| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Acute Care Needleless Connectors Market Size 2023 |

USD 2,142.42 Million |

| Acute Care Needleless Connectors Market, CAGR |

4.98% |

| Acute Care Needleless Connectors Market Size 2032 |

USD 3,150.51 Million |

Market Overview:

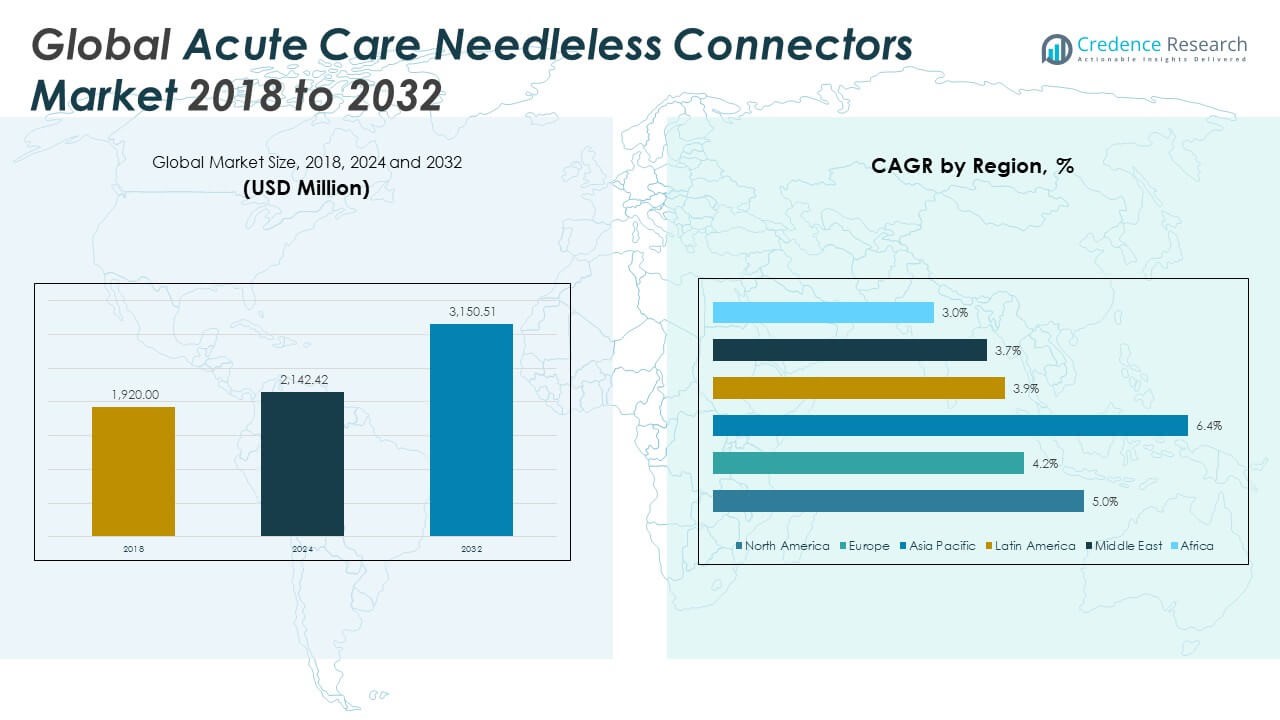

The Global Acute Care Needleless Connectors Market size was valued at USD 1,920.00 million in 2018 to USD 2,142.42 million in 2024 and is anticipated to reach USD 3,150.51 million by 2032, at a CAGR of 4.98% during the forecast period.

Key market drivers include the increasing prevalence of hospital-acquired infections (HAIs) and the global emphasis on minimizing cross-contamination through safe intravenous access systems. Healthcare institutions are rapidly adopting needleless connectors as a standard of care, driven by stricter regulatory guidelines from organizations such as the CDC and OSHA. Continuous innovation in connector design—such as neutral fluid displacement technology, antimicrobial coatings, and closed-system mechanisms—has significantly improved device performance, safety, and ease of use. These advancements are also aligned with hospital efficiency initiatives, as needleless connectors help reduce infection-related complications, lower treatment costs, and decrease hospital stays. Moreover, the shift toward minimally invasive procedures and heightened demand for patient-centric, cost-effective solutions are further accelerating the global adoption of these systems.

