Market overview

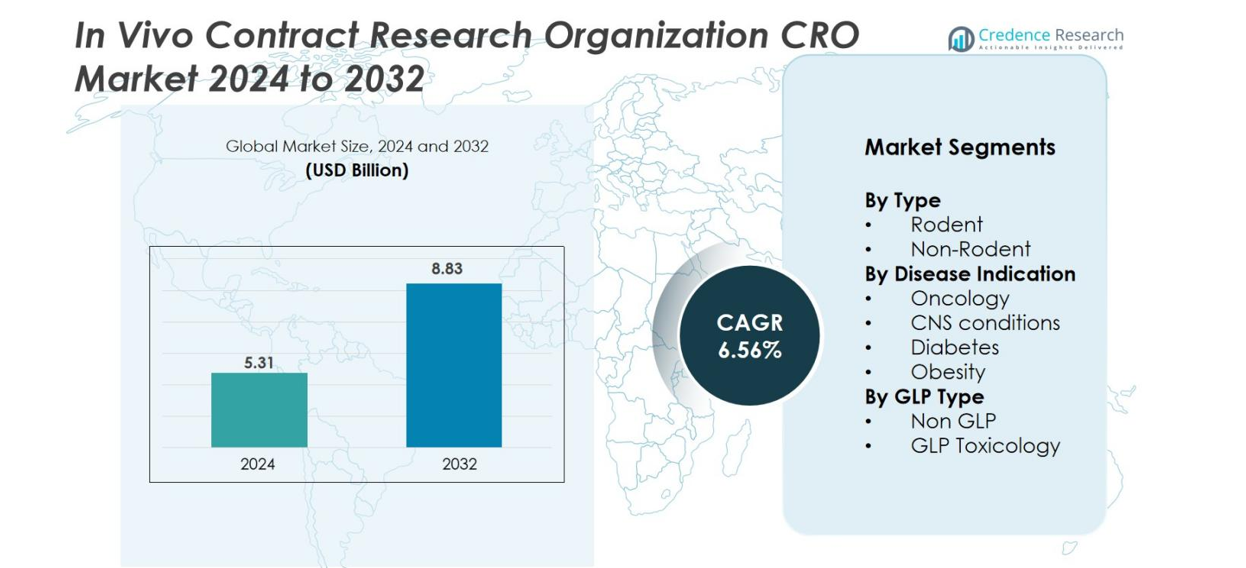

The In Vivo Contract Research Organization (CRO) market size was valued at USD 5.31 Billion in 2024 and is anticipated to reach USD 8.83 Billion by 2032, at a CAGR of 6.56% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| In Vivo Contract Research Organization (CRO) Market Size 2024 |

USD 5.31 Billion |

| In Vivo Contract Research Organization (CRO) Market, CAGR |

6.56% |

| In Vivo Contract Research Organization (CRO) Market Size 2032 |

USD 8.83 Billion |

In Vivo Contract Research Organization (CRO) Market features a competitive landscape led by globally established players with advanced preclinical capabilities. Key companies including Charles River Laboratories, IQVIA, ICON plc, Labcorp, Evotec, Crown Bioscience, Taconic Biosciences, GemPharmatech, Biocytogen, PsychoGenics, and Janvier Labs strengthen their positions through diversified in vivo models, GLP-compliant toxicology, and therapeutic-area specialization. North America remains the leading region with 40% market share, supported by strong pharmaceutical R&D activity and extensive CRO infrastructure, followed by Europe with 28% and Asia Pacific with 22%, reflecting rapid expansion in biomedical research and cost-efficient outsourcing capacity.

Market Insights

- The In Vivo Contract Research Organization (CRO) market was valued at USD 5.31 billion in 2024 and is projected to reach USD 8.83 billion by 2032, registering a CAGR of 6.56% during the forecast period.

- Market growth is driven by rising preclinical R&D spending, expanding oncology pipelines, and increasing outsourcing of complex in vivo studies to reduce costs and accelerate development timelines.

- Key trends include rapid adoption of advanced animal models such as humanized mice and PDX systems, along with growing integration of digital tools, imaging technologies, and AI-driven analytics to enhance study precision.

- The competitive landscape features major players such as Charles River Laboratories, IQVIA, ICON plc, Labcorp, Evotec, Crown Bioscience, Taconic Biosciences, and GemPharmatech, supported by expanding service portfolios and global research networks.

