Market Overview

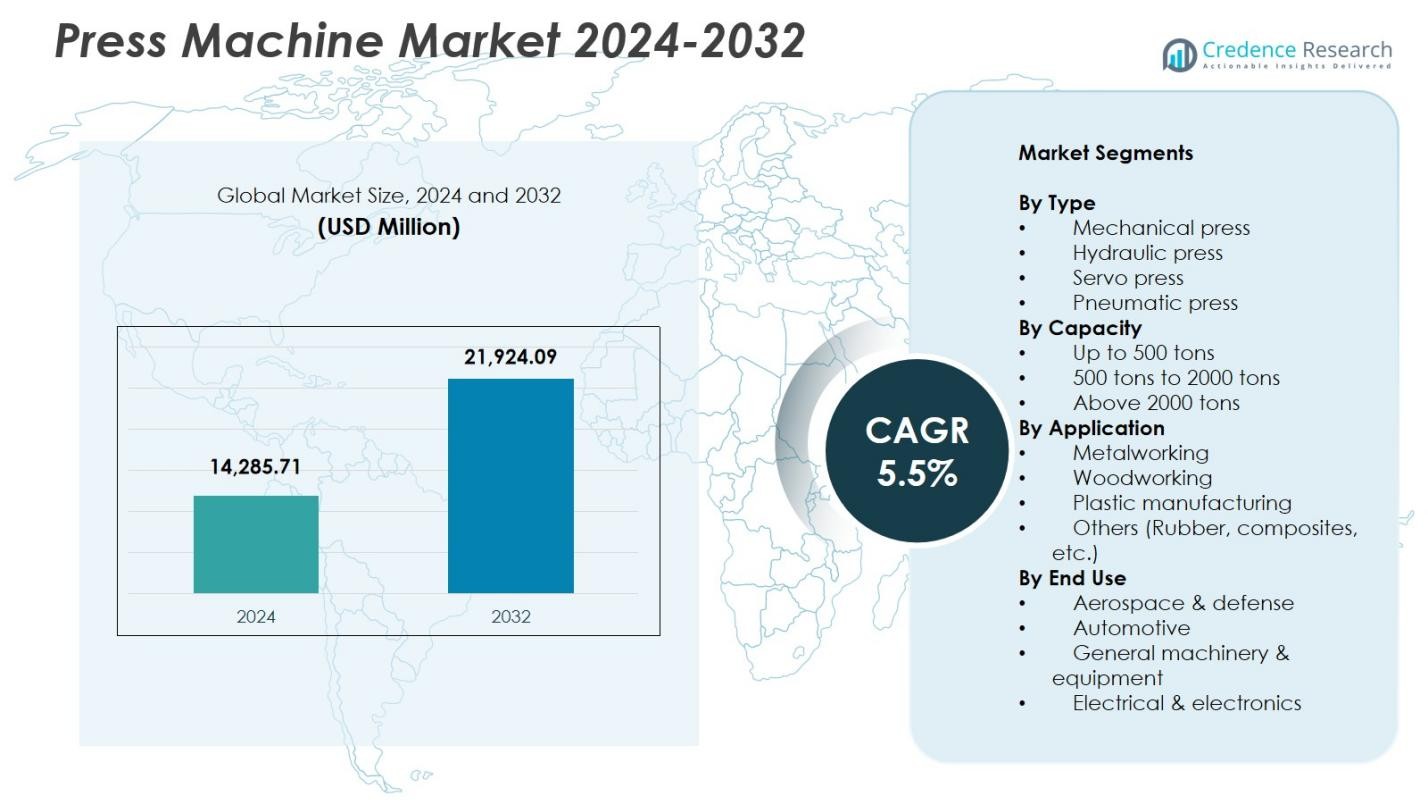

Press Machine Market size was valued at USD 14,285.71 Million in 2024 and is anticipated to reach USD 21,924.09 Million by 2032, at a CAGR of 5.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Press Machine Market Size 2024 |

USD 14,285.71 Million |

| Press Machine Market, CAGR |

5.5% |

| Press Machine Market Size 2032 |

USD 21,924.09 Million |

Press Machine Market features leading players such as Schuler Group, AMADA PRESS SYSTEM CO., LTD., Komatsu Ltd., Nidec Minster, Beckwood Press, Macrodyne Technologies Inc., BRUDERER AG, Bliss-Bret, Isgec Heavy Engineering Ltd., and AIDA, all of which strengthen global adoption through advanced mechanical, hydraulic, and servo press solutions. These companies focus on technological innovation, automation integration, and high-precision forming systems that support automotive, aerospace, and metal fabrication industries. Asia-Pacific led the Press Machine Market in 2024 with 38.6% share, driven by large-scale manufacturing activities in China, Japan, India, and South Korea, while North America and Europe followed with strong demand for automated and energy-efficient press technologies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Press Machine Market reached USD 14,285.71 Million in 2024 and will grow at a CAGR of 5.5% through 2032.