Regionally, North America leads the global market, accounting for the largest revenue share due to its advanced healthcare infrastructure, early adoption of safety-engineered devices, and robust regulatory compliance. The United States continues to dominate the region, with increasing use of needleless connectors across hospitals, outpatient centers, and home infusion setups. Europe follows closely, driven by strong government policies around infection prevention and standardization of safety practices across healthcare systems in countries like Germany, the UK, and France. The Asia Pacific region is emerging as the fastest-growing market, with countries such as China, India, and Japan experiencing rapid expansion in healthcare spending, infrastructure modernization, and clinical awareness. Latin America and the Middle East & Africa, while representing smaller market shares, are showing increasing potential supported by growing investments in healthcare services and rising incidence of hospital-related infections. Collectively, these regional dynamics reflect a strong global push toward safer, more effective vascular access solutions in acute care settings.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Global Acute Care Needleless Connectors Market grew from USD 1,920.00 million in 2018 to USD 2,142.42 million in 2024 and is expected to reach USD 3,150.51 million by 2032, registering a CAGR of 4.98% during the forecast period.

- Strict infection control regulations from organizations like the CDC and WHO are driving mandatory adoption of needleless connectors across hospitals to reduce catheter-related bloodstream infections.

- Increased demand for intravenous therapy in emergency, surgical, and intensive care units is fueling the use of connectors that ensure secure, closed-system fluid access.

- Hospitals are adopting needleless systems to protect healthcare workers from needlestick injuries and comply with occupational safety standards, especially in high-turnover environments.

- The shift toward outpatient and home-based care for long-term therapy patients is boosting demand for compact, easy-to-use needleless connectors that support safe self-administration.

- Market growth is challenged by inconsistent design standards, leading to compatibility issues, training difficulties, and potential safety risks in multi-device clinical environments.

- North America holds the largest revenue share due to strong infrastructure and early regulatory adoption, while Asia Pacific is the fastest-growing region, driven by rising healthcare investments in countries like China and India.

Market Drivers:

Stringent Infection Control Guidelines Promote Adoption Across Healthcare Facilities:

The Global Acute Care Needleless Connectors Market is significantly influenced by strict infection prevention protocols in hospitals and surgical centers. Rising rates of catheter-related bloodstream infections (CRBSIs) have led to mandatory use of needleless devices in many healthcare systems. Regulatory bodies including the Centers for Disease Control and Prevention (CDC) and the World Health Organization (WHO) advocate the use of closed-system connectors. Their use reduces touch contamination, supports patient safety, and aligns with hospital accreditation requirements.

- For instance, ICU Medical’s Clave® Needlefree Connector was cited in studies showing a 50% reduction in bloodstream infection rates when compared to conventional split septum devices, supporting compliance with CDC guidelines in over 80% of U.S. acute care hospitals as of 2023.

Rise in Intravenous Therapy Procedures Across Critical Care Units:

A growing number of patients in emergency and intensive care units require intravenous therapy for hydration, antibiotics, and medications. This rise in IV-related procedures has led to greater demand for connectors that ensure secure, leak-proof access. Needleless connectors provide a sterile barrier that prevents backflow and occlusion. Their role in supporting the safe administration of high-risk medications is central to their increased usage in acute care environments.

- For instance, Becton, Dickinson and Company (BD)’s MaxZero™ needleless connector has been implemented across over 600 U.S. hospitals, where it demonstrated a 57% reduction in catheter occlusion rates in multi-center clinical trials conducted between 2022 and 2023.

