Market Overview

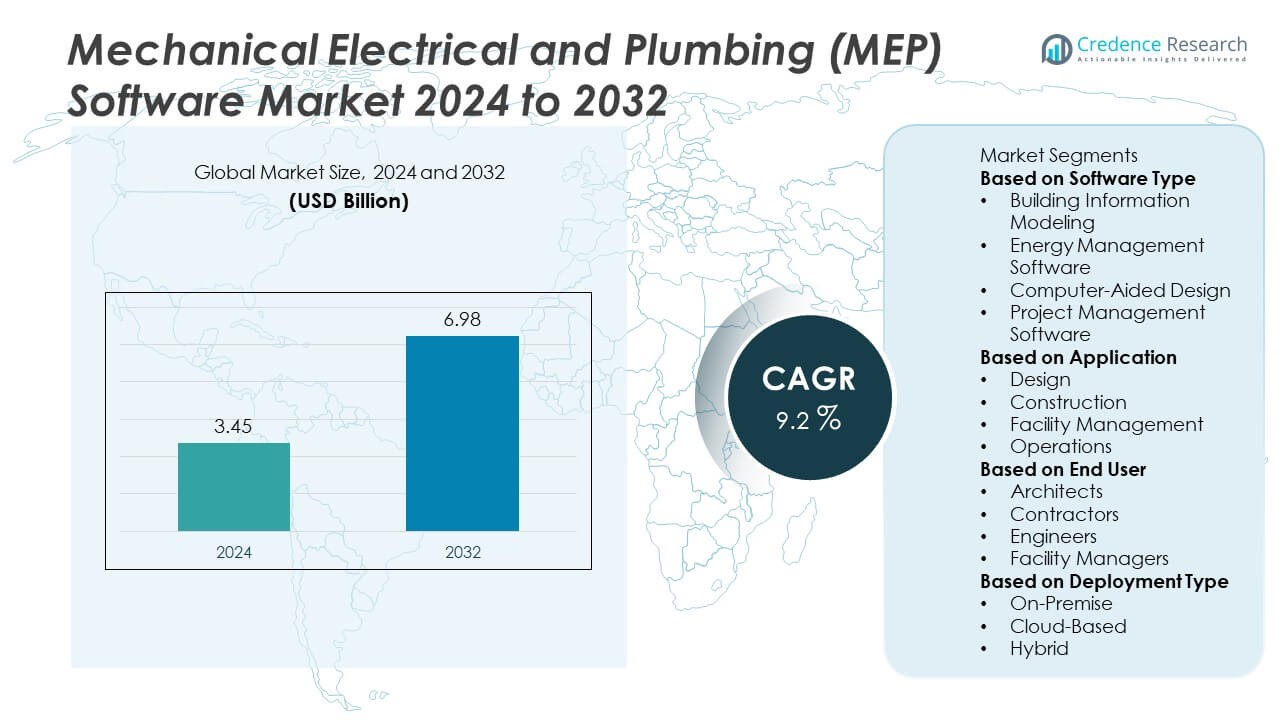

The Mechanical, Electrical, and Plumbing (MEP) Software Market was valued at USD 3.45 billion in 2024 and is projected to reach USD 6.98 billion by 2032, expanding at a CAGR of 9.2% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Mechanical, Electrical, and Plumbing (MEP) Software Market Size 2024 |

USD 3.45 Billion |

| Mechanical, Electrical, and Plumbing (MEP) Software Market, CAGR |

9.2% |

| Mechanical, Electrical, and Plumbing (MEP) Software Market Size 2032 |

USD 6.98 Billion |

The Mechanical Electrical and Plumbing (MEP) Software Market grows steadily, driven by rising adoption of Building Information Modeling (BIM), demand for sustainable construction, and increasing infrastructure projects worldwide. It supports energy-efficient design, regulatory compliance, and reduced project risks through accurate system modeling.

