Market Overview

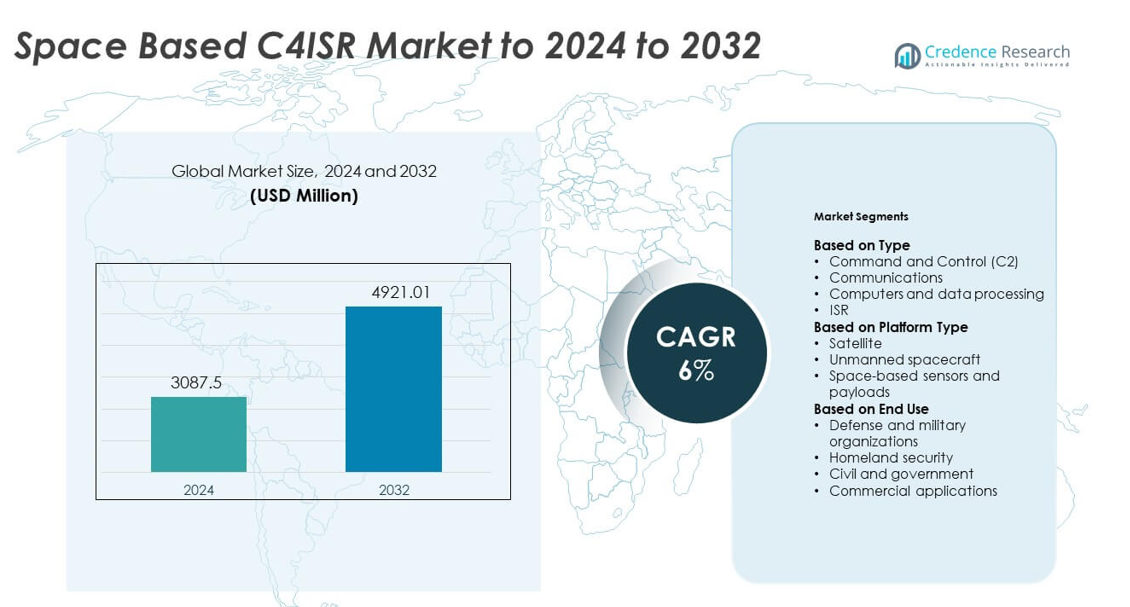

Space Based C4ISR Market size was valued at USD 3087.5 million in 2024 and is anticipated to reach USD 4921.01 million by 2032, at a CAGR of 6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Space Based C4ISR Market Size 2024 |

USD 3087.5 million |

| Space Based C4ISR Market, CAGR |

6% |

| Space Based C4ISR Market Size 2032 |

USD 4921.01 million |

The Space Based C4ISR Market features major companies including Lockheed Martin Corporation, Maxar Technologies Ltd, CACI International Inc., Elbit Systems Ltd, General Dynamics Corporation, Kratos Defense & Security Solutions Inc., Northrop Grumman Corporation, BAE Systems PLC, and The Boeing Company. These players drive advancements in satellite communication, ISR payloads, and secure data processing for defense missions. Strong investment in AI-enabled analysis, multi-orbit networks, and resilient architectures supports their competitive reach. North America remained the leading region in 2024 with about 41% share, followed by Europe and Asia Pacific, which continued to expand due to rising defense modernization efforts.

Market Insights

- Space Based C4ISR Market reached USD 3087.5 million in 2024 and will hit USD 4921.01 million by 2032 at a 6% CAGR.

- Growth is driven by rising defense modernization, expanding ISR deployment, and strong demand for secure satellite communication across multi-domain operations.

- Key trends include rapid expansion of low-earth-orbit constellations, AI-enabled analytics for real-time decision support, and increasing commercial participation in space-based imaging and communication services.

- The market remains competitive with major companies advancing high-resolution payloads, resilient communication links, and multi-orbit integration while facing restraints such as high deployment costs and rising space security risks.