Focus on Preventing Needlestick Injuries in Healthcare Workers:

Healthcare facilities are implementing advanced vascular access systems to reduce needlestick injuries among nurses, phlebotomists, and other staff. Needleless connectors eliminate exposure to hollow-bore needles, which can transmit bloodborne pathogens. These safety connectors also comply with occupational health regulations, reducing liability for hospitals and encouraging widespread institutional adoption. Demand continues to rise in high-volume facilities with rotating staff and intense procedural schedules.

Expansion of Outpatient and Home-Based Acute Care Services:

Healthcare providers are increasingly shifting toward outpatient and home-based care models, particularly for chronic patients requiring long-term intravenous therapy. Needleless connectors support mobile and at-home infusion setups due to their compact design and minimal maintenance requirements. Their user-friendly features appeal to both healthcare professionals and caregivers. This shift is especially visible in oncology, palliative care, and post-surgical recovery settings.

Market Trends:

Adoption of Antimicrobial Technologies in Connector Design:

The Global Acute Care Needleless Connectors Market is witnessing a clear trend toward antimicrobial enhancements in connector manufacturing. To curb microbial colonization and prevent bloodstream infections, manufacturers are incorporating materials infused with silver ions, ethanol, or chlorhexidine. These antimicrobial agents create a protective barrier on the connector surface, helping reduce contamination risk. Hospitals with long-dwell IV access protocols favor these solutions to maintain sterility over extended periods.

- For instance, Nexus Medical’s ClearGuard® HD Antimicrobial Barrier Cap achieved a 69% reduction in central line-associated bloodstream infections (CLABSIs) in a randomized trial across 14 U.S. hospitals published in 2023, owing to its innovative chlorhexidine-based technology.

Demand for Transparent Housings for Visual Monitoring:

Transparency in design has become a priority for needleless connector manufacturers. Clear connectors allow nurses to verify whether blood reflux, fluid residue, or air bubbles are present in the line. This improves the efficiency of flushing, disinfection, and patency checks. Visual indicators increase compliance with cleaning protocols and support better clinical outcomes. Adoption of such connectors is growing across pediatric, critical care, and oncology units.

- For instance, Designed for neonatal and pediatric patients, Nutrisafe2 connectors feature a transparent housing and a non-threaded interior, reducing residues and enhancing visual confirmation of line contents. Evidence indicates fewer retained residues than ENFit connectors, supporting improved cleanliness and dosing accuracy in intensive care units.

Development of Cost-Efficient Disposable Connector Systems:

Hospitals in low-to-mid-income regions are adopting disposable needleless connector lines to reduce reprocessing costs. These single-use connectors provide sterile vascular access at a lower cost, while also eliminating the risks associated with improper sterilization. Manufacturers are developing economically viable, short-term use connectors to cater to budget-constrained facilities. Their demand is increasing in ambulatory care centers, rural clinics, and emergency relief operations.

Compatibility with Standard IV Systems Across Brands:

Universal design compatibility is shaping purchasing decisions in large healthcare networks. Needleless connectors that integrate seamlessly with a wide variety of IV systems, catheters, and syringes reduce training requirements and lower procurement complexity. Hospitals seek multi-functional, cross-platform connectors that ensure fluid consistency and minimize mechanical disconnection risks. This trend supports standardization efforts in supply chain and inventory management.

Market Challenges Analysis:

Limited Standardization and Design Complexity Across Connector Types:

The Global Acute Care Needleless Connectors Market faces a major challenge due to inconsistent standards in connector design, function, and compatibility across regions and manufacturers. These variations can lead to clinical confusion, increased training requirements, and risks of misuse, particularly in high-pressure acute care settings. Hospitals often deal with multiple connector types that require specific handling procedures, which complicates workflow and increases the potential for human error. Incompatibility between different connectors and IV systems can compromise the integrity of closed systems and introduce infection risk. Despite advances in connector technology, many healthcare facilities lack the infrastructure or resources to transition uniformly to the safest options. The absence of globally harmonized regulatory frameworks also creates uncertainty for manufacturers trying to meet varied compliance demands.

