Market Overview:

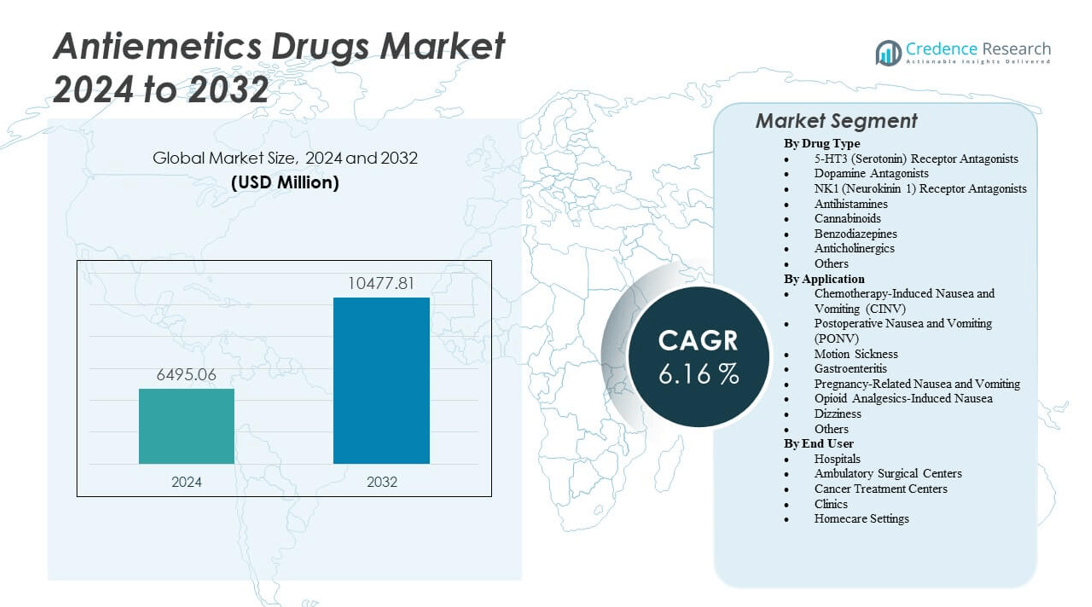

The Antiemetics Drugs Market is projected to grow from USD 6,495.06 million in 2024 to an estimated USD 10,477.81 million by 2032, with a compound annual growth rate (CAGR) of 6.16% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Antiemetics Drugs Market Size 2024 |

USD 6,495.06 million |

| Antiemetics Drugs Market, CAGR |

6.16% |

| Antiemetics Drugs Market Size 2032 |

USD 10,477.81 million |

Market growth is fueled by the rising prevalence of cancer, leading to higher chemotherapy usage and associated nausea cases. Increasing demand for postoperative and motion sickness treatments further drives product adoption. Pharmaceutical firms are investing in advanced 5-HT3 and NK1 receptor antagonists with improved efficacy and safety profiles. Expanding awareness of supportive care in oncology and growing access to healthcare services strengthen the market outlook.

North America dominates due to its advanced cancer treatment infrastructure and wide adoption of antiemetic therapy in hospitals. Europe follows, supported by regulatory standardization and well-structured healthcare systems. The Asia-Pacific region is rapidly expanding with improved healthcare spending and access to cost-effective generics in India, China, and Japan. Latin America and the Middle East show emerging growth with increasing investments in oncology care.

Market Insights:

- The Antiemetics Drugs Market is valued at USD 6,495.06 million in 2024 and is projected to reach USD 10,477.81 million by 2032, growing at a CAGR of 6.16%.

- Rising cancer prevalence and higher chemotherapy usage drive demand for antiemetic drugs across oncology settings.

- Advancements in 5-HT3 and NK1 receptor antagonists enhance treatment efficacy and reduce side effects.

- Increasing surgical procedures and postoperative care needs further boost product consumption.

- Limited access to advanced therapies in developing nations restrains market penetration.

- North America leads the market due to strong healthcare infrastructure and high prescription rates.

