Market Overview

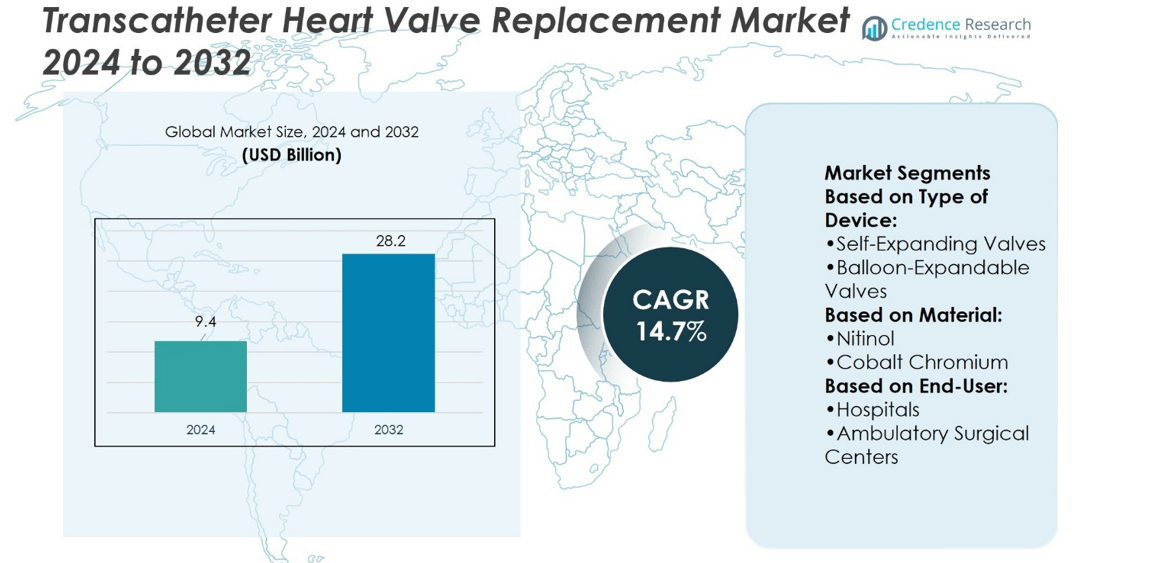

Transcatheter Heart Valve Replacement Market size was valued at USD 9.4 billion in 2024 and is anticipated to reach USD 28.2 billion by 2032, at a CAGR of 14.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Transcatheter Heart Valve Replacement Market Size 2024 |

USD 9.4 billion |

| Transcatheter Heart Valve Replacement Market, CAGR |

14.7% |

| Transcatheter Heart Valve Replacement Market Size 2032 |

USD 28.2 billion |

The Transcatheter Heart Valve Replacement Market grows with rising demand for minimally invasive cardiac procedures that reduce recovery time and hospital stays. Increasing prevalence of valvular heart diseases among aging populations drives adoption. Advancements in valve design, including self-expanding and balloon-expandable technologies, improve procedural safety and long-term outcomes. Growing physician preference for catheter-based solutions supports expansion into high-risk and intermediate-risk patient groups. Favorable regulatory approvals and expanding clinical trial evidence strengthen market acceptance. Technological integration, such as advanced imaging and digital planning tools, enhances precision and success rates, positioning TAVR as a transformative option in modern cardiovascular treatment strategies.

North America holds the largest share of the Transcatheter Heart Valve Replacement Market, driven by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong reimbursement policies. Europe follows with significant demand supported by aging demographics and clinical research activities. Asia Pacific shows rapid growth due to expanding healthcare access and rising cardiovascular disease cases. Key players shaping the market landscape include Abbott, Medtronic, Edwards Lifesciences Corporation, and Boston Scientific Corporation, focusing on innovation, clinical trials, and strategic collaborations.

Market Insights

- Transcatheter Heart Valve Replacement Market size was valued at USD 9.4 billion in 2024 and is anticipated to reach USD 28.2 billion by 2032, at a CAGR of 14.7%.

- Rising demand for minimally invasive cardiac procedures is a key driver of growth.

- Growing prevalence of valvular heart diseases among aging populations supports wider adoption.

- Advancements in valve technologies, including self-expanding and balloon-expandable devices, shape market trends.

- Strong competition exists among Abbott, Medtronic, Edwards Lifesciences Corporation, and Boston Scientific Corporation, focusing on innovation and clinical trials.

- High procedural costs and limited access in low-income regions remain major restraints.