Growing Threat of Microbial Colonization and Biofilm Formation:

Infection control remains a persistent challenge in the Global Acute Care Needleless Connectors Market due to the risk of microbial colonization and biofilm development inside the connectors. Even with neutral or positive displacement mechanisms, studies have shown that improper disinfection practices or repeated manipulation can allow microorganisms to enter the fluid pathway. Once colonized, these connectors become a source of bloodstream infections, especially in patients with central venous catheters. It raises concerns about product safety, especially in environments with limited adherence to disinfection protocols. Despite the availability of antimicrobial coatings, their effectiveness may decline over time, particularly under continuous use. These risks continue to drive demand for rigorous infection control training and innovation in self-cleaning or passive disinfection designs.

Market Opportunities:

Rising Demand in Emerging Healthcare Markets Across Asia, Latin America, and Africa:

The Global Acute Care Needleless Connectors Market has strong growth potential in emerging economies where healthcare systems are expanding rapidly. Countries such as India, Brazil, and South Africa are investing in hospital infrastructure, infection control protocols, and staff training. These efforts support the transition from conventional IV access methods to needleless systems. It enables hospitals to reduce needlestick injuries and align with global safety practices. Government-backed healthcare reforms and international funding for infection prevention programs further create favorable conditions for market entry. Local partnerships and affordable product variants tailored for resource-limited settings can help global players penetrate untapped markets.

Advancement of Antimicrobial Technologies and Smart Connector Integration:

The push for advanced infection prevention opens opportunities for innovation in antimicrobial coatings and smart connector technologies. Manufacturers can invest in self-disinfecting materials, passive cleaning mechanisms, and integrated visual indicators to reduce manual errors. It aligns with growing demand for automated and intelligent medical devices that improve workflow and safety. Incorporating data-tracking features to monitor usage patterns and disinfection compliance may attract hospitals seeking outcome-based procurement. Regulatory approval of these next-generation systems can strengthen brand differentiation and support premium pricing strategies. The market favors suppliers that combine innovation with clinically validated outcomes.

