Market Overview

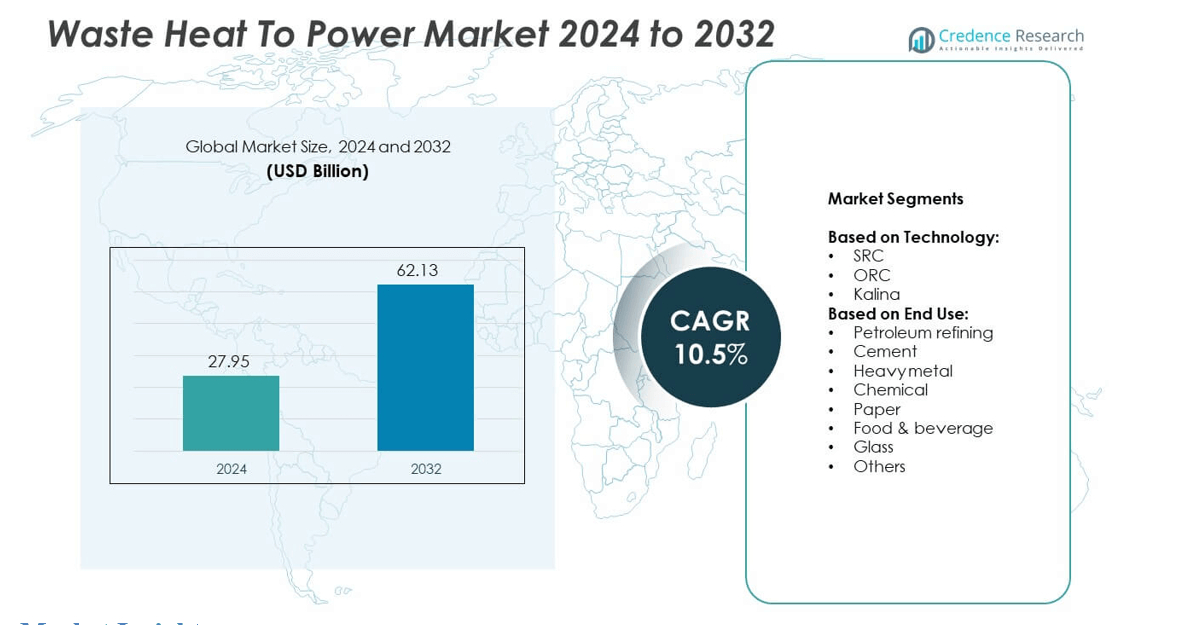

Waste Heat to Power Market size was valued at USD 27.95 billion in 2024 and is anticipated to reach USD 62.13 billion by 2032, at a CAGR of 10.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Waste Heat to Power Market Size 2024 |

USD 27.95 billion |

| Waste Heat to Power Market, CAGR |

10.5% |

| Waste Heat to Power Market Size 2032 |

USD 62.13 billion |

The Waste Heat to Power market grows through rising industrial demand for energy efficiency and cost control. Governments enforce strict emission regulations, pushing adoption of recovery systems across sectors like cement, steel, and chemicals. Companies invest in SRC and ORC technologies to reduce fossil fuel use and operational expenses. Trends show increasing integration with renewable sources and digital monitoring systems. The market also benefits from modular product development, enabling flexible deployment across mid-sized facilities and emerging industrial regions.

North America leads the Waste Heat to Power market, driven by strong industrial adoption and regulatory frameworks. Europe follows with advanced infrastructure and strict emission targets, while Asia Pacific records rapid growth due to expanding manufacturing and energy demand. Latin America and the Middle East & Africa witness steady uptake supported by modernization projects. Key players shaping the market include Thermax Ltd, Siemens Energy, Ormat Technologies, and Mitsubishi Heavy Industries, Ltd., each contributing through technology innovation and global project execution.

Market Insights

- The Waste Heat to Power market was valued at USD 27.95 billion in 2024 and is projected to reach USD 62.13 billion by 2032, growing at a CAGR of 10.5%.

- Rising industrial focus on energy efficiency and emission reduction fuels the demand for heat recovery systems across cement, chemical, and refining sectors.