- Asia-Pacific emerges as a high-growth region supported by expanding healthcare access and generic availability.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Global Cancer Incidence Elevating Demand for Chemotherapy-Induced Nausea and Vomiting Control

The growing cancer population worldwide has intensified the demand for antiemetic therapies. Chemotherapy-induced nausea and vomiting (CINV) remains one of the most distressing side effects of cancer treatment. Hospitals and oncology centers focus on integrating multi-drug regimens to reduce these adverse effects. The rising use of combination antiemetic drugs helps patients complete their treatment cycles successfully. It drives pharmaceutical companies to develop highly selective receptor antagonists. The Antiemetics Drugs Market gains strong momentum from continuous clinical advancements. Patient-centric approaches, including early symptom management, strengthen therapy adherence. This shift improves patient outcomes and boosts healthcare provider satisfaction rates.

- For instance, Merck’s Emend (aprepitant) achieved a complete response (no emesis, no rescue medication) in the delayed phase for 51% of pediatric patients across days 2 through 5, compared to 26% with standard therapy, as shown in a phase 3 trial and confirmed in FDA regulatory reviews

Expanding Research and Development Efforts in Advanced Receptor Antagonists

Global pharmaceutical firms are investing heavily in new formulations targeting neurokinin-1 (NK1) and serotonin (5-HT3) receptors. These innovations aim to enhance drug efficacy and reduce side effects compared to traditional therapies. Clinical studies show improved outcomes with second-generation receptor antagonists. It supports regulatory approvals across multiple oncology indications. Biopharmaceutical collaborations between research institutions and companies accelerate molecule discovery. The Antiemetics Drugs Market benefits from partnerships driving precision formulations. Strong pipelines of novel compounds enable diversified product offerings. Continuous innovation ensures broader accessibility and long-term commercial sustainability.

- For instance, Helsinn Healthcare’s Aloxi (palonosetron) demonstrates an elimination half-life of approximately 40 hours, as specified in the official prescribing information and corroborated in peer-reviewed pharmacokinetic studies, enabling extended protection from CINV with a single dose.

Increased Surgical and Postoperative Procedures Requiring Nausea Management

The rising number of surgical procedures worldwide has elevated demand for post-operative nausea and vomiting (PONV) prevention drugs. Patients undergoing anesthesia or invasive surgeries experience nausea that disrupts recovery timelines. Hospitals now adopt preventive administration protocols to minimize post-surgical discomfort. It fuels consistent procurement of antiemetic medications in both developed and emerging economies. The Antiemetics Drugs Market benefits from rising healthcare awareness and improved perioperative care guidelines. Pharmaceutical firms align product portfolios with hospital-based treatment frameworks. Improved drug formulations ensure faster onset and longer symptom relief. Increasing outpatient surgeries also add to overall prescription frequency.

Growing Focus on Pediatric and Geriatric Patient Care in Nausea Management

Healthcare systems emphasize age-specific antiemetic solutions to manage nausea in vulnerable groups. Children undergoing chemotherapy or viral infections often require safe, dosage-adjusted antiemetics. Older adults need well-tolerated drugs due to polypharmacy risks. It pushes firms to invest in age-appropriate formulations and delivery mechanisms. The Antiemetics Drugs Market expands through tailored products for pediatric and geriatric use. Governments support research funding for non-invasive and oral formulations. Pharmaceutical advancements enhance patient compliance and recovery outcomes. Broader clinical adoption improves quality of care and boosts product credibility.

Market Trends

Shift Toward Combination Therapy and Multi-Targeted Drug Regimens

Combination antiemetic therapy has emerged as a standard for treating complex nausea conditions. Physicians prefer multi-receptor agents that target both central and peripheral pathways. It enhances treatment response and minimizes breakthrough nausea incidents. The Antiemetics Drugs Market sees expanding use of dual-acting formulations for better control. Clinical guidelines now recommend combined 5-HT3 and NK1 receptor antagonists for CINV management. Pharmaceutical research prioritizes optimizing dosage synergy and safety profiles. Adoption of fixed-dose combinations simplifies administration in hospital settings. The trend supports wider patient adherence and stronger therapeutic reliability.

- For instance, in a multicenter randomized phase III trial supported by Merck & Co., the addition of aprepitant (EMEND®) to ondansetron (Zofran®), with or without dexamethasone, in pediatric cancer patients resulted in approximately 50% of patients experiencing no vomiting or need for rescue medication in the 25–120 hours following chemotherapy, versus approximately 25% in the control group who received ondansetron alone.

