Agricultural Coatings Market Overview:

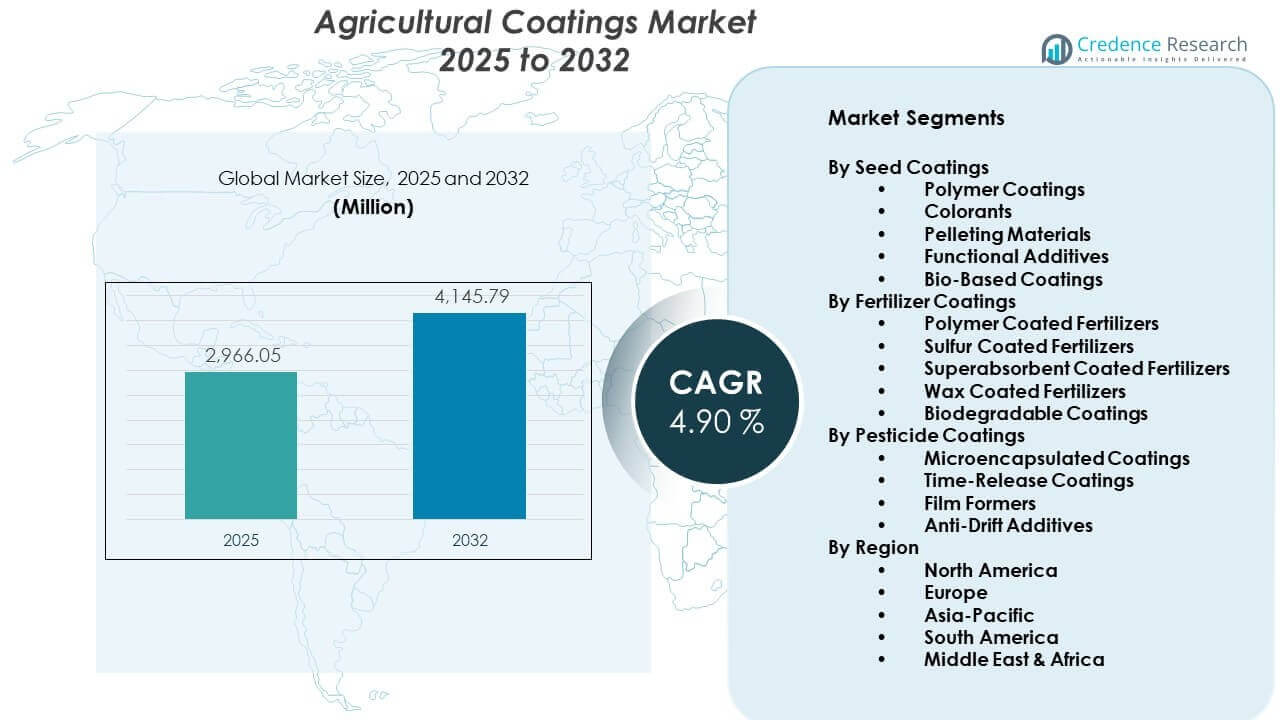

The Agricultural Coatings Market is projected to grow from USD 2,966.05 million in 2025 to an estimated USD 4,145.79 million by 2032, with a compound annual growth rate (CAGR) of 4.90% from 2025 to 2032.

| RT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Agricultural Coatings Market Size 2025 |

USD 2,966.05 million |

| Agricultural Coatings Market, CAGR |

4.90% |

| Agricultural Coatings Market Size 2032 |

USD 4,145.79 million |

Agricultural Coatings Market Insights:

- North America holds the largest share at 33%, followed by Europe at 28% and Asia-Pacific at 22%, driven by advanced farming practices, regulatory backing, and growing adoption of modern inputs.

- Asia-Pacific is the fastest-growing region with 22% share, supported by government subsidies, large-scale crop production, and a shift toward sustainable agriculture.

- Seed coatings lead the market with over 40% share due to widespread usage in crop protection and enhanced germination across diverse climates.

