Agricultural Lubricant Market Overview:

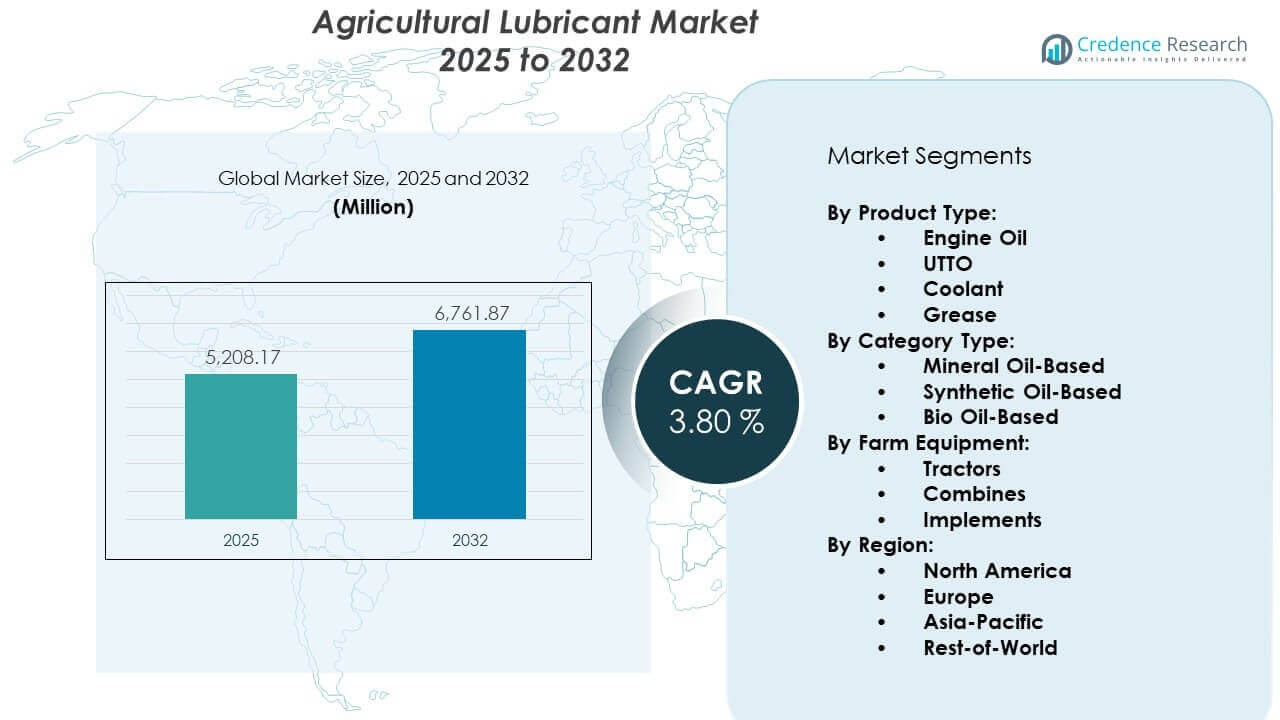

The Agricultural Lubricant Market is projected to grow from USD 5,208.17 million in 2025 to an estimated USD 6,761.87 million by 2032, with a compound annual growth rate (CAGR) of 3.80% from 2025 to 2032.

Rising awareness of preventive maintenance among farmers has led to increased use of engine oils, greases, and hydraulic fluids that reduce wear and ensure machinery uptime.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Agricultural Lubricant Market Size 2025 |

USD 5,208.17 million |

| Agricultural Lubricant Market, CAGR |

3.80% |

| Agricultural Lubricant Market Size 2032 |

USD 6,761.87 million |

Agricultural Lubricant Market Insights:

- North America (32%), Europe (28%), and Asia-Pacific (22%) lead the market due to strong mechanization, advanced farm practices, and rising equipment adoption.

- Asia-Pacific is the fastest-growing region with 22% share, driven by expanding agricultural infrastructure, government equipment subsidies, and increasing tractor penetration.