- Regionally, North America leads with 40% share, followed by Europe at 28% and Asia Pacific at 22%, while the rodent segment dominates by type with nearly 65% share due to broad applicability in early-stage research.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis

By Type

The rodent segment dominates the In Vivo CRO market, accounting for an estimated 65% share due to its widespread use in early-stage efficacy, toxicology, and pharmacokinetic studies. Rodents remain the preferred model because they are cost-effective, genetically well-characterized, and suitable for a broad range of therapeutic investigations. Non-rodent models, while essential for advanced regulatory toxicology, represent a smaller portion of the market owing to higher costs and stricter handling requirements. Growth in rodent-based research is reinforced by rising preclinical pipelines and the increasing adoption of humanized and genetically engineered mouse models.

- For instance, Biocytogen has developed over 4,390 genetically engineered mouse and rat models (including humanized and immunodeficient varieties) to accelerate drug development.

By Disease Indication

Oncology is the leading disease indication, contributing roughly 45% of market share, driven by escalating global cancer prevalence and the surge in immuno-oncology drug development. Tumor xenograft, syngeneic, and PDX models remain central to evaluating therapeutic responses and biomarker discovery. CNS conditions form the second-largest segment, supported by demand for neurodegenerative disorder treatments. Meanwhile, diabetes and obesity studies continue to expand with the growing metabolic disease burden. The dominance of oncology is further reinforced by pharmaceutical investments in targeted therapies and the need for robust in vivo efficacy validation.

- For instance, the Jackson Laboratory (JAX) maintains an extensive, validated collection of hundreds of patient-derived xenograft (PDX) models, including over 350 available for preclinical efficacy studies, which enables preclinical screening of targeted and immunotherapeutic agents.

By GLP Type

The non-GLP segment leads the market with an estimated 55% share, as early-stage efficacy screening and exploratory toxicology typically precede formal regulatory studies. Non-GLP workflows offer faster turnaround times, lower costs, and greater flexibility, which appeal to biotechs optimizing preclinical candidates. Conversely, the GLP toxicology segment continues to grow steadily, supported by rising IND submissions and increased regulatory oversight. Demand for GLP-compliant studies is further driven by the expansion of biologics and cell-based therapies requiring rigorous safety evaluations. Together, both segments form a complementary workflow within the CRO ecosystem.

Key Growth Drivers

Rising Preclinical R&D Investments

Increasing preclinical R&D spending and expanding drug pipelines significantly drive the in vivo CRO market. Pharmaceutical and biotech companies outsource early-stage studies to accelerate candidate validation and reduce fixed operational costs. The growth of oncology, CNS, and metabolic disease pipelines increases demand for specialized in vivo expertise. Rising IND submissions and the pressure to shorten development timelines further encourage reliance on CROs with advanced facilities, enabling sponsors to improve efficiency and focus internal resources on core innovation.

- For instance, WuXi AppTec reports collaboration with nearly 6,000 global pharmaceutical and biotech clients across more than 30 countries, supporting a large volume of early-stage discovery and preclinical in vivo projects.

Advancements in Animal Models

Rapid advancements in animal models including humanized mice, PDX systems, and CRISPR-engineered organisms fuel strong market growth. These models enhance translational accuracy and support complex disease research, especially in oncology and immunology. CROs integrating next-generation sequencing, imaging tools, and biomarker analytics deliver higher-quality data and reduce clinical attrition. As drug modalities expand into biologics, cell therapy, and gene therapy, sponsors increasingly depend on CROs offering sophisticated in vivo platforms that improve prediction of therapeutic performance.

- For instance, Taconic Biosciences reports having a library of over 20,600 genetically engineered models (GEMs) including transgenic, knockout, and humanized mouse and rat strains.

Increasing Regulatory Demand for Toxicology Studies

Stricter global regulatory requirements for safety assessment accelerate demand for CRO-based GLP toxicology studies. These studies require specialized facilities, validated workflows, and experienced technicians that many biopharma companies lack internally. Outsourcing ensures regulatory alignment, reliable documentation, and efficient study initiation. Rising submissions for biologics and advanced therapies heighten the need for comprehensive toxicology packages. CROs offering integrated safety pharmacology, toxicology, and regulatory support are well positioned to capture increasing outsourcing demand across early development pipelines.