- North America led with about 41% share in 2024, followed by Europe at nearly 26% and Asia Pacific at 22%, while satellites held around 65% share as the dominant platform segment.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Type

Command and Control C2 led the Space Based C4ISR Market in 2024 with about 38% share. Demand grew as nations expanded real-time battle management, threat tracking, and mission coordination through resilient space networks. C2 systems supported faster decision cycles and stronger situational awareness across multi-domain operations. Communications also grew as satellite links enabled high-bandwidth data transfer for defense missions. ISR adoption rose with higher use of electro-optical, infrared, and radar payloads. Computers and data processing advanced due to rising AI use in autonomous threat detection and data fusion.

- For instance, Lockheed Martin’s AEHF satellites support user data rates up to 8.2 Mbit/s on protected links, enabling hardened command-and-control communications for deployed forces.

By Platform Type

Satellites dominated this segment in 2024 with nearly 65% share. Growth came from heavy investment in LEO constellations that enhance global coverage, secure communications, and persistent surveillance. Defense programs relied on satellites for navigation, missile warning, and encrypted connectivity. Space-based sensors and payloads expanded as nations deployed advanced imaging and hyperspectral systems. Unmanned spacecraft gained attention due to repair, servicing, and inspection missions, yet remained smaller due to limited operational deployment and high cost barriers.

- For instance, Iridium’s upgraded Iridium NEXT constellation fields 66 operational cross-linked satellites in orbit at roughly 780 km altitude, providing global low-latency connectivity for military and government users.

By End Use

Defense and military organizations held the leading share in 2024 at about 58%. Expansion came from rising geopolitical tensions, modernization programs, and demand for resilient space architectures that support command, communication, and surveillance needs. Militaries used space assets to improve precision targeting, missile warning, and secure information flow. Homeland security grew with interest in border monitoring and disaster response support. Civil and government users applied C4ISR systems for environmental tracking and national space programs. Commercial applications rose as private players adopted satellite analytics for communication, imaging, and navigation services.

Key Growth Drivers

Rising defense modernization programs

Global military forces expanded investments in advanced satellite networks, secure communication links, and resilient surveillance systems. Defense agencies prioritized improved command and control structures to support real-time decision-making across land, air, sea, and space domains. Growing geopolitical tensions pushed countries to upgrade space-based capabilities for early warning, missile tracking, and threat assessment. This modernization wave strengthened demand for next-generation C4ISR architectures with higher bandwidth, better encryption, and stronger data processing efficiency across mission-critical operations.

- For instance, Airbus’ Skynet 6A military communications satellite is planned to deliver three-and-a-half times the capacity of the current Skynet 5 series and is scheduled for launch in 2026, with entry into service for the UK Ministry of Defence due in 2027.

Increasing demand for ISR enhancement

Space-based intelligence, surveillance, and reconnaissance gained traction as nations sought persistent coverage, superior imaging, and long-range monitoring. High-resolution sensors, infrared payloads, and radar systems allowed quicker detection of potential threats and improved situational awareness. Defense planners favored ISR tools that support perimeter security, maritime domain awareness, and border surveillance. Rising interest in low-Earth-orbit constellations further boosted imaging frequency and data reliability, driving sustained investment in ISR-focused C4ISR infrastructure.

- For instance, Maxar’s WorldView-3 satellite collects panchromatic imagery at 31 cm ground resolution and can image up to roughly 680,000 square kilometers per day, supporting high-detail surveillance and reconnaissance tasks.

Rapid adoption of AI and advanced analytics

AI-enabled data fusion and automated threat recognition strengthened operational outcomes across defense missions. Space-based systems generated large data volumes that required faster processing and intelligent filtering. Machine learning models supported object tracking, anomaly detection, and communication routing, reducing human workload. Governments accelerated AI integration to optimize mission planning and improve real-time responsiveness. The transition toward autonomous decision support systems boosted long-term demand for advanced computing within C4ISR platforms.