Rising Popularity of Oral and Transdermal Drug Delivery Routes

The convenience of oral and transdermal delivery systems has gained prominence in antiemetic treatments. Patients prefer formulations that avoid injections or hospital visits. Transdermal patches deliver sustained symptom relief and minimize gastrointestinal irritation. It allows flexible dosing across oncology and motion sickness therapies. The Antiemetics Drugs Market witnesses higher demand for non-invasive options. Pharmaceutical innovators design controlled-release mechanisms for long-term symptom control. Oral dispersible tablets offer better patient compliance in pediatric and geriatric care. Such advancements enhance treatment experience and broaden global accessibility.

- For instance, ondansetron ODT (Zofran® orally disintegrating tablet) is extensively prescribed in pediatric regimens, with the FDA label specifying a pediatric dosage of one 4 mg ODT tablet given 3 times a day for children aged 4 to 11 following chemotherapy, reflecting widespread use for non-injectable antiemetic therapy.

Integration of Digital Health and Remote Prescription Monitoring

Digital health platforms now support remote prescription refills and nausea symptom tracking. Mobile applications and wearable sensors provide real-time patient feedback. It helps clinicians adjust antiemetic dosages efficiently and prevent complications. The Antiemetics Drugs Market integrates telemedicine with hospital care pathways. Pharmaceutical companies collaborate with tech firms for smart medication management. Digital adherence programs improve patient engagement and long-term compliance. Hospitals use electronic health records to monitor nausea frequency patterns. Integration of AI-driven data analytics strengthens post-treatment monitoring systems.

Increased Focus on Green Chemistry and Sustainable Drug Manufacturing

Pharmaceutical companies embrace environmentally sustainable production methods for antiemetic formulations. Green chemistry reduces waste, energy use, and hazardous solvent exposure. It aligns with global environmental safety and cost-efficiency goals. The Antiemetics Drugs Market benefits from sustainable manufacturing frameworks. Regulatory agencies encourage eco-friendly production to improve compliance and brand image. Companies redesign supply chains to minimize carbon footprints. Investments in biodegradable packaging and solvent recovery systems improve operational efficiency. The trend aligns with global pharmaceutical sustainability standards.

Market Challenges Analysis

High Treatment Costs and Limited Reimbursement Frameworks in Developing Economies

High drug prices restrict patient access to advanced antiemetic therapies in low-income regions. Patented receptor antagonists remain costly for large-scale procurement. Many healthcare systems lack comprehensive reimbursement programs for supportive cancer care. It limits adoption despite growing clinical need. The Antiemetics Drugs Market faces unequal affordability across geographies. Cost-sensitive hospitals prefer generic formulations with reduced efficacy. Pharmaceutical manufacturers must balance innovation with affordability to remain competitive. Slow approval processes and weak insurance frameworks further delay patient accessibility.

Adverse Effects and Drug Resistance Limiting Long-Term Use

Certain antiemetic drugs cause side effects such as dizziness, constipation, or headache. Prolonged use leads to receptor adaptation, reducing treatment effectiveness over time. It challenges healthcare providers to select safer, alternate options. The Antiemetics Drugs Market encounters resistance-related complications that hinder therapy success. Continuous dose adjustments increase clinical supervision costs. Patients often discontinue treatment due to recurring side effects. Pharmaceutical firms invest in safer, selective receptor modulators to overcome this issue. Improving drug tolerability and minimizing dependency remains a core industry focus.

Market Opportunities

Development of Personalized Medicine and Targeted Therapeutic Approaches

Pharmacogenomics enables customized antiemetic therapy based on individual genetic profiles. Clinicians use biomarker data to identify optimal drug combinations and doses. It enhances treatment precision and reduces adverse reactions. The Antiemetics Drugs Market benefits from personalized medicine integration in oncology care. Research institutions collaborate with biotech companies to develop patient-specific formulations. Hospitals adopt genomic screening for chemotherapy support programs. Advancements in molecular diagnostics expand opportunities for tailored antiemetic solutions. This trend fosters patient safety and optimized healthcare outcomes.