- Market expansion is driven by rising adoption of mechanical presses, which held a 41.8% share, supported by strong demand from automotive, aerospace, and metal fabrication industries.

- Key trends include rapid integration of servo-driven technology, automation, and smart factory systems that enhance precision, efficiency, and operational safety across industrial production lines.

- Leading players such as Schuler Group, AMADA PRESS SYSTEM CO., LTD., Komatsu Ltd., and Nidec Minster strengthen market presence through innovation in high-tonnage, energy-efficient, and digitally enabled press systems.

- Asia-Pacific dominated with a 38.6% regional share, followed by North America at 27.4% and Europe at 24.9%, while the metalworking segment led applications with a 54.7% share, reflecting strong industrial manufacturing activity worldwide.

Market Segmentation Analysis:

Market Segmentation Analysis:

By Type

The Press Machine Market by type is dominated by mechanical presses, accounting for 41.8% share in 2024, driven by their high-speed operation, cost-efficiency, and suitability for mass production across automotive, electronics, and metal fabrication industries. Mechanical presses support consistent stroke cycles and superior repeatability, making them the preferred choice for stamping and blanking operations. Hydraulic presses follow due to their precision and flexibility in handling thicker materials, while servo presses gain traction for energy savings and programmable motion control. Pneumatic presses maintain stable adoption in light-duty applications, particularly in small-scale assembly and component fabrication.

- For instance, Hudson Technologies employs hydraulic presses to produce cryogenic pump housings from heavy-gauge stainless steel, maintaining tight wall thickness tolerances through controlled draw sequences.

By Capacity

The Up to 500 tons capacity segment held the leading position with 46.3% share in 2024, supported by strong utilization in small and medium manufacturing units involved in stamping, light metal forming, and electronics component production. This segment benefits from lower installation costs, compact machine footprint, and adaptability across multiple fabrication tasks. The 500 to 2000 tons segment grows steadily as automotive and heavy machinery industries expand large-part forming operations, while the Above 2000 tons segment gains demand from shipbuilding, defense, and structural steel fabrication requiring high-force forming capabilities.

- For instance, French Oil’s 2000 ton hydraulic press system features sideplate construction with a 64 x 64 inch pressing surface and up-acting cylinder for molding large seals in oil and gas manufacturing.

By Application

The metalworking segment dominated the Press Machine Market with 54.7% share in 2024, driven by extensive use in automotive body parts, aerospace components, industrial machinery, and sheet-metal fabrication. Continuous investment in automated stamping lines, lightweight metal forming, and high-precision machining technologies supports its leadership. Woodworking machines show steady adoption in furniture and panel processing industries, while plastic manufacturing presses benefit from rising demand for molded components. The Others segment (rubber and composites) expands gradually as composite materials gain traction in EVs, industrial equipment, and lightweight structural applications.

Key Growth Drivers

Rising Demand from Automotive and Metal Fabrication Industries

Surging production of automotive components, metal parts, and engineered structures significantly drives the Press Machine Market. Automakers increasingly invest in high-speed stamping, deep drawing, and precision forming systems to support vehicle lightweighting and EV component manufacturing. Metal fabrication facilities adopt advanced presses to enhance throughput, reduce operational downtime, and maintain consistent product quality. Growing modernization of manufacturing plants, along with automation-led efficiency improvements, further accelerates adoption. This strong industrial reliance positions press machines as essential assets in meeting global production volume and precision requirements.

- For instance, Toyota implemented high-speed die stamping machines with servo-driven technology to produce automotive components involving complex geometries, incorporating automated storage systems to optimize material flow.

Advancements in Servo and Hybrid Press Technologies

Technological innovations, particularly servo-driven and hybrid press systems, act as major growth catalysts. These machines offer programmable motion control, superior energy efficiency, reduced noise, and enhanced precision during complex forming operations. Manufacturers benefit from improved flexibility, allowing production of intricate components with minimized setup times and enhanced safety. The ability to integrate presses with real-time monitoring, predictive maintenance tools, and smart factory platforms strengthens their appeal in highly automated production environments. As industries transition toward Industry 4.0 frameworks, demand for intelligent press systems continues to rise.

- For instance, AIDA’s DSF Series direct drive servo presses use servo motors ranging from 60 to 3,000 tons capacity to transmit power directly without reducers, enabling precise ram motion control and built-in energy management that suppresses peak electrical power.

