education to strengthen therapeutic positioning.

- High treatment costs, varying reimbursement coverage, and potential side effects such as dyspnea and bleeding risks remain key restraints affecting consistent adoption across regions.

- North America leads adoption due to advanced healthcare infrastructure and strong treatment integration, Europe maintains high prescription rates through guideline adherence, Asia-Pacific shows rapid uptake with expanding cardiac care facilities, and Latin America and the Middle East & Africa see gradual growth through hospital modernization.

- Opportunities emerge from expanding healthcare access in emerging markets, regulatory approvals for new indications, and collaborative research that can extend Brilinta’s role in broader cardiovascular disease management.

Market Drivers

Rising Prevalence of Cardiovascular Diseases Driving Demand

The Brilinta Market benefits from the growing incidence of acute coronary syndrome and other cardiovascular conditions worldwide. An aging global population and lifestyle-related risk factors increase the need for effective antiplatelet therapy. Healthcare systems integrate Brilinta into treatment protocols to reduce the risk of thrombotic events following percutaneous coronary interventions. It is widely prescribed for secondary prevention in high-risk patients. Clinical guidelines from leading cardiology associations support its inclusion in standard care pathways. This expanding patient pool strengthens consistent demand across both developed and emerging regions.

- For instance, The US FDA expanded Brilinta’s indication to allow long-term use in patients with a history of myocardial infarction, aligning labeling with sustained secondary prevention.

Strong Clinical Evidence Supporting Efficacy and Safety

Extensive clinical trial data reinforces the therapeutic value of Brilinta in improving cardiovascular outcomes. Trials such as PLATO and PEGASUS-TIMI 54 demonstrated significant reductions in major adverse cardiovascular events compared to traditional therapies. Physicians value its ability to provide rapid platelet inhibition with reversible binding properties. It supports superior long-term management strategies in patients with prior myocardial infarction. The continuous release of post-marketing surveillance data enhances physician confidence in prescribing it. Such strong evidence base drives adoption across hospital and outpatient settings.

- For instance, in the PLATO trial, Brilinta demonstrated a 16% relative risk reduction in cardiovascular death, myocardial infarction, or stroke compared to clopidogrel, benefiting over 18,000 acute coronary syndrome patients worldwide.

Expanding Indications and Regulatory Approvals

Regulatory authorities in multiple countries have approved Brilinta for broader cardiovascular applications. It now covers indications beyond acute coronary syndrome, including long-term secondary prevention in patients with established coronary artery disease. Expansion into stroke prevention segments adds to its clinical relevance. Pharmaceutical strategies focus on submitting new data to health agencies to secure additional label extensions. Hospitals and cardiology centers respond by incorporating it into wider patient management plans. This expanded clinical footprint directly supports market growth potential.

Growing Access Through Healthcare Infrastructure Development

Improved healthcare infrastructure in emerging markets increases patient access to advanced cardiovascular therapies. Governments and private insurers enhance reimbursement frameworks for essential cardiovascular drugs, including Brilinta. It benefits from inclusion in national essential medicine lists in certain regions. Expansion of specialist cardiac care facilities supports higher diagnosis and treatment rates. Distribution networks adapt to reach rural and underserved areas, ensuring consistent supply. These improvements in access accelerate uptake among newly diagnosed and high-risk patient populations.

Market Trends

Increasing Use in Long-Term Secondary Prevention Protocols

The Brilinta Market is witnessing a shift toward extended treatment durations for patients with prior myocardial infarction. Physicians incorporate it into long-term therapy plans to reduce recurrent cardiovascular events. This approach aligns with evolving clinical guidelines that emphasize sustained platelet inhibition in high-risk populations. Real-world data supports its tolerability and sustained efficacy over multiple years of therapy. Hospitals adapt their discharge protocols to ensure continued outpatient prescription. This trend strengthens its role in chronic cardiovascular care pathways.

- For instance, the PEGASUS–TIMI 54 trial showed ticagrelor 60 mg twice daily, continued beyond one year after MI, reduced the composite of CV death, MI, or stroke by ~15–16% versus placebo, with an expected increase in major bleeding.

