Market Overview

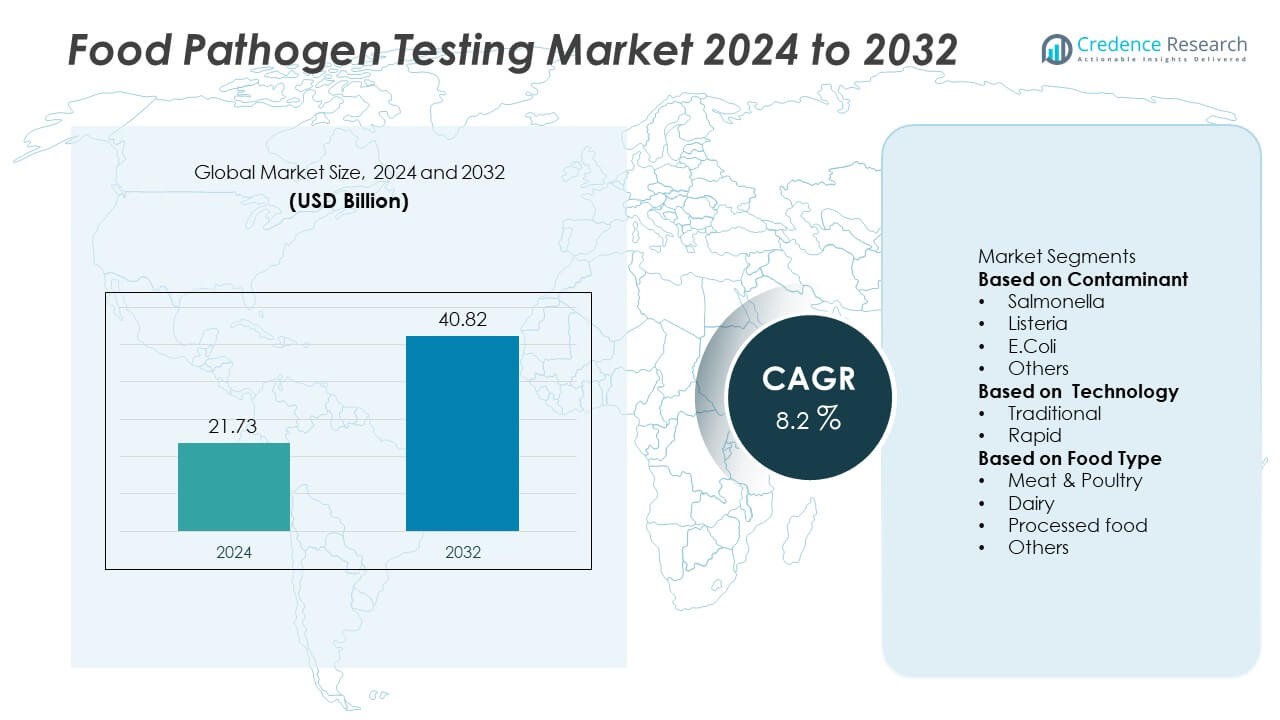

The Food Pathogen Testing Market was valued at USD 21.73 billion in 2024 and is projected to reach USD 40.82 billion by 2032, growing at a CAGR of 8.2% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Food Pathogen Testing Market Size 2024 |

USD 21.73 Billion |

| Food Pathogen Testing Market, CAGR |

8.2% |

| Food Pathogen Testing Market Size 2032 |

USD 40.82 Billion |

Top players in the Food Pathogen Testing market include Eurofins Scientific, ALS Limited, Genetic ID NA Inc., SGS S.A., Bureau Veritas S.A., Microbac Laboratories, Inc., Intertek Group PLC, AsureQuality, BIOMERIEUX SA, and IFP Institut für Produktqualität GmbH. These companies compete through global lab networks, rapid PCR platforms, and advanced molecular diagnostics. They focus on high-throughput testing, digital reporting, and strong regulatory compliance support for food producers. Regionally, North America leads the market with a 37% share, followed by Europe with 29% and Asia Pacific with 25%. Latin America holds 8%, while the Middle East and Africa together account for 6%, reflecting growing but still developing testing capacity.

Market Insights

- The Food Pathogen Testing market reached USD 21.73 billion in 2024 and is projected to hit USD 40.82 billion by 2032, registering a CAGR of 8.2%, driven by rising global emphasis on food safety.

