| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| South Korea Diabetes Drugs Market Size 2023 |

USD 3,344.06 Million |

| South Korea Diabetes Drugs Market, CAGR |

3.75% |

| South Korea Diabetes Drugs Market Size 2032 |

USD 4,823.91 Million |

Market Overview

South Korea Diabetes Drugs Market size was valued at USD 3,344.06 million in 2023 and is anticipated to reach USD 4,823.91 million by 2032, at a CAGR of 3.75% during the forecast period (2023-2032).

The South Korea diabetes drugs market is driven by the rising prevalence of diabetes, particularly Type 2 diabetes, due to lifestyle changes and an aging population. Advances in pharmaceutical innovations, including GLP-1 receptor agonists and SGLT2 inhibitors, are enhancing treatment efficacy and patient outcomes. Government initiatives, such as improved healthcare infrastructure and reimbursement policies, are increasing patient access to diabetes medications. The market is also witnessing a shift towards personalized medicine and digital health solutions, such as smart insulin delivery systems and AI-driven diabetes management tools. Additionally, the growing preference for combination therapies is improving treatment adherence and effectiveness. Pharmaceutical companies are focusing on research and development to introduce novel drug formulations with fewer side effects. Despite pricing challenges and regulatory hurdles, increasing awareness and early diagnosis efforts are expected to sustain market growth. The overall trend indicates steady expansion, driven by technological advancements and a strong demand for effective diabetes management solutions.

The South Korea diabetes drugs market is geographically diverse, with major urban centers such as Seoul, Busan, Daegu, and Gyeonggi Province serving as key hubs for diabetes treatment and pharmaceutical advancements. These regions benefit from well-established healthcare infrastructure, a high concentration of medical research institutions, and strong government support for chronic disease management. The presence of top-tier hospitals and access to advanced diabetes medications further drive market growth. Leading pharmaceutical companies operating in this space include Novo Nordisk, Sanofi, Merck & Co., Eli Lilly, AstraZeneca, Takeda, Boehringer Ingelheim, and Novartis, among others. Domestic players such as Handok are also expanding their footprint by developing biosimilars and innovative therapies tailored to local patient needs. With increasing investments in research, digital health integration, and a growing focus on personalized medicine, these key players are expected to further shape the competitive landscape of South Korea’s diabetes drugs market in the coming years.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The South Korea diabetes drugs market was valued at USD 3,344.06 million in 2023 and is projected to reach USD 4,823.91 million by 2032, growing at a CAGR of 3.75%.

- The rising prevalence of Type 2 diabetes, driven by aging demographics and lifestyle changes, is a key market driver.

- Growing adoption of novel drug classes such as GLP-1 receptor agonists and SGLT2 inhibitors is transforming diabetes treatment.

- Pharmaceutical giants like Novo Nordisk, Sanofi, Merck & Co., Eli Lilly, and AstraZeneca dominate the competitive landscape, alongside domestic players like Handok.

- High costs of advanced diabetes treatments and stringent regulatory requirements pose market restraints.

- Major urban centers like Seoul, Busan, Daegu, and Gyeonggi Province lead in diabetes drug adoption due to advanced healthcare infrastructure.

- Increasing investments in digital health solutions, such as AI-driven diabetes management and smart insulin delivery, are shaping future market trends.

Report Scope

This report segments the South Korea Diabetes Drugs Market as follows:

Market Drivers

Rising Diabetes Prevalence and Aging Population

The increasing prevalence of diabetes, particularly Type 2 diabetes, is a significant driver of the South Korea diabetes drugs market. Sedentary lifestyles, unhealthy diets, and genetic predisposition contribute to the growing number of diabetes cases. For instance, the International Diabetes Federation (IDF) reported that 12.5% of South Koreans aged 19 and older were living with diabetes as of 2022, with the prevalence rising to 14.8% among those aged 30 and older. As life expectancy increases, the demand for effective diabetes management solutions is expanding. The aging demographic is more susceptible to diabetes and related complications, necessitating long-term medication use. This trend is expected to sustain the market’s growth over the forecast period.