The Mechanical Electrical and Plumbing (MEP) Software Market demonstrates strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America leads adoption through advanced infrastructure projects, high use of BIM, and early integration of cloud-based design platforms. Europe emphasizes sustainable construction, strict regulatory compliance, and rapid deployment of digital solutions in green building initiatives. Asia-Pacific emerges as the fastest-growing region, driven by rapid urbanization, government-led infrastructure programs, and smart city projects. Latin America and the Middle East & Africa are gradually expanding, supported by modernization efforts and investments in commercial and residential construction. Prominent players shaping this market include Autodesk, offering widely used BIM platforms such as Revit, Trimble, known for integrated design and construction solutions, Bentley Systems, specializing in infrastructure-focused modeling tools, and Procore Technologies, which provides cloud-based collaboration software for large-scale construction management.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Mechanical Electrical and Plumbing (MEP) Software Market was valued at USD 3.45 billion in 2024 and is projected to reach USD 6.98 billion by 2032, growing at a CAGR of 9.2% during the forecast period.

- Rising adoption of Building Information Modeling (BIM) and sustainable design practices drives market growth, as contractors and engineers seek accurate modeling solutions to reduce risks and improve project efficiency.

- Key trends include integration of cloud-based platforms, artificial intelligence, and immersive technologies such as virtual reality and augmented reality, which enhance collaboration and enable real-time design validation.

- The competitive landscape is defined by major players such as Autodesk, Trimble, Bentley Systems, and Procore Technologies, which focus on innovation, digital transformation, and global expansion to strengthen their positions.

- High implementation costs, integration complexities, and shortages of skilled professionals act as restraints, limiting adoption among small and medium-sized enterprises and in cost-sensitive regions.

- North America demonstrates strong growth supported by digital infrastructure and early BIM adoption, Europe emphasizes sustainable construction and regulatory compliance, Asia-Pacific emerges as the fastest-growing region due to smart city initiatives, while Latin America and the Middle East & Africa expand gradually with infrastructure modernization.

- Continuous innovation in cloud collaboration, energy-efficient modeling, and scalable digital solutions creates new opportunities, positioning MEP software as a vital enabler of efficient, sustainable, and future-ready construction practices.

Market Drivers

Growing Demand for Building Information Modeling (BIM) in Construction

The Mechanical Electrical and Plumbing (MEP) Software Market is propelled by the increasing adoption of Building Information Modeling (BIM) in modern construction. BIM enables architects, engineers, and contractors to collaborate on integrated digital models that reduce design errors and improve project outcomes. It allows stakeholders to visualize complex systems before installation, ensuring better decision-making. Governments in multiple regions mandate BIM for public infrastructure projects, pushing further adoption. Companies adopt MEP software to improve compliance with these regulations and optimize design accuracy. The trend toward digital transformation in construction strongly supports the use of BIM-enabled MEP platforms.

- For instance, Autodesk reported that its Revit BIM platform is used by over 4 million professionals worldwide, and its automated clash detection reduces rework by up to 40,000 coordination issues per project on large-scale construction sites.

Rising Focus on Energy Efficiency and Sustainable Design

Sustainability is a major driver for the Mechanical Electrical and Plumbing (MEP) Software Market. Energy-efficient building systems require precise design to reduce energy consumption and carbon emissions. It helps engineers simulate HVAC, electrical, and plumbing performance to optimize efficiency. Green building certifications such as LEED and BREEAM encourage the use of advanced software for compliance and validation. Developers rely on these solutions to meet sustainability targets and lower operational costs. The integration of renewable energy systems into building design further accelerates adoption of MEP software.

- For instance, Bentley Systems’ OpenBuildings Energy Simulator was deployed in more than 1,500 projects across 45 countries, helping clients model HVAC and electrical systems that cut annual energy consumption by over 30 GWh in certified green buildings.

Increasing Infrastructure Development and Urbanization

Global urbanization and large-scale infrastructure projects create strong demand for the Mechanical Electrical and Plumbing (MEP) Software Market. Governments invest in smart cities, transportation systems, and large commercial complexes where complex MEP systems are critical. It provides design accuracy and automation that save time and reduce project risks. Construction companies rely on MEP software to coordinate multiple contractors and ensure seamless execution. Growing investments in residential and commercial high-rise buildings further boost demand. The expansion of infrastructure across emerging economies strengthens the long-term outlook for MEP solutions.