- Strong market drivers include increasing foodborne illness cases, stricter regulatory standards, and higher testing frequency across meat and poultry, the leading food type segment with a 38% share, supported by high contamination risks.

- Key trends include rapid adoption of PCR and DNA-based technologies, which lead the technology segment with a 61% share, along with growing automation, digital reporting, and integrated lab workflows.

- Competitive activity remains intense, with major players expanding lab networks, investing in rapid detection platforms, and strengthening partnerships with global food processors, while high testing costs continue to restrain adoption among small producers.

- Regionally, North America leads with a 37% share, followed by Europe at 29%, Asia Pacific at 25%, Latin America at 8%, and the Middle East & Africa at 6%, reflecting diverse testing maturity levels across global markets.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Contaminant

Salmonella leads the contaminant segment with a 34% share, driven by frequent outbreaks in poultry, eggs, and processed meat. Food processors increase screening because Salmonella spreads fast across supply chains. Listeria holds steady demand due to strict rules for ready-to-eat food, while E. coli testing grows across beef and fresh produce plants. Rising global food recalls push companies to adopt wider contaminant panels. Government audits also raise testing volumes in export-focused facilities. The need for early detection supports strong uptake of multiplex assays that identify multiple pathogens in one run, improving speed and reliability for quality teams.

- For instance, bioMérieux expanded its VIDAS pathogen testing line with an assay capable of detecting Salmonella with a time-to-result of 19 hours, validated on a wide variety of food products and environmental samples, including standard and large-size samples.

By Technology

Rapid testing dominates the technology segment with a 61% share, supported by strong demand for quick results and higher testing throughput. Food producers adopt PCR, immunoassay, and DNA-based platforms to shorten decision cycles and release batches faster. Traditional culture methods remain relevant for confirmatory processes, but slower turnaround reduces broader use. The need to detect low-level contamination in large batches strengthens adoption of rapid tools. Rising automation in sample prep and workflow integration improves accuracy in high-volume labs. Companies focus on meeting strict safety rules, which further boosts investment in rapid pathogen screening systems.

- For instance, Thermo Fisher Scientific advanced rapid pathogen workflows by introducing the Thermo Scientific SureTect PCR System, which delivers results for foodborne pathogens in as little as eight hours.

By Food Type

Meat and poultry hold the dominant position in the food type segment with a 38% share, driven by high contamination risks linked to Salmonella and Campylobacter. Producers increase testing at slaughterhouses and processing lines to prevent product recalls. Dairy products show steady demand because Listeria control remains a priority for cheese and milk plants. Processed food testing rises as global brands expand ready-to-eat lines. The shift toward packaged and frozen meals increases the need for routine microbiological checks. Growing exports also push facilities to adopt strict testing rules, supporting stronger uptake of advanced pathogen detection methods.

Key Growth Drivers

Rising Incidence of Foodborne Illnesses

Growing cases of foodborne diseases strengthen the demand for routine pathogen testing across global supply chains. Food processors increase testing frequency to reduce contamination linked to Salmonella, Listeria, and E. coli. Governments enforce tougher compliance rules, pushing companies to upgrade detection capabilities. Expanding international trade also raises the need for strict testing to meet export standards. Companies invest in automated labs and high-throughput platforms to avoid costly recalls. The resulting focus on preventive safety strengthens long-term growth for advanced pathogen testing technologies.

- For instance, Eurofins strengthened outbreak prevention by operating more than 900 analytical laboratories worldwide, performing over 450 million tests annually, including extensive Salmonella and Listeria panels.

Strict Regulatory Frameworks and Compliance Requirements

Regulatory bodies enforce stronger rules for microbial testing, driving adoption across meat, dairy, and processed food categories. Standards such as HACCP and ISO-based protocols require continuous monitoring of pathogens at multiple production stages. Food processors respond by expanding in-house labs and outsourcing specialized testing. Frequent audits and zero-tolerance policies increase spending on validated detection systems. The push for traceable supply chains further increases testing volumes. This regulatory tightening underpins steady growth as companies prioritize compliance to maintain product safety and market access.

- For instance, Intertek strengthened HACCP-aligned monitoring by operating over 1,000 laboratories that perform microbial testing across 100 countries, ensuring traceability for exporters.