- Adoption of Organic Rankine Cycle and Kalina cycle technologies is rising, driven by demand for compact and low-temperature systems in diverse applications.

- Key players such as Thermax Ltd, Siemens Energy, Ormat Technologies, and Mitsubishi Heavy Industries, Ltd. compete through modular designs, digital integration, and sector-specific solutions.

- High upfront capital costs and complex system customization limit adoption among small and medium industries, especially in cost-sensitive regions.

- North America leads in adoption due to advanced industries and strong policy support, while Asia Pacific grows rapidly with rising industrialization and infrastructure expansion.

- Europe remains a key contributor due to strict decarbonization mandates, and Latin America and the Middle East & Africa show steady gains through energy diversification initiatives

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Industrial Energy Demand Supports Market Expansion

The Waste Heat to Power market benefits from the rising need for energy efficiency in industrial sectors. Heavy industries such as cement, steel, glass, and chemicals generate significant waste heat during core operations. Companies seek ways to reduce operational costs and carbon emissions using energy recovery systems. Waste heat recovery allows industries to convert lost energy into usable electricity. This directly contributes to reduced fossil fuel usage and supports energy cost optimization. It also aligns with growing industrial sustainability goals. The Waste Heat to Power market gains traction from these industrial priorities.

- For instance, Climeon commissioned four HeatPower 150 units at the UK’s Rhodesia genset plant in February 2025, using low-temperature waste heat from reciprocating engines to increase overall energy efficiency

Strict Regulatory Pressure Drives Technology Adoption

Government regulations aimed at reducing greenhouse gas emissions encourage the deployment of energy recovery technologies. Regulatory bodies implement carbon pricing, energy efficiency mandates, and pollution control laws across developed and emerging economies. These measures push industries to adopt systems that meet efficiency norms. Waste Heat To Power solutions help meet compliance while generating economic value. Companies view this dual benefit as a key driver for investment. It also supports national energy security goals in power-deficit regions. The Waste Heat to Power market expands through this regulatory support.

- For instance, Combined Heat and Power (CHP) systems are significantly more efficient than conventional separate heat and power generation and can achieve efficiencies of over 80%, compared to 50% for typical technologies.

Growing Focus on Decarbonization in Power Generation

Global decarbonization goals influence the adoption of sustainable energy solutions. Utilities and independent power producers integrate Waste Heat to Power systems into renewable energy portfolios. It offers low-emission electricity without requiring fresh fuel input. The technology complements solar and wind sources by enhancing energy mix diversity. It also helps reduce dependence on intermittent power sources. Countries investing in cleaner grids adopt this technology to balance supply and emissions targets. The Waste Heat to Power market gains momentum from this transition.

Advancements in Heat Recovery Technology Encourage Growth

Technological progress improves efficiency, scalability, and affordability of heat recovery systems. Developments in organic Rankine cycle, supercritical CO₂ systems, and compact heat exchangers boost energy conversion rates. Equipment manufacturers offer modular systems tailored to specific industrial environments. It allows retrofitting in existing plants without major redesign. Improved maintenance diagnostics and remote monitoring further increase operational efficiency. The Waste Heat to Power market grows as technology becomes more adaptable and accessible.

Market Trends

Integration with Renewable Energy Systems Gains Traction

The Waste Heat to Power market sees a growing trend of integration with renewable energy infrastructure. Hybrid plants now combine waste heat recovery with solar thermal or biomass sources. This synergy improves overall energy efficiency and ensures stable power generation. Renewable energy developers explore waste heat recovery to enhance capacity utilization and lower emissions. Policymakers encourage hybrid setups through targeted incentives and regulatory frameworks. This trend supports decarbonization while boosting system reliability. The Waste Heat to Power market benefits from this multi-source optimization approach.

- For instance, Climeon completed deliveries of six HeatPower 300 waste heat recovery units, destined for integration aboard newly built A.P. Møller–Maersk container vessels to convert engine exhaust heat into electricity.

