Market Overview

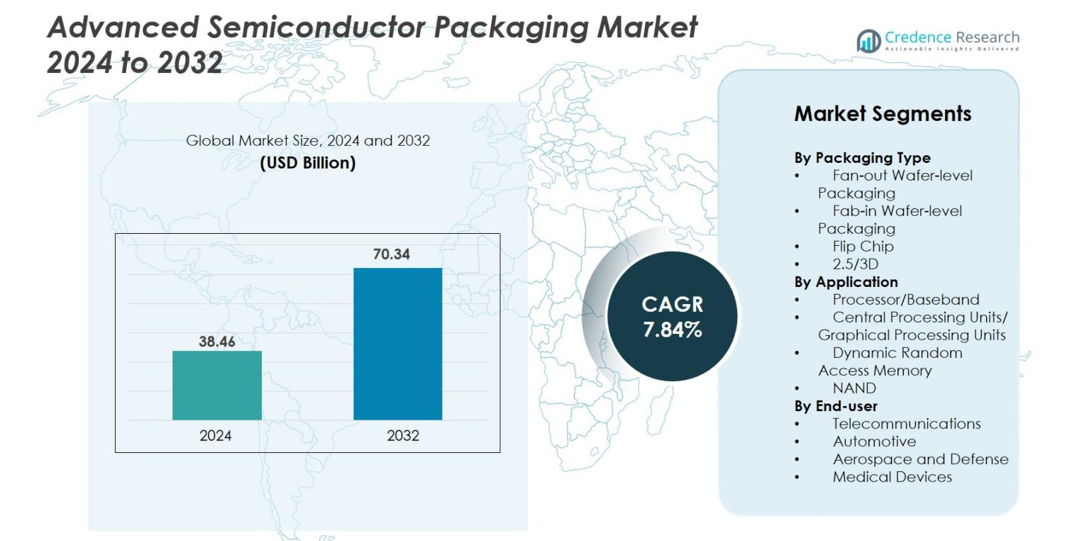

Advanced Semiconductor Packaging Market size was valued at USD 38.46 billion in 2024 and is anticipated to reach USD 70.34 billion by 2032, at a CAGR of 7.84% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Advanced Semiconductor Packaging Market Size 2024 |

USD 38.46 billion |

| Advanced Semiconductor Packaging Market , CAGR |

7.84% |

| Advanced Semiconductor Packaging Market Size 2032 |

USD 70.34 billion |

Advanced Semiconductor Packaging market continues to experience strong growth, supported by leading companies such as ASE Technology Holding Co., Ltd., Amkor Technology, Intel Corporation, Advanced Micro Devices, Inc., Infineon Technologies AG, STMicroelectronics, Hitachi, Ltd., Sumitomo Chemical Co., Ltd., KYOCERA Corporation and Avery Dennison Corporation. These players advance technologies including fan-out packaging, flip chip and 2.5D/3D integration to meet rising demand from AI, data centers, automotive electronics and 5G infrastructure. Asia-Pacific leads the market with over 41% share due to its strong semiconductor manufacturing base, followed by North America at about 32%, driven by high adoption in HPC, cloud and advanced computing applications.

Market Insights

- Advanced Semiconductor Packaging Market reached USD 38.46 billion in 2024 and is set to hit USD 70.34 billion by 2032, expanding at a CAGR of 7.84% during the forecast period.

- Market growth is driven by rising adoption of high-performance computing, AI accelerators, CPUs/GPUs and memory devices, with CPUs/GPUs leading applications at 35 % share and flip-chip dominating packaging types at 40 percent share.

- Trends highlight rapid momentum in 2.5D/3D IC integration and fan-out wafer-level packaging as demand surges for miniaturization, high bandwidth and better thermal performance across mobile, AI and data-center devices.

- Key players strengthen the landscape with advanced integration technologies, including ASE, Amkor, Intel, AMD, STMicroelectronics, Infineon and Hitachi, focusing on thermal efficiency, chiplet architectures and heterogeneous integration.

- Regional analysis shows Asia-Pacific leading with 41% share, followed by North America at 32% and Europe at 22 %, while telecom end-users dominate with 38% market share.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis

By Packaging Type

The Advanced Semiconductor Packaging market shows strong momentum across fan-out wafer-level packaging, fab-in wafer-level packaging, flip chip, and 2.5/3D IC packaging. Flip chip remains the dominant sub-segment, accounting for 40% market share in 2024 due to its high I/O density, strong thermal performance and suitability for advanced logic and high-performance computing devices. The rapid adoption of 2.5/3D packaging is also accelerating, driven by the need for heterogeneous integration and improved bandwidth in AI accelerators and data-center processors. The shift toward miniaturization and enhanced electrical performance continues to fuel demand for wafer-level packaging solutions.

