Market Overview

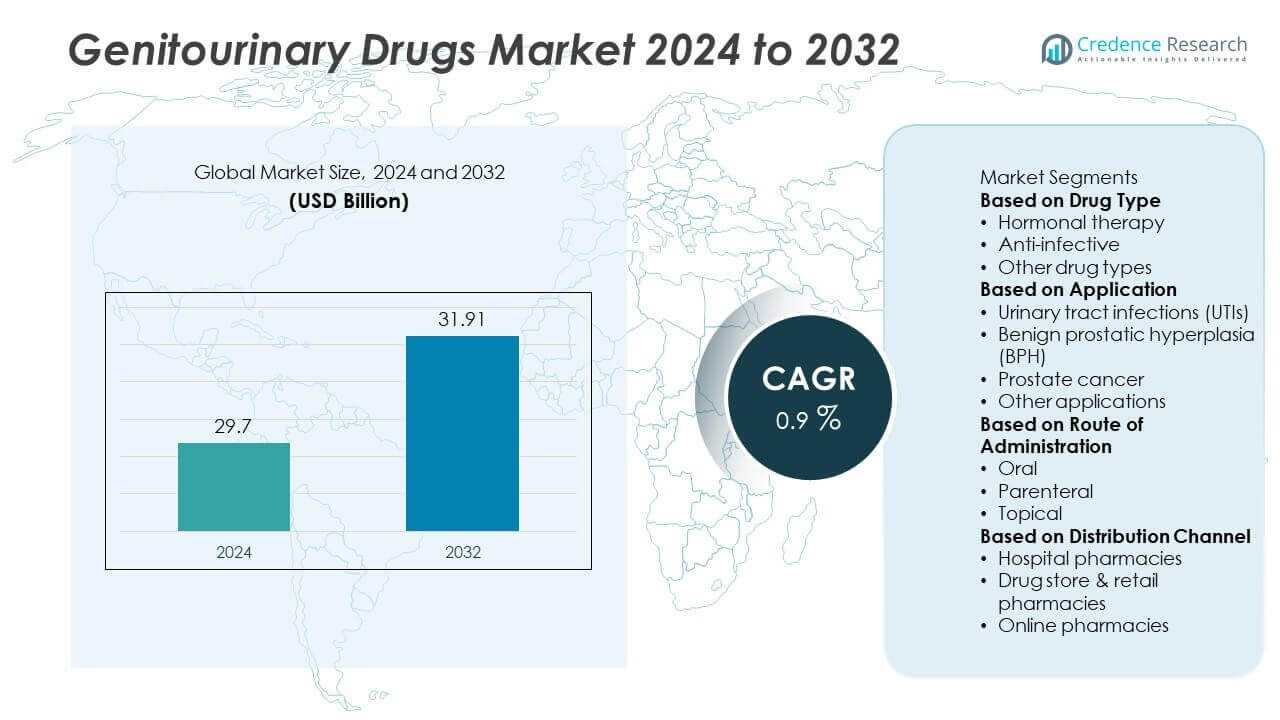

The Genitourinary Drugs Market was valued at USD 29.7 billion in 2024 and is projected to reach USD 31.91 billion by 2032, growing at a CAGR of 0.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Genitourinary Drugs Market Size 2024 |

USD 29.7 Billion |

| Genitourinary Drugs Market, CAGR |

0.9% |

| Genitourinary Drugs Market Size 2032 |

USD 31.91 Billion |

The Genitourinary Drugs Market is driven by the rising prevalence of urinary tract infections, prostate disorders, kidney diseases, and bladder conditions, particularly in aging populations. It benefits from strong demand for antibiotics, hormonal therapies, and biologics that improve patient outcomes.

