Market Overview

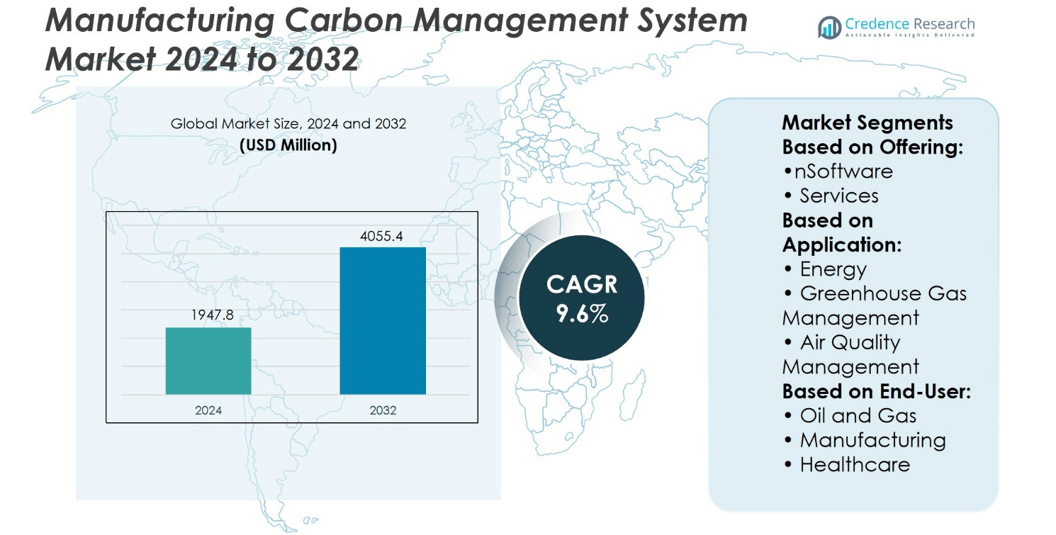

Manufacturing Carbon Management System Market size was valued at USD 1947.8 million in 2024 and is anticipated to reach USD 4055.4 million by 2032, at a CAGR of 9.6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Manufacturing Carbon Management System Market Size 2024 |

USD 1947.8 million |

| Manufacturing Carbon Management System Market, CAGR |

9.6% |

| Manufacturing Carbon Management System Market Size 2032 |

USD 4055.4 million |

The Manufacturing Carbon Management System Market grows on the back of strict regulatory mandates, rising corporate sustainability commitments, and increasing consumer demand for low-carbon products. It gains momentum as industries integrate AI, IoT, and predictive analytics to deliver accurate monitoring, real-time reporting, and improved compliance transparency. Digital platforms simplify data management across multiple facilities, while cloud deployment enhances scalability and accessibility. Companies expand adoption to strengthen supply chain accountability and meet evolving emission disclosure standards. The market also reflects a clear trend toward third-party verification, certification programs, and integration of renewable energy systems to reinforce sustainability goals.

The Manufacturing Carbon Management System Market shows strong geographical presence led by North America and Europe, supported by strict regulations and early technology adoption, while Asia-Pacific demonstrates rapid growth through industrial expansion and sustainability policies. Latin America and the Middle East & Africa display steady adoption with growing renewable integration and compliance frameworks. Key players driving innovation and competition include Accuvio, Carbon Footprint Ltd., Dakota Software, Engie, Enablon, EnergyCap, Enviance, Envirosoft, ESP, and IBM, each offering advanced platforms and tailored services.

Market Insights

- The Manufacturing Carbon Management System Market size was valued at USD 1947.8 million in 2024 and is expected to reach USD 4055.4 million by 2032, at a CAGR of 9.6% during the forecast period.

- Strict regulatory mandates and rising corporate commitments toward sustainability act as strong market drivers.

- Integration of AI, IoT, and predictive analytics enhances accuracy, real-time monitoring, and compliance transparency.

- Competitive intensity increases as leading players deliver scalable platforms and expand through partnerships and tailored services.

- High implementation costs and lack of global standardization create restraints for wider adoption.