- North America leads the market, Europe follows with significant share, and Asia Pacific shows fastest growth due to rising healthcare investments and cardiovascular disease cases.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Growing Burden of Cardiovascular Diseases Driving Adoption

The Transcatheter Heart Valve Replacement Market is propelled by the rising prevalence of cardiovascular diseases, particularly aortic stenosis among aging populations. It benefits from the increasing number of patients who are unfit for open-heart surgery due to comorbidities. Rising life expectancy and lifestyle-related conditions heighten the demand for less invasive procedures. Healthcare providers favor transcatheter solutions for faster recovery and improved patient outcomes. The growing clinical evidence supporting safety and efficacy boosts physician confidence in recommending this procedure. Expanding patient awareness further supports adoption across developed and emerging markets.

- For instance, Meril Life Sciences’ Myval transcatheter heart valve has been implanted in over 8,000 patients across more than 70 centers globally, showing high device success and supporting reduced hospital stays, consistent with positive clinical outcomes observed in studies.

Technological Innovations Supporting Broader Clinical Applications

Advances in valve design, imaging guidance, and catheter delivery systems strengthen the growth of the Transcatheter Heart Valve Replacement Market. It is supported by improvements that minimize complications, enhance durability, and increase suitability for diverse patient groups. Expansion into low- and intermediate-risk patient categories broadens the treatment base. Strong R&D efforts from leading medical device companies drive continuous innovation. Clinical trials validate next-generation devices, reinforcing acceptance by regulators and practitioners. Enhanced durability and reduced reintervention rates make transcatheter procedures a compelling choice in cardiovascular care.

- For instance, MicroPort Scientific Corporation’s VitaFlow transcatheter aortic valve system has been implanted in more than 10,000 patients across multiple regions, demonstrating consistent device performance and reduced complication rates.

Regulatory Approvals and Reimbursement Policies Expanding Access

The Transcatheter Heart Valve Replacement Market benefits from favorable regulatory approvals and expanding reimbursement frameworks across key regions. It gains momentum as agencies recognize the procedure’s clinical and economic value. National health systems and private insurers adopt supportive coverage, enabling greater patient access. Government initiatives targeting advanced cardiac care improve procedure availability in hospitals and specialty clinics. Streamlined approval pathways accelerate the introduction of next-generation devices. The combination of regulatory support and coverage incentives ensures stronger adoption across both developed and developing economies.

Rising Hospital Investments and Specialist Training Programs

Growing investments in hospital infrastructure and specialist training programs support the growth of the Transcatheter Heart Valve Replacement Market. It advances as medical centers adopt hybrid operating rooms and advanced imaging systems. Healthcare providers prioritize skilled workforce development to handle complex cardiovascular procedures. Collaborative training programs between manufacturers and hospitals ensure higher procedural success rates. Increased adoption by specialty centers improves patient trust and referral patterns. Rising procedural volumes encourage more hospitals to expand transcatheter offerings. These developments collectively strengthen the long-term growth outlook for the market.

Market Trends

Expansion Toward Low- and Intermediate-Risk Patient Groups

The Transcatheter Heart Valve Replacement Market is witnessing a clear shift toward treating lower-risk patient categories. It benefits from strong clinical trial outcomes demonstrating safety and efficacy across broader populations. Physicians increasingly recommend transcatheter approaches for patients previously managed through surgical options. This expansion enlarges the eligible patient pool, driving procedural volume across hospitals and specialty centers. The trend underscores growing physician confidence and patient preference for less invasive care. It also strengthens the long-term demand trajectory for advanced valve replacement solutions.

- For instance, Boston Scientific LOTUS Edge valve system demonstrated a 99% successful implantation rate and low paravalvular leak rates in clinical trials, the product was voluntarily recalled and discontinued.

Integration of Advanced Imaging and Navigation Technologies

The Transcatheter Heart Valve Replacement Market gains momentum through integration of cutting-edge imaging modalities and navigation systems. It is supported by real-time imaging that enables precise valve placement and reduces complication risks. Hospitals adopt advanced echocardiography, CT, and fluoroscopy technologies to improve outcomes. Device makers design delivery systems compatible with these imaging tools, enhancing procedural accuracy. This trend accelerates acceptance in complex and high-risk cases. It also establishes a pathway for more efficient training and standardization of procedures globally.