- For instance, Intel’s Foveros 3D stacking technology incorporates die-to-die bump pitches as small as 36 microns, allowing vertical integration of compute tiles in products such as Meteor Lake.

By Application

Processor/baseband, CPUs/GPUs, DRAM and NAND remain key application areas in the Advanced Semiconductor Packaging market. The CPUs/GPUs segment leads with 35% market share, supported by rising AI workloads, gaming demand and data-center expansion. DRAM and NAND packaging continue gaining traction as memory technologies evolve toward higher density and faster throughput. Processor/baseband packaging is strengthened by widespread 5G deployment. Across applications, the primary drivers include rising compute requirements, increased demand for energy-efficient processing and the shift toward advanced nodes requiring specialized high-performance packaging.

- For instance, NVIDIA’s H100 GPU uses TSMC’s 2.5D CoWoS packaging with 6 HBM3 stacks delivering an aggregate memory bandwidth of 3 TB/s, enabling high-throughput AI training workloads.

By End-user

Telecommunications, automotive, aerospace & defense and medical devices represent the key end-use segments in the Advanced Semiconductor Packaging market. Telecommunications dominates with 38% share, driven by rapid 5G infrastructure rollout, high-bandwidth networking equipment and increased data-traffic demands. The automotive segment is growing quickly as EVs, ADAS and autonomous driving systems rely heavily on high-reliability advanced packaging. Aerospace & defense benefits from rad-hard, high-precision semiconductor solutions, while medical devices demand miniaturized, energy-efficient and reliable chips. Increasing digitalization and performance requirements across industries remain major demand drivers.

Key Growth Drivers

Rising Demand for High-Performance Computing and AI Acceleration

The Advanced Semiconductor Packaging market experiences strong growth due to the accelerating adoption of high-performance computing (HPC), AI accelerators and data-center processors that require advanced packaging to achieve superior bandwidth, thermal efficiency and interconnect density. AI workloads demand faster transfer rates between logic and memory, making technologies like 2.5D/3D packaging, HBM integration and hybrid bonding essential. Hyperscale data-center operators, semiconductor foundries and cloud service providers increasingly rely on advanced packaging to overcome the limitations of traditional scaling. Additionally, the surge in generative AI, machine learning models and cloud-based computation further boosts reliance on architectures supported by advanced packaging. As transistor miniaturization approaches physical limits, packaging innovation becomes a core enabler of performance improvements, driving sustained investment and technological advancements in the market.

- For instance, AMD’s MI300A APU integrates CPU, GPU and HBM components using 3D stacking and chiplet packaging, combining 24 Zen 4 cores with 128 GB of HBM3 to accelerate large-scale AI model training and scientific computing.

Expansion of 5G, IoT Ecosystems and Advanced Connectivity Requirements

The rollout of 5G networks and the explosive growth of IoT ecosystems significantly propel demand for advanced semiconductor packaging. 5G infrastructure, small cells, RF modules and high-frequency communication devices rely on compact, thermally robust packaging technologies that support high-speed data transmission. Fan-out wafer-level packaging and flip chip packaging are widely adopted to enable miniaturized, power-efficient, and high-performance 5G components. IoT devices—ranging from smart home systems to industrial automation platforms—require reliable, low-power packaging for sensors, microcontrollers and connectivity chips. Ultra-reliable and low-latency communications (URLLC) create additional packaging complexity, further accelerating innovation. As consumer, industrial and enterprise applications increasingly depend on seamless connectivity, demand for specialized semiconductor packaging solutions continues to rise.

- For instance, Qualcomm’s QTM545 mmWave antenna module uses advanced packaging technologies and integrates multiple phased-array antennas capable of supporting beamforming operations up to 43.5 GHz, enabling compact 5G smartphone designs.

Automotive Electrification and ADAS Driving Semiconductor Complexity

The rapid transition toward electric vehicles (EVs), hybrid vehicles and advanced driver-assistance systems (ADAS) fuels demand for high-reliability semiconductor packaging. Automotive electronics now require advanced packaging to support radar, LiDAR, power management ICs, battery-control units and infotainment processors. These applications demand exceptional durability, wide temperature tolerance and strong thermal stability, placing advanced packaging at the center of innovation. Technologies like flip chip, fan-out and multi-chip integration play critical roles in enabling faster processing, enhanced safety features and greater efficiency. As global automakers invest heavily in autonomous driving and electrification, semiconductor content per vehicle continues rising sharply, making automotive one of the largest emerging growth drivers in the advanced packaging market.