The Genitourinary Drugs Market demonstrates strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, each with unique growth drivers. North America leads with advanced healthcare infrastructure, high prevalence of prostate and kidney disorders, and strong research activity. Europe emphasizes regulatory-driven adoption of innovative therapies, particularly for prostate cancer and urinary tract infections, while Asia-Pacific shows the fastest expansion due to rising healthcare spending, large patient pools, and strong penetration of generics in China and India. Latin America and the Middle East & Africa are experiencing steady growth supported by improving access to essential medicines and government-backed health initiatives. Key players driving this market include Abbott Laboratories, Bayer AG, AstraZeneca Plc, and GlaxoSmithKline Plc, who focus on expanding therapeutic portfolios, strengthening R&D pipelines, and entering partnerships to extend reach. Their strategies ensure availability of both innovative and affordable drugs across diverse healthcare systems.

Market Insights

- The Genitourinary Drugs Market was valued at USD 29.7 billion in 2024 and is projected to reach USD 31.91 billion by 2032, at a CAGR of 0.9%.

- Key drivers include the rising prevalence of urinary tract infections, prostate disorders, kidney diseases, and bladder conditions, especially in aging populations worldwide.

- Market trends highlight the growing role of biologics, targeted therapies, and immunotherapies, alongside increased use of digital health tools and telemedicine for patient management.

- Competitive analysis shows leading companies such as Abbott Laboratories, Bayer AG, AstraZeneca Plc, GlaxoSmithKline Plc, and Eli Lilly and Company focusing on innovation, R&D, and global partnerships to strengthen portfolios.

- Market restraints include high treatment costs, limited access in emerging economies, regulatory hurdles, and rising concerns over antibiotic resistance affecting long-term drug effectiveness.

- Regional analysis shows North America driving adoption with advanced healthcare systems and innovation, Europe emphasizing regulatory compliance and cancer treatment, while Asia-Pacific grows rapidly with large patient pools, healthcare reforms, and cost-effective generics. Latin America and the Middle East & Africa continue to expand steadily with improving infrastructure and health initiatives.

- The long-term outlook remains stable, with opportunities created by increasing healthcare investment, stronger insurance coverage, and development of novel therapies that improve access and address unmet needs across urological disorders globally.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Prevalence of Genitourinary Disorders Across the Globe

The Genitourinary Drugs Market is driven by the growing incidence of urinary tract infections, kidney diseases, prostate disorders, and overactive bladder conditions. It addresses the increasing burden of age-related urological conditions in both men and women. Lifestyle changes, poor dietary habits, and higher exposure to risk factors elevate the number of cases. Chronic conditions such as diabetes and hypertension further increase susceptibility to genitourinary complications. The rising patient pool ensures consistent demand for effective therapies. Pharmaceutical companies expand their drug portfolios to meet these rising treatment needs.

- For instance, GSK received FDA approval for gepotidacin (Blujepa) as the first oral antibiotic in a new class in nearly 30 years for uncomplicated urinary tract infections, making it available for female adults and adolescents aged 12 years and above.

Expanding Geriatric Population and Associated Health Complications

The rapid growth of the elderly population worldwide directly fuels demand for urological medications. The Genitourinary Drugs Market supports treatments for age-related problems like benign prostatic hyperplasia, urinary incontinence, and chronic kidney disorders. It benefits from growing awareness and diagnosis of these conditions among older adults. Healthcare systems across developed and emerging economies allocate more resources to elderly care. Longer life expectancy increases the need for prolonged treatment cycles. This demographic trend secures a stable patient base for long-term growth in the market.

- For instance, Ionis Pharmaceuticals gained FDA approval for donidalorsen (Dawnzera), a subcutaneous therapy administered once every four weeks, which reduced hereditary angioedema attacks by 81% over 24 weeks in patients including older adults with chronic comorbidities.

Strong Research Pipeline and Focus on Novel Drug Development

Innovation remains a central driver as companies invest in research and development of advanced therapeutics. The Genitourinary Drugs Market evolves through biologics, targeted therapies, and extended-release formulations that improve patient compliance. It benefits from clinical trials focusing on new mechanisms of action for resistant infections and chronic conditions. Collaboration between academic institutions and pharmaceutical companies accelerates development of next-generation drugs. Patent expiries also create opportunities for generic drugs to expand access. This continuous cycle of innovation and competition enhances treatment outcomes.