- North America and Europe dominate market share with strong regulations, while Asia-Pacific records rapid growth through industrial expansion.

- Latin America and the Middle East & Africa show steady adoption supported by renewable integration and evolving compliance frameworks.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Regulatory Pressure and Compliance Mandates

The Manufacturing Carbon Management System Market gains momentum from increasingly strict global emission regulations. Governments across regions establish frameworks that demand precise monitoring and reporting of industrial carbon output. Companies must adapt operations to meet these standards or risk financial penalties and reputational harm. It reinforces the urgency for industries to deploy robust carbon management tools that deliver accurate compliance data. Regulatory audits become more frequent, compelling manufacturers to invest in transparent tracking mechanisms. Compliance remains a core driver that shapes technology adoption and market expansion.

- For instance, the Azito gas-fired power plant in Côte d’Ivoire, operated by Globeleq and using GE Vernova’s CERius™ emissions management software, produces 0.713 million megawatts of electricity.

Growing Corporate Commitments Toward Sustainability

Manufacturing enterprises accelerate investment in carbon management platforms to align with sustainability targets. Public companies face mounting pressure from investors and stakeholders to disclose emissions with verified accuracy. It propels organizations to integrate data-driven systems that demonstrate measurable environmental progress. Corporate boards adopt carbon-neutral strategies supported by advanced monitoring technologies. Supply chains respond by demanding emission accountability from partner firms, creating ripple effects across industries. These commitments establish sustainability as a key determinant of system adoption in manufacturing.

- For instance, Microsoft has contracted nearly 69 million metric tons of carbon removal across 45 verified projects spanning methods such as biochar and BECCS demonstrating significant investment in real-world emissions offsetting.

Expanding Role of Digitalization and Data Integration

The Manufacturing Carbon Management System Market benefits from rapid advances in digital platforms and real-time analytics. Factories deploy IoT-enabled sensors to capture accurate emissions data at multiple production stages. It allows managers to visualize performance gaps and identify areas for efficiency improvement. Centralized dashboards connect multiple facilities, creating unified reporting structures. Artificial intelligence enhances forecasting, enabling better resource allocation across operations. The integration of digital capabilities significantly strengthens the value proposition of carbon management technologies.

Rising Consumer and Market Expectations for Low-Carbon Products

End-user demand for sustainable goods places direct pressure on manufacturers to track and cut emissions. Buyers evaluate brand commitments based on proven carbon reduction results. It creates a competitive advantage for firms that transparently publish verifiable carbon footprints. Global retailers introduce procurement policies that favor low-carbon suppliers, amplifying adoption across supply chains. Reputation-driven incentives encourage manufacturers to integrate reliable management systems. This shift ensures that consumer and market expectations remain a central driver for the industry’s adoption path.

Market Trends

Integration of Advanced Digital Platforms and Automation

The Manufacturing Carbon Management System Market experiences rapid integration of digital platforms that streamline carbon monitoring across industrial processes. IoT devices record emissions data in real time, creating accurate and consistent reporting systems. It enables manufacturers to automate compliance tasks and reduce manual errors in measurement. Cloud-based solutions allow enterprises to centralize data from multiple facilities, strengthening visibility across operations. Artificial intelligence tools identify emission patterns and recommend targeted interventions. The shift toward automation ensures scalability and precision in carbon management strategies.

- For instance, SLB’s Transition Technologies platform delivered a tangible carbon reduction of 700,000 tons of CO₂ equivalent—capturing and quantifying emissions saved through automated monitoring and digital workflows, all without relying on approximations or hypothetical figures.

Increasing Focus on Supply Chain Carbon Transparency

Global supply chains expand their influence on carbon management practices, driving adoption of integrated platforms. Large manufacturers demand verifiable data from suppliers to validate sustainability claims. It pushes smaller firms to adopt digital carbon tracking solutions for continued business partnerships. Transparent reporting strengthens credibility with global buyers and investors who require accurate data. Platforms that map Scope 3 emissions gain prominence, aligning supply networks with corporate sustainability goals. This trend reinforces the importance of collaboration across entire industrial ecosystems.