Deployment in Small and Medium Enterprises Increases

The adoption of compact and cost-effective recovery units rises among small and medium industrial players. Earlier limited to large facilities, waste heat systems now scale for mid-size operations. Manufacturers design plug-and-play units that require minimal installation time and floor space. SMEs seek solutions that reduce energy bills without high upfront costs. Governments offer grants and subsidies to drive adoption in this segment. This growing SME participation unlocks new revenue channels. The Waste Heat to Power market expands into previously underserved user groups.

- For instance, Alfa Laval’s E-PowerPack offers modular plug-and-play units with net electrical output options of 100 kW or 200 kW, fit for marine and smaller industrial setups, and promises up to 120,000 hours of service life before overhaul is needed

Digitalization and Predictive Maintenance Shape Operations

Smart technologies enter heat recovery system design and operation. Sensors, IoT platforms, and AI tools enable real-time data monitoring and fault detection. These features reduce downtime, improve energy yield, and extend equipment lifespan. Operators gain remote access to performance dashboards and predictive alerts. This transformation lowers maintenance costs and increases plant availability. The Waste Heat to Power market shifts toward data-driven efficiency as digitalization matures.

Focus on Modular and Mobile Systems Strengthens

Industries show rising interest in modular and transportable waste heat systems. These units support faster deployment across multiple facilities or temporary installations. Modular designs also reduce engineering complexity and lead times. Vendors offer scalable solutions that adapt to specific site requirements. Mobile waste heat units serve mining, oilfield, and construction sectors with high heat discharge. The Waste Heat to Power market sees increased demand for flexible and mobile deployment options.

Market Challenges Analysis

High Initial Capital Costs Limit Adoption Across Industries

The Waste Heat to Power market faces a key challenge in the form of high upfront costs. Installation involves expensive components such as turbines, heat exchangers, and control systems. Many small and mid-sized industries struggle to justify the investment without clear short-term returns. Even with long-term energy savings, budget constraints often delay deployment. Financing support from public or private institutions remains inconsistent across regions. This cost barrier reduces the speed of technology penetration in cost-sensitive markets. The Waste Heat to Power market must address pricing and financing models to scale further.

Technical Limitations and Design Complexity Hinder Efficiency

The efficiency of waste heat recovery depends heavily on temperature levels and process design. Low-temperature waste heat streams offer limited energy conversion potential, reducing economic viability. Matching system configuration to each facility’s unique heat profile increases engineering complexity. Space constraints, corrosive environments, and maintenance access further complicate system design. Operators also face integration issues with existing plant infrastructure. The Waste Heat to Power market encounters slow adoption where technical fit is poor or customization becomes costly.

Market Opportunities

Emerging Economies Offer Strong Industrial Expansion Potential

The Waste Heat to Power market holds strong growth prospects in emerging economies with expanding industrial bases. Countries in Asia, Latin America, and Africa invest in cement, steel, chemicals, and power sectors. These industries generate high volumes of waste heat suitable for energy recovery. Governments in these regions promote energy efficiency through incentives and policy reforms. Local manufacturers and EPC firms also begin offering tailored, low-cost recovery systems. Infrastructure upgrades and industrial modernization efforts create new deployment avenues. The Waste Heat to Power market can scale quickly by tapping into these industrializing regions.

Public-Private Partnerships Encourage Infrastructure Modernization

Collaborations between government agencies and private players present key growth avenues. Public-private partnerships (PPPs) accelerate the development of sustainable infrastructure in power and manufacturing sectors. Policymakers prioritize clean energy projects through tax benefits, funding support, and technology transfer agreements. Private firms bring advanced technologies and implementation expertise to large-scale deployments. These partnerships reduce investment risks and improve project bankability. The Waste Heat to Power market benefits from this coordinated approach to cleaner and cost-efficient energy generation.

Market Segmentation Analysis:

By Technology:

The Waste Heat to Power market segments into Steam Rankine Cycle (SRC), Organic Rankine Cycle (ORC), and Kalina cycle. SRC dominates due to its proven efficiency and wide use in high-temperature industrial applications. It suits large-scale operations where steam-based energy recovery aligns with existing systems. ORC follows as a fast-growing segment, favored in low to medium temperature settings and sectors with spatial limitations. It provides greater flexibility and simpler integration, especially for food and chemical industries. Kalina cycle, though still in niche use, attracts interest for its higher efficiency in recovering energy from variable heat sources. The Waste Heat to Power market continues to see innovation across all three cycles.