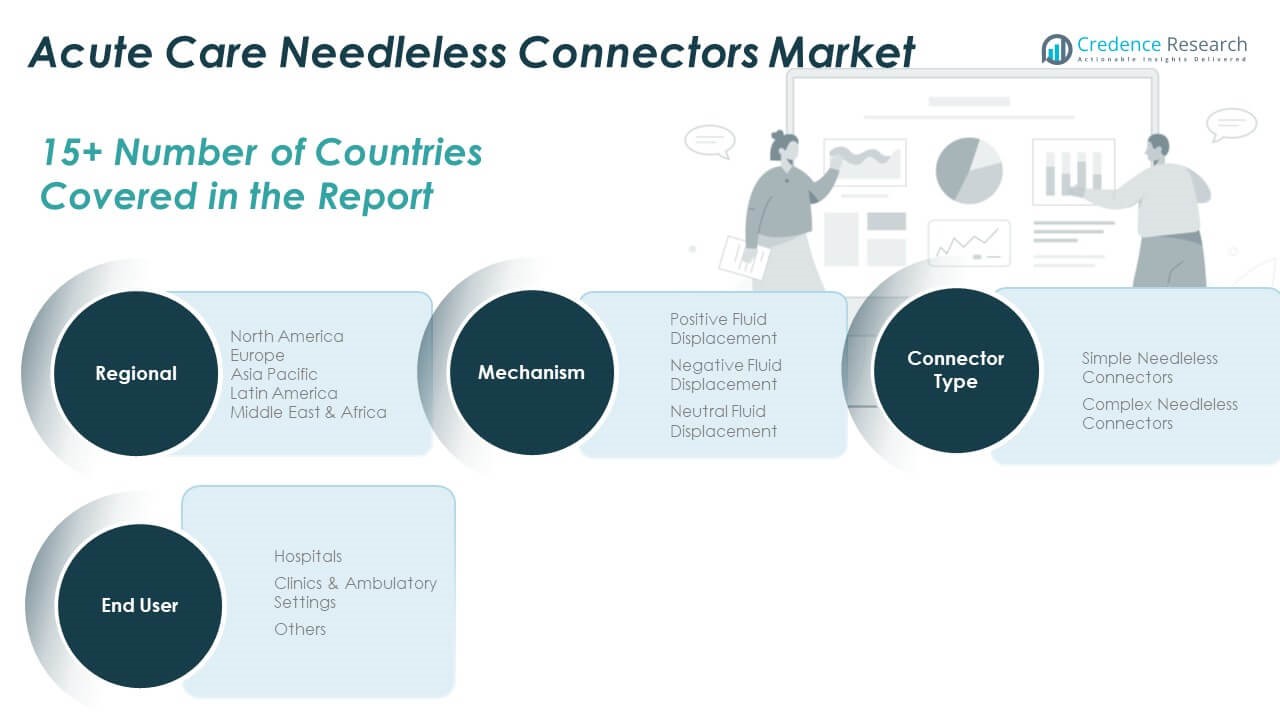

Market Segmentation Analysis:

By Mechanism

The Global Acute Care Needleless Connectors Market is segmented into positive fluid displacement, negative fluid displacement, and neutral fluid displacement connectors. Positive fluid displacement connectors account for the largest market share due to their superior performance in preventing blood reflux and minimizing catheter occlusion risks. These connectors are widely used in hospitals for critical care applications. Negative fluid displacement connectors are seeing reduced use as they are more susceptible to infection-related complications. Neutral fluid displacement connectors are gaining momentum because they offer a balanced approach, combining safety and compatibility across diverse clinical settings such as ICUs and oncology wards.

- For example, a study covering 2,454 central lines found CLABSI rates decreased across all connector types and hospital settings, with neutral connectors associated with the lowest occlusion rates .

By Connector Type

Based on connector type, the market is classified into simple and complex needleless connectors. Simple needleless connectors dominate the market owing to their cost-efficiency, user-friendliness, and suitability for routine medical procedures. They are preferred in high-volume environments such as general wards and emergency departments. Complex needleless connectors are designed for high-risk or specialized procedures that require advanced flow control, minimal manipulation, and integrated safety features. Their adoption is steadily increasing in oncology, intensive care, and pediatric units where safety and precision are critical.

- For example, In clinical evaluations, the One-Link connector dual-seal design provided a 26% reduction in catheter occlusion and an additional layer of protection against microbial ingress. Its clear housing also aids in the visualization of blood or fluid residues.

By End-User

By end-user, the market is segmented into hospitals, clinics & ambulatory settings, and others. Hospitals represent the largest revenue contributor due to high patient volumes, frequent use of IV therapy, and strict infection prevention protocols. Clinics and ambulatory care centers are rapidly adopting needleless connectors to enhance procedural safety and align with regulatory standards. The others segment, which includes long-term care facilities and home healthcare providers, is expanding as more patients receive complex therapies outside traditional hospital settings. This trend is driven by growing demand for home-based infusion solutions, particularly in oncology, palliative care, and chronic disease management.

Segmentation:

By Mechanism

- Positive Fluid Displacement

- Negative Fluid Displacement

- Neutral Fluid Displacement

By Connector Type

- Simple Needleless Connectors

- Complex Needleless Connectors

By End-user

- Hospitals

- Clinics & Ambulatory Settings

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East

- Africa

Regional Analysis:

North America

North America accounted for the largest share of the Global Acute Care Needleless Connectors Market, with a market size of USD 793.34 million in 2018, reaching USD 875.81 million in 2024, and projected to hit USD 1,286.36 million by 2032, growing at a CAGR of 5.0%. This growth is driven by advanced healthcare infrastructure, widespread awareness of hospital-acquired infection (HAI) prevention, and stringent adherence to safety regulations such as those from OSHA and CDC. The United States leads the region in adoption, supported by a well-structured reimbursement landscape and the presence of major industry players like ICU Medical and Becton, Dickinson and Company. Group purchasing organizations (GPOs) and large hospital networks favor bulk procurement of standardized, safety-focused connectors, pushing manufacturers to innovate and scale. Canada contributes significantly, with hospitals investing in infection prevention and training programs to support the implementation of closed IV systems.