Expansion of Manufacturing Capacity in Emerging Economies

Rapid industrialization in Asia-Pacific, Latin America, and parts of Eastern Europe boosts market growth as governments promote local manufacturing and infrastructure expansion. Small and medium enterprises increasingly adopt cost-effective press machines to improve productivity and meet rising export demands. Favorable policies such as tax incentives, technology parks, and industrial corridor development further encourage equipment investments. Additionally, global manufacturers establish new facilities or expand existing ones in low-cost regions to optimize supply chains. This shift toward regional production hubs strengthens demand for versatile and high-capacity press machines.

Key Trends & Opportunities

Growing Adoption of Automation and Smart Manufacturing

Automation-driven production lines are becoming a key trend as manufacturers integrate robots, sensors, and digital control systems with press machines. This trend supports improved operational safety, real-time process optimization, and reduced labor dependency. Smart presses capable of self-diagnosis, adaptive force control, and predictive analytics create new opportunities for efficiency gains. Industries focused on precision components, such as EV parts and electronics, increasingly require automated presses to achieve tighter tolerances and shorter cycle times. The shift toward connected and intelligent manufacturing environments broadens opportunities for advanced press machine solutions.

- For instance, SCHUNK’s electrical and sensor-based clamping systems monitor clamping status, workpieces, and tool vibrations in real time. Integrated into robotic applications, they support flexible automation cells like GROW for tasks such as laser marking or part separation.

Increasing Use of Lightweight Materials in End-Use Industries

The growing preference for lightweight materials in automotive, aerospace, and electronics sectors creates significant opportunities for advanced forming technologies. Press machines capable of handling aluminum, high-strength steel, composites, and multi-material structures are in high demand. Manufacturers deploy flexible forming presses to achieve complex geometries while maintaining structural integrity and durability. This trend is reinforced by global fuel-efficiency regulations, EV adoption, and sustainability goals. As lightweighting becomes integral to product design, innovative pressing techniques and high-precision systems gain prominence across industrial supply chains.

- For instance, the fischer group uses HFQ aluminum hotforming technology to produce 10 structural components, including an outer door ring weighing less than 9kg that integrates the A-pillar, B-pillar, and sill for a premium EV sedan.

Key Challenges

High Initial Investment and Integration Costs

Despite strong industrial demand, the high capital cost of advanced press machines presents a major challenge for small and medium manufacturers. Acquisition expenses, combined with installation, tooling, and integration costs for automation systems, often delay technology upgrades. Companies struggle to justify investments without clear ROI visibility, particularly in regions with fluctuating production volumes. Financing constraints further reduce adoption in developing markets. These barriers limit modernization efforts and widen the technological gap between large enterprises and smaller production units requiring cost-efficient forming solutions.

Maintenance Complexity and Skilled Labor Shortage

Press machines, especially servo and hydraulic systems, require specialized maintenance to ensure reliable, safe, and continuous operation. The shortage of skilled technicians capable of diagnosing mechanical, electrical, and control-related issues increases operational risks. Unplanned downtime, improper calibration, and safety non-compliance add to production costs and reduce equipment lifespan. As manufacturing processes become more automated and digitally integrated, the need for highly trained personnel intensifies. This persistent skills gap challenges industry players, slowing the adoption of advanced press technologies and impacting overall operational efficiency.

Regional Analysis

North America

North America held 27.4% share in 2024, driven by strong adoption of advanced mechanical, hydraulic, and servo press machines across automotive, aerospace, and metal fabrication industries. The U.S. leads regional demand as manufacturers invest in automation, digital monitoring systems, and high-speed forming technologies to improve productivity and reduce operational downtime. The expansion of EV manufacturing, coupled with reshoring initiatives, strengthens the need for precision forming solutions. Canada contributes through steady growth in industrial machinery, fabricated metal products, and energy-sector component manufacturing, reinforcing overall market expansion.

Europe

Europe accounted for 24.9% share in 2024, supported by well-established automotive production hubs in Germany, France, Italy, and the U.K. The region’s focus on lightweight metal forming, energy-efficient systems, and stringent manufacturing standards boosts demand for advanced press machines. Investments in Industry 4.0, including smart presses equipped with servo technology and integrated automation, further drive adoption. Eastern European countries show rising consumption as global OEMs expand localized manufacturing. Additionally, the aerospace and industrial machinery sectors benefit from precision forming capabilities, strengthening Europe’s role as a technology-driven press machine market.

Asia-Pacific

Asia-Pacific dominated the Press Machine Market with 38.6% share in 2024, driven by massive manufacturing activity in China, Japan, India, and South Korea. The region benefits from large-scale automotive, electronics, metalworking, and construction component production, creating high demand for mechanical and hydraulic presses. Government initiatives promoting industrial automation, export-oriented manufacturing, and capacity expansion further accelerate adoption. China leads with extensive press machine manufacturing and consumption, while India’s rapid industrialization and “Make in India” incentives fuel market growth. Strong supplier ecosystems and cost-effective production enhance the region’s leadership.