- By Product Type, engine oil accounts for the largest share at 41%, followed by UTTO and grease, due to high usage in tractors and transmission systems.

- By Category Type, mineral oil-based lubricants hold 54% share, while synthetic and bio-based options gain momentum in environmentally regulated and high-performance applications.

Agricultural Lubricant Market Drivers:

Rising Mechanization and Equipment Usage Across Farming Operations

Mechanization has intensified across both developed and emerging agricultural economies. The use of tractors, combine harvesters, and precision equipment has expanded farm efficiency. These machines require consistent lubrication to ensure smooth performance and extended service life. The Agricultural Lubricant Market benefits from the rising dependency on machines that endure harsh outdoor conditions. Engine oils, greases, and transmission fluids see growing usage due to frequent maintenance cycles. Manufacturers promote high-performance lubricants that meet strict OEM standards. It helps operators reduce unexpected downtime during critical harvest periods. Growth in agri-infrastructure directly supports lubricant demand across field operations.

- For instance, Shell developed the Rimula R4 L engine oil, which uses Low-SAPS technology to provide up to 50% better engine protection against wear and deposits compared to industry standards, supporting the heavy-duty cycles of modern 400+ HP harvesters.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

OEM Recommendations and Growing Equipment Maintenance Awareness

Original equipment manufacturers strongly influence lubricant usage by endorsing specific product formulations. Farmers increasingly follow OEM recommendations to ensure warranty protection and optimal performance. Routine maintenance culture is gaining traction across large farms and cooperatives. It has led to growing demand for customized lubricant blends designed for farm conditions. Lubricant makers now collaborate with OEMs to co-develop fluids aligned with machine technologies. This synergy drives premium lubricant sales in the Agricultural Lubricant Market. Preventive maintenance schedules are now part of agribusiness operations. Greater awareness of machine wear patterns supports consistent lubricant consumption.

- For instance, ExxonMobil partners with major OEMs to provide the Mobil Delvac series, which is tested to maintain its protective properties for up to 600 hours of engine operation, effectively doubling the standard drain interval for many utility tractors.

Shift Toward Longer Drain Intervals and High-Performance Fluids

Longer drain intervals reduce downtime and maintenance costs for large-scale farms. Lubricants that enable extended service intervals without compromising performance are gaining popularity. Synthetic and semi-synthetic blends help reduce friction, wear, and oxidation. These properties support uninterrupted equipment usage throughout planting and harvesting seasons. The Agricultural Lubricant Market benefits from fluid formulations that resist degradation under high pressure. Equipment longevity improves when exposed to fewer fluid changeovers. OEMs design newer engines and hydraulic systems that need advanced lubricants. It drives innovation in formulation, packaging, and delivery across agricultural hubs.

Environmental Concerns Fuel Demand for Biodegradable Lubricants

Environmental protection norms are influencing lubricant choices in farming regions. Operators are now adopting bio-based lubricants to reduce ecological risks. These fluids are non-toxic, biodegradable, and safe around soil and crops. Europe and North America lead this shift with support from regulatory bodies. The Agricultural Lubricant Market sees steady demand for eco-friendly oils in sensitive areas like orchards and wetlands. Public agencies and large estates now include green lubricants in procurement policies. Manufacturers invest in developing renewable base stocks and low-toxicity additives. It fosters sustainable lubrication strategies across diversified farm landscapes.

Agricultural Lubricant Market Trends:

Increased Digitization of Lubricant Monitoring and Dispensing Systems

Digital tools now support lubricant monitoring across farms, enhancing visibility into consumption patterns. IoT-based sensors and smart dispensers track fluid levels, viscosity, and service needs. Farmers can automate lubricant refills and schedule replacements based on real-time data. This trend reduces wastage and improves machinery uptime. Lubricant manufacturers integrate cloud-based platforms into service packages for large farm clients. The Agricultural Lubricant Market benefits from rising interest in predictive maintenance backed by data. Digital tools help ensure correct fluid application across complex machinery. It creates value for tech-savvy operators managing fleet-wide performance metrics.