Advancements in Pharmaceutical Innovations

Technological advancements in diabetes drug development are transforming the treatment landscape in South Korea. Novel drug classes, such as GLP-1 receptor agonists, SGLT2 inhibitors, and DPP-4 inhibitors, are improving treatment efficacy, offering better glycemic control with fewer side effects. For instance, the Ministry of Food and Drug Safety recently approved Mounjaro, a GLP-1 receptor agonist, which has demonstrated superior glycemic control and weight management benefits in clinical trials. Furthermore, the pharmaceutical industry is focusing on research and development to introduce combination therapies that enhance patient compliance. The growing emphasis on personalized medicine, with tailored drug regimens based on genetic and metabolic profiling, is also contributing to market expansion.

Government Support and Healthcare Infrastructure

South Korea’s robust healthcare infrastructure and supportive government policies play a crucial role in driving the diabetes drugs market. The National Health Insurance (NHI) system provides coverage for diabetes medications, making treatment more accessible to a larger population. Additionally, the government actively promotes diabetes awareness campaigns and early screening programs to facilitate timely diagnosis and management. Regulatory bodies are streamlining approval processes for innovative diabetes treatments, allowing faster market entry for advanced drugs. Investments in digital health solutions, such as telemedicine and AI-driven diabetes management platforms, are further enhancing patient care and medication adherence.

Growing Adoption of Digital Health and Smart Therapeutics

The integration of digital health technologies into diabetes management is accelerating market growth in South Korea. Smart insulin delivery systems, continuous glucose monitoring (CGM) devices, and mobile health applications are gaining popularity among patients and healthcare providers. These innovations improve treatment outcomes by enabling real-time monitoring and personalized therapeutic interventions. Pharmaceutical companies are increasingly collaborating with tech firms to develop AI-powered solutions for diabetes care. The shift toward data-driven and patient-centric approaches is enhancing medication adherence and disease management. As digital health adoption increases, it is expected to further drive demand for advanced diabetes medications in the country.

Market Trends

Growing Preference for Novel Drug Classes

The South Korea diabetes drugs market is witnessing a shift toward newer drug classes that offer enhanced efficacy and additional health benefits. GLP-1 receptor agonists, SGLT2 inhibitors, and DPP-4 inhibitors are gaining market traction due to their ability to improve glycemic control while addressing comorbidities such as obesity and cardiovascular disease. These medications are becoming the preferred choice among healthcare providers as they offer better patient outcomes with fewer side effects compared to traditional therapies like sulfonylureas and insulin. As more clinical studies validate their long-term benefits, the adoption of these novel drug classes is expected to rise steadily.

Increasing Demand for Combination Therapies

Combination therapies are becoming increasingly popular in diabetes management as they enhance treatment effectiveness and improve patient adherence. Fixed-dose combinations (FDCs) of oral antidiabetic drugs (OADs) and injectable therapies are being developed to simplify treatment regimens, reducing the pill burden for patients. For instance, research published by the Korean Endocrine Society highlights the efficacy of fixed-dose combinations in achieving better glycemic control and reducing the risk of complications. Pharmaceutical companies are focusing on launching new combination drugs tailored to individual patient needs, further driving market growth. The rising acceptance of such therapies among both patients and healthcare providers is expected to fuel the market in the coming years.

Integration of Digital Health and Smart Diabetes Management

The adoption of digital health solutions in diabetes care is transforming the South Korean market. Patients and healthcare professionals are increasingly utilizing mobile health applications, continuous glucose monitoring (CGM) devices, and smart insulin delivery systems to optimize diabetes management. For instance, Kakao Healthcare, in collaboration with Novo Nordisk, has launched Project Gamma, an AI-powered diabetes management platform that integrates smart insulin pens and real-time glucose monitoring. Telemedicine services are also expanding, providing remote consultations and medication management, which enhances accessibility for diabetic patients. These digital health advancements are complementing pharmaceutical treatments, leading to better patient engagement and improved disease control.

Expansion of Biosimilar and Generic Drug Markets

The rising demand for cost-effective diabetes treatments is driving the growth of biosimilars and generic drugs in South Korea. As patents for several blockbuster diabetes drugs expire, domestic pharmaceutical companies are investing in biosimilar and generic alternatives to provide affordable treatment options. These cost-efficient alternatives are increasing accessibility for a broader patient population while reducing the financial burden on the healthcare system. Government initiatives to promote generic drug adoption and streamline regulatory approvals are further accelerating this trend. As competition intensifies, innovation in formulation and delivery methods is expected to shape the future of the diabetes drug market in South Korea.