Government Support and Expanding Healthcare Infrastructure

Supportive healthcare policies and infrastructure development stimulate growth in emerging and developed regions alike. The Genitourinary Drugs Market benefits from government programs that improve access to essential medicines. It is strengthened by rising health expenditure, better diagnostic facilities, and awareness campaigns targeting urological health. Expanding insurance coverage across many countries increases affordability of long-term therapies. Multinational pharmaceutical companies partner with local players to extend distribution networks. These initiatives expand the reach of genitourinary drugs, ensuring availability to larger patient populations.

Market Trends

Shift Toward Targeted Therapies and Precision Medicine

The Genitourinary Drugs Market is witnessing a move toward targeted therapies designed to address specific disease mechanisms. It supports precision medicine approaches that improve treatment efficacy and reduce adverse effects. Pharmaceutical companies develop drugs tailored for patient subgroups based on genetic and molecular profiling. This trend is especially relevant for prostate cancer and chronic kidney conditions. Personalized approaches enhance patient outcomes and open pathways for new product approvals. Growing adoption of biomarker-driven treatments strengthens this market direction.

- For instance, AstraZeneca’s Phase III PROfound trial showed that in a subset of 245 patients with BRCA1, BRCA2, or ATM gene mutations, olaparib achieved a median radiographic progression-free survival of 7.4 months compared to 3.6 months in the control group. For the overall trial population of 387 patients, the median radiographic progression-free survival was 5.8 months with olaparib versus 3.5 months in the control arm.

Increasing Role of Biologics and Immunotherapies

Biologics and immunotherapies are gaining traction for the treatment of genitourinary cancers and inflammatory disorders. The Genitourinary Drugs Market benefits from monoclonal antibodies and immune checkpoint inhibitors that provide improved survival outcomes. It supports innovative approaches that complement traditional chemotherapy and hormone-based treatments. Patients benefit from longer progression-free survival rates and fewer side effects compared to older drugs. The trend highlights the integration of advanced science into mainstream urology and oncology care. Expanding regulatory approvals accelerate their entry into global markets.

- For instance, Bristol-Myers Squibb announced updated data from the CheckMate -9ER trial for nivolumab (Opdivo) combined with cabozantinib in previously untreated advanced renal cell carcinoma. At a median follow-up of 44.0 months, the trial demonstrated a 3-year overall survival probability of 58.7% for patients treated with the combination, compared to 49.5% for those treated with sunitinib, reinforcing immunotherapy’s role in long-term disease control. The trial included 651 patients in total, with 323 receiving the nivolumab-plus-cabozantinib combination.

Rising Demand for Combination Therapies

Combination therapies are becoming more prominent as they deliver improved outcomes in complex conditions. The Genitourinary Drugs Market integrates multi-drug regimens to address resistance and enhance effectiveness. It applies widely in prostate cancer, urinary tract infections, and chronic kidney disorders. Healthcare providers prefer this approach to optimize results while reducing risks of recurrence. Pharmaceutical firms increasingly launch fixed-dose combinations that simplify dosing for patients. The adoption of these therapies reflects the demand for comprehensive treatment strategies.

Expansion of Digital Health and Telemedicine Support

Digital platforms and telemedicine tools are reshaping access to care in urology. The Genitourinary Drugs Market benefits from digital prescriptions, virtual consultations, and patient monitoring solutions. It ensures continuous management of chronic conditions like overactive bladder and benign prostatic hyperplasia. Patients gain easier access to physicians, especially in remote or underserved areas. Integration of mobile apps improves adherence to prescribed therapies. This digital shift enhances the patient experience and strengthens the long-term adoption of genitourinary drugs.