Shift Toward Rapid and High-Accuracy Testing Technologies

Industry adoption of rapid testing technologies accelerates as producers seek faster batch release and high accuracy. PCR, DNA sequencing, and immunoassay platforms support same-day results, reducing downtime and operational losses. Automation improves consistency in high-volume environments, allowing real-time monitoring of contamination risks. Food companies also use advanced tools to detect low pathogen loads in complex samples. Growing pressure to prevent cross-contamination supports investment in high-sensitivity detection methods. This technology shift boosts efficiency and strengthens market demand for next-generation systems.

Key Trends & Opportunities

Growing Use of Automation and Digital Solutions

Automation emerges as a major trend as food companies adopt robotic sample handling, AI-driven analytics, and cloud-based reporting. These tools improve consistency, reduce manual errors, and support faster data interpretation. Digital dashboards help quality teams track contamination patterns across facilities. Remote monitoring expands opportunities for centralized decision-making. Adoption of smart labs also raises throughput and lowers operational costs. As digital transformation accelerates in the food industry, advanced automated testing solutions create strong long-term growth opportunities.

- For instance, Bruker supported digital integration by deploying thousands of MALDI Biotyper units worldwide, each capable of identifying hundreds of clinically relevant species (most recently expanded to 549 validated species in the U.S.) or over 4,300 species in the full research-use-only library.

Expansion of Ready-to-Eat and Packaged Food Categories

Rising demand for ready-to-eat meals and packaged food boosts testing requirements across global processing plants. These products carry high contamination risks because they bypass cooking after packaging. Companies expand pathogen screening to protect product safety and brand reputation. Growth in frozen meals, snacks, bakery items, and convenience foods increases batch-level testing. Export-oriented manufacturers face stricter regulations, further lifting testing volumes. This segment expansion creates strong opportunities for advanced pathogen detection technologies with higher speed and sensitivity.

- For instance, Neogen’s ANSR® molecular detection system and Reveal® 2.0 lateral flow tests for Listeria and Salmonella are validated to detect the target organisms at levels as low as 1 CFU (colony-forming unit) per analytical unit (which commonly uses a 25 g sample after an enrichment step).

Key Challenges

High Testing Costs and Limited Access for Small Producers

Advanced pathogen testing technologies require significant investment, making adoption difficult for small and mid-size producers. High costs for PCR systems, consumables, and lab infrastructure restrict broader use. Smaller firms rely on third-party labs, causing slower turnaround times and higher per-sample expenses. Limited budgets delay the shift to rapid, automated methods. These cost barriers create gaps in testing frequency and increase contamination risks. Addressing affordability remains essential for expanding market penetration across developing regions.

Complexity of Detecting Emerging and Low-Level Contaminants

Detecting low-level pathogens and emerging strains remains a technical challenge for many testing platforms. Complex matrices in foods like dairy, meat, and processed products can interfere with detection accuracy. Pathogen evolution also demands continuous updates to testing protocols. False negatives risk product recalls and safety issues. Labs require skilled personnel to manage advanced molecular tools, adding to operational difficulty. These detection challenges slow adoption for some applications and drive continued investment in more sensitive, reliable testing technologies.

Regional Analysis

North America

North America leads the Food Pathogen Testing market with a 37% share, driven by strict regulatory standards, advanced lab infrastructure, and strong adoption of rapid testing technologies. The U.S. enforces rigorous compliance programs such as FSMA, which increases testing across meat, poultry, dairy, and processed foods. Frequent product recalls push producers to expand routine microbial screening. High investments in automated PCR and DNA-based platforms strengthen regional leadership. Canada also increases testing volumes as food exports grow. Strong industry-regulatory collaboration continues to support innovation and maintain North America’s position as the largest testing hub.

Europe

Europe holds a 29% share supported by structured food safety regulations, strong traceability programs, and widespread adoption of standardized testing protocols. Authorities enforce strict pathogen control across ready-to-eat foods, dairy plants, and meat processing units. Countries such as Germany, the U.K., and France maintain high testing frequency due to Listeria and Salmonella risks. Advanced laboratories and EU-wide compliance frameworks encourage rapid adoption of molecular diagnostic tools. Growing demand for premium and organic products increases the need for contamination monitoring. Europe’s established regulatory environment continues to drive steady growth in advanced pathogen testing.