Key Trends & Opportunities

Rapid Shift Toward 2.5D and 3D Heterogeneous Integration

A major trend shaping the Advanced Semiconductor Packaging market is the shift toward 2.5D and 3D heterogeneous integration, which enables multiple dies—logic, memory, analog and RF—to coexist within a compact, high-performance package. This trend offers exceptional opportunities for device makers aiming to overcome traditional scaling limitations of Moore’s Law. Technologies such as TSVs (through-silicon vias), chiplet integration and hybrid bonding are becoming essential for next-generation computing platforms. Companies increasingly adopt chiplet-based architectures to improve manufacturing flexibility, reduce cost and enhance performance. The growing need for edge AI, HPC and advanced networking offers substantial opportunities for 3D packaging providers to deliver modular, scalable and energy-efficient semiconductor solutions.

- For instance, Sony’s CMOS image sensors employ 3D stacked architectures integrating a pixel layer and logic layer connected through thousands of TSVs, improving signal processing speed and achieving readout rates exceeding 120 frames per second in high-resolution sensors.

Growing Adoption of Fan-Out Packaging for Mobile and Consumer Devices

Fan-out wafer-level packaging (FOWLP) continues emerging as a key opportunity area due to its ability to deliver thinner profiles, high I/O density and improved electrical performance required for smartphones, wearables and AR/VR devices. As OEMs push for ultra-thin, multi-functional consumer electronics, demand for FOWLP grows significantly. Its capability to integrate RF components, application processors and PMICs within compact architectures makes it ideal for next-generation mobile platforms. Additionally, opportunities expand in infotainment chips, sensor hubs and power modules across consumer electronics. The combination of low-cost, high-bandwidth and form-factor advantages positions fan-out packaging as a central opportunity for semiconductor manufacturers.

- For instance, Apple’s A10 Fusion processor was one of the first major smartphone chips manufactured using TSMC’s InFO fan-out packaging, achieving a package thickness of 0.8 mm while maintaining high I/O routing density suitable for flagship mobile devices.

Key Challenges

High Manufacturing Costs and Complex Production Processes

One of the biggest challenges in the Advanced Semiconductor Packaging market is the high cost associated with manufacturing and process complexity. Advanced techniques like TSV-based 3D packaging, hybrid bonding and chiplet integration require expensive equipment, precise process control and highly skilled engineering. Yield losses can be significant due to increased design intricacy, multi-die stacking and thermal management requirements. These challenges elevate production costs and limit adoption among smaller manufacturers. As devices grow more complex, maintaining consistent reliability and quality becomes increasingly difficult. The need for significant capital investment also restrains new entrants from scaling advanced packaging capabilities.

Thermal Management and Reliability Constraints in High-Density Integration

As semiconductor devices move toward higher functional density, managing heat dissipation and ensuring long-term reliability becomes a critical challenge. Advanced packaging technologies, especially 3D stacked solutions, face inherent thermal limitations that can lead to performance degradation, electromigration and device failure. Ensuring structural integrity under high-power operation is a major engineering concern, particularly in automotive, aerospace and industrial applications. Complexities in material selection, interconnect design and heat-spreader integration further complicate thermal management. Overcoming these constraints requires innovative cooling solutions, advanced materials and robust reliability testing, creating technical hurdles for manufacturers.

Regional Analysis

North America

North America holds a strong position in the Advanced Semiconductor Packaging market, accounting for 32% share in 2024, driven by robust demand from data centers, AI accelerators and advanced computing platforms. The U.S. dominates regional adoption due to strong semiconductor R&D, rapid HPC deployment and expansion of cloud infrastructure. Leading foundries and OSATs continue investing in advanced packaging technologies such as 2.5D, 3D ICs and chiplet architectures. Growth is further supported by government initiatives to localize semiconductor manufacturing. Increasing adoption in telecommunications and automotive electronics reinforces North America’s continued leadership in the market.

Europe

Europe represents 22% market share in the Advanced Semiconductor Packaging market, supported by strong automotive, industrial automation and aerospace demand. Packaging innovation accelerates as European automakers integrate advanced electronics for EVs, ADAS and autonomous systems. Germany, France and the U.K. lead adoption due to high semiconductor usage in power electronics, sensors and high-reliability systems. Growing investments in chip manufacturing under EU Chips Act programs further strengthen regional capabilities. Europe’s emphasis on energy-efficient, high-reliability semiconductor packaging drives adoption of fan-out, flip-chip and advanced multi-chip solutions across automotive and industrial applications.