- For instance, Turboden offers ORC units delivering up to 40 MW per single shaft, suited for distributed power generation across diverse temperatures

By End-Use:

The Waste Heat to Power market serves multiple energy-intensive industries, with petroleum refining holding a major share. Refineries operate continuously and emit large volumes of waste heat, making energy recovery highly viable. Cement production also contributes significantly due to its high thermal input and emission levels. The heavy metal and chemical industries follow, both generating consistent high-grade waste heat suited for SRC and ORC systems. Paper and food & beverage industries adopt low-to-medium temperature recovery systems to cut costs and improve sustainability. The glass industry presents strong growth potential with rising investments in furnace efficiency. Other sectors include textiles, bricks, and industrial gases, where waste heat recovery gains momentum through tailored system designs. The Waste Heat to Power market diversifies across end-use segments by offering scalable, application-specific solutions.

- For instance, Augury released its Halo™ R4000 series edge-AI sensors in November 2024—the smallest and lightest industrial-grade sensors in the company’s lineup, measuring approximately 56 mm x 52 mm. The sensors are designed to operate in extreme environments and support up to 40 sensors per gateway when integrated with the Cassia X-2000 gateway

Segments:

Based on Technology:

Based on End Use:

- Petroleum refining

- Cement

- Heavy metal

- Chemical

- Paper

- Food & beverage

- Glass

- Others

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounted for 31.2% of the global Waste Heat To Power market in 2024, holding the largest share due to strong industrial infrastructure and early adoption of energy recovery systems. The United States leads with widespread deployment in petroleum refining, cement, and chemical manufacturing facilities. Federal and state-level programs incentivize energy efficiency projects, including tax credits and low-interest financing. Companies adopt advanced SRC and ORC systems to improve margins and comply with emission reduction mandates. The presence of key manufacturers and engineering firms accelerates technology innovation and market penetration. Canada supports the market with initiatives targeting carbon neutrality in industrial operations. Strong regulatory enforcement and consistent energy pricing make North America a stable contributor to long-term market growth.

Europe

Europe represented 26.4% of the Waste Heat To Power market in 2024, backed by strict climate policies and large-scale industrial modernization. Countries such as Germany, France, and Italy prioritize waste heat recovery to meet emissions targets under the EU Green Deal. Cement and glass sectors actively implement SRC and Kalina systems to lower energy costs and carbon output. Government subsidies, carbon credits, and research programs encourage continuous investment in heat recovery infrastructure. Eastern European nations also enter the market with support from EU development funds. Companies across the region integrate smart monitoring tools to maximize recovery performance. Europe remains a leader in efficiency standards and cross-border collaborations in clean energy deployment.

Asia Pacific

Asia Pacific held 23.7% of the global share in 2024 and is projected to record the fastest growth during the forecast period. Rapid industrialization in China, India, Japan, and Southeast Asia drives demand for energy-saving technologies. Governments offer policy support through energy efficiency targets, industrial upgrade programs, and emissions controls. China leads regional adoption, especially in cement, metallurgy, and chemicals. Japan focuses on compact ORC systems and mobile units suited for diverse industrial environments. India ramps up infrastructure for cleaner energy and resource optimization. Asia Pacific offers long-term opportunity due to its expanding industrial footprint, favorable policies, and rising electricity demand.

Latin America

Latin America contributed 10.1% of the Waste Heat To Power market in 2024, with growing adoption in cement and mining sectors. Brazil and Mexico are the leading countries due to their large industrial bases and focus on energy cost reduction. Local manufacturers begin offering modular and low-maintenance recovery systems tailored for mid-sized industries. Government-led energy efficiency programs support initial investments, though wider adoption still faces financing challenges. Regional growth remains steady, driven by infrastructure modernization and environmental awareness. The presence of global EPC players also supports knowledge transfer and project execution across Latin American markets.