Key Trends & Opportunities

Adoption of Digital and AI-Driven Technologies

The integration of AI, automation, and digital monitoring represents a major trend creating new opportunities for in vivo CROs. AI-based analytics improve study design, accelerate data interpretation, and enhance reproducibility. Automated monitoring systems reduce human error and refine behavioral assessment. Digital pathology and imaging platforms support deeper biomarker analysis. Sponsors increasingly favor CROs using advanced digital tools to improve transparency and efficiency. This shift enables CROs to deliver richer datasets, differentiate services, and secure long-term strategic partnerships.

- For instance, Explicyte’s digital pathology workflow for immuno-oncology uses two automated Ventana Discovery XT systems and can handle up to 200 samples per week, including Tissue MicroArrays, with automated staining protocols.

Growing Demand for Specialized Therapeutic Expertise

Rising demand for therapeutic-area specialization—especially in immuno-oncology, rare diseases, and neurological disorders—creates strong opportunities for CROs. Sponsors seek partners with deep model expertise, advanced imaging capabilities, and disease-specific biomarker knowledge. Growth in cell and gene therapy pipelines increases the need for complex in vivo studies, including biodistribution and long-term toxicity assessments. Niche CROs offering targeted expertise gain competitive advantage. As precision medicine expands, CROs providing tailored in vivo strategies aligned with disease mechanisms benefit from sustained outsourcing demand.

- For instance, Champions Oncology maintains a molecularly characterised tumour model bank comprising over 1,400 solid tumour and haematological in-vivo models, supporting advanced immuno-oncology and cell therapy research.

Key Challenges

Ethical and Regulatory Pressures on Animal Use

Tightening ethical regulations and rising scrutiny of animal research pose challenges for in vivo CROs. Compliance with welfare standards requires significant investment in facility improvements, documentation, and staff training. Global differences in animal research guidelines also complicate harmonized study execution. CROs must integrate refined practices and explore alternative methods such as organ-on-chip or in vitro systems. While essential for responsible research, these requirements increase operational complexity, extend project timelines, and raise costs across preclinical programs.

High Costs and Limited Availability of Specialized Models

The high cost of in vivo studies, especially those involving primates or humanized models, remains a significant challenge. Specialized models require advanced infrastructure, skilled personnel, and controlled environments, limiting global capacity. Demand for non-human primate toxicology exceeds supply, creating long wait times and bottlenecks. Smaller biotechs face financial barriers to accessing premium in vivo capabilities. CROs struggle to scale operations without compromising quality, leading to capacity constraints that can delay early-stage development timelines and outsourcing decisions.

Regional Analysis

North America

North America holds the largest share of the in vivo CRO market, accounting for 40% of global revenue. The region benefits from a strong pharmaceutical ecosystem, high R&D expenditure, and well-established GLP-compliant CRO infrastructure. The presence of major industry players, extensive use of advanced animal models, and increasing demand for specialized toxicology services further strengthen market leadership. Favorable regulatory frameworks and continuous investment in drug discovery accelerate outsourcing activities. The rapid expansion of oncology and immunotherapy pipelines also reinforces the region’s dominance, creating sustained demand for high-quality in vivo research services.

Europe

Europe represents 28% of the in vivo CRO market, supported by a robust biotechnology sector, strong academic-industry collaboration, and comprehensive regulatory standards. Countries such as Germany, France, and the U.K. remain key contributors due to their advanced research facilities and growing investment in translational science. Increased focus on rare diseases, cell therapy, and personalized medicine is accelerating demand for specialized in vivo expertise. Despite strict ethical regulations governing animal research, the region continues expanding its outsourcing footprint through high-quality GLP toxicology capabilities. Rising pharmaceutical innovation and supportive government funding contribute to steady market growth.

Asia Pacific

Asia Pacific holds 22% market share and is the fastest-growing regional segment, driven by expanding biomedical research, cost-efficient outsourcing, and growing adoption of advanced animal models. China, India, South Korea, and Japan lead regional activity with significant investments in preclinical infrastructure and rising domestic drug development. Globally competitive CROs, supportive government policies, and increasing clinical trial activity further strengthen regional growth. The region’s cost advantages and rapid project turnaround attract Western pharmaceutical companies seeking scalable preclinical solutions. Expansion of oncology, metabolic disease, and gene therapy research continues to boost demand for in vivo CRO services.