Europe

Europe remains the second-largest region, with the market growing from USD 466.56 million in 2018 to USD 498.70 million in 2024, and is projected to reach USD 689.18 million by 2032, registering a CAGR of 4.2%. The region’s strong public health systems and policy-driven approach to infection control support broad adoption of safety-engineered infusion devices. Countries such as Germany, the United Kingdom, France, and the Netherlands have mandated infection prevention guidelines, which promote the use of needle-free IV connectors in acute and ambulatory care settings. EU directives targeting antimicrobial resistance and catheter-related bloodstream infections (CRBSIs) have led to the integration of antimicrobial connectors. Hospitals in Western Europe often base purchasing decisions on clinical validation, cost-efficiency, and ease of integration into existing systems. In Eastern Europe, market expansion is being supported by EU-backed health modernization programs, international aid, and private sector investment, all contributing to a gradual but notable uptake of advanced connector technologies.

Asia Pacific

Asia Pacific represents the fastest-growing regional market, expanding from USD 424.32 million in 2018 to USD 496.71 million in 2024, and is projected to reach USD 813.78 million by 2032 at a CAGR of 6.4%. This growth is fueled by a rapid rise in hospital construction, increasing procedural volumes, and healthcare reforms in populous countries like China and India. The region is experiencing significant demand for IV therapy and infusion devices due to a growing middle class, aging populations, and expansion of health insurance coverage. Local manufacturers are introducing cost-effective needleless connectors, driving volume-based adoption in public and private hospitals. Meanwhile, countries like Japan, Australia, and South Korea focus on high-end, safety-certified connectors to comply with international standards. Medical tourism, especially in Thailand and Malaysia, adds pressure on hospitals to adhere to infection control norms, further pushing market demand.

Latin America

Latin America holds a modest but growing share of the Global Acute Care Needleless Connectors Market, rising from USD 110.98 million in 2018 to USD 122.53 million in 2024, with projections reaching USD 165.94 million by 2032 at a CAGR of 3.9%. Brazil and Mexico dominate the regional market, driven by the modernization of public health systems, improvements in clinical safety standards, and growth in private hospital chains. The region’s urban hospitals are adopting needleless connectors to comply with international infection control protocols, particularly in oncology, emergency care, and intensive care units. However, adoption remains inconsistent across rural and under-resourced facilities due to budgetary constraints and limited training infrastructure. Growing partnerships with U.S.-based suppliers, regional distributors, and healthcare NGOs are helping bridge the awareness and supply gap. The presence of international accreditation bodies in private hospitals also accelerates the demand for compliant IV access technologies.

Middle East

Middle East is experiencing steady growth in the Acute Care Needleless Connectors Market, with its size increasing from USD 74.30 million in 2018 to USD 77.76 million in 2024, and projected to reach USD 103.35 million by 2032 at a CAGR of 3.7%. The Gulf Cooperation Council (GCC) countries—particularly Saudi Arabia, the UAE, and Qatar—are leading regional development, investing heavily in healthcare infrastructure and hospital infection control programs. Hospitals are integrating closed-system connectors as part of broader efforts to meet Joint Commission International (JCI) and CAP accreditation standards. The region’s private healthcare sector is agile in adopting new medical technologies, often sourcing directly from U.S. and European suppliers. Public hospital procurement processes remain more conservative, often constrained by centralized purchasing systems and limited training infrastructure.