- For instance, Chevron utilizes its LubeWatch oil analysis program, which uses laboratory-grade data to identify wear particles as small as 2 to 5 microns, allowing farm managers to predict equipment failure up to 200 operating hours before it occurs.

Customized Formulations for Diverse Climate and Soil Conditions

Different climates and soil types affect lubricant requirements across regions. Tropical farms experience high dust, humidity, and operating temperatures, demanding heat-stable greases and engine oils. Cold climates require low-temperature flowability and viscosity stability. Manufacturers now tailor lubricant compositions to meet these specific environmental needs. The Agricultural Lubricant Market embraces regional customization to serve varied field conditions. It includes anti-rust, anti-foaming, and anti-wear additives suited to local applications. Local distributors also stock seasonal grades to meet peak farming schedules. Tailored offerings improve fluid life and machine compatibility in regional markets.

- For instance, MC-Base-Oil technology, a proprietary molecular conversion process by FUCHS that improves performance compared to standard mineral oils.

Growth in Private Label and Contract Manufacturing Partnerships

Private-label lubricants are expanding across agricultural supply chains. Distributors and cooperatives now partner with contract manufacturers to supply branded fluids at competitive prices. These lubricants offer performance similar to leading brands while providing pricing flexibility. The Agricultural Lubricant Market sees volume growth through local alliances and white-label strategies. It enables regional players to serve niche crop segments and smaller farm clusters. Contract manufacturing supports faster lead times and inventory responsiveness. Co-branded solutions also create loyalty in rural distribution networks. This trend expands lubricant access without diluting quality benchmarks.

Sustainable Packaging and Refill Models in Rural Distribution Channels

Rural lubricant distribution has started integrating sustainable practices. Refillable drums, bulk delivery, and eco-safe packaging options are gaining preference. Distributors now promote packaging formats that reduce plastic waste and leakage. The Agricultural Lubricant Market aligns with circular economy efforts by offering reusable canisters and dispensers. It helps reduce logistics costs and supports environmental goals. Brands differentiate through packaging innovations like tamper-proof seals and smart caps. These features offer safety, accuracy, and durability during transport and use. Adoption grows where bulk buyers prioritize cost efficiency and reduced environmental impact.

Agricultural Lubricant Market Challenges Analysis:

Volatile Base Oil Prices and Supply Chain Fluctuations Impact Margins

The Agricultural Lubricant Market remains sensitive to fluctuations in crude oil prices and base oil availability. Lubricant manufacturers depend heavily on consistent base oil supply, which is prone to geopolitical and economic disruptions. Price instability can reduce profit margins or lead to frequent product repricing. Small and medium-sized farms face challenges absorbing sudden cost increases, limiting their lubricant purchases. Distributors also deal with inventory risks when costs shift between order placements and deliveries. Currency fluctuations further complicate international procurement of base stocks. It affects product availability in developing countries. Consistent price stability remains a critical need across lubricant sourcing channels.

Limited Adoption of Advanced Lubricants in Low-Income Farming Regions

Advanced lubricants face low adoption in cost-sensitive and under-mechanized regions. Many smallholders use basic mineral oils or unbranded alternatives that lack durability or compatibility. The Agricultural Lubricant Market faces hurdles where awareness, training, and availability are limited. In some countries, informal markets dominate, reducing the reach of branded products. High-grade lubricants are viewed as expensive, despite offering long-term savings. Equipment compatibility issues also deter use of premium products. This challenge slows the spread of efficient lubrication practices across fragmented agricultural systems. Bridging the adoption gap requires localized outreach, incentives, and education campaigns.