Latin America

Latin America accounts for 6% of the in vivo CRO market, supported by growing pharmaceutical investments and improving research capabilities in countries such as Brazil, Mexico, and Argentina. The region offers competitive operational costs and an expanding base of preclinical facilities, enabling increasing outsourcing from global and regional drug developers. Advancements in toxicology, infectious disease models, and regulatory alignment with international standards are enhancing market credibility. Although infrastructure gaps and limited high-complexity capabilities remain challenges, continued investment in biomedical research is expected to enhance regional participation in global in vivo CRO activities.

Middle East & Africa

The Middle East and Africa region holds 4% of the market, reflecting early-stage but steadily expanding adoption of outsourced preclinical research. Growth is supported by increasing investments in healthcare innovation, rising interest in biotechnology, and efforts to develop GLP-compliant research infrastructure in countries such as the UAE, Saudi Arabia, and South Africa. The region’s demand for in vivo studies is driven by rising prevalence of chronic diseases and expanding pharmaceutical manufacturing. However, limited local expertise and infrastructure constraints restrict large-scale operations. Ongoing government initiatives and research partnerships are expected to gradually strengthen market presence.

Market Segmentations

By Type

By Disease Indication

- Oncology

- CNS conditions

- Diabetes

- Obesity

By GLP Type

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the In Vivo CRO market is characterized by a mix of global leaders, specialized regional providers, and emerging niche players focused on complex disease modelling and advanced toxicology services. Major companies such as Charles River Laboratories, IQVIA, ICON plc, Labcorp, Envigo, Taconic Biosciences, Crown Bioscience, Evotec, GemPharmatech, and Biocytogen maintain strong market positions through extensive research infrastructure, diversified service portfolios, and long-standing partnerships with pharmaceutical and biotechnology firms. These players invest heavily in expanding humanized models, PDX platforms, CRISPR-engineered systems, and digital data capabilities to enhance study quality and reduce development timelines. The market also includes specialized providers like PsychoGenics, Janvier Labs, and Caidya, which focus on CNS, oncology, and metabolic disease models. Competition intensifies as CROs pursue strategic acquisitions, geographic expansion, and technological integration to meet rising demand for complex in vivo studies, GLP-compliant toxicology, and integrated preclinical solutions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Evotec

- Taconic Biosciences, Inc.

- GemPharmatech

- Icon Plc

- Biocytogen Boston Corp

- Crown Bioscience

- Janvier Labs

- PsychoGenics Inc.

- IQVIA Inc.

- Charles River Laboratories

Recent Developments

- In July 2025, InnoSer, Connected-Pathology, and Poulpharm formed a strategic partnership aimed at expanding preclinical and histopathology services across multi-species in-vivo models.

- In March 2024, Agathos Biologics, a North Dakota–based company in Fargo, launched its recombinant adeno-associated virus (rAAV) production service utilizing its proprietary AE1-BHK cell line, and recorded its first rAAV sale to CRO Genovac and a contract manufacturing organization.

- In November 2023, Crown Bioscience, a JSR Life Sciences company, introduced OrganoidXplore™, a high-speed and clinically relevant organoid panel-screening platform designed to accelerate preclinical oncology drug discovery.

Report Coverage

The research report offers an in-depth analysis based on Type, Disease Indication, GLP Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will continue expanding as pharmaceutical and biotech companies increase outsourcing of preclinical in vivo studies to accelerate development timelines.

- Demand for advanced animal models, including humanized and CRISPR-engineered systems, will grow rapidly to improve translational accuracy.

- Integration of AI, automation, and digital monitoring will enhance data quality and streamline study workflows across CROs.

- Oncology, CNS disorders, and metabolic diseases will remain dominant research areas driving sustained in vivo model utilization.

- GLP toxicology services will see rising demand as regulatory requirements for complex biologics and gene therapies intensify.

- Asia Pacific will strengthen its position as a high-growth region due to expanding biomedical infrastructure and competitive outsourcing costs.

- Strategic collaborations between CROs, pharma companies, and academic institutions will increase to support advanced model development.

- Consolidation through mergers and acquisitions will intensify as global CROs seek expanded capabilities and geographic reach.

- Ethical and regulatory pressures will drive investment in refined practices and validated alternative methods.

- CROs offering specialized therapeutic expertise and integrated preclinical solutions will gain a competitive advantage in long-term partnerships.