Advancements in Cloud-Based and Collaborative Platforms

The Mechanical Electrical and Plumbing (MEP) Software Market benefits from rapid advancements in cloud-based and collaborative design tools. Cloud platforms enable remote access, real-time collaboration, and seamless integration of data across project teams. It improves workflow efficiency by allowing simultaneous updates from architects, engineers, and contractors. Cloud deployment also reduces upfront IT costs, making solutions accessible to mid-sized firms. Growing reliance on mobile devices for field access enhances usability and project coordination. The shift toward cloud-based collaboration ensures continued growth of MEP software adoption.

Market Trends

Adoption of Artificial Intelligence and Automation in Design

The Mechanical Electrical and Plumbing (MEP) Software Market shows a clear trend toward integrating artificial intelligence and automation into design processes. AI-driven tools help engineers detect clashes, optimize layouts, and predict potential failures before installation. It reduces rework and accelerates project timelines while improving accuracy. Automated workflows also enable faster generation of detailed drawings and simulations. This trend enhances productivity in both large-scale projects and mid-sized developments. The use of AI-driven design is becoming a standard feature in competitive MEP solutions.

- For instance, Trimble’s SysQue MEP design platform leverages automation to generate fabrication-ready models and has documented reductions of over 25,000 manual data inputs per project, improving delivery times by up to 30% in large-scale commercial builds.

Expansion of Cloud-Based Collaboration and Remote Access

The Mechanical Electrical and Plumbing (MEP) Software Market benefits from rapid adoption of cloud-based platforms that support real-time collaboration. Cloud integration allows multiple stakeholders to access and update designs simultaneously, reducing delays and miscommunication. It supports remote work environments, making design and review possible from any location. Mobile compatibility further enhances on-site decision-making by providing field engineers with immediate access to updated models. This shift toward cloud collaboration streamlines workflows across distributed teams. Growing reliance on these platforms indicates long-term adoption across the construction industry.

- For instance, Procore Technologies’ cloud collaboration suite connects over 2.7 million construction professionals globally, and its BIM model viewer processes more than 500,000 model interactions per day, ensuring seamless coordination between contractors, engineers, and field teams.

Integration with Sustainable and Smart Building Solutions

The Mechanical Electrical and Plumbing (MEP) Software Market aligns closely with the global shift toward sustainable and smart building practices. Energy-efficient design features are increasingly embedded within MEP software to support compliance with green building certifications. It enables simulations of HVAC performance, water usage, and energy flow to minimize resource consumption. Smart building integration allows systems to adapt to real-time occupancy and usage patterns. Developers use these tools to improve operational efficiency and enhance tenant comfort. This trend ensures that MEP solutions remain central to future-ready construction.

Growing Use of Virtual Reality (VR) and Augmented Reality (AR)

The Mechanical Electrical and Plumbing (MEP) Software Market is witnessing strong adoption of VR and AR technologies for design visualization and project coordination. It allows engineers and contractors to interact with 3D models in immersive environments, improving understanding of complex systems. AR tools enable real-time overlay of digital models on construction sites for precise installation guidance. This reduces errors and enhances efficiency in field execution. Clients also benefit from improved visualization of completed projects before construction begins. The growing role of immersive technologies is redefining collaboration and design validation in MEP workflows.

Market Challenges Analysis

High Implementation Costs and Complexity of Integration

The Mechanical Electrical and Plumbing (MEP) Software Market faces challenges related to high implementation costs and integration complexities. Advanced software platforms require significant investment in licenses, hardware, and training, which limits adoption among small and medium-sized enterprises. It often demands skilled professionals who can handle complex modeling and simulation tasks, increasing overall project costs. Compatibility issues between different software tools also create integration barriers within multi-vendor project environments. Many construction firms struggle to align legacy systems with advanced cloud and BIM platforms. The financial and technical barriers slow down adoption in cost-sensitive markets despite the clear efficiency benefits.