Market Challenges Analysis

High Treatment Costs and Limited Access in Emerging Economies

The Genitourinary Drugs Market faces challenges due to high treatment costs and unequal access across regions. It requires significant financial resources for biologics, targeted therapies, and long-term medication regimens. Many patients in emerging economies lack insurance coverage or face limited reimbursement policies. This restricts adoption of advanced drugs and encourages reliance on generics. Infrastructure gaps, including diagnostic delays and inadequate specialist availability, further limit timely treatment. These barriers slow the market’s potential expansion, especially in low- and middle-income regions.

Regulatory Hurdles and Safety Concerns in Drug Development

Complex regulatory frameworks and safety concerns create obstacles for new product approvals. The Genitourinary Drugs Market must address stringent requirements for clinical trials and post-marketing surveillance. It faces delays when adverse effects, resistance issues, or insufficient efficacy are identified during testing. Pharmaceutical companies invest heavily in trials, yet many products fail to achieve approval or face recalls. Rising scrutiny of antibiotic resistance and long-term side effects adds pressure on manufacturers. These challenges increase costs and reduce the speed of bringing innovative therapies to patients.

Market Opportunities

Rising Demand for Novel Therapies in Oncology and Chronic Conditions

The Genitourinary Drugs Market offers opportunities through the growing demand for innovative therapies targeting cancers and chronic kidney diseases. It supports advancements in precision medicine, immunotherapy, and biologics that address unmet clinical needs. Prostate and bladder cancers remain areas of strong research focus with multiple late-stage pipelines. Companies investing in breakthrough treatments gain competitive advantage in these high-burden conditions. Expansion of generic and biosimilar drugs also improves accessibility for wider patient populations. This balance between innovation and affordability creates a resilient growth path for the market.

Expanding Role of Emerging Economies and Healthcare Infrastructure

Healthcare modernization in Asia-Pacific, Latin America, and the Middle East creates significant opportunities for growth. The Genitourinary Drugs Market benefits from rising healthcare expenditure, stronger insurance frameworks, and government support for essential medicines. It aligns with increasing awareness campaigns that encourage early diagnosis and treatment of urological conditions. Pharmaceutical companies are expanding regional partnerships to strengthen distribution and improve access. Growing investments in hospital networks and diagnostic centers further enhance treatment adoption. This regional expansion strategy ensures long-term opportunities for global players across developing markets.

Market Segmentation Analysis:

By Drug Type

The Genitourinary Drugs Market is segmented into antibiotics, hormones, anti-inflammatory agents, and others including antineoplastics and biologics. Antibiotics remain a vital category due to their role in treating urinary tract infections, which are among the most common conditions worldwide. It continues to generate stable demand, though rising resistance issues push development of new formulations. Hormones play a central role in managing prostate disorders and fertility-related conditions, making them an essential therapeutic class. Anti-inflammatory agents are widely used in cases of bladder pain syndrome and interstitial cystitis. The growing presence of biologics and targeted therapies strengthens the market’s capacity to address complex urological diseases.

- For instance, GSK & Spero Therapeutics Stopped the late-stage Phase III trial of tebipenem HBr for complicated urinary tract infections (cUTIs) early after an interim analysis of 1,690 patients showed the drug met its primary efficacy endpoint versus IV imipenem-cilastatin.

By Application

Segmentation by application includes urinary tract infections, kidney diseases, prostate disorders, bladder disorders, and cancers affecting the urinary system. The Genitourinary Drugs Market is largely driven by the high prevalence of urinary tract infections across all age groups. It also benefits from strong demand in prostate health management, especially in aging populations. Kidney diseases, often linked to diabetes and hypertension, create sustained demand for effective drugs. Bladder disorders including overactive bladder and incontinence drive adoption of long-term therapies. Oncology-focused drugs targeting prostate and bladder cancers represent a growing segment with significant research activity. This broad application base reinforces the strategic importance of drug development in multiple therapeutic areas.