Expansion Across Emerging Markets Through Strategic Partnerships and Awareness Campaigns

Rising healthcare infrastructure in Asia-Pacific, Latin America, and Africa presents growth avenues. Pharmaceutical firms collaborate with local distributors to widen product reach. Public health campaigns promote awareness of nausea management and cancer care. The Antiemetics Drugs Market expands with improved access to treatment facilities. Partnerships with government agencies support training programs for physicians. Localization strategies reduce import dependence and ensure steady supply chains. Growing demand for generic and over-the-counter options strengthens market penetration. Education initiatives improve early diagnosis and timely treatment interventions.

Market Segmentation Analysis:

By Drug Type

The Antiemetics Drugs Market includes several pharmacological classes addressing diverse causes of nausea and vomiting. 5-HT3 receptor antagonists dominate due to their proven efficacy in chemotherapy and postoperative care. Dopamine antagonists maintain strong use in gastrointestinal and neurological conditions. NK1 receptor antagonists gain traction for their superior control in cancer therapy–related nausea. Antihistamines and anticholinergics remain popular in motion sickness management. Cannabinoids show growing acceptance in patients unresponsive to conventional therapy. Benzodiazepines assist in anxiety-related nausea control. It continues to diversify through expanded indications and novel receptor-specific drug approvals.

- For instance, in a meta-analysis of nine randomized controlled trials including 3,463 patients, palonosetron (marketed by Eisai and Helsinn) demonstrated significantly higher efficacy than first-generation 5-HT3 receptor antagonists, with cumulative relative risk reductions for vomiting over 5 days post-chemotherapy (RR = 1.23, 95% CI: 1.13-1.34; p<0.001)

By Application

The market spans a wide range of therapeutic applications. Chemotherapy-induced nausea and vomiting hold the largest share due to high cancer treatment demand. Postoperative nausea represents a consistent growth area in surgical care. Motion sickness and gastroenteritis applications drive demand across travel and infection-related disorders. Pregnancy-related nausea treatments gain visibility with safer drug formulations. Opioid-induced nausea remains a concern for chronic pain therapy. Dizziness management supports neurology and rehabilitation care needs. It benefits from ongoing research in targeted antiemetic solutions addressing multiple causes.

- For instance, in a pivotal phase III trial of 200 patients, Heron Therapeutics’ SUSTOL (granisetron extended-release) achieved a complete response rate (no emesis, no rescue medication) of 83% in the acute phase and 69% in the delayed phase following moderately emetogenic chemotherapy.

By End User

Hospitals lead due to their role in cancer, surgical, and emergency treatments requiring nausea management. Ambulatory surgical centers adopt antiemetic protocols for faster recovery outcomes. Cancer treatment centers account for significant usage owing to chemotherapy support needs. Clinics handle prescription renewals for chronic nausea and vestibular disorders. Homecare settings expand steadily through oral and transdermal formulations enabling patient convenience. It gains momentum with digital prescription systems and telemedicine-based monitoring. This diverse end-user landscape ensures consistent market penetration and strong therapeutic relevance.

Segmentation:

By Drug Type

- 5-HT3 (Serotonin) Receptor Antagonists

- Dopamine Antagonists

- NK1 (Neurokinin 1) Receptor Antagonists

- Antihistamines

- Cannabinoids

- Benzodiazepines

- Anticholinergics

- Others

By Application

- Chemotherapy-Induced Nausea and Vomiting (CINV)

- Postoperative Nausea and Vomiting (PONV)

- Motion Sickness

- Gastroenteritis

- Pregnancy-Related Nausea and Vomiting

- Opioid Analgesics-Induced Nausea

- Dizziness

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Cancer Treatment Centers

- Clinics

- Homecare Settings

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

North America holds the dominant share of 38% in the Antiemetics Drugs Market, driven by a strong cancer treatment infrastructure and rapid adoption of advanced antiemetic therapies. The region benefits from high healthcare spending, established reimbursement systems, and extensive clinical research in oncology and gastroenterology. The United States remains the primary revenue contributor due to widespread chemotherapy use and early introduction of NK1 receptor antagonists. Canada supports growth through national health programs emphasizing palliative and supportive care. It maintains high prescription rates across hospital and outpatient settings. Continuous regulatory approvals and digital prescribing platforms strengthen market expansion and accessibility.

