Market Overview

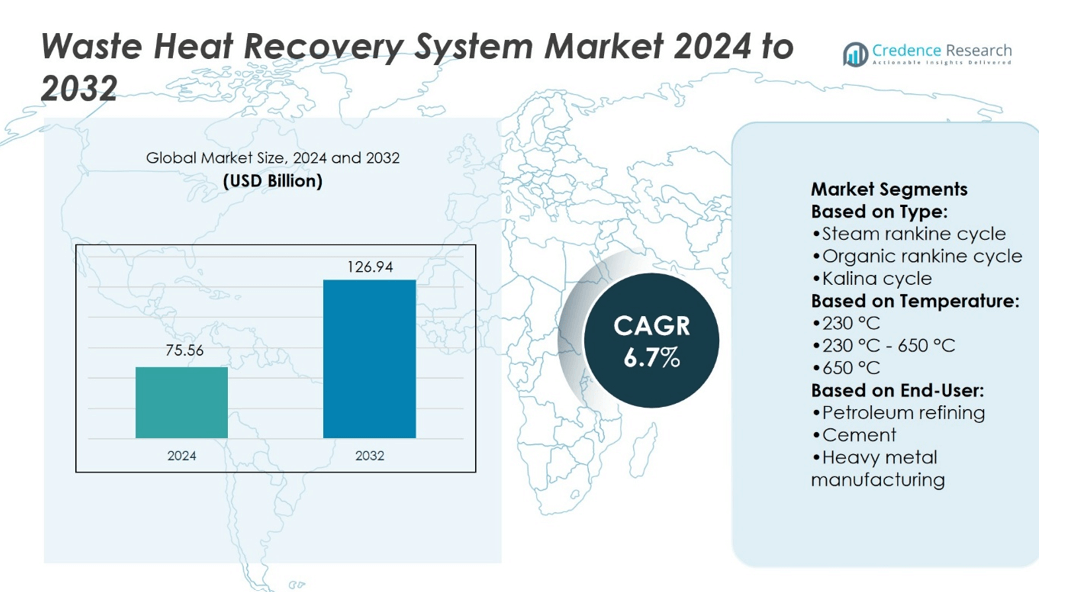

Waste Heat Recovery System Market size was valued at USD 75.56 billion in 2024 and is anticipated to reach USD 126.94 billion by 2032, at a CAGR of 6.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Waste Heat Recovery System Market Size 2024 |

USD 75.56 billion |

| Waste Heat Recovery System Market, CAGR |

6.7% |

| Waste Heat Recovery System Market Size 2032 |

USD 126.94 billion |

The Waste Heat Recovery System Market grows through strong drivers and evolving trends shaping global demand. Rising focus on energy efficiency and sustainability goals pushes industries to adopt advanced recovery solutions. Governments enforce strict emission regulations, creating incentives for technology integration across petroleum refining, cement, chemical, and heavy metal sectors. Expanding industrial operations in emerging economies strengthen adoption, while digital tools such as IoT and AI enhance efficiency and monitoring. Modular and scalable system designs attract small and medium enterprises, while integration with renewable energy projects broadens application scope. These factors together drive consistent growth and innovation in the market.

The Waste Heat Recovery System Market shows strong presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific leads with rapid industrialization, while North America and Europe benefit from strict energy efficiency policies and advanced technologies. Latin America and the Middle East & Africa display gradual but steady adoption through refining and cement industries. Key players such as AURA, Bosch Industriekessel GmbH, Climeon, Durr Group, Exergy International SRL, and General Electric drive competition with innovative solutions.

Market Insights

- The Waste Heat Recovery System Market was valued at USD 75.56 billion in 2024 and is projected to reach USD 126.94 billion by 2032, growing at a CAGR of 6.7%.

- Rising demand for energy efficiency and sustainability goals drives strong adoption across industries.

- Governments enforce strict emission norms, encouraging integration of advanced recovery systems in key sectors.

- Trends highlight growing use of IoT, AI, and modular system designs to enhance efficiency.