Rising Integration into Stroke Prevention Strategies

Clinical research is expanding Brilinta’s potential in ischemic stroke prevention and management. Trials investigate its efficacy in reducing recurrent stroke risks when used in specific patient groups. It attracts interest from neurologists for use in secondary prevention settings alongside standard therapies. Regulatory submissions in multiple regions seek label expansion to include these new indications. Academic centers actively participate in large-scale, multicountry trials to validate its broader role. This trend could expand its market beyond core cardiology applications.

- For instance, the THALES trial demonstrated that Brilinta plus aspirin reduced the risk of stroke and death by 17% compared to aspirin alone in patients with acute non-cardioembolic ischemic stroke or high-risk TIA.

Growing Adoption of Patient-Centric Dosing Strategies

Pharmaceutical development focuses on optimizing Brilinta’s dosing schedules to improve adherence and reduce side effects. Lower-dose regimens are evaluated for long-term use in patients requiring extended antiplatelet therapy. It supports the goal of minimizing bleeding risks while preserving cardiovascular protection. Personalized medicine approaches match dosing intensity with patient-specific risk profiles. Hospitals integrate pharmacist-led counseling programs to reinforce adherence. This trend enhances patient outcomes and treatment continuity.

Expansion of Collaborative Research and Real-World Evidence Generation

Global healthcare networks and pharmaceutical companies collaborate to produce extensive real-world evidence on Brilinta’s performance. Data from electronic health records and large patient registries offer insights into effectiveness in diverse clinical settings. It helps refine treatment guidelines and identify optimal patient segments for therapy. Post-marketing studies assess comparative outcomes against other antiplatelet agents. Regulatory agencies increasingly value such evidence in decision-making processes. This trend accelerates market confidence and supports broader prescribing practices.

Market Challenges Analysis

High Treatment Costs and Reimbursement Limitations

The Brilinta Market faces challenges from the high cost of therapy, which can limit access in price-sensitive regions. Branded formulations often remain beyond the reach of uninsured or underinsured patients. Limited reimbursement coverage in certain healthcare systems restricts broader adoption. It places financial pressure on hospitals and clinics in low- and middle-income countries. Health authorities may prioritize lower-cost generic antiplatelet agents, reducing its market share potential. These economic barriers can slow uptake despite strong clinical evidence supporting its benefits.

Adverse Effects and Patient Compliance Issues

Side effects such as dyspnea and bleeding risks present significant hurdles for long-term therapy adherence. Some patients discontinue treatment prematurely due to intolerance or perceived discomfort. It requires careful patient selection and monitoring to balance efficacy with safety. Physicians may opt for alternative antiplatelet therapies in cases with high bleeding risk. Poor compliance undermines clinical outcomes and reduces the overall effectiveness of prevention strategies. This challenge emphasizes the need for enhanced patient education and tailored dosing regimens to maintain sustained use.

Market Opportunities

Expansion into Emerging Cardiovascular Care Markets

The Brilinta Market holds strong growth potential in emerging economies with increasing cardiovascular disease prevalence. Expanding healthcare infrastructure and broader access to diagnostic services create more opportunities for early intervention. Governments are investing in specialized cardiac care centers, which drives demand for advanced antiplatelet therapies. It benefits from inclusion in updated national treatment guidelines in several developing regions. Partnerships with local distributors can improve reach in underserved areas. This expansion supports both patient outcomes and long-term market sustainability.

Diversification of Indications Through Ongoing Clinical Research

Extensive clinical trials exploring Brilinta’s role in stroke prevention, peripheral artery disease, and other thrombotic conditions could widen its therapeutic scope. Positive trial results may lead to regulatory approvals for new patient segments, strengthening its competitive positioning. It has the potential to serve as a core therapy in multidisciplinary cardiovascular management. Integration into combination regimens with other agents offers opportunities for personalized treatment approaches. Collaborative research with academic institutions can accelerate adoption in new specialties. These developments create a pathway for expanding market relevance beyond its current cardiovascular focus.

Market Segmentation Analysis:

By Demographic

The Brilinta Market serves a wide demographic spectrum, with primary demand concentrated among adults over the age of 50 who face elevated cardiovascular risk. This group includes patients with acute coronary syndrome, history of myocardial infarction, or established coronary artery disease. It also addresses younger patients with genetic or lifestyle-related predispositions to cardiovascular events. Gender-specific studies have shown consistent efficacy in both male and female patients, though dosing and monitoring requirements may vary based on comorbidities. Elderly populations often require careful management to balance efficacy with bleeding risk, making patient selection critical.