- Fertilizer coatings account for approximately 35% share, driven by the need for controlled nutrient release and increasing environmental compliance.

Agricultural Coatings Market Drivers:

Rising Focus on Crop Yield Enhancement and Input Efficiency

The Agricultural Coatings Market gains momentum due to global pressure to boost food production. Coatings applied to seeds, fertilizers, and pesticides improve absorption, minimize wastage, and extend product effectiveness. Coated seeds offer improved germination and plant vigor in variable field conditions. Fertilizer coatings reduce nutrient leaching and volatilization, helping farmers achieve higher efficiency. These outcomes lower input costs over time, encouraging adoption in both developed and emerging economies. Governments and private players support innovations in coating technologies. Precision agriculture tools work well with controlled-release inputs. The market sees increasing demand from commercial farms aiming to optimize return per hectare.

- For instance, Corteva Agriscience reported in its 2024 Field Trial Data that fields treated with N-Serve® nitrogen stabilizer in the fall of 2023 maintained up to 19% more nitrogen in the ammonium form than untreated samples.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Growing Demand for Sustainable and Eco-Friendly Farming Inputs

Environmental concerns push demand for biodegradable and non-toxic coating formulations. Farmers seek safer options that protect soil health while enhancing agricultural productivity. Water-soluble and bio-based coatings attract attention due to lower residue risks. These coatings support eco-certification goals for export crops. Regulatory bodies encourage low-impact alternatives, influencing product development. The Agricultural Coatings Market responds with active R&D into greener chemistries. Suppliers invest in scalable eco-friendly formulations to meet tightening environmental norms. Adoption of organic and low-toxicity coatings rises across Europe, North America, and parts of Asia.

- For instance, BASF SE has developed the Sepiret® Red 01 seed treatment coating, which uses a microplastic-free formulation to provide superior dust control and enhanced abrasion resistance. This technology is specifically designed to help European growers comply with EU restrictions on synthetic polymer microparticles while maintaining high standards for seed plantability and flowability.

Technological Advancements Supporting Controlled Release and Targeted Action

Coating manufacturers introduce microencapsulation, nanocoatings, and polymer science to refine functionality. These solutions help time-release nutrients, pesticides, or moisture-retaining agents. Controlled application improves resource use and mitigates crop burn or overdose. Advanced coatings enable compatibility with various soil types and weather patterns. Players invest in multi-layered structures that respond to temperature or pH triggers. It supports a smarter farming model that reduces environmental impact while boosting performance. The Agricultural Coatings Market benefits from collaborations between agrochemical firms and material science companies. These synergies create highly customized offerings tailored for crop-specific applications.

Supportive Government Initiatives and Subsidy Programs

Policymakers promote sustainable agriculture through subsidies and grants for coated inputs. Programs in countries like India, China, the U.S., and Brazil aim to modernize farming with science-backed tools. Farmers receive financial support to test and adopt coated fertilizers and seeds. These initiatives increase market access for smallholders and cooperatives. Public-private partnerships promote trials of novel coatings in rural regions. The Agricultural Coatings Market finds growth where governments invest in training and infrastructure. Awareness campaigns and demonstration farms showcase performance gains. This ecosystem drives deeper market penetration in underserved areas.

Agricultural Coatings Market Trends:

Shift Toward Smart Agriculture and Digital Input Tracking

Farmers increasingly use smart systems to monitor input performance across growth cycles. Agricultural coatings optimized for IoT and digital sensors improve traceability and performance mapping. Coatings with color indicators or traceable layers allow data integration with precision tools. Large-scale farms demand products that sync with field monitoring platforms. These trends reshape how farmers choose and apply coated products. The Agricultural Coatings Market aligns with digital farming by offering smart-compatible solutions. Input suppliers bundle digital services with coated seeds or fertilizers. This helps drive data-driven agriculture in high-yield regions.

- For instance, Yara International integrated its Atfarm digital monitoring tool with satellite-based and N-Sensor optical technology rather than coated fertilizer sensors to help farmers reach a 75% Nitrogen Use Efficiency (NUE) target, utilizing variable rate application maps that can reduce nitrogen application by up to 12% to 14%.