Middle East & Africa

The Middle East & Africa accounted for 8.6% of the global market in 2024, supported by rising industrial energy needs and regional diversification strategies. Countries like Saudi Arabia, UAE, and South Africa invest in clean energy projects to reduce reliance on fossil fuels. Petroleum refining, glass, and chemical sectors offer favorable conditions for heat recovery deployment. Regional governments encourage investment through incentives and partnerships with international technology providers. Infrastructure limitations and policy delays still hinder faster adoption. However, rising demand for cost-efficient energy drives gradual growth. The Waste Heat To Power market in this region continues to develop with improving regulatory support and industrial investment.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Thermax Ltd

- Dürr Group

- Ormat Technologies

- General Electric

- Walchandnagar Industries Limited (WIL)

- Climeon

- IHI Corporation

- Aura GmbH & CO. KG

- Rentech Boiler System

- Forbes Marshall

- AC Boiler SpA

- Siemens Energy

- Exergy International Srl

- Mitsubishi Heavy Industries, Ltd.

- Cochran Ltd.

Competitive Analysis

The leading players in the Waste Heat To Power market include Thermax Ltd, Dürr Group, Ormat Technologies, General Electric, Walchandnagar Industries Limited (WIL), Climeon, IHI Corporation, Aura GmbH & CO. KG, Rentech Boiler System, Forbes Marshall, AC Boiler SpA, Siemens Energy, Exergy International Srl, Mitsubishi Heavy Industries, Ltd., and Cochran Ltd. These companies compete on technology innovation, application-specific customization, and global project execution capabilities. Many focus on advancing Organic Rankine Cycle and Kalina cycle technologies to improve efficiency in low-temperature waste heat recovery. Key players continue to invest in modular system design and scalable product lines to meet rising demand from mid-size industrial users. Companies strengthen their global footprint through partnerships, local manufacturing, and EPC services. Regional adaptation remains critical, with players tailoring solutions to varying industrial regulations, energy costs, and infrastructure conditions. Competitive strategies also include digital integration for performance monitoring and predictive maintenance. The market shows a balanced mix of large multinational corporations and regionally strong technology providers. This competitive landscape drives continuous innovation, cost optimization, and faster deployment cycles. Players that offer flexible systems, proven reliability, and localized support will sustain long-term success across diverse end-use industries.

Recent Developments

- In 2024, Climeon completed deliveries of six HeatPower 300 waste heat recovery units, destined for integration aboard newly built A.P. Møller–Maersk container vessels to convert engine exhaust heat into electricity.

- In 2024, Exergy did announce and progress with projects in Turkey. Notably, a new 8 MW geothermal binary plant for Emirler Enerji was contracted in January 2024, building on previous work in the country.

- In August 2023, Siemens’s new line monitoring relay generation was introduced. The SIRIUS 3UG5 line of monitoring relays incorporates well-established technology and modern innovations in features and applications.

- In July 2023, Yokohama City Government, Tokyo Gas Co., Ltd. (Tokyo Gas), Mitsubishi Heavy Industries, Ltd. (MHI), and group company MHI Environmental and Chemical Engineering Co., Ltd. (MHIEC) are scheduled to commence running a demonstration experiment of the process of capturing and using CO2 (note 1) in which CO2 contained in flue gas from a municipal waste-to-energy plant is captured and sent to the of Tokyo Gas in a demo location for methanation (note 2).

Report Coverage

The research report offers an in-depth analysis based on Technology, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will grow steadily due to rising focus on industrial energy efficiency.

- Adoption of ORC systems will increase across low-to-medium temperature industries.

- Hybrid projects combining waste heat recovery with renewables will gain traction.

- Small and medium industries will drive demand for modular and cost-effective systems.

- Governments will expand support through stricter energy efficiency mandates.

- Advancements in Kalina cycle technology will improve low-grade heat conversion.

- Digital monitoring and predictive maintenance will boost operational reliability.

- Emerging markets in Asia and Latin America will open new revenue opportunities.

- Collaborations between public and private sectors will support infrastructure upgrades.

- Equipment manufacturers will focus on compact, mobile systems for remote sites.