Key Trends and Opportunities

Expansion of LEO satellite constellations

Low-Earth-orbit constellations created strong opportunities for faster communication, wider coverage, and lower latency across military and commercial users. Nations invested in new clusters to support tactical communication, earth observation, and space domain awareness. The trend pushed suppliers to develop lighter, scalable payloads that work in distributed architectures. Strong focus on multi-orbit integration opened new growth avenues for companies offering flexible C4ISR systems that link LEO, MEO, and GEO networks.

- For instance, Eutelsat OneWeb’s first-generation LEO constellation is planned for 648 operational satellites (600 active plus 48 on-orbit spares), and the final deployment of the initial constellation was completed in March 2023.

Growth of commercial participation in space systems

Private companies entered the C4ISR landscape with advanced small satellites, imaging analytics, and communication services. Partnerships between defense agencies and commercial operators grew as governments sought cost-effective and rapid-deployment solutions. Commercial data providers offered improved imagery refresh rates, cloud-based processing, and tailored analytics for defense missions. This shift unlocked opportunities for dual-use technologies that support both strategic and civilian applications.

- For instance, Planet Labs operates a fleet of about 200 Earth-imaging satellites, enabling daily monitoring of the entire land surface and supplying imagery and analytics to security and government clients.

Advances in resilient and secure space architectures

Space-based systems faced rising threats from jamming, cyber intrusions, and anti-satellite technologies. In response, countries pursued hardened networks, encrypted links, and redundancy architectures to ensure uninterrupted mission support. Growth in protected communication satellites and space situational awareness tools created new demand for secure C4ISR frameworks. This trend enabled suppliers to innovate in anti-jam technologies, secure signal routing, and autonomous defensive capabilities.

Key Challenges

High deployment and maintenance costs

Building advanced satellites, sensors, and communication payloads required significant financial investment. Development, launch services, and orbital maintenance created budget constraints for smaller nations. Cost also increased with widening mission complexity, frequent upgrades, and the need for more resilient architectures. These financial hurdles limited broad adoption and slowed modernization efforts across several regions. The long lifecycle of space assets further complicated cost planning and sustainability.

Increasing space security threats

Growing risks from cyberattacks, jamming, spoofing, and anti-satellite weapons created major concerns for C4ISR operators. Nations had to invest in defensive capabilities to protect networks from physical and electronic threats. Rising congestion in orbit added collision hazards and tracking challenges. These factors raised vulnerability across mission platforms and demanded stronger situational awareness tools. Ensuring system reliability under hostile conditions remained a central challenge for global defense agencies.

Regional Analysis

North America

North America led the Space Based C4ISR Market in 2024 with about 41% share. Strong defense budgets and continuous modernization programs drove demand for advanced satellite communication, ISR platforms, and secure command networks. The region expanded low-earth-orbit deployments and strengthened missile warning capabilities. Growth also came from rising collaboration between government agencies and commercial space companies that accelerated innovation in imaging, analytics, and data processing. Increasing geopolitical concerns and investment in space domain awareness reinforced North America’s leadership position.

Europe

Europe accounted for nearly 26% share in 2024, supported by rising defense cooperation and sovereign space programs. Countries enhanced satellite-based surveillance, environmental monitoring, and secure communication systems to improve regional security readiness. Growing participation in multilateral projects and investments in next-generation payloads increased capability development. The market gained further momentum from expanding commercial imaging and analytics providers. Modernization of navigation, early warning, and border protection networks boosted Europe’s adoption of C4ISR architectures.

Asia Pacific

Asia Pacific held about 22% share in 2024 and recorded fast expansion driven by rising defense budgets and territorial security concerns. Nations invested heavily in ISR satellites, communication networks, and space-based threat detection to strengthen strategic preparedness. Growth in regional launch capabilities and indigenous space programs improved access to affordable satellite platforms. Increasing commercial involvement supported broader availability of advanced payloads and data analytics. Rapid modernization across military structures positioned Asia Pacific as a high-growth region.