Expansion of Customized Crop-Specific Coating Solutions

Manufacturers design coatings tailored for specific crop requirements like rice, wheat, corn, or vegetables. These coatings meet unique germination cycles, nutrient demands, or pest resistance levels. Region-specific adaptations address local climate and soil factors. Demand grows for formulations optimized for tropical, temperate, or arid farming zones. Customization improves efficacy and reduces trial-and-error application. It reduces dependence on broad-spectrum inputs that often cause waste. The Agricultural Coatings Market evolves toward crop-centric innovation pipelines. Companies collaborate with agronomists to refine localized coating packages.

- For instance, Syngenta launched the VAYANTIS seed treatment coating specifically for corn, which provides a physical barrier against Pythium and has been verified to increase plant stand by 10% in cold, wet soil conditions compared to non-customized generic coatings.

Rising Interest in Biological Coatings and Microbial Carriers

Bio-based coatings gain popularity for carrying beneficial microbes and biological stimulants. Farmers adopt solutions that combine coatings with biofertilizers or biofungicides. These combinations promote root growth, nutrient uptake, and resistance to disease. Agricultural biotechnology firms explore encapsulating live organisms in stable coatings. Shelf-stability and survivability improve with new coating matrices. The Agricultural Coatings Market includes bio-coating start-ups focusing on regenerative agriculture. This trend supports organic farming and low-chemical input models. Governments back trials of biological coatings in sustainable agriculture programs.

Growth in Post-Harvest Coating Applications

Beyond field use, coatings now support extended shelf life of harvested produce. Edible coatings applied to fruits and vegetables reduce moisture loss and spoilage. Post-harvest treatments gain ground in export-heavy markets like Latin America and Southeast Asia. Coatings with antifungal and antimicrobial properties prevent transit damage. The food industry partners with coating developers to comply with packaging and safety norms. It strengthens the Agricultural Coatings Market by adding value beyond the farm gate. Cold chain logistics companies adopt coating technologies to cut storage losses. Retailers demand produce with longer shelf-life and better visual appeal.

Agricultural Coatings Market Challenges Analysis:

Lack of Standardization and Limited Farmer Awareness in Developing Regions

Inconsistent regulatory frameworks slow uniform adoption across countries. Farmers often struggle to distinguish between quality coatings and ineffective alternatives. Local input distributors rarely offer technical training on coated products. Smallholder farmers lack the resources to test performance claims. This affects trust and slows repeat purchases. Governments face hurdles in enforcing quality control, especially in fragmented rural markets. The Agricultural Coatings Market depends heavily on informed usage and proper handling. Gaps in knowledge, infrastructure, and product availability limit market growth.

Complex Supply Chains and High Production Costs of Advanced Coatings

Producing microencapsulated or multi-layer coatings involves high R&D and equipment costs. Many local manufacturers cannot scale without significant investment. Global supply chain disruptions impact the availability of specialty materials. Polymer and binder prices remain volatile, affecting coating affordability. Transportation costs also add to end-user prices in remote regions. Companies struggle to balance performance with affordability. The Agricultural Coatings Market needs scalable, cost-effective innovations to widen its reach. Without accessible pricing, penetration into price-sensitive markets remains limited.

Agricultural Coatings Market Opportunities:

High Growth Potential in Emerging Agricultural Economies and Climate-Stressed Regions

Rising food demand in Africa, Southeast Asia, and Latin America creates strong market entry opportunities. Countries facing erratic rainfall or poor soil quality seek coated solutions for crop stability. Local governments support modernization of farming inputs. The Agricultural Coatings Market finds expansion room in these underserved geographies. Vendors can offer affordable, high-performance coatings tailored to regional crop cycles. These regions also benefit from digital farming tools that enhance coating use.