- For instance, KEYNOTE-564 Study Treatment with pembrolizumab after surgery in patients with clear cell renal cell carcinoma at high risk for recurrence showed improved overall survival compared with placebo.

By Route of Administration

The Genitourinary Drugs Market is divided by route of administration into oral, injectable, and topical formulations. Oral drugs dominate due to their convenience, widespread availability, and suitability for chronic conditions requiring long-term treatment. It offers higher patient compliance and supports mass prescription in both developed and emerging healthcare systems. Injectable drugs hold a strong share in oncology and advanced prostate treatments where targeted delivery is critical. Topical therapies are used for localized conditions such as bladder pain or external genitourinary disorders. The variety of delivery options allows healthcare providers to tailor treatments according to disease severity and patient needs. This diversity in administration methods expands the overall accessibility of genitourinary therapies.

Segments:

Based on Drug Type

- Hormonal therapy

- Anti-infective

- Other drug types

Based on Application

- Urinary tract infections (UTIs)

- Benign prostatic hyperplasia (BPH)

- Prostate cancer

- Other applications

Based on Route of Administration

Based on Distribution Channel

- Hospital pharmacies

- Drug store & retail pharmacies

- Online pharmacies

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Genitourinary Drugs Market with nearly 36% in 2024. The region benefits from advanced healthcare infrastructure, widespread insurance coverage, and strong awareness of urological health. The United States dominates due to a high prevalence of urinary tract infections, prostate cancer, and chronic kidney disorders. It also benefits from extensive research and development efforts by leading pharmaceutical companies based in the country. Canada contributes with significant demand for bladder and kidney disorder treatments, supported by government health programs. Mexico shows growth potential with rising investments in healthcare and expanding access to essential drugs. The strong presence of key market players and high adoption of biologics further strengthen the region’s leadership.

Europe

Europe accounts for around 28% of the Genitourinary Drugs Market share in 2024. The region’s growth is shaped by strict regulatory frameworks, high healthcare spending, and a well-developed pharmaceutical industry. Countries like Germany, France, and the United Kingdom dominate regional demand with advanced treatments for prostate disorders and urinary tract infections. It benefits from increasing focus on aging populations, where urological conditions are more prevalent. Government initiatives supporting cancer research, coupled with early diagnostic programs, improve access to therapies. Southern and Eastern European countries also show rising demand as healthcare systems expand and adopt innovative medicines. The growing presence of generics and biosimilars strengthens affordability and accessibility across the region.

Asia-Pacific

Asia-Pacific represents close to 24% of the Genitourinary Drugs Market share in 2024, with the fastest projected growth rate during the forecast period. China leads with high patient volumes for urinary tract infections and kidney diseases, supported by government-backed healthcare reforms. Japan and South Korea contribute through strong adoption of advanced therapies and significant pharmaceutical innovation. India emerges as a key growth market with rising awareness, expanding hospital infrastructure, and increasing insurance penetration. It also benefits from the presence of cost-effective generics, which improve access to essential treatments. Growing investments in oncology and biologics for urological cancers enhance long-term opportunities in the region. The rapid pace of urbanization and lifestyle changes further increase demand for urological medications.

Latin America

Latin America holds about 7% of the Genitourinary Drugs Market share in 2024. The region shows steady progress as healthcare access improves and awareness of genitourinary disorders increases. Brazil dominates demand with its large population and significant burden of prostate and kidney diseases. Mexico and Argentina follow with rising adoption of generic drugs and government programs promoting access to essential medicines. It faces challenges related to limited healthcare infrastructure and high treatment costs, but expanding private healthcare systems drive market growth. Increasing pharmaceutical investment and partnerships with global players support future expansion in the region.