Asia Pacific

Asia Pacific accounts for a 25% share, driven by rapid expansion of the food processing industry and rising consumer awareness of food safety. China and India increase testing adoption due to frequent contamination events and growing export requirements. Large-scale production of poultry, seafood, and packaged foods boosts testing volumes across regional facilities. Governments strengthen safety rules, encouraging investment in modern labs and rapid detection systems. Rising urbanization and demand for packaged meals further expand market needs. Improvements in infrastructure and regulatory enforcement make Asia Pacific a fast-growing region for pathogen testing solutions.

Latin America

Latin America holds an 8% share, supported by growing food exports and rising compliance requirements across meat, poultry, and fresh produce sectors. Brazil, Mexico, and Argentina expand pathogen testing to meet international trade standards. Increasing global demand for regional meat and fruit exports drives investment in modern microbial detection systems. However, limited lab infrastructure and uneven regulatory enforcement slow widespread adoption. Food processors gradually shift from traditional methods to rapid technologies to reduce contamination risks. Strengthening regional guidelines is expected to support further market expansion.

Middle East & Africa

The Middle East & Africa region accounts for a 6% share, driven by the growing import of packaged and processed foods and rising awareness of foodborne illnesses. GCC countries strengthen regulatory oversight to improve food safety in retail and hospitality sectors. Expanding manufacturing activity in the UAE and Saudi Arabia increases demand for pathogen screening. Africa’s adoption grows slowly due to limited lab facilities, but international aid programs support capability development. Rising urban populations and expanding cold-chain logistics boost testing needs. Investments in modern diagnostic tools are expected to improve regional market penetration.

Market Segmentations:

By Contaminant

- Salmonella

- Listeria

- E.Coli

- Others

By Technology

By Food Type

- Meat & Poultry

- Dairy

- Processed food

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape is shaped by major players such as Eurofins Scientific, ALS Limited, Genetic ID NA Inc., SGS S.A., Bureau Veritas S.A., Microbac Laboratories, Inc., Intertek Group PLC, AsureQuality, BIOMERIEUX SA, and IFP Institut für Produktqualität GmbH. Companies compete through extensive lab networks, advanced molecular testing capabilities, and strong global presence. Leading firms invest in high-throughput PCR systems, automated sample preparation, and next-generation sequencing to improve accuracy and turnaround time. Partnerships with food manufacturers and regulatory bodies strengthen service reliability and expand testing coverage across supply chains. Many players focus on real-time reporting platforms and digital workflow tools to support faster decision-making. Expansion strategies include acquisitions, accreditation upgrades, and portfolio diversification into allergen testing, GMO analysis, and environmental monitoring. Rising demand for rapid and validated detection methods encourages continuous innovation, helping major laboratories maintain market leadership in the evolving food safety ecosystem.

Key Player Analysis

- Eurofins Scientific

- ALS Limited

- Genetic ID NA Inc.

- SGS S.A.

- Bureau Veritas S.A.

- Microbac Laboratories, Inc.

- Intertek Group PLC

- AsureQuality

- BIOMERIEUX SA

- IFP Institut für Produktqualität GmbH

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In October 2024, SGS S.A. expanded its food and nutraceutical testing capacity in North America by relocating to a larger facility in Fairfield, New Jersey.

- In June 2024, AsureQuality started a redevelopment project at its Auckland food laboratory designed to increase capacity and boost its food pathogen testing capability.

- In November 2023, SGS S.A. announced the availability of PCR-based pathogen testing for the food industry in Mexico and other regions.

Report Coverage

The research report offers an in-depth analysis based on Contaminant, Technology, Food Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand as food processors increase routine testing across global supply chains.

- Adoption of rapid PCR and sequencing tools will grow to support faster batch release.

- Automation in sample handling and data reporting will strengthen testing accuracy and speed.

- Digital platforms will enable real-time monitoring of contamination trends across facilities.

- Rising demand for ready-to-eat and packaged food will drive higher testing frequency.

- Regulations will tighten further, increasing mandatory testing standards for exporters.

- Emerging pathogens and evolving strains will push companies to upgrade detection technologies.

- Cloud-based lab systems will support centralized decision-making for large food producers.

- Expanding cold-chain logistics in developing regions will increase the need for reliable testing.

- Investments in affordable rapid tests will improve market access for small and mid-size producers.