Asia-Pacific

Asia-Pacific dominates the Advanced Semiconductor Packaging market with 41% share, driven by strong manufacturing bases in China, Taiwan, South Korea and Japan. The region leads global OSAT capacity, wafer fabrication and memory production, supporting large-scale adoption of flip-chip, fan-out and 2.5/3D packaging. Rising demand for smartphones, consumer electronics, 5G devices and AI servers fuels continuous expansion. Major semiconductor companies and foundries invest heavily in advanced packaging lines, especially in Taiwan and South Korea. Asia-Pacific’s cost advantages, ecosystem maturity and rapid technology adoption ensure its continued leadership in high-volume and high-performance packaging demand.

Latin America

Latin America holds 3% market share in the Advanced Semiconductor Packaging market, with gradual growth driven by expanding telecom infrastructure, increasing electronics consumption and rising adoption of connected automotive solutions. Brazil and Mexico lead demand due to strengthening industrial automation and consumer electronics markets. The region relies heavily on imports of advanced semiconductor devices, but growth in IoT deployment, smart manufacturing and 5G mobility is creating opportunities for increased adoption of packaged semiconductors. While local manufacturing capacity remains limited, rising digital transformation initiatives are expected to support steady future growth.

Middle East & Africa

The Middle East & Africa region accounts for 2% share of the Advanced Semiconductor Packaging market, driven primarily by increasing investments in telecommunications, defense electronics and smart city infrastructure. Countries such as the UAE, Saudi Arabia and South Africa are expanding demand for advanced semiconductor components used in networking equipment, industrial devices and security systems. Increased focus on digital transformation and AI adoption supports gradual market growth. Although the region lacks semiconductor manufacturing capabilities, strong import demand and rising deployment of high-performance electronics contribute to steady adoption of advanced packaging solutions.

Market Segmentations

By Packaging Type

- Fan-out Wafer-level Packaging

- Fab-in Wafer-level Packaging

- Flip Chip

- 2.5/3D

By Application

- Processor/Baseband

- Central Processing Units/ Graphical Processing Units

- Dynamic Random Access Memory

- NAND

By End-user

- Telecommunications

- Automotive

- Aerospace and Defense

- Medical Devices

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Advanced Semiconductor Packaging market features a dynamic competitive landscape driven by continuous innovation, capacity expansion and rising investments in next-generation technologies. Key players such as ASE Technology Holding Co., Ltd., Amkor Technology, Intel Corporation, Advanced Micro Devices, Inc., Infineon Technologies AG, STMicroelectronics, Hitachi, Ltd., Sumitomo Chemical Co., Ltd., KYOCERA Corporation, and Avery Dennison Corporation actively strengthen their portfolios with advanced solutions including fan-out packaging, flip-chip, 2.5D/3D integration and heterogeneous chiplet architectures. Leading OSATs expand production capabilities to meet growing demand from AI, 5G, automotive and high-performance computing markets, while IDMs focus on proprietary packaging innovations to optimize performance and energy efficiency. Strategic partnerships between foundries, material suppliers and equipment manufacturers accelerate technology development and commercial scalability. Companies increasingly invest in R&D to enhance thermal management, high-density interconnects and cost-effective packaging approaches. As device complexity rises, competition intensifies around integration capabilities, reliability and time-to-market performance.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In November 2025, IBM and University of Dayton announced a joint research collaboration to advance next-generation semiconductor technologies including advanced packaging and photonics.

- In September 2025, LCY Chemical Corp. launched its “Advanced Formulations” for semiconductor advanced packaging—high-precision materials (hydrocarbon polymers, colourless polyimide) tailored for high-integration, high-precision packaging in AI/HPC markets.

- In May 2025, GlobalFoundries signed an MOU with A*STAR (Singapore) to accelerate advanced packaging innovation through R&D collaboration and support for GF’s Singapore manufacturing facility.

Report Coverage

The research report offers an in-depth analysis based on Packaging Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will accelerate due to rising adoption of AI, HPC and next-generation data-center architectures.

- 5D and 3D heterogeneous integration will become the preferred approach for advanced logic and memory devices.

- Chiplet-based designs will gain widespread adoption across consumer, automotive and enterprise applications.

- Fan-out wafer-level packaging demand will grow as mobile, wearable and AR/VR devices require thinner, high-density solutions.

- Automotive electronics, especially EVs and ADAS, will significantly expand their share in advanced packaging consumption.

- Advanced thermal management materials and cooling technologies will become essential for high-power semiconductor designs.

- Foundry-OSAT collaborations will increase to accelerate packaging innovation and reduce time-to-market.

- Regional manufacturing expansion will intensify, driven by localization efforts across Asia-Pacific, North America and Europe.

- AI-driven design automation tools will streamline multi-chip integration and reduce development complexity.

- Sustainability measures will shape new packaging materials and processes to reduce power consumption and manufacturing waste.