Market Challenges Analysis

High Cost of Advanced Diabetes Treatments

The rising cost of innovative diabetes medications poses a significant challenge to market growth in South Korea. Newer drug classes, such as GLP-1 receptor agonists and SGLT2 inhibitors, offer superior efficacy but come at a higher price, making them less accessible for a portion of the population. For instance, the Ministry of Health and Welfare reported that out-of-pocket expenses for advanced diabetes treatments account for a significant portion of household healthcare spending, particularly for elderly patients requiring long-term medication. Despite government reimbursement policies, out-of-pocket expenses for advanced treatments remain a concern for many patients, particularly those requiring long-term medication. The cost disparity between branded drugs and their generic or biosimilar counterparts further limits widespread adoption. Pharmaceutical companies must balance innovation with affordability to ensure broader access to effective diabetes management solutions.

Regulatory and Market Access Barriers

Stringent regulatory requirements and complex approval processes for new diabetes drugs present another challenge for market players. South Korea’s regulatory framework demands extensive clinical trials and safety evaluations before granting market approval, which can delay the launch of innovative treatments. Additionally, pricing negotiations with the National Health Insurance (NHI) system can be lengthy, impacting the timely availability of new medications. The increasing competition from generics and biosimilars also exerts pressure on pharmaceutical companies to justify pricing while maintaining profitability. These market access barriers may slow the entry of cutting-edge therapies, affecting the pace of diabetes drug market expansion in South Korea.

Market Opportunities

The South Korea diabetes drugs market presents significant growth opportunities driven by increasing investments in research and development (R&D) for innovative treatment solutions. Pharmaceutical companies are focusing on the development of next-generation therapies, including novel GLP-1 receptor agonists, dual-acting drugs, and advanced insulin formulations that offer improved glycemic control with minimal side effects. The growing adoption of personalized medicine, supported by advancements in genetic profiling and precision therapeutics, further enhances treatment outcomes. Additionally, the expansion of biosimilars and cost-effective generic alternatives is creating opportunities for domestic pharmaceutical firms to strengthen their market presence while increasing affordability for patients. Collaborations between multinational and local pharmaceutical companies are also facilitating faster drug development and commercialization, enhancing access to innovative diabetes treatments.

The integration of digital health solutions and AI-driven diabetes management tools is another key area of opportunity in South Korea. With the increasing use of continuous glucose monitoring (CGM) systems, mobile health applications, and smart insulin delivery devices, there is potential for pharmaceutical companies to enhance patient adherence and treatment efficacy. Government initiatives supporting telemedicine and digital healthcare are further accelerating this trend, providing better access to remote consultations and personalized treatment plans. The growing emphasis on preventive healthcare and early diabetes detection programs presents an opportunity for pharmaceutical companies to expand their market reach by offering holistic diabetes management solutions. As healthcare policies continue to evolve, companies that invest in innovative, patient-centric approaches will likely gain a competitive advantage in South Korea’s dynamic diabetes drugs market.

Market Segmentation Analysis:

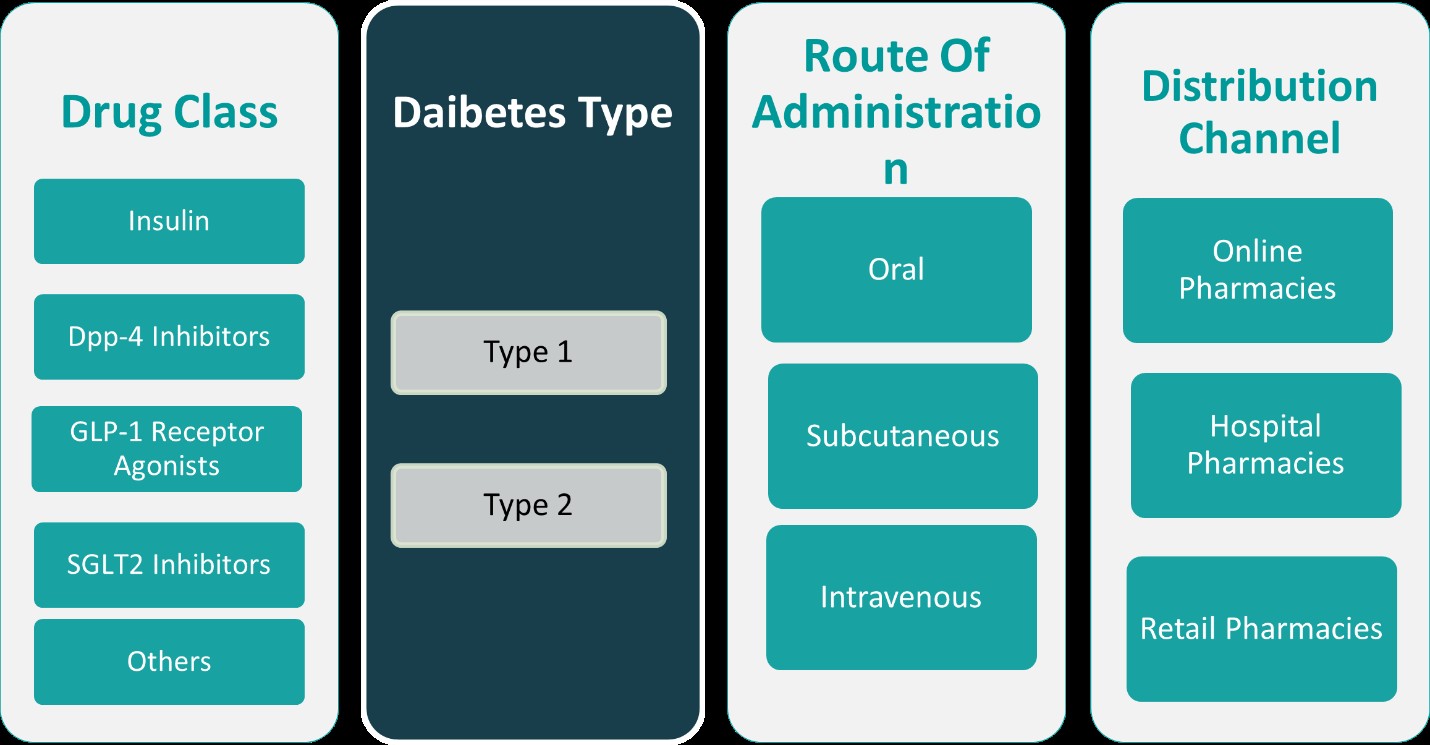

By Drug Class:

The South Korea diabetes drugs market is categorized into insulin, DPP-4 inhibitors, GLP-1 receptor agonists, SGLT2 inhibitors, and other antidiabetic medications. Insulin remains a crucial segment, particularly for Type 1 diabetes management and advanced Type 2 diabetes cases. With ongoing advancements, ultra-long-acting and biosimilar insulin formulations are gaining market traction. DPP-4 inhibitors continue to be widely prescribed due to their ability to improve glycemic control with minimal risk of hypoglycemia. GLP-1 receptor agonists are growing in popularity, driven by their added cardiovascular and weight management benefits. SGLT2 inhibitors are experiencing strong adoption as they not only lower blood sugar but also offer renal and heart-related advantages. The “Others” category includes traditional sulfonylureas, thiazolidinediones, and combination therapies, which remain relevant, particularly in cost-sensitive patient segments. The increasing availability of combination therapies incorporating multiple drug classes is further optimizing diabetes management, improving patient adherence, and expanding the treatment landscape in South Korea.

By Diabetes Types:

Diabetes drugs in South Korea are also segmented by diabetes type, including Type 1, Type 2, and lesser-known variations such as Diabetes Type 3, Type 4, and Type 5. Type 1 diabetes primarily relies on insulin therapy, with growing interest in automated insulin delivery systems and biosimilar insulins. Type 2 diabetes constitutes the largest market segment, driven by lifestyle-related factors and an aging population. Treatment strategies for Type 2 diabetes are shifting toward combination therapies, personalized medicine, and digital health integration to enhance disease management. Diabetes Type 3, often linked to neurodegenerative conditions such as Alzheimer’s, is gaining research attention, leading to potential new therapeutic approaches. Diabetes Type 4, associated with age-related insulin resistance, is becoming more relevant due to South Korea’s aging demographic. Diabetes Type 5, which includes rare and atypical diabetes cases, presents niche opportunities for targeted drug development. The growing awareness and classification of these diabetes subtypes are influencing treatment protocols and expanding the market for innovative therapies.