Middle East and Africa

The Middle East and Africa together account for nearly 5% of the Genitourinary Drugs Market share in 2024. The region demonstrates rising demand due to growing prevalence of kidney disorders and urinary tract infections. The United Arab Emirates and Saudi Arabia lead adoption with investments in advanced healthcare facilities and access to branded therapies. South Africa and Egypt represent key African markets with increasing burden of prostate cancer and chronic kidney diseases. It faces barriers such as high drug costs and limited insurance coverage, but government-backed health initiatives improve access in urban centers. Ongoing development of healthcare infrastructure and greater international collaborations create growth opportunities for the market across the region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- GlaxoSmithKline Plc

- Bristol-Myers Squibb Co.

- Merck & Co., Inc.

- Abbott Laboratories

- Ionis Pharmaceuticals, Inc.

- Bayer AG

- Hoffmann-La Roche Ltd.

- Eli Lilly and Company

- AstraZeneca Plc

- Allergan, Inc.

Competitive Analysis

The competitive landscape of the Genitourinary Drugs Market is shaped by leading players such as Abbott Laboratories, Bayer AG, AstraZeneca Plc, GlaxoSmithKline Plc, Eli Lilly and Company, Bristol-Myers Squibb Co., Merck & Co., Inc., F. Hoffmann-La Roche Ltd., Ionis Pharmaceuticals, Inc., and Allergan, Inc. These companies compete by expanding their therapeutic portfolios across urinary tract infections, prostate disorders, kidney diseases, and bladder conditions. They invest heavily in research and development to advance biologics, targeted therapies, and immunotherapies while also focusing on cost-effective generics to improve accessibility. Strategic partnerships, licensing agreements, and acquisitions strengthen their presence across both developed and emerging markets. Many players emphasize late-stage clinical pipelines for prostate and bladder cancers, areas with significant unmet medical needs. Innovation in drug delivery methods, including extended-release formulations and combination therapies, further enhances competitiveness. By balancing innovation, affordability, and geographic reach, these companies maintain leadership in a market that demands both advanced and widely accessible treatments.

Recent Developments

- In August 2025, The FDA approved donidalorsen (brand name Dawnzera) for prophylaxis in hereditary angioedema (HAE) in patients 12 years and older. Treatment—administered via subcutaneous injection once every four weeks—reduced monthly attack frequency by 81% over a 24-week study period compared to placebo.

- In August 2025, The FDA accepted for priority review GSK’s supplemental New Drug Application for gepotidacin (Blujepa) in treating uncomplicated urogenital gonorrhea in patients aged 12 years and older (weighing ≥45 kg). FDA’s Prescription Drug User Fee Act (PDUFA) action date is set for December 11, 2025

- In May 2025, In the Phase 3 Pivot-PO study, oral tebipenem HBr met its primary non-inferiority endpoint for treating complicated UTIs (cUTIs). The independent data monitoring board recommended early trial termination. Trial enrolled 1,690 patients and showed comparable efficacy to IV imipenem-cilastatin, with no new safety issues.

- In March 2025, The FDA approved gepotidacin (brand name Blujepa) as an oral antibiotic for uncomplicated urinary tract infections (uUTIs) in female adults and pediatric patients aged 12 and older.

Report Coverage

The research report offers an in-depth analysis based on Drug Type, Application, Route of Administration, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will remain steady with consistent demand for treatments targeting urinary tract infections and kidney diseases.

- Growth will be supported by rising prevalence of prostate disorders in aging populations worldwide.

- Biologics and immunotherapies will gain traction in managing urological cancers and chronic conditions.

- Combination therapies will expand adoption as providers seek improved efficacy and reduced resistance.

- Digital health and telemedicine will enhance patient access and strengthen long-term treatment adherence.

- Emerging economies will drive growth through healthcare investments, insurance expansion, and generic drug availability.

- Regulatory focus on safety and resistance management will shape future drug development pipelines.

- Innovation in drug delivery, including extended-release formulations, will improve patient compliance.

- Partnerships between global and local pharmaceutical companies will strengthen market reach and access.

- Continued R&D in precision medicine and targeted approaches will open new opportunities for advanced genitourinary treatments.