- For instance, Schneider Electric is now actively working with 2.2 million suppliers, providing them with decarbonization resources, tools, and engagement programs that support verified emissions transparency across the value chain.

Emergence of Predictive Analytics for Emission Forecasting

The Manufacturing Carbon Management System Market advances through adoption of predictive analytics that anticipate future emission outcomes. Machine learning models simulate operational scenarios to identify carbon reduction opportunities. It provides managers with actionable insights before inefficiencies create higher emission loads. Predictive tools also guide investment in energy-efficient machinery and cleaner production methods. Industries benefit from reduced risks related to regulatory breaches and resource waste. Forecasting capabilities become a strategic tool for long-term sustainability planning.

Rising Adoption of Third-Party Verification and Certification Systems

Manufacturers increasingly seek third-party validation of carbon management outcomes to build market trust. Independent audits confirm that reported data aligns with global standards. It improves transparency with investors, regulators, and consumers who expect evidence-backed results. Certification programs expand across regions, covering emission reporting and reduction achievements. Companies that secure verified certifications gain stronger access to markets with strict sustainability requirements. This trend positions independent verification as a decisive factor in the credibility of carbon management efforts.

Market Challenges Analysis

High Implementation Costs and Complexity of System Integration

The Manufacturing Carbon Management System Market faces challenges related to high upfront investment and technical integration hurdles. Large manufacturers may absorb costs, but small and medium enterprises struggle to allocate resources for system deployment. It requires significant capital for hardware, software, and workforce training. Integration with existing enterprise resource planning platforms increases complexity and delays adoption. Many firms find the cost of customization too high, especially when managing diverse production environments. This barrier slows adoption rates and limits accessibility across broader segments of the industry.

Limited Standardization and Data Accuracy Issues

The absence of unified global standards creates inconsistencies in carbon reporting practices. Manufacturers often face difficulties aligning internal metrics with varied regional frameworks. It increases the risk of inaccurate emission reporting, undermining regulatory compliance and stakeholder trust. Data collection depends heavily on sensor accuracy and digital connectivity, which remain inconsistent across facilities. Organizations must invest in rigorous verification processes that extend project timelines. These challenges highlight the pressing need for harmonized guidelines and reliable digital infrastructure to improve system efficiency.

Market Opportunities

Expansion of Green Manufacturing and Renewable Integration

The Manufacturing Carbon Management System Market presents significant opportunities through alignment with global green manufacturing initiatives. Governments introduce incentives for industries that adopt renewable energy and carbon-neutral production practices. It creates demand for platforms that can track and validate emission reductions in real time. Manufacturers gain opportunities to optimize operations by linking systems with renewable energy sources such as solar and wind. Transparent reporting of these initiatives strengthens brand positioning with sustainability-focused investors and consumers. This shift positions carbon management systems as an essential enabler of low-carbon industrial growth.

Rising Demand for Digital Twins and Advanced Analytics Applications

The market opens new growth avenues through adoption of digital twins and advanced analytics in carbon management. Digital replicas of manufacturing facilities allow simulation of energy flows and emission scenarios under varied conditions. It provides decision-makers with accurate forecasts that guide investment in cleaner technologies. Companies can identify high-impact interventions that reduce operational costs while meeting emission targets. Expansion of AI-driven analytics offers further opportunities for precise benchmarking and performance optimization. These tools elevate carbon management systems from compliance solutions to strategic assets for competitive advantage.

Market Segmentation Analysis:

By Offering

The Manufacturing Carbon Management System Market segments by offering into software and services. Software platforms dominate adoption because enterprises seek integrated dashboards for data visualization, compliance tracking, and predictive modeling. It enables real-time monitoring across production facilities with scalable features that adapt to regional regulations. Services hold strong potential through consulting, system integration, and managed operations that support long-term compliance. Providers deliver tailored solutions that align with industry-specific requirements, ensuring consistent system performance. The combination of robust software tools and expert services ensures comprehensive adoption across diverse industrial operations.

- For instance, Optera’s carbon management software currently monitors more than 225 million tonnes of CO₂ emissions across approximately 84,000 customer sites providing a single platform.