Africa

Africa represents the smallest market but offers long-term potential for growth. The market size increased from USD 50.50 million in 2018 to USD 70.92 million in 2024 and is expected to reach USD 91.90 million by 2032, growing at a CAGR of 3.0%. The region’s healthcare systems vary widely, with the most significant adoption seen in South Africa, Kenya, Nigeria, and Egypt. Urban hospitals in these countries are gradually incorporating needleless connectors, supported by partnerships with NGOs, global health organizations, and donor agencies focused on reducing HAIs and improving maternal and child health outcomes. Despite these efforts, limited access to consistent funding, low awareness among frontline staff, and insufficient regulatory enforcement hinder broader uptake. Supply chain inefficiencies and low procurement budgets further slow market development. Africa is expected to see steady growth in the adoption of safe IV access technologies over the next decade.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Medtronic

- Omnia Medical

- 3M

- Terumo

- Smiths Medical

- Convatec

- Vygon

- Sage Products

- Hollister

- Teleflex

- Fresenius Kabi

- Cardinal Health

- Ethan Medical

- BD (Becton, Dickinson and Company)

- Braun Melsungen AG

Competitive Analysis:

The Global Acute Care Needleless Connectors Market is highly competitive, driven by continuous innovation, regulatory compliance, and clinical safety demands. Key players include BD, ICU Medical, B. Braun Melsungen, Teleflex, and Smiths Medical, each offering a broad range of connectors with patented technologies. It favors companies with strong distribution networks, proven infection prevention performance, and integrated product portfolios. Market leaders focus on enhancing connector designs with neutral fluid displacement, antimicrobial coatings, and closed-system features. Smaller and regional players compete by offering cost-effective alternatives and targeting niche care settings. Strategic collaborations with healthcare providers and expansion into emerging markets support competitive positioning. Companies also invest in clinical validation and regulatory certifications to meet global standards and gain hospital trust. The pace of product development and ability to adapt to evolving safety guidelines will continue to shape competitive dynamics in this market.

Recent Developments:

- In April 2025, Medtronic advanced its long-term strategic partnership with Abbott through the submission of a new interoperable insulin pump for FDA approval. This partnership aims to integrate Medtronic’s insulin delivery systems with Abbott’s continuous glucose monitoring (CGM) technology, enhancing patient safety, workflow efficiency, and connected care in diabetes therapy, which is closely related to infusion and needleless connector innovations.

- In January 2025, Terumo launched the Injection Filter Needle as part of its INFINO™ Development Program. Though primarily intended for both hypodermic and intravitreal drug delivery, the product features a new 5-micrometer integrated mesh filter and advanced hub design to enhance safety, sterility, and clinical integration. This launch extends Terumo’s solutions for needleless and safe infusion applications.

Market Concentration & Characteristics:

The Global Acute Care Needleless Connectors Market exhibits moderate to high market concentration, with a few dominant players controlling a significant share of global revenue. It is characterized by strong brand loyalty, high regulatory scrutiny, and a focus on clinical performance and infection prevention. Companies with established product portfolios and regulatory approvals maintain a competitive edge, particularly in hospital procurement cycles. The market demands consistent innovation in design, ease of use, and safety features to meet evolving clinical needs. It also reflects high entry barriers due to stringent quality standards, patent protection, and long approval timelines. Customer preferences lean toward proven technologies backed by clinical evidence, making reputation and reliability key factors in purchasing decisions.

Report Coverage:

The research report offers an in-depth analysis based on mechanism, connector type, and end-user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising global focus on infection control will continue to drive adoption across acute care settings.

- Technological advancements will enhance connector performance, usability, and antimicrobial resistance.

- Increased healthcare spending in Asia Pacific will support strong regional market expansion.

- Home infusion therapy growth will boost demand for user-friendly and portable connector designs.

- Hospitals will prioritize closed-system connectors to comply with evolving regulatory standards.

- Integration of smart tracking features may improve compliance and product differentiation.

- Aging populations and chronic disease prevalence will increase the volume of IV therapies.

- Collaborations between manufacturers and healthcare systems will streamline product standardization.

- Entry of regional manufacturers may intensify price competition in emerging markets.

- Continued emphasis on clinical evidence will shape procurement decisions and product approvals.