- Competition remains intense with players focusing on innovation, scalability, and regional expansion strategies.

- High capital costs and long payback periods act as restraints for small and medium enterprises.

- Asia-Pacific leads with rapid industrialization, North America and Europe show advanced adoption, while Latin America and Middle East & Africa record gradual growth through refining and cement industries.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Energy Efficiency and Sustainability Goals

The Waste Heat Recovery System Market benefits from the global focus on energy efficiency. Industries face growing pressure to optimize resources and minimize waste. Many organizations view heat recovery systems as a direct method to cut emissions. It reduces dependency on primary energy sources while supporting carbon reduction targets. Governments and corporations align sustainability goals with system adoption. Demand continues to rise as businesses integrate eco-friendly solutions into operations.

- For instance, Exergy International installed around 60 ORC power plants and amassed nearly 500 MWe total capacity. These systems help reduce emissions, lower reliance on primary energy, and align with sustainability targets.

Expanding Industrial Applications Across Multiple Sectors

The Waste Heat Recovery System Market gains momentum through broad adoption across manufacturing, oil and gas, and power generation. Heavy industries consume high energy volumes, making waste heat recovery a strategic necessity. It enables factories to reduce fuel consumption while enhancing operational efficiency. Steel, cement, and chemical sectors actively deploy advanced systems to reclaim heat from kilns and furnaces. Growth also stems from food processing and refining plants seeking energy cost reduction. The diverse applications ensure consistent market expansion across global industries.

- For instance, Bosch’s Universal Heat Recovery Steam Boiler (HRSB) delivers 400 to 4,100 kg/h of saturated steam, operates under 10 or 16 bar pressure, and handles flue gas up to 550 °C, with flows from 500 to 23,500 kg/h.

Supportive Government Regulations and Incentive Programs

The Waste Heat Recovery System Market strengthens through regulatory frameworks and financial incentives. Many governments introduce strict emission norms that encourage adoption of recovery technologies. Incentive programs such as tax credits and subsidies further promote system investments. It provides industries with financial relief and accelerates payback periods. Energy conservation laws in developed regions strongly support implementation. Emerging economies also establish favorable policies to drive sustainable industrial growth. These measures ensure steady expansion across both advanced and developing markets.

Technological Advancements and Improved System Designs

The Waste Heat Recovery System Market experiences strong growth through continuous technological innovation. Advanced system designs improve efficiency, reliability, and scalability across industries. It integrates with modern equipment, enabling better monitoring and optimization of recovered heat. Compact designs reduce installation challenges in space-constrained facilities. Emerging digital solutions enhance predictive maintenance and performance tracking. Continuous R&D investments provide systems with higher efficiency levels, driving wider adoption globally. These advancements secure the long-term relevance of waste heat recovery solutions.

Market Trends

Growing Integration with Renewable and Clean Energy Solutions

The Waste Heat Recovery System Market shows a strong trend toward integration with renewable energy. Companies explore hybrid systems that combine waste heat recovery with solar, wind, or biomass energy. It strengthens sustainability efforts while lowering reliance on fossil fuels. Industrial operators increasingly align heat recovery with broader clean energy initiatives. This trend positions waste heat systems as a complementary solution in decarbonization strategies. Growing investments in renewable infrastructure further support adoption of integrated recovery technologies.

- For instance, GE’s ORegen system generated 14 MW of electricity from waste heat at a compressor station, using no additional fuel, water, or emissions. In another case, GE’s 7HA.02 turbines at Ohio’s Guernsey Power Station use waste heat to power steam turbines. The plant delivers 1.875 GW total output, serving 1.4 million homes.

Rising Adoption of Advanced Digital and Automation Technologies

The Waste Heat Recovery System Market expands through the use of automation, IoT, and AI-based monitoring tools. Digital platforms enable real-time tracking of heat recovery efficiency. It helps operators identify faults, optimize operations, and extend system lifespan. Smart sensors and predictive analytics deliver significant performance gains. Industrial users value the reduced downtime and improved output from automated systems. This trend ensures higher adoption across both established and emerging industries.