By Application

Applications cover energy, greenhouse gas management, air quality management, and related sustainability initiatives. Energy management solutions provide immediate operational savings by optimizing fuel and electricity use in production. Greenhouse gas management drives adoption where industries must meet strict emission limits and disclosure requirements. It supports enterprises with automated reporting and accurate measurement of Scope 1, 2, and 3 emissions. Air quality management addresses local regulatory mandates for cleaner environments and aligns with corporate social responsibility goals. Broader applications such as waste management and resource efficiency strengthen overall adoption.

- For instance, BASF’s combined heat and power (CHP) systems have achieved a reduction of 10.8 million MWh in fossil fuel-derived energy while avoiding the equivalent of 2.2 million metric tons of CO₂ emissions demonstrating substantial real-world impact through integrated energy optimization and automation.

By End-User

End users include oil and gas, manufacturing, and healthcare sectors, among others. Oil and gas companies prioritize carbon management platforms due to high emission intensity and stringent reporting requirements. Manufacturing industries drive demand through complex, multi-facility operations that require unified compliance tools. Healthcare organizations adopt these systems to track energy consumption and maintain environmentally responsible operations. It positions carbon management as a strategic necessity across critical sectors with diverse compliance obligations. The Adventure Motorcycle Wheels Market highlights how adjacent industries emphasize sustainability, creating parallels in how adoption trends extend into specialized mobility solutions.

Segments:

Based on Offering:

Based on Application:

- Energy

- Greenhouse Gas Management

- Air Quality Management

Based on End-User:

- Oil and Gas

- Manufacturing

- Healthcare

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Manufacturing Carbon Management System Market with 32% of global revenue. Strong regulatory frameworks from agencies such as the Environmental Protection Agency (EPA) and state-level climate initiatives push companies to adopt advanced carbon tracking platforms. It benefits from early adoption of digital technologies and the presence of leading providers offering integrated solutions across software and services. Manufacturers in automotive, aerospace, and industrial machinery prioritize accurate monitoring to align with net-zero commitments. The region also witnesses growing partnerships between technology vendors and energy companies to address Scope 3 emission disclosures. High awareness among investors and consumers strengthens compliance adoption and secures North America’s leading position.

Europe

Europe accounts for 29% of the Manufacturing Carbon Management System Market, driven by strict European Union directives on emission reduction and sustainability disclosure. Member states enforce aggressive climate neutrality goals, compelling manufacturers to integrate digital carbon management platforms. It benefits from significant demand in heavy industries such as steel, cement, and chemicals, where compliance is central to operations. The region is also a pioneer in certification programs and third-party audits that validate carbon reduction efforts. Technology vendors in Europe increasingly embed predictive analytics and AI-enabled dashboards to help firms manage operational efficiency. High integration of renewable energy into manufacturing processes further drives platform adoption across the continent.

Asia-Pacific

Asia-Pacific secures 24% of the Manufacturing Carbon Management System Market and demonstrates strong growth potential due to industrial expansion in China, India, Japan, and South Korea. Rapid urbanization and industrial output create high emission intensity, generating urgent demand for advanced monitoring and reporting systems. Governments in the region introduce stricter frameworks, including China’s national carbon trading scheme and India’s energy efficiency mandates. It fosters collaboration between domestic manufacturers and international solution providers to deploy scalable carbon management technologies. The region’s electronics, automotive, and heavy industrial sectors represent major adopters. Increasing focus on sustainable supply chains also accelerates system integration across cross-border manufacturing hubs.

Latin America

Latin America contributes 8% to the Manufacturing Carbon Management System Market, supported by gradual enforcement of sustainability standards in Brazil, Mexico, and Argentina. Industrial sectors such as oil and gas, mining, and food processing lead adoption due to their direct exposure to international supply chains. It remains an emerging market where affordability and accessibility are critical adoption drivers. Partnerships with global service providers help local firms integrate cloud-based platforms without heavy capital investments. Renewable energy expansion, particularly in hydropower and solar, creates additional use cases for carbon tracking technologies. Growing alignment with European and North American buyers reinforces adoption of emission reporting standards across industries.