Data Security Concerns and Shortage of Skilled Professionals

The Mechanical Electrical and Plumbing (MEP) Software Market encounters growing concerns about data security and intellectual property protection. Cloud-based platforms, while improving collaboration, expose project data to risks of cyberattacks and unauthorized access. It forces companies to invest in advanced security frameworks, raising operational expenses. Another major challenge is the shortage of skilled professionals capable of utilizing advanced features such as AI-driven design, VR integration, and complex BIM modeling. Many firms rely on traditional methods due to limited workforce expertise in digital construction tools. The combination of cybersecurity risks and talent shortages continues to hinder full-scale adoption across regions.

Market Opportunities

Expansion of Smart Cities and Green Building Initiatives

The Mechanical Electrical and Plumbing (MEP) Software Market presents strong opportunities through the global push for smart cities and sustainable construction. Governments allocate large budgets to infrastructure projects that demand advanced design and monitoring solutions. It enables engineers to model energy-efficient HVAC, electrical, and plumbing systems that align with sustainability targets. Growing adoption of green building certifications such as LEED and BREEAM further drives reliance on precise software for compliance. Smart city initiatives also require advanced integration of IoT-enabled building systems, which depend on accurate MEP modeling. These developments create long-term prospects for software vendors offering sustainable and future-ready solutions.

Rising Adoption in Emerging Economies and Digital Transformation

The Mechanical Electrical and Plumbing (MEP) Software Market benefits from rising adoption in emerging economies where rapid urbanization and infrastructure growth create strong demand. Construction industries in Asia-Pacific, Latin America, and the Middle East invest heavily in digital design tools to manage large-scale projects. It helps contractors and developers reduce costs, improve design accuracy, and accelerate timelines. Cloud-based MEP platforms further open opportunities for mid-sized firms seeking affordable and scalable solutions. Industrial digital transformation also drives demand for advanced features such as AI-based optimization and AR-driven visualization. These opportunities position the market for significant expansion across diverse applications.

Market Segmentation Analysis:

By Software Type

The Mechanical Electrical and Plumbing (MEP) Software Market is segmented by software type into drafting and design software, BIM software, and analysis software. Drafting and design solutions remain widely used for creating 2D and 3D layouts that support accurate system planning. It provides engineers with essential tools for quick schematics and initial project workflows. BIM software represents the fastest-growing segment, offering integrated modeling environments that allow multidisciplinary collaboration across mechanical, electrical, and plumbing systems. Its ability to detect clashes and provide real-time updates positions it as a vital tool for complex infrastructure projects. Analysis software supports energy efficiency and performance simulation, helping developers optimize HVAC, electrical, and water systems for reduced operational costs and regulatory compliance.

- For instance, Glodon’s Cubicost BIM QTO platform updates quantity takeoff automatically across changes and aligns with regional measurement standards, enabling teams to process thousands of item counts in minutes—dramatically cutting manual estimation time.

By Application

The Mechanical Electrical and Plumbing (MEP) Software Market by application includes residential, commercial, and industrial construction. Residential adoption is increasing as urbanization drives demand for high-rise buildings and energy-efficient housing projects. It allows contractors to model plumbing and electrical layouts that enhance safety and reduce costs. The commercial segment shows strong dominance with widespread adoption across office complexes, hospitals, airports, and shopping centers. MEP software ensures accurate planning of critical systems in these environments where safety and efficiency are priorities. Industrial applications expand steadily, driven by manufacturing plants, data centers, and logistics hubs requiring complex and reliable MEP infrastructure. Growing investments in infrastructure development worldwide reinforce the adoption of MEP solutions across all three application categories.

- For instance, Bentley Systems’ OpenBuildings Designer has been used in over 1,800 hospital and airport projects globally, supporting complex HVAC and electrical design that improved operational efficiency by saving more than 15 million labor hours in execution phases.