- For instance, Cochran’s case study at Evolve Polymers, Hemswell shows a modular heat recovery boiler capturing exhaust from two gas engines (at over 460 °C) and generating 2 tonnes of steam per hour.

Increasing Demand from Energy-Intensive Industries

The Waste Heat Recovery System Market records strong demand from cement, steel, glass, and chemical industries. Energy-intensive operations create large volumes of recoverable heat. It drives steady investments in recovery systems to reduce costs and emissions. Expansion of heavy industrial projects in Asia-Pacific strengthens market growth. North American and European industries focus on compliance with strict emission standards. The trend reinforces the role of waste heat recovery as a core efficiency measure.

Shift Toward Modular and Scalable System Designs

The Waste Heat Recovery System Market experiences a trend toward modular, flexible system designs. Manufacturers offer scalable solutions that fit facilities of different sizes. It improves accessibility for small and medium enterprises seeking efficiency gains. Modular systems reduce installation time and lower upfront costs. Growing demand for customized configurations supports broader adoption across varied industries. This trend enhances the long-term growth outlook of waste heat recovery technologies.

Market Challenges Analysis

High Capital Costs and Long Payback Periods Restrict Adoption

The Waste Heat Recovery System Market faces a major challenge from high upfront investment requirements. Many systems demand significant capital for installation, engineering, and integration into existing infrastructure. It creates hesitation among small and medium enterprises with limited budgets. The long payback period further discourages rapid adoption, especially in industries with tight margins. Complex financing structures and limited access to incentives in some regions add pressure. These cost-related barriers restrict broader market penetration despite clear long-term benefits.

Technical Limitations and Operational Complexities Impact Performance

The Waste Heat Recovery System Market also struggles with technical constraints that limit efficiency. Systems often face challenges in capturing low-grade heat, reducing overall energy recovery potential. It requires advanced designs and materials that increase project complexity. Operational issues such as maintenance downtime and integration difficulties disrupt efficiency. Industries with variable heat flows find it difficult to achieve consistent recovery levels. These technical and operational hurdles slow adoption across diverse industrial environments.

Market Opportunities

Expanding Role in Global Sustainability and Decarbonization Efforts

The Waste Heat Recovery System Market holds strong opportunities through alignment with global climate goals. Nations commit to carbon neutrality targets, pushing industries to reduce emissions. It enables companies to achieve energy efficiency while meeting sustainability benchmarks. Growing interest in circular economy practices further boosts demand for recovery systems. Industries recognize the dual benefit of cost savings and compliance with green standards. The rising focus on cleaner production ensures steady expansion of adoption worldwide.

Emerging Applications in Developing Economies and New Sectors

The Waste Heat Recovery System Market also gains opportunities from growth in developing regions. Expanding industrial bases in Asia-Pacific, Latin America, and Africa create high demand for energy-saving solutions. It allows local industries to cut fuel costs while improving competitiveness. New applications in data centers, commercial facilities, and district heating broaden the scope. Governments in emerging markets support adoption through policy incentives and infrastructure investments. These opportunities expand market reach beyond traditional heavy industries.

Market Segmentation Analysis:

By Type

The Waste Heat Recovery System Market divides into steam Rankine cycle, organic Rankine cycle, and Kalina cycle. The steam Rankine cycle dominates due to its maturity and efficiency in handling high-temperature applications. It finds widespread use in heavy industries such as cement, steel, and refining. The organic Rankine cycle shows strong growth as industries adopt it for low- to medium-temperature heat recovery. Its flexibility and ability to use diverse working fluids make it suitable for smaller facilities. The Kalina cycle, though less established, attracts attention for its superior efficiency in low-temperature operations. Ongoing advancements may enhance its adoption in niche sectors.

- For instance, the Heat Power 300 module generates 50–355 kW net power, absorbing 1,000–4,500 kW of thermal energy per unit, and scales to multi‑unit systems. In another real‑world application, a HeatPower 300 unit at NEO GROUP’s PET plant in Lithuania produced 2,700 MWh of clean electricity in one year.