Innovation in Edible and Biodegradable Coating Solutions for Post-Harvest Use

Post-harvest loss prevention is a growing concern in global agri-supply chains. Coating developers can expand offerings into produce preservation and transport packaging. Biodegradable coatings that reduce food waste appeal to both retailers and exporters. The Agricultural Coatings Market supports cross-industry innovation between food tech and agri-input firms. Opportunities lie in integrating coatings with logistics and traceability platforms.

Agricultural Coatings Market Segmentation Analysis:

By Seed Coatings Driving Productivity Through Enhanced Protection

Seed coatings lead the Agricultural Coatings Market, offering essential protection and improved seed performance. Polymer coatings provide a physical barrier that enhances seed shelf life and planting efficiency. Colorants support identification and branding while ensuring even application. Pelleting materials increase seed size and uniformity for mechanical planting. Functional additives improve seedling vigor and germination rates under variable conditions. Bio-based coatings gain traction for their eco-friendly properties, aligning with sustainability trends. Demand grows among both commercial and smallholder farmers for seed performance optimization. The segment benefits from innovations in precision agriculture and hybrid seed technologies.

- For instance, BASF (formerly Bayer) provides Poncho/Votivo seed treatment, which is recommended for use with specialized polymers like Flo Rite® 1706 to enhance seed flowability and plantability in high-speed vacuum planters while its biological component (Bacillus firmus) creates a living barrier to protect roots from nematodes.

By Fertilizer Coatings Supporting Nutrient Efficiency and Environmental Safety

Fertilizer coatings represent a rapidly growing segment focused on nutrient delivery control. Polymer-coated fertilizers enable slow-release mechanisms that match crop uptake needs. Sulfur coatings offer cost-effective protection and help address sulfur deficiencies in soil. Superabsorbent coatings improve water retention and nutrient absorption in arid regions. Wax coatings reduce premature nutrient release and enhance application precision. Biodegradable coatings address regulatory pressure for sustainable practices and reduce long-term soil buildup. This segment gains importance in markets adopting climate-smart farming methods. It plays a key role in minimizing runoff and groundwater contamination. Governments promote coated fertilizers through subsidy programs to increase nutrient use efficiency.

- For instance, Nutrien Ltd. produces ESN (Environmentally Smart Nitrogen), a polymer-coated urea that prevents nitrogen loss for up to 50–80 days, ensuring that nutrients remain available during the critical mid-season growth stages when the crop requires them most.

By Pesticide Coatings Advancing Safety and Application Precision

Pesticide coatings support safer, more targeted delivery of crop protection agents. Microencapsulated coatings offer controlled release, reducing environmental exposure and operator risk. Time-release coatings extend effectiveness and reduce application frequency. Film formers enhance adhesion to crop surfaces, limiting drift and wastage. Anti-drift additives improve spray accuracy under windy conditions, supporting precision spraying. This segment gains importance as regulatory scrutiny increases on pesticide usage. The Agricultural Coatings Market leverages coating technologies to improve safety profiles without compromising efficacy. Strong adoption is seen in high-value crops and export-oriented farming systems.

Segmentation:

By Seed Coatings

- Polymer Coatings

- Colorants

- Pelleting Materials

- Functional Additives

- Bio-Based Coatings

By Fertilizer Coatings

- Polymer Coated Fertilizers

- Sulfur Coated Fertilizers

- Superabsorbent Coated Fertilizers

- Wax Coated Fertilizers

- Biodegradable Coatings

By Pesticide Coatings

- Microencapsulated Coatings

- Time-Release Coatings

- Film Formers

- Anti-Drift Additives

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America and Europe Maintain Strong Market Hold

North America holds the largest share of the Agricultural Coatings Market, accounting for around 33%. The U.S. leads with widespread use of seed and fertilizer coatings supported by precision agriculture and advanced farming inputs. Europe follows closely with a market share of approximately 28%, driven by environmental regulations and demand for bio-based coatings. Countries like Germany, France, and the Netherlands actively promote coated fertilizers and pesticides aligned with sustainability goals. Both regions benefit from strong R&D, established agricultural infrastructure, and supportive policies. Companies focus on developing eco-friendly, high-performance coatings for high-value crops in these mature markets.