By End User

The Mechanical Electrical and Plumbing (MEP) Software Market by end user includes contractors, consultants, and engineers. Contractors rely on MEP software to coordinate with multiple stakeholders and manage on-site workflows efficiently. It helps them reduce errors, avoid delays, and control costs through better planning and documentation. Consultants use MEP software for system design validation, compliance checks, and project audits, ensuring clients meet safety and energy efficiency standards. Engineers form a critical user group, leveraging these platforms to model complex systems and deliver optimized layouts across large projects. The software’s ability to integrate data from multiple disciplines makes it an essential tool for improving collaboration between all end-user groups.

Segments:

Based on Software Type

- Building Information Modeling

- Energy Management Software

- Computer-Aided Design

- Project Management Software

Based on Application

- Design

- Construction

- Facility Management

- Operations

Based on End User

- Architects

- Contractors

- Engineers

- Facility Managers

Based on Deployment Type

- On-Premise

- Cloud-Based

- Hybrid

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Mechanical Electrical and Plumbing (MEP) Software Market, accounting for around 34% of global revenue in 2024. The region benefits from early adoption of Building Information Modeling (BIM), strong digital infrastructure, and established construction standards. It shows steady demand across commercial projects, including hospitals, airports, and office complexes where advanced MEP planning is essential. The United States drives growth with large-scale smart city initiatives and strong adoption of cloud-based design platforms. Canada and Mexico also contribute, supported by urban expansion and infrastructure modernization. High levels of investment in sustainable construction and regulatory frameworks that enforce energy efficiency encourage consistent adoption of MEP software.

Europe

Europe represents nearly 28% of the Mechanical Electrical and Plumbing (MEP) Software Market in 2024. The region is driven by strict sustainability regulations and widespread enforcement of energy efficiency directives. Countries such as Germany, the UK, and France lead adoption through advanced use of BIM software in public and private projects. It benefits from strong investments in green building initiatives, which require simulation and analysis tools to reduce carbon emissions. Southern and Eastern Europe show growing adoption as infrastructure modernization projects expand. The mature construction sector in Western Europe continues to upgrade to cloud-based collaboration platforms, which improve project efficiency and compliance. Europe’s focus on achieving carbon neutrality by 2050 further strengthens reliance on advanced MEP software solutions.

Asia-Pacific

Asia-Pacific captures about 23% of the Mechanical Electrical and Plumbing (MEP) Software Market in 2024 and is the fastest-growing region. Rapid urbanization, industrial expansion, and large-scale infrastructure investments fuel demand for advanced design platforms. China leads adoption with significant investments in smart city initiatives and massive urban development projects. India shows strong growth through government-led infrastructure programs and rising demand for high-rise residential complexes. Japan and South Korea demonstrate adoption driven by automation and digital construction practices. It benefits from rising adoption of cloud-based BIM platforms, which reduce costs for mid-sized firms and enhance collaboration across large projects. Asia-Pacific’s strong emphasis on smart, sustainable, and large-scale construction projects positions it as a key growth hub.

Latin America

Latin America accounts for nearly 9% of the Mechanical Electrical and Plumbing (MEP) Software Market in 2024. Growth is supported by increasing investment in commercial construction, particularly in Brazil, Mexico, and Chile. It benefits from the gradual shift toward digital construction practices, though adoption remains uneven across countries. Demand is strongest in large-scale projects such as airports, healthcare facilities, and public infrastructure, where accurate system design is crucial. Limited awareness of advanced BIM platforms and high implementation costs act as barriers in some markets. Government-led modernization programs are expected to improve adoption, creating opportunities for software providers targeting mid-tier construction firms.