Europe

Europe accounts for 27% of the global share, supported by well-structured healthcare systems and extensive use of antiemetics in cancer and surgical care. Countries such as Germany, the United Kingdom, France, and Italy maintain high utilization rates in oncology treatment centers. Pharmaceutical advancements and hospital-based drug procurement strategies promote steady product demand. The region’s focus on evidence-based medicine and regulatory harmonization enhances therapy standardization. It benefits from growing awareness of patient comfort and improved antiemetic efficacy. Rising adoption of oral and transdermal formulations across outpatient care further strengthens the market footprint.

Asia-Pacific

Asia-Pacific holds 25% of the global market share and exhibits the fastest growth pace due to expanding healthcare infrastructure and rising cancer incidence. China, Japan, and India drive demand with large patient populations and improving access to oncology treatments. Governments invest in healthcare modernization and affordable antiemetic availability under national cancer control programs. Local manufacturers develop cost-effective formulations to increase patient reach. The Antiemetics Drugs Market gains momentum in this region through clinical collaborations and increasing generic penetration. It benefits from growing medical tourism and public awareness of supportive care practices.

Latin America and Middle East & Africa

Latin America captures 6% share, supported by gradual healthcare expansion and improved access to hospital-based treatment. Brazil and Mexico lead the region through oncology and gastroenterology programs. The Middle East & Africa hold 4% share, with growth led by the UAE, Saudi Arabia, and South Africa. These regions face challenges from limited reimbursement coverage but show progress in hospital modernization. It advances with international pharmaceutical partnerships, improving drug distribution networks, and public health initiatives. Expansion of cancer care centers continues to support steady, long-term market penetration.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Pfizer Inc.

- GlaxoSmithKline plc (GSK)

- Johnson & Johnson

- Merck & Co., Inc.

- Sanofi S.A.

- Novartis AG

- Roche Holding AG

- Teva Pharmaceutical Industries Ltd.

- Cipla Limited

- Reddy’s Laboratories Ltd.

- Sun Pharmaceutical Industries Ltd.

- Hikma Pharmaceuticals PLC

Competitive Analysis:

The Antiemetics Drugs Market is highly competitive, with global pharmaceutical companies focusing on innovation, formulation improvement, and patient safety. Leading firms such as Pfizer, GSK, Novartis, and Merck strengthen their portfolios through next-generation 5-HT3 and NK1 receptor antagonists. Roche and Sanofi invest in oncology-linked antiemetic solutions integrated into cancer care protocols. Teva, Cipla, and Dr. Reddy’s emphasize generic and cost-effective options to expand accessibility in emerging markets. It experiences consistent product launches and regulatory approvals, supporting therapeutic diversity. Companies pursue mergers, licensing deals, and collaborations to enhance distribution efficiency. Strategic focus on targeted formulations and minimal side effects defines the evolving competitive landscape.

Recent Developments:

- In November 2025, Evoke Pharma, a specialty pharmaceutical company known for GIMOTI®, the first FDA-approved nasal spray formulation of metoclopramide, entered into a definitive agreement to be acquired by QOL Medical. This acquisition values Evoke Pharma at $11.00 per share and is expected to close by the end of 2025, reflecting a strategic move to leverage Evoke’s commercial products for gastrointestinal conditions.

- In January 2024, Johnson & Johnson announced its intention to acquire Ambrx Biopharma, a company developing next-generation antibody drug conjugates for oncology. The transaction, valued at approximately $2 billion, is intended to strengthen J&J’s oncology pipeline, which includes treatments requiring supportive care regimens where antiemetics are often co-administered.

Report Coverage:

The research report offers an in-depth analysis based on Drug Type, Application and End User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising cancer prevalence will sustain demand for advanced antiemetic therapies across global oncology centers.

- Development of novel receptor antagonists and personalized therapy will enhance treatment precision.

- Expanding generic drug production will improve affordability and patient access in developing nations.

- Increasing research on cannabinoid-based antiemetics will open new therapeutic pathways.

- Integration of digital prescription systems will streamline drug delivery and adherence monitoring.

- Growth of outpatient and ambulatory surgical care will boost demand for fast-acting antiemetic formulations.

- Expanding geriatric population will drive prescriptions for safer, better-tolerated antiemetic drugs.

- Strong collaborations between pharmaceutical and biotechnology firms will accelerate innovation pipelines.

- Regulatory support for novel dosage forms such as transdermal patches will improve convenience and compliance.

- Rising awareness about supportive cancer care will strengthen hospital procurement and global market penetration.