- For instance, JenaValve Technology, Inc.’s Trilogy THV system in the ALIGN-AR trial achieved device success in over 95% of 500 high-risk aortic regurgitation patients, with 0% procedural death, 1.4% mortality at 30 days, 1.6% valve embolization, and 0.8% disabling stroke, all confirmed via advanced imaging and navigation technologies.

Focus on Next-Generation Valve Durability and Design

The Transcatheter Heart Valve Replacement Market continues to evolve with the development of next-generation devices emphasizing durability. It is driven by innovations aimed at extending valve life and minimizing reinterventions. Manufacturers introduce improved leaflet materials, anti-calcification treatments, and smaller delivery systems. These advancements expand suitability for younger patient populations requiring long-term performance. Growing clinical evidence validates device reliability, supporting stronger adoption in competitive settings. It reinforces the market’s position as a transformative segment in cardiovascular care.

Growing Collaborations Between Hospitals and Device Manufacturers

The Transcatheter Heart Valve Replacement Market is shaped by rising collaborations between healthcare providers and medical device companies. It benefits from partnerships that support training, data sharing, and clinical research. Hospitals engage in multicenter trials, generating evidence for broader adoption. Manufacturers invest in education programs that improve physician skill levels and procedural consistency. These collaborations accelerate regulatory acceptance and reimbursement policy development. It ensures the technology’s integration into mainstream cardiovascular treatment pathways worldwide.

Market Challenges Analysis

High Procedure Costs and Limited Accessibility Across Regions

The Transcatheter Heart Valve Replacement Market faces challenges from high procedural costs and limited accessibility in several regions. It requires advanced facilities, specialized equipment, and skilled professionals, raising overall treatment expenses. Reimbursement remains uneven, with many healthcare systems offering partial or no coverage. This restricts adoption in price-sensitive markets, where patients cannot afford out-of-pocket payments. Hospitals in low- and middle-income regions often lack infrastructure to support complex interventions. The imbalance between developed and emerging economies creates disparities in access, slowing global adoption despite strong clinical outcomes.

Clinical Risks, Device Limitations, and Regulatory Complexities

The Transcatheter Heart Valve Replacement Market also contends with clinical risks, device limitations, and regulatory complexities. It carries potential complications such as paravalvular leaks, valve migration, and long-term durability concerns. Limited availability of devices for unique anatomies reduces treatment suitability for certain patients. Regulatory bodies demand extensive clinical evidence, lengthening approval timelines and raising R&D costs. Physicians require continuous training to handle evolving technologies, adding further burden on healthcare systems. These challenges collectively restrain the pace of market expansion, even as technological progress addresses several barriers.

Market Opportunities

Rising Demand from Expanding Patient Pool and Early Diagnosis

The Transcatheter Heart Valve Replacement Market holds strong opportunities due to the rising prevalence of aortic stenosis and broader adoption of early diagnostic practices. It benefits from increasing detection of heart valve diseases among aging populations and patients with comorbidities. Advancements in screening programs and imaging technologies identify candidates at earlier stages, widening the treatment base. Growing physician confidence supports expansion into low- and intermediate-risk patient groups. Healthcare providers prioritize less invasive procedures to shorten recovery and improve patient outcomes. These trends create a large and sustainable opportunity for transcatheter interventions across global healthcare systems.

Emerging Markets and Strategic Industry Collaborations Driving Growth

The Transcatheter Heart Valve Replacement Market also gains opportunities from growing demand in emerging economies and strategic industry collaborations. It expands as governments and private hospitals invest in advanced cardiac care infrastructure. Partnerships between manufacturers and healthcare providers enhance training, improve procedural success, and speed adoption. Device makers focus on smaller, flexible, and durable valve systems that address diverse anatomical needs. Expanding clinical trial networks generate data supporting faster regulatory approvals worldwide. These opportunities position the market for significant long-term growth while strengthening access to advanced cardiovascular solutions.

Market Segmentation Analysis:

By Type of Device

The Transcatheter Heart Valve Replacement Market is segmented by type of device into self-expanding valves, balloon-expandable valves, and others. Self-expanding valves hold a strong position due to their flexibility and ease of deployment in complex anatomies. It supports reduced complications in patients with heavily calcified vessels or irregular structures. Balloon-expandable valves remain widely adopted for their precision in placement and favorable clinical outcomes. They are preferred in patients with stable anatomy where controlled deployment is critical. The “others” category includes emerging hybrid designs that combine flexibility with durability, reflecting ongoing innovation in device technology. This segmentation highlights the diversity of treatment options tailored to patient needs.