Segments:

Based on Drug Class:

- Insulin

- DPP-4 Inhibitors

- GLP-1 Receptor Agonists

- SGLT2 Inhibitors

- Others

Based on Diabetes Types:

- Type 1

- Type 2

- Diabetes Type 3

- Diabetes Type 4

- Diabetes Type 5

Based on Route of Administration:

- Oral

- Subcutaneous

- Intravenous

- Route of Administration 4

- Route of Administration 5

Based on Technology:

- Technology 1

- Technology 2

- Technology 3

Based on Distribution Channel:

- Online Pharmacies

- Hospital Pharmacies

- Retail Pharmacies

- Distribution Channel 4

- Distribution Channel 5

Based on the Geography:

- Seoul Metropolitan Region

- Gyeonggi Province

- Busan and Ulsan Regions

- Daegu Region

Regional Analysis

Seoul Metropolitan Region

The Seoul Metropolitan Region holds the largest market share in the South Korea diabetes drugs market, accounting for approximately 40% of the total market. As the most densely populated region with advanced healthcare infrastructure, Seoul serves as a key hub for diabetes diagnosis, treatment, and research. The presence of leading hospitals, research institutions, and pharmaceutical companies fosters innovation and early adoption of advanced diabetes treatments. High healthcare expenditure and a growing number of specialized diabetes care centers contribute to the region’s dominance. Additionally, the increasing elderly population and lifestyle-related diabetes cases drive demand for novel therapeutics, including GLP-1 receptor agonists and SGLT2 inhibitors. Government initiatives promoting diabetes awareness and digital health solutions further support market growth in Seoul.

Gyeonggi Province

Gyeonggi Province follows with a 25% market share, driven by its large and diverse population, as well as its proximity to the Seoul Metropolitan Region. The province is home to several major hospitals and pharmaceutical manufacturing facilities, making it a key player in South Korea’s healthcare sector. The growing prevalence of diabetes, especially Type 2 diabetes, is fueling demand for both traditional and innovative treatment options. The increasing adoption of biosimilars and generic alternatives is also evident in this region, providing cost-effective solutions for diabetes management. Furthermore, the province benefits from government-supported healthcare programs and insurance policies that enhance accessibility to diabetes medications. The rising use of digital health platforms and telemedicine services in Gyeonggi Province is further transforming diabetes care and improving patient adherence.

Busan and Ulsan Regions

The Busan and Ulsan regions collectively account for 20% of the South Korea diabetes drugs market, supported by a well-established healthcare system and increasing diabetes prevalence. As major industrial and economic centers, these regions experience high rates of lifestyle-related diabetes due to sedentary work environments and dietary habits. The presence of leading medical universities and research centers enhances diabetes treatment options, driving the adoption of innovative drug therapies. The government’s focus on expanding healthcare access in these areas is improving early diabetes diagnosis and treatment. Additionally, the demand for combination therapies and novel drug classes such as GLP-1 receptor agonists and DPP-4 inhibitors is rising, as healthcare providers prioritize more effective and convenient treatment solutions for patients.

Daegu Region

The Daegu Region holds a 15% market share in the South Korea diabetes drugs market, with steady growth driven by an aging population and increasing healthcare investments. Daegu is known for its expanding pharmaceutical and biotechnology industries, which support drug research and development. The region has witnessed a rise in diabetes awareness programs and government-funded healthcare initiatives, encouraging early detection and treatment. Although traditional oral antidiabetic drugs remain prevalent, there is a noticeable shift toward advanced therapies, including insulin analogs and personalized diabetes management solutions. Additionally, Daegu’s growing digital health ecosystem is playing a key role in improving patient monitoring and treatment adherence. With continued investments in healthcare innovation, the region is poised for further market expansion in the coming years.

Key Player Analysis

- Novo Nordisk A/S

- Sanofi

- Merck & Co., Inc.

- Eli Lilly and Company

- AstraZeneca

- Takeda Pharmaceutical Company Limited

- Boehringer Ingelheim International GmbH

- Novartis AG

- Johnson & Johnson Services, Inc.