By Temperature

The Waste Heat Recovery System Market segments into below 230 °C, 230 °C–650 °C, and above 650 °C. The 230 °C–650 °C range leads due to its alignment with common industrial processes. It is particularly suited for steel, cement, and chemical production lines. The below 230 °C segment grows steadily as industries explore solutions for low-grade heat recovery. The use of advanced cycles such as Kalina supports this category. Heat above 650 °C, though smaller in share, offers significant potential in energy-intensive industries. High-temperature recovery delivers superior efficiency gains, driving investments in specialized systems.

- For instance, AURA’s Turbine Waste Heat Recovery Unit (WHRU) handles flue gas up to 430 °C, with a thermal oil output up to 15,000 kW and exemplary systems achieving 12,000 kW output. Additionally, its steam generator modules operate between 130 °C and 230 °C, delivering up to 5 MW of steam output.

By End User

The Waste Heat Recovery System Market includes petroleum refining, cement, heavy metal manufacturing, and chemical sectors. Petroleum refining stands out as a leading adopter due to high energy consumption and emission targets. Cement producers invest heavily in waste heat recovery to lower costs and meet sustainability requirements. It enables consistent recovery from kilns, making the segment highly attractive. Heavy metal manufacturing also integrates these systems to manage rising energy costs and strict environmental norms. The chemical sector leverages recovery systems to improve operational efficiency and support clean production practices. Each end user segment reinforces the long-term demand for advanced recovery technologies.

Segments:

Based on Type:

- Steam rankine cycle

- Organic rankine cycle

- Kalina cycle

Based on Temperature:

- 230 °C

- 230 °C – 650 °C

- 650 °C

Based on End-User:

- Petroleum refining

- Cement

- Heavy metal manufacturing

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds a market share of around 32% in the Waste Heat Recovery System Market, making it one of the leading regions. Strong environmental regulations and energy efficiency mandates drive adoption across industries such as petroleum refining, chemicals, and heavy metals. It benefits from strict frameworks by agencies like the Environmental Protection Agency (EPA), which enforce emission controls and encourage investment in clean technologies. The United States dominates the regional share, supported by large-scale industrial operations and a strong focus on sustainability. Canada follows with steady adoption in oil and gas processing and heavy industries, leveraging recovery systems to cut energy costs. Growing partnerships between technology providers and industrial users strengthen market maturity in this region. Continuous investment in advanced systems ensures North America maintains its leadership in the global landscape.

Europe

Europe accounts for approximately 28% of the global Waste Heat Recovery System Market, reflecting its strong commitment to decarbonization and renewable energy integration. The region’s emphasis on circular economy principles makes waste heat recovery central to industrial strategy. It finds robust demand in cement, steel, and chemical industries across Germany, the UK, and France. The European Union’s energy efficiency directives support wide deployment of recovery systems to meet sustainability goals. Northern European countries adopt advanced Kalina and organic Rankine cycles for low-temperature applications, reflecting a trend toward innovative solutions. Eastern Europe also shows progress, with rising industrial activity and modern infrastructure investments creating opportunities. Collaboration between governments, industry, and research organizations positions Europe as a technology-driven market. The focus on carbon neutrality by 2050 reinforces long-term growth prospects in this region.

Asia-Pacific

Asia-Pacific leads with the largest market share of about 34% in the Waste Heat Recovery System Market, supported by rapid industrialization and expanding energy demand. China holds a dominant position due to its massive steel, cement, and refining industries. It heavily invests in waste heat recovery technologies to manage energy consumption and environmental pressures. India follows with strong growth, driven by government initiatives promoting sustainable manufacturing and cost reduction. Japan and South Korea adopt advanced technologies, including organic Rankine cycles, to align with their carbon-neutral commitments. Southeast Asian nations, including Indonesia and Vietnam, expand adoption in cement and refining sectors as industrial bases grow. The region’s rising population and urbanization further drive demand for efficient energy systems. Asia-Pacific maintains its leadership through large-scale adoption, supportive policies, and rapid technological advancement.