Middle East and Africa

The Middle East and Africa represent 7% of the Manufacturing Carbon Management System Market. The region emphasizes emission management in energy-intensive sectors such as oil and gas, petrochemicals, and mining. Governments implement diversification strategies aligned with national sustainability visions, creating space for carbon management platforms. It witnesses pilot programs in Gulf states where industrial hubs integrate cloud-based systems for accurate reporting. African nations advance slowly but benefit from renewable energy projects that encourage emission transparency. Limited standardization and infrastructure challenges hinder adoption, yet increasing collaboration with global providers drives steady uptake. The focus on energy transition and regulatory modernization ensures long-term opportunities for market growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Enviance

- Accuvio

- EnergyCap

- IBM

- Envirosoft

- Carbon Footprint Ltd.

- Engie

- ESP

- Dakota Software

- Enablon

Competitive Analysis

The Manufacturing Carbon Management System Market is Accuvio, Carbon Footprint Ltd., Dakota Software, Engie, Enablon, EnergyCap, Enviance, Envirosoft, ESP, and IBM. The Manufacturing Carbon Management System Market is defined by strong competition among technology providers that emphasize accuracy, automation, and integration into existing enterprise systems. Vendors prioritize innovation in cloud-based platforms, artificial intelligence, and data analytics to enhance real-time monitoring and predictive capabilities. Companies differentiate by offering scalable solutions that align with diverse regulatory frameworks and industry requirements. Strategic collaborations with industrial clients and energy providers expand market presence while building trust through verified reporting standards. Service portfolios increasingly combine software platforms with consulting, integration, and managed operations to ensure long-term adoption. The competitive environment rewards firms that demonstrate measurable sustainability outcomes, seamless deployment, and strong adaptability across global manufacturing networks.

Recent Developments

- In January 2025, ENGIE is progressing towards carbon-neutral objectives for the Gulf region by responding to an increasing demand in large-scale solar and wind energy projects.

- In March 2024, IBM’s new RFP for climate-adaptive Resilient Cities pledged up to USD 45 million, marking the company’s entry into climate adaptation.

- In August 2024, the U.S. Department of Energy’s Office of Fossil Energy and Carbon Management pledged to spend a total of USD 54.4 million on developing advanced carbon management technology.

- In November 2024, the Australian government launched its third Annual Climate Change Statement in which they decided plans to invest under the Future Made in Australia plan.

Market Concentration & Characteristics

The Manufacturing Carbon Management System Market demonstrates moderate concentration with a mix of global technology providers and specialized regional firms. It is characterized by high entry barriers driven by regulatory expertise, software development capabilities, and the need for integration with enterprise platforms. Larger players dominate through comprehensive portfolios that combine software, services, and compliance solutions, while smaller firms focus on niche applications or regional requirements. It reflects strong demand for cloud-based platforms, artificial intelligence, and predictive analytics that deliver accurate monitoring and reporting of emissions. Buyers emphasize transparency, scalability, and cost efficiency, creating opportunities for providers that align technology with evolving compliance frameworks. The market shows consistent consolidation activity, where strategic partnerships and acquisitions strengthen competitive positioning and expand access to multi-industry clients.

Report Coverage

The research report offers an in-depth analysis based on Offering, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see stronger adoption of AI-driven platforms for real-time emission tracking.

- Cloud-based deployment will continue to dominate due to scalability and remote accessibility.

- Predictive analytics will guide investment decisions in energy efficiency and clean technologies.

- Regulatory frameworks will expand, creating higher compliance requirements for manufacturers.

- Integration with renewable energy systems will become a standard feature of carbon platforms.

- Demand for Scope 3 emission management will grow across global supply chains.

- Third-party verification and certification will play a larger role in market credibility.

- Partnerships between technology providers and industrial clients will accelerate system innovation.

- Small and medium enterprises will increasingly adopt modular and cost-effective solutions.

- Digital twins and IoT-enabled systems will redefine monitoring and forecasting in manufacturing facilities.