- Bayer AG

- Handok

- Medtronic

Competitive Analysis

The South Korea diabetes drugs market is highly competitive, with major global and domestic pharmaceutical companies driving innovation and market expansion. Leading players such as Novo Nordisk, Sanofi, Merck & Co., Eli Lilly, AstraZeneca, Takeda, Boehringer Ingelheim, Novartis, Johnson & Johnson, Bayer, Handok, and Medtronic play a pivotal role in shaping the industry. These companies focus on developing next-generation diabetes therapies, including GLP-1 receptor agonists, SGLT2 inhibitors, and insulin analogs, to enhance treatment efficacy and patient outcomes. Companies are also expanding their product portfolios by developing biosimilars and fixed-dose combination therapies to enhance affordability and accessibility. In addition to traditional pharmaceutical competition, the market is experiencing rapid advancements in digital health integration, with AI-driven diabetes management tools, smart insulin delivery systems, and continuous glucose monitoring (CGM) devices gaining popularity. Regulatory challenges and pricing pressures continue to influence market dynamics, prompting companies to optimize their supply chains and focus on cost-effective treatment solutions. Strong government support for healthcare innovation and chronic disease management further fuels the competitive landscape, ensuring continuous development and adoption of advanced diabetes medications.

Recent Developments

- In March 2025, Novo Nordisk signed a deal worth up to $2 billion for the rights to UBT251, a new obesity and diabetes drug developed by United BioTechnology. The drug combines GLP-1, GIP, and glucagon to manage blood sugar and reduce hunger.

- In February 2025, Sanofi received FDA approval for MERILOG, the first rapid-acting insulin aspart biosimilar, to improve glycemic control in adults and pediatric patients with diabetes.

- In December 2024, JD Health began offering Merck’s GLUCOPHAGE XR (Reduce Mass) online in China, enhancing access to metformin hydrochloride extended-release tablets for type 2 diabetes patients.

- In December 2024, Torrent Pharma acquired three diabetes brands from Boehringer Ingelheim, including those with Empagliflozin, to strengthen its anti-diabetes portfolio

- In November 2024, AstraZeneca presented promising early data for its obesity pipeline, including AZD5004, an oral GLP-1 receptor blocker, at ObesityWeek 2024.

Market Concentration & Characteristics

The South Korea diabetes drugs market is moderately concentrated, with a mix of global pharmaceutical giants and domestic companies competing for market share. Leading players dominate the industry through extensive R&D investments, product innovation, and strategic collaborations, focusing on advanced diabetes therapies such as GLP-1 receptor agonists, SGLT2 inhibitors, and biosimilar insulins. The market is characterized by high regulatory standards, increasing demand for personalized treatment solutions, and a growing shift toward combination therapies to improve patient adherence. While established brands hold a significant portion of the market, emerging domestic manufacturers are gaining traction by introducing cost-effective biosimilars and generic alternatives. The adoption of digital health technologies, AI-powered treatment solutions, and smart insulin delivery systems is further shaping market dynamics. With government support for diabetes management programs and a rising diabetic population, the market is expected to witness steady growth, driven by innovation and evolving treatment approaches.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Drug Class, Diabetes Types, Route of Administration, Technology, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The South Korea diabetes drugs market will continue to grow steadily, driven by rising diabetes prevalence and an aging population.

- Advancements in GLP-1 receptor agonists, SGLT2 inhibitors, and insulin analogs will enhance treatment options.

- Increased adoption of digital health solutions, AI-driven diabetes management, and smart insulin devices will improve patient adherence.

- Biosimilars and generic diabetes drugs will gain traction, making treatments more affordable and accessible.

- Combination therapies will become more common, offering better glycemic control and improved patient compliance.

- Regulatory policies will continue to evolve, streamlining approvals for innovative diabetes medications.

- Growing investments in R&D and personalized medicine will lead to more targeted and efficient treatment approaches.

- Telemedicine and remote patient monitoring will expand, enhancing diabetes management in underserved areas.

- Partnerships between global and domestic pharmaceutical companies will accelerate new drug development and commercialization.

- Government initiatives promoting preventive healthcare and early diabetes detection will shape future market trends.