Latin America

Latin America captures nearly 4% of the Waste Heat Recovery System Market, reflecting slower but steady adoption. Brazil leads in regional share, supported by expanding cement and refining sectors. It adopts waste heat recovery technologies to cut operational costs and reduce reliance on imported fuels. Mexico also contributes, with strong uptake in petroleum refining and chemical industries. It faces challenges from limited capital investment and uneven regulatory frameworks. However, regional governments increasingly promote clean technologies to enhance sustainability. Emerging industries in Chile, Argentina, and Colombia explore recovery systems to align with green development agendas. The region’s market growth is gradual but offers potential with expanding industrial modernization.

Middle East & Africa

The Middle East & Africa hold a combined market share of about 2% in the Waste Heat Recovery System Market. Adoption is primarily concentrated in Gulf countries such as Saudi Arabia, the UAE, and Qatar. It focuses on petroleum refining and petrochemical sectors, where energy intensity is high. Strong government-backed industrial diversification programs encourage investment in waste heat recovery. Africa, though at an early stage, shows opportunities in cement and mining industries, particularly in South Africa. Limited financial resources and infrastructure challenges slow broader adoption across the region. However, rising industrialization and environmental policies may accelerate growth over time. The Middle East & Africa, though smaller in scale, remain strategically important due to energy-intensive industries and long-term development goals.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The competitive landscape of the Waste Heat Recovery System Market players include AURA, BIHL, Bosch Industriekessel GmbH, Climeon, Cochran, Durr Group, Exergy International SRL, Forbes Marshall, Fortum, and General Electric. The Waste Heat Recovery System Market is highly competitive, driven by continuous innovation and efficiency improvements. Companies focus on developing systems that maximize energy utilization while meeting strict environmental regulations. Strong emphasis is placed on modular and scalable designs that suit both large and mid-sized industrial operations. Growing demand for digital integration, including IoT-based monitoring and predictive analytics, further shapes competition. Firms also expand their global reach through partnerships, acquisitions, and regional projects to strengthen market presence. The push toward sustainability and carbon neutrality ensures ongoing investment in advanced recovery solutions. This dynamic environment encourages continuous improvement and supports long-term industry growth.

Recent Developments

- In February 2025, Climeon commissioned its first land-based HeatPower genset at Landmark Power Holdings’ Rhodesia plant in the UK, demonstrating the potential of ORC-based waste heat recovery for efficient, low-carbon power generation in flexible gas engine plants.

- In February 2025, Siemens Energy, and NEM Energy signed a new deal in order to deliver two horizontal Heat Recovery Steam Generators (HRSGs) for a new combined cycle power plant in Texas, USA. An estimated 1.2 GW will be produced by the facility when it is finished.

- In October 2024, Exergy international and Clean Energy Technologies, Inc signs an MOU to promote ORC Heat Recovery Solutions throughout the Americas and nearby locations. This strategic collaboration seeks to propel growth in the heat recovery solutions industry.

- In September 2024, Thermax teamed up with Ceres Power to produce large-scale Solid Oxide Electrolysis Cells (SOECs), which are a piece of equipment used to produce green hydrogen. Through this collaboration, Thermax will use its vast knowledge of waste heat recovery and heat integration to design, engineer, and develop SAM balance of module (SBM), a foundational element for the subsequent development of a multi-MW SOEC electrolyser module.

Report Coverage

The research report offers an in-depth analysis based on Type, Temperature, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with rising demand for energy-efficient industrial solutions.

- Adoption will grow as stricter emission regulations push industries toward sustainability.

- Integration with renewable energy projects will enhance long-term relevance.

- Advanced digital tools will improve monitoring, maintenance, and efficiency of systems.

- Modular and scalable designs will increase adoption among small and medium industries.

- Low-temperature recovery technologies will gain momentum in diverse applications.

- Heavy industries such as cement and steel will remain major adopters.

- Emerging economies will offer strong growth opportunities through industrial expansion.

- Strategic collaborations and R&D investments will drive technological innovation.

- Global decarbonization goals will secure steady demand for waste heat recovery systems.