Latin America

Latin America held 5.6% share in 2024, supported by growing metal fabrication, automotive assembly, and machinery production activities in Brazil, Mexico, and Argentina. Demand is driven by increased investments in industrial modernization, infrastructure development, and OEM expansion. Brazil’s automotive and agricultural machinery sectors adopt advanced forming technologies to enhance productivity, while Mexico benefits from nearshoring trends that boost manufacturing capacity. Despite economic fluctuations, rising SME investments in compact and mid-capacity press machines sustain market development. Continued regional industrialization strengthens long-term growth potential.

Middle East & Africa

The Middle East & Africa region captured 3.5% share in 2024, influenced by expanding construction, metal fabrication, and industrial machinery sectors in the UAE, Saudi Arabia, and South Africa. Infrastructure megaprojects and diversification efforts under national development programs stimulate demand for forming and stamping equipment. The region increasingly adopts hydraulic and mechanical presses for steel fabrication, automotive servicing components, and heavy-equipment manufacturing. South Africa’s established mining and machinery industries further contribute to demand. Although adoption levels remain moderate, increasing industrial investments and technology upgrades support steady market growth.

Market Segmentations:

By Type

- Mechanical press

- Hydraulic press

- Servo press

- Pneumatic press

By Capacity

- Up to 500 tons

- 500 tons to 2000 tons

- Above 2000 tons

By Application

- Metalworking

- Woodworking

- Plastic manufacturing

- Others (Rubber, composites, etc.)

By End Use

- Aerospace & defense

- Automotive

- General machinery & equipment

- Electrical & electronics

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Press Machine Market is shaped by leading manufacturers such as Schuler Group, AMADA PRESS SYSTEM CO., LTD., Nidec Minster, Beckwood Press, Komatsu Ltd., Macrodyne Technologies Inc., BRUDERER AG, Bliss-Bret, Isgec Heavy Engineering Ltd., and AIDA. These companies focus on expanding product portfolios across mechanical, hydraulic, servo, and high-tonnage press systems to meet the evolving needs of automotive, metal fabrication, aerospace, and industrial machinery sectors. Market participants prioritize innovations in servo-driven technology, automation integration, real-time monitoring, and energy-efficient designs to enhance precision and productivity. Strategic partnerships, regional expansions, and investments in smart manufacturing solutions strengthen their competitive positioning. Additionally, companies increasingly emphasize customized presses tailored to specific forming requirements, enabling them to cater to diverse industrial applications. Continuous technological advancements, aftermarket service capabilities, and strong global distribution networks further reinforce the leadership of established players in driving long-term market growth.

Key Player Analysis

- Schuler Group

- AMADA PRESS SYSTEM CO., LTD.

- Nidec Minster

- Beckwood Press

- Komatsu Ltd.

- Macrodyne Technologies Inc.

- BRUDERER AG

- Bliss-Bret

- Isgec Heavy Engineering Ltd.

- AIDA

Recent Developments

- In July 2025 Nidec Drive Technology (part of Nidec) unveiled the new straight-side link press SX-8-360, capable of 3,000 spm, and the large-capacity TVX-4000-430 press for heavy motor cores at the MF‑TOKYO 2025 exhibition.

- In October 2024 Nidec Minster acquired Canadian press-room automation supplier Linear Automation Inc. to expand its global press and automation offerings.

- In December 2024 Schuler Group partnered with Ceer Manufacturing Complex to install its first fully automatic press shop in the Middle East, marking a significant expansion in smart-manufacturing deployment.

- In January 2022 Macrodyne Technologies Inc. acquired German press-maker Dunkes GmbH, broadening its hydraulic press portfolio and European manufacturing footprint.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Type, Capacity, Application, End Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for advanced servo and hybrid presses will rise as manufacturers prioritize precision and energy efficiency.

- Adoption of automation-integrated press machines will accelerate across automotive and metalworking industries.

- Lightweight material forming will create new opportunities for high-flexibility and high-tonnage presses.

- Emerging economies will expand press installation capacity due to industrialization and manufacturing investments.

- Smart factory integration with IoT, sensors, and predictive maintenance will become standard practice.

- Custom-built presses tailored to specific production needs will gain stronger market preference.

- EV component manufacturing will significantly boost demand for high-precision forming equipment.

- Sustainability initiatives will drive the shift toward low-noise, low-energy, and eco-efficient press systems.

- Replacement of aging equipment in developed markets will support long-term machinery upgrades.

- Strategic collaborations between press manufacturers and automation providers will shape future technological advancements.