Latin America

Latin America captured around 6% share in 2024, supported by expanding interest in satellite communication, disaster monitoring, and border surveillance. Governments adopted space-based tools to enhance national security and environmental tracking. Budget limitations slowed large-scale deployment, yet partnerships with international agencies enabled access to imaging and communication services. Growing demand for maritime surveillance and resource protection further supported adoption. Emerging commercial ventures in small satellites improved cost-effective entry into C4ISR applications.

Middle East and Africa

Middle East and Africa held nearly 5% share in 2024, driven by rising security needs and investments in surveillance and communication systems. Several countries focused on space-enabled monitoring for border protection, critical infrastructure security, and regional threat detection. Adoption increased through collaborations with global space agencies providing ISR data and satellite services. Defense modernization programs in select Gulf nations further boosted demand. Limited domestic manufacturing and high procurement costs kept adoption moderate across developing economies.

Market Segmentations:

By Type

- Command and Control (C2)

- Communications

- Computers and data processing

- ISR

By Platform Type

- Satellite

- Unmanned spacecraft

- Space-based sensors and payloads

By End Use

- Defense and military organizations

- Homeland security

- Civil and government

- Commercial applications

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Space Based C4ISR Market is shaped by leading companies such as Lockheed Martin Corporation, Maxar Technologies Ltd, CACI International Inc., Elbit Systems Ltd, General Dynamics Corporation, Kratos Defense & Security Solutions Inc., Northrop Grumman Corporation, BAE Systems PLC, and The Boeing Company. The competitive environment reflects strong focus on advanced satellite platforms, secure communication systems, and high-resolution ISR payloads that support defense modernization across major regions. Market participants continue to invest in AI-driven analytics, resilient network architectures, and multi-orbit integration to enhance mission readiness. Partnerships with government agencies and commercial space operators strengthen technology development and speed deployment cycles. Rising demand for low-Earth-orbit constellations, encrypted links, and space domain awareness systems further intensifies competition. Companies emphasize innovation in payload miniaturization, data fusion, and multi-mission flexibility to expand their global footprint in the evolving space defense ecosystem.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Lockheed Martin Corporation

- Maxar Technologies Ltd

- CACI International Inc.

- Elbit Systems Ltd

- General Dynamics Corporation

- Kratos Defense & Security Solutions Inc.

- Northrop Grumman Corporation

- BAE Systems PLC

- The Boeing Company

Recent Developments

- In 2025, Elbit Systems unveiled a new AI-based wide-area persistent surveillance system called Frontier at the DSEI exhibition in London.

- In 2025, Maxar won $205 million in strategic contracts across the Middle East and Africa to provide direct satellite imagery tasking, 3D terrain data, and AI-powered change detection for C5ISR systems, enabling persistent surveillance and multi-domain operations.

- In 2022, General Dynamics Mission Systems secured a seven-year contract with Iridium for the Space Development Agency’s Tranche 1 satellite ground segment, sustaining C4ISR infrastructure

Report Coverage

The research report offers an in-depth analysis based on Type, Platform Type, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Rising demand for advanced satellite networks will strengthen global C4ISR capabilities.

- Defense agencies will expand investments in resilient communication and surveillance systems.

- Low-Earth-orbit constellations will support faster data flows and wider mission coverage.

- AI-driven analytics will enhance real-time threat detection and decision-making speed.

- Growth in commercial space activity will boost dual-use C4ISR applications.

- Autonomous spacecraft and payloads will improve inspection and maintenance efficiency.

- Secure architectures will evolve to counter jamming, cyber risks, and anti-satellite threats.

- Miniaturized payloads will enable more frequent and affordable satellite launches.

- Multinational defense collaborations will accelerate shared space intelligence programs.

- Space domain awareness systems will expand to track rising orbital congestion.