- For instance, Abbott’s Portico system, specifically when used with the FlexNav delivery system, has shown favorable clinical outcomes, including high procedural success rates and good performance in patients with varied anatomies. However, a claimed 99.3% implantation success rate and 0% valve embolization are not supported by evidence from specific clinical studies.

By Material

Segmentation by material includes nitinol, cobalt chromium, and others. Nitinol dominates this segment due to its shape-memory properties, corrosion resistance, and biocompatibility. It supports flexibility during deployment while ensuring durability inside the patient’s body. Cobalt chromium offers strength and thinner struts, enabling compact valve designs and smoother delivery through catheters. The “others” category covers stainless steel and novel alloys under development to extend valve life and reduce complications. It reflects strong focus on material science to improve performance and patient safety. This material-based segmentation underscores the role of advanced metals in shaping the future of valve replacement devices.

- For instance, Bracco’s HeartSee v4.0 enables subendocardial ischemia mapping and stress flow assessment in each PET scan, while VUEWAY® has now been administered in over 1 million patient injections across more than 480 facilities, offering efficient contrast clarity at a reduced gadolinium yield.

By End User

The Transcatheter Heart Valve Replacement Market is also divided by end user into hospitals, ambulatory surgical centers, and others. Hospitals dominate the segment due to advanced infrastructure, availability of hybrid operating rooms, and trained specialists. It benefits from large procedural volumes and access to reimbursement support. Ambulatory surgical centers are emerging as viable treatment sites, driven by demand for faster recovery, lower costs, and convenience. The “others” category includes specialty cardiac clinics that provide localized services in select markets. Growing adoption across diverse care settings expands access to minimally invasive valve replacement globally. This end-user segmentation emphasizes the central role of healthcare infrastructure and patient preferences in shaping market expansion.

Segments:

Based on Type of Device:

- Self-Expanding Valves

- Balloon-Expandable Valves

Based on Material:

Based on End-User:

- Hospitals

- Ambulatory Surgical Centers

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America dominates the Transcatheter Heart Valve Replacement market with 48.3% share in 2024. The United States leads due to a high prevalence of aortic stenosis, well-developed healthcare infrastructure, and widespread acceptance of minimally invasive procedures. Favorable reimbursement policies and government-backed healthcare programs encourage hospitals to adopt advanced valve replacement therapies. Clinical trials such as EARLY TAVR expand patient eligibility to low-risk groups, further boosting adoption. Canada also contributes significantly, supported by public healthcare investments and growing awareness of structural heart disease treatment options. Key players prioritize product launches and partnerships in this region, making North America the most influential contributor to market revenues.

Europe

Europe held 30.2% share in 2024, positioning it as the second-largest regional market. Germany, France, and the United Kingdom represent the largest contributors, driven by rapidly aging populations and rising rates of cardiovascular disease. Public healthcare systems in these countries ensure patient access to TAVR procedures, supporting broad market penetration. Device approvals across the European Union further expand usage, while research studies strengthen physician confidence in outcomes. Companies continue introducing innovative products, such as next-generation self-expanding and balloon-expandable valves, which enhance treatment options. Countries in Eastern Europe are also witnessing growth as investments in hospital infrastructure improve access to advanced cardiovascular care. Overall, Europe remains a strong growth hub with consistent adoption of new technologies.

Asia-Pacific

Asia-Pacific accounted for 14.6% share in 2024, and it remains the fastest-growing region in this market. Japan and China lead adoption due to large elderly populations, increasing prevalence of heart valve disease, and improving healthcare capacity. Japan benefits from strong regulatory frameworks that speed up device approvals, while China witnesses growth through domestic manufacturing and expanding specialized cardiac centers. India also shows promising growth, with an estimated 300,000 patients eligible for TAVR procedures and rising hospital investments in urban centers. South Korea is witnessing momentum following regulatory approvals for new valves. Rapid urbanization, rising disposable income, and government focus on advanced healthcare technologies continue to position Asia-Pacific as the leading growth engine of the market.

Latin America

Latin America represented 4.1% share in 2024, with Brazil and Argentina driving demand. Growing cardiovascular disease incidence and increasing adoption of advanced surgical alternatives support regional market development. Brazil’s private healthcare sector is investing in advanced cardiac facilities, while Argentina is participating in international clinical trials, increasing exposure to TAVR technologies. Limited reimbursement structures and high costs remain obstacles in the public healthcare segment, slowing widespread adoption. However, medical tourism and specialized centers are helping expand access to advanced procedures in major cities. Multinational companies also target partnerships with local hospitals to build clinical capacity and strengthen awareness, ensuring future growth potential across Latin America.