Middle East & Africa

The Middle East & Africa holds about 6% of the Mechanical Electrical and Plumbing (MEP) Software Market in 2024, representing a region with significant growth potential. The Middle East, particularly the UAE and Saudi Arabia, invests heavily in mega infrastructure and smart city projects, driving adoption of advanced design tools. Africa shows gradual adoption, supported by urban expansion and improvements in basic infrastructure. It enables contractors and engineers to plan and manage increasingly complex building systems. Energy efficiency regulations in the Gulf region further encourage the use of software to meet sustainability standards. Though the market share is currently smaller compared to other regions, continued infrastructure development creates strong opportunities for expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The competitive landscape of the Mechanical Electrical and Plumbing (MEP) Software Market is defined by leading players such as Autodesk, Trimble, Bentley Systems, Procore Technologies, AVEVA, Oracle, Sage, GRAITEC, Glodon, and DuPont. These companies focus on innovation, strategic partnerships, and expansion into emerging markets to strengthen their positions. Market leadership is influenced by widely adopted BIM platforms that set the standard for integrated design and collaboration, construction technologies that connect hardware, software, and cloud platforms for precise execution, and infrastructure-focused applications that deliver advanced modeling tools for large-scale industrial and commercial projects. Cloud-based collaboration platforms further enhance competitiveness by streamlining workflows and improving project visibility. Engineering design suites increasingly integrate MEP functionalities, while enterprise-level project management and financial solutions complement workflows to deliver end-to-end project efficiency. Specialized regional and niche offerings add value through design automation and cost estimation tools, while material science integration into design solutions provides a unique differentiator. Overall, competition revolves around delivering scalable, cloud-enabled, and collaborative platforms that reduce costs, improve energy efficiency, and enhance accuracy in complex building projects.

Recent Developments

- In June 2025, Autodesk released a security-focused update for AutoCAD MEP 2025, addressing critical vulnerabilities.

- In June 2025, Bentley Systems launched its 2025 iTwin4Good Challenge inviting university students worldwide to develop digital twin solutions that aim to address modern infrastructure challenges—highlighting Bentley’s emphasis on innovation in infrastructure and engineering domains.

- In December 2024, Oracle released Oracle Forms and Reports version 14.1.2.0, featuring modernized widgets and built-in support for REST data sources—offering enhanced platform capabilities that benefit MEP-related workflows.

- In October 2024, GRAITEC established a strategic partnership with MSUITE, enhancing its support for BIM-to-FAB workflows specifically tailored to the MEP community.

Market Concentration & Characteristics

The Mechanical Electrical and Plumbing (MEP) Software Market demonstrates moderate to high concentration, with global leaders and specialized vendors shaping competition through innovation and strong regional presence. Major companies such as Autodesk, Trimble, Bentley Systems, and Procore Technologies dominate the landscape with comprehensive BIM platforms, cloud-enabled collaboration tools, and integrated design solutions. It reflects characteristics of a technology-driven market where precision, interoperability, and compliance with building codes define competitive advantage. Vendors invest heavily in artificial intelligence, automation, and immersive technologies to improve accuracy and streamline project execution. Smaller players contribute by offering niche solutions that address regional standards and industry-specific workflows. The market is strongly influenced by government mandates for BIM adoption, sustainability goals, and increasing demand for energy-efficient building design. High entry barriers exist due to the need for advanced R&D capabilities, software expertise, and strong distribution networks. It continues to evolve toward cloud-based, scalable, and collaborative platforms that align with the digital transformation of the construction industry.

Report Coverage

The research report offers an in-depth analysis based on Software Type, Application, End User, Deployment Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for integrated BIM and design automation will grow across complex infrastructure projects.

- Cloud-based, collaborative platforms will gain broader adoption among remote and distributed project teams.

- Embedded AI tools will streamline clash detection, energy optimization, and system coordination in MEP workflows.

- VR and AR applications will become more common for immersive walkthroughs and on-site design validation.

- Adoption of mobile design applications will increase, enabling real-time access and updates during field operations.

- Software providers will embed sustainability analysis tools to support green certifications and energy-efficient designs.

- Integration with digital twin platforms will enhance predictive maintenance and continuous system monitoring.

- Mid-sized firms in emerging markets will adopt scalable, subscription-based MEP solutions for affordability and flexibility.

- Cross-industry collaborations will expand adoption of MEP software in sectors such as healthcare, data centers, and industrial facilities.

- Software vendors will enhance API support to improve interoperability with enterprise systems like ERP and project management tools.