- For instance, in PEGASUS-TIMI 54 (mean age 65), adults ≥50 with prior MI on aspirin had primary events of 7.8% on ticagrelor 60 mg twice daily vs 9.0% on placebo over a median 33 months; TIMI major bleeding was 2.3% vs 1.1%.

By Psychographic

Psychographic segmentation in the Brilinta Market focuses on patient attitudes toward preventive healthcare, adherence to long-term medication, and trust in advanced pharmaceutical solutions. Patients who value proactive cardiovascular risk management are more likely to remain compliant with prescribed regimens. It appeals to individuals who prioritize evidence-based therapies backed by strong clinical trial data. Physicians often target health-conscious segments with comprehensive counseling to reinforce the importance of continuous therapy. In markets where awareness campaigns have improved patient knowledge about cardiovascular risks, adoption rates are higher.

- For instance, AstraZeneca’s PLATO trial reported a lower 12-month rate of vascular death/MI/stroke with ticagrelor vs. clopidogrel (9.8% vs. 11.7%), reinforcing appeal among evidence-seeking patients and physicians.

By Behavioral

Behavioral segmentation captures patterns related to prescription initiation, adherence, and long-term therapy continuation. The Brilinta Market shows strong uptake in hospital discharge protocols for post-acute coronary syndrome patients, where immediate initiation is critical for reducing recurrent event risks. It is often included in structured follow-up programs to ensure consistent use during the high-risk period after intervention. Patient adherence is influenced by perceived side effects, ease of dosing, and quality of physician-patient communication. Behavioral targeting also considers the role of pharmacy-led interventions and digital reminder systems to improve compliance. This approach enables healthcare providers to identify and engage patients most likely to benefit from sustained antiplatelet therapy.

Segments:

Based on Demographic

- Age Groups

- Gender

- Income Levels

Based on Psychographic

- Lifestyle

- Values and Beliefs

- Personality Traits

Based on Behavioral

- Usage Rate

- Benefits Sought

- Loan and Subscription Behavior

Based on Medical

- Type of Cardiovascular Condition

- Co-morbid Conditions

- Concurrent Medications

Based on Socioeconomic

- Education Level

- Occupational Status

- Urban vs. Rural Distribution

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 42% of the Brilinta Market, supported by advanced healthcare infrastructure, high awareness of cardiovascular disease prevention, and favorable reimbursement policies. The United States dominates regional sales, driven by strong integration of Brilinta into treatment guidelines for acute coronary syndrome and secondary prevention. High diagnosis rates, widespread access to interventional cardiology, and robust insurance coverage enable broad adoption. Canada contributes through centralized healthcare initiatives that prioritize evidence-based antiplatelet therapies. It benefits from consistent physician education programs and ongoing real-world evidence studies validating clinical outcomes. Strategic collaborations between pharmaceutical companies and hospital networks further enhance prescribing rates in this region.

Europe

Europe holds 31% of the Brilinta Market, with leading demand from the United Kingdom, Germany, France, and Italy. The region’s strong focus on clinical guideline adherence and government-funded healthcare systems supports high prescription volumes. European cardiology associations endorse Brilinta for secondary prevention in high-risk patients, reinforcing its position in standard care protocols. It benefits from centralized procurement in several countries, improving accessibility in both urban and rural hospitals. Ongoing clinical trials in the region explore expanded indications, including stroke prevention. Investment in cardiovascular research infrastructure allows rapid adoption of new therapeutic strategies, strengthening market penetration.

Asia-Pacific

Asia-Pacific represents 17% of the Brilinta Market, fueled by growing cardiovascular disease incidence, expanding healthcare access, and rising awareness of advanced therapies. China, Japan, India, and Australia lead the regional adoption curve, supported by urbanization and increased availability of interventional cardiology facilities. It gains momentum from national healthcare reforms that improve access to prescription drugs in emerging economies. Localized physician training programs promote correct patient selection and monitoring. Expansion of generic and branded supply channels ensures consistent availability across metropolitan and secondary cities. The region’s large patient base presents significant potential for long-term growth as diagnostic capabilities expand.