Asia-Pacific Emerges as a High-Growth Region

Asia-Pacific accounts for about 22% of the Agricultural Coatings Market and shows the fastest growth rate among all regions. China and India drive demand due to large-scale agricultural production and growing adoption of modern farming practices. Farmers seek coated seeds and fertilizers to combat soil degradation and climate variability. Regional governments support precision farming and promote input efficiency through subsidies and awareness programs. The market sees increasing penetration of polymer and biodegradable coatings through public-private partnerships. Rising food security concerns and export demands also push adoption of protective and performance-enhancing agricultural inputs.

Latin America and Middle East & Africa Offer Steady Growth Potential

Latin America represents roughly 10% of the market, led by Brazil and Argentina where commercial farming dominates. Fertilizer coatings see strong uptake in this region to address soil nutrient challenges in large-scale soybean and corn farms. Middle East & Africa hold a smaller share at 7%, yet the market shows potential due to increasing investment in water-efficient agriculture and crop productivity solutions. Coatings that support drought tolerance and nutrient conservation gain traction in arid zones. The Agricultural Coatings Market finds opportunity in improving post-harvest preservation and minimizing input losses in these regions. International agencies and local governments support adoption through pilot programs and agricultural development projects.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The Agricultural Coatings Market features a competitive landscape with strong participation from global chemical and agri-input leaders. Companies like BASF SE, Bayer AG, Clariant, Croda International, and Corteva Agriscience dominate with diverse product lines in seed, fertilizer, and pesticide coatings. These firms invest heavily in R&D to improve coating technologies, focusing on controlled release, bio-based materials, and crop-specific customization. Strategic collaborations, portfolio expansion, and regional partnerships drive their market presence. Emerging players offer innovation in biodegradable and microbial coatings, intensifying competition in sustainable solutions. The market remains innovation-driven, where differentiation hinges on performance, regulatory compliance, and adaptability to climate-smart agriculture. It continues to evolve with technological advancements and regulatory shifts, favoring firms with global reach and strong research capabilities.

Recent Developments:

- In January 2026, Bayer sold its global Flubendiamide active ingredient business assets to Tagros Chemicals India across Latin America, EMEA, and Asia-Pacific, enabling Tagros to expand in crop protection formulations under its new Arqivo entity.

- In January 2026, BASF Agricultural Solutions announced the acquisition of biological insect control from AgBiTech Group, with closing anticipated in the first half of 2026 to enhance its crop protection offerings.

- In November 2025, Clariant announced a joint venture with FUHUA to develop innovative non-halogenated phosphorus-based flame retardants for industries including agriculture, with the facility in Leshan, Sichuan Province.

Report Coverage:

The research report offers an in-depth analysis based on Seed Coatings, Fertilizer Coatings, and Pesticide Coatings. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for smart coatings with controlled-release and sensor-responsive functions will grow, aligning with rising adoption of precision agriculture technologies globally.

- Use of biodegradable and eco-friendly coatings will rise significantly in response to strict environmental regulations and pressure to reduce chemical residue.

- Asia-Pacific will remain the fastest-growing region, supported by government subsidies, agricultural modernization, and rising demand for food security solutions.

- Seed coating adoption will expand across developing economies as awareness and access to high-quality coated seeds improve through extension programs and cooperatives.

- Manufacturers will increase investment in crop-specific coating formulations, targeting corn, rice, wheat, soy, and high-value vegetables to meet tailored agronomic needs.

- Strategic partnerships between agrochemical firms and material science innovators will lead to breakthroughs in microbial and polymer-based coating technologies.

- Water scarcity and soil degradation in arid and semi-arid regions will drive the adoption of moisture-retentive and nutrient-efficient coatings.

- Coatings designed for post-harvest applications will become more relevant as countries look to reduce food loss in transit and storage.

- Global players will expand capacity in emerging markets through joint ventures and local production facilities to meet growing regional demand.

- Regulatory clarity and harmonized standards for coated agricultural inputs will improve market access and product confidence across global supply chains.