Middle East & Africa

The Middle East & Africa held 2.8% share in 2024, marking it as a smaller but steadily growing market. Countries such as Saudi Arabia and the UAE continue investing heavily in modern cardiovascular facilities and advanced surgical capabilities. South Africa contributes to regional demand through specialized cardiac hospitals and adoption of minimally invasive therapies. Despite these developments, high costs and limited healthcare access across rural areas restrict large-scale expansion. However, ongoing regulatory approvals for devices, coupled with government-led healthcare initiatives, are expected to increase procedure volumes. Expanding medical tourism in Gulf countries and strategic collaborations between multinational manufacturers and local healthcare providers are also driving gradual but sustainable adoption of transcatheter heart valve replacement technologies in this region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Meril Life Sciences

- MicroPort Scientific Corporation

- Boston Scientific Corporation

- Suzhou Jiecheng Medical Technology Co. Ltd.

- Medtronic plc

- Venus Medtech (Hangzhou) Inc.

- JenaValve Technology, Inc.

- Abbott

- Sahajanand Medical Technologies Limited

- Edwards Lifesciences Corporation

Competitive Analysis

The Transcatheter Heart Valve Replacement Market include Meril Life Sciences, MicroPort Scientific Corporation, Boston Scientific Corporation, Suzhou Jiecheng Medical Technology Co. Ltd., Medtronic plc, Venus Medtech (Hangzhou) Inc., JenaValve Technology, Inc., Abbott, Sahajanand Medical Technologies Limited, and Edwards Lifesciences Corporation. The market demonstrates consistent expansion across industrial, commercial, and consumer segments worldwide. Growing demand for sustainable solutions drives companies to develop advanced technologies with higher efficiency. Regulatory frameworks encourage adoption by setting strict performance, safety, and environmental standards. Industries such as healthcare, energy, construction, and automotive remain primary adopters due to wide application benefits. Rising urbanization fuels infrastructure development, which strengthens the demand for durable and innovative solutions. Digital transformation supports integration of smart systems, creating opportunities for next-generation products. Consumer awareness regarding eco-friendly materials further boosts adoption across packaging, mobility, and household applications. Global supply chain improvements enable faster scaling of production capacities to meet rising needs. Emerging economies contribute significantly to growth due to industrialization, population expansion, and increasing investments in sustainable infrastructure. The sector reflects a balance between technological innovation, policy support, and evolving customer preferences.

Recent Developments

- In November 2024, Abbott introduced its experimental balloon-expandable transcatheter aortic valve implantation (TAVI) system for patients with severe aortic stenosis. This new system seeks to enable AI-assisted procedures and offers a less invasive treatment option for those at high risk for open-heart surgery.

- In March 2024, Medtronic revealed that the FDA has approved its Evolut FX+ transcatheter aortic valve replacement (TAVR) system for patients with symptomatic severe aortic stenosis. This updated system features a diamond-shaped frame that offers enhanced coronary access while maintaining the high valve performance the Evolut platform is known for.

- In January 2024, Eisenhower Health became the first hospital in the U.S. to be designated as an Edwards Benchmark Program Case Observation Site for treating aortic stenosis in patients undergoing transcatheter aortic valve replacement.

- In June 2023, JenaValve Technology, Inc., a leading innovator in transcatheter aortic valve replacement (TAVR) systems, has entered into a strategic partnership with egnite, Inc., a digital health company focused on cardiovascular care. This collaboration is designed to deepen insights into the care models and outcomes for patients suffering from aortic regurgitation (AR), aiming to drive improvements in treatment strategies and patient management.

Report Coverage

The research report offers an in-depth analysis based on Type of Device, Material, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Rising demand for minimally invasive procedures will drive steady adoption.

- Aging global population will increase the pool of patients eligible for procedures.

- Continuous improvements in valve materials will enhance device durability and outcomes.

- Growing acceptance of TAVR among younger patients will expand treatment scope.

- Hybrid surgical and catheter-based approaches will gain wider clinical relevance.

- Expanding reimbursement coverage will strengthen patient access across regions.

- Increasing clinical trials will support approval of new devices and indications.

- Regional healthcare investments will accelerate adoption in emerging economies.

- Digital tools and imaging advances will improve procedure accuracy and planning.

- Strategic collaborations between device makers and hospitals will shape market expansion.