Latin America

Latin America holds 6% of the Brilinta Market, with Brazil, Mexico, and Argentina driving demand. Rising investments in public healthcare systems and private hospital networks improve access to modern cardiovascular treatments. It benefits from gradual inclusion into treatment protocols for post-myocardial infarction and high-risk coronary artery disease patients. Efforts to expand interventional cardiology services in urban centers further increase uptake. Pharmaceutical companies focus on physician education and awareness campaigns to improve adoption rates. However, variations in reimbursement and economic constraints limit consistent penetration across all markets in the region.

Middle East & Africa

The Middle East & Africa account for 4% of the Brilinta Market, supported by targeted investments in tertiary care hospitals and specialized cardiac centers. Gulf countries, including Saudi Arabia and the United Arab Emirates, lead in adoption due to advanced healthcare systems and high cardiovascular disease burden. It benefits from government-backed initiatives to modernize treatment protocols and improve access to branded antiplatelet therapies. In Africa, uptake remains concentrated in urban hospitals with advanced cardiology departments. International partnerships with healthcare NGOs and training programs for cardiologists support gradual expansion. The region’s market potential remains underdeveloped but is expected to grow with continued infrastructure improvements.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Amgen

- Boehringer

- Merck

- Ingelheim Pfizer

- AstraZeneca

- Roche

- Eli Lilly

- Pfizer

- GSK

- Ingelheim

Competitive Analysis

The competitive landscape of the Brilinta Market is shaped by the presence of major pharmaceutical companies with strong cardiovascular therapy portfolios. Leading players include AstraZeneca, Pfizer, Amgen, Merck, and GSK, each leveraging global distribution networks, clinical expertise, and regulatory strategies to strengthen market position. AstraZeneca, as the originator of Brilinta, maintains dominance through extensive clinical trial programs, post-marketing surveillance, and strategic collaborations with healthcare institutions to expand usage across approved and emerging indications. Pfizer supports its cardiovascular portfolio with comprehensive physician outreach, ensuring integration into treatment protocols for acute coronary syndrome and secondary prevention. Amgen focuses on innovation in cardiovascular care, aligning with collaborative research to enhance patient outcomes. Merck emphasizes its global presence and market access capabilities, ensuring consistent supply and regional penetration. GSK contributes through research partnerships and targeted market expansion efforts. Competitive strategies include investment in real-world evidence, label extensions, and expansion into high-growth regions with evolving healthcare infrastructure.

Recent Developments

- In May 2025, Teva Pharmaceuticals launched an AB-rated generic version of Brilinta (ticagrelor) tablets in the U.S

- In August 2024, The U.S. FDA accepted the Biologics License Application (BLA) for bentracimab, a novel specific reversal agent for ticagrelor (Brilinta), granting it priority review status with a target action date in early 2025

Market Concentration & Characteristics

The Brilinta Market exhibits moderate concentration, with a limited number of multinational pharmaceutical companies influencing global supply, regulatory strategy, and clinical adoption. AstraZeneca leads through direct product ownership, while other key industry participants impact market dynamics via distribution partnerships, competitive therapies, and ongoing cardiovascular research. It is characterized by high entry barriers due to stringent regulatory requirements, extensive clinical trial obligations, and the need for strong physician outreach programs. The market relies heavily on evidence-based positioning supported by large-scale trials and post-marketing surveillance. Patient outcomes, safety profiles, and guideline endorsements significantly shape prescribing behavior. It shows strong alignment with specialized cardiovascular care networks and benefits from integration into hospital discharge protocols for acute coronary syndrome. The competitive environment is defined by continuous investment in label expansions, development of reversal agents, and the pursuit of long-term treatment indications to strengthen market sustainability.

Report Coverage

The research report offers an in-depth analysis based on Demographic, Psychographic, Behavioral, Medical, Socioeconomic and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with broader adoption of Brilinta in long-term secondary prevention therapies.

- Clinical trial outcomes will support new indications, including stroke prevention and peripheral artery disease.

- Healthcare infrastructure improvements in emerging markets will drive higher prescription volumes.

- Regulatory approvals for label extensions will strengthen its clinical positioning.

- Real-world evidence will enhance physician confidence and guide optimal prescribing practices.

- Patient-centric dosing strategies will improve adherence and treatment continuity.

- Development of reversal agents will increase physician comfort in managing bleeding risks.

- Integration into more hospital discharge protocols will boost early initiation rates.

- Digital health tools will support patient monitoring and compliance.

- Strategic collaborations will expand access in underserved regions and diversify market reach.