Agricultural Lubricant Market Opportunities:

Growing Farm Consolidation Unlocks Demand for Bulk and Premium Lubricants

Large-scale farm consolidation is reshaping agricultural operations in major economies. Bigger farms manage large fleets and require efficient fluid management systems. These operations prefer bulk purchases and long-drain lubricants for cost savings. The Agricultural Lubricant Market gains traction from clients seeking tailored service agreements and supply contracts. Premium lubricants offer longer service intervals and greater protection, aligning with commercial farm goals. It creates space for value-added partnerships with lubricant service providers.

Bio-Based Lubricants Gain Support Through Regulatory and Environmental Policies

Sustainability programs across the EU, North America, and parts of Asia encourage eco-safe farming practices. Bio-based lubricants now receive regulatory backing and tax incentives in many countries. This opens avenues for lubricant makers offering biodegradable, plant-derived oils. The Agricultural Lubricant Market taps this opportunity by expanding bio-lubricant portfolios. Green certifications and low-toxicity standards improve brand appeal across public and private sectors.

Agricultural Lubricant Market Segmentation Analysis:

By Product Type

The Agricultural Lubricant Market includes four key product types: engine oil, UTTO (Universal Tractor Transmission Oil), coolant, and grease. Engine oil holds the largest share due to high consumption in tractors and heavy-duty equipment. UTTO supports both hydraulic and transmission systems in modern machinery, driving its demand. Coolants are critical in temperature regulation and engine protection during long operational cycles. Greases find steady application in moving parts and joints exposed to dust and moisture. Each product type plays a role in enhancing machine reliability across seasons.

- For instance, TotalEnergies Dynatrans MPV is a high-performance Universal Tractor Transmission Oil (UTTO) specifically developed for transmissions with wet brakes and hydraulic systems in agricultural and construction equipment. This lubricant provides specialized friction control that protects against “judder” (chatter) or excessive slip at high temperatures and prevents friction brakes from sticking at low temperatures.

By Category Type

Lubricants in this market are segmented into mineral oil-based, synthetic oil-based, and bio oil-based categories. Mineral oil-based lubricants dominate due to low cost and widespread availability. Synthetic oil-based lubricants offer better performance, oxidation stability, and longer drain intervals. Bio oil-based lubricants are gaining attention for their biodegradability and environmental safety. The Agricultural Lubricant Market benefits from increasing regulatory pressure favoring sustainable options, especially in developed regions.

- For instance, Shell demonstrated that by switching to its synthetic technology, such as the Shell Rimula R6 LM 10W-40, agricultural operations like LoginEKO extended oil drain intervals from 250 to 450 hours, effectively reducing maintenance downtime.

By Farm Equipment

Key equipment segments include tractors, combines, and implements. Tractors account for the highest lubricant demand due to extensive engine and hydraulic use in daily operations. Combines require advanced lubrication for harvesting systems, especially under high load. Implements such as plows and sprayers rely on greases and specialty fluids for operational durability. The growing mechanization of farms across emerging economies directly supports lubricant demand across all equipment segments.

Segmentation:

By Product Type:

- Engine Oil

- UTTO

- Coolant

- Grease

By Category Type:

- Mineral Oil-Based

- Synthetic Oil-Based

- Bio Oil-Based

By Farm Equipment:

- Tractors

- Combines

- Implements

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America and Europe Lead with Advanced Mechanization

North America accounts for the largest share of the Agricultural Lubricant Market, holding approximately 32%. The region benefits from large-scale commercial farming, widespread mechanization, and a strong presence of OEMs and lubricant manufacturers. The U.S. and Canada maintain high usage of tractors, combines, and precision equipment, supporting constant demand for engine oils and UTTO. Europe follows closely with a 28% share, driven by stringent environmental regulations and adoption of bio-based lubricants. Countries such as Germany, France, and the UK invest in high-performance synthetic lubricants for sustainable operations. Both regions promote preventive maintenance practices that enhance lubricant consumption and product innovation.

Asia-Pacific Emerges as the Fastest-Growing Region

Asia-Pacific holds a 22% share in the Agricultural Lubricant Market and shows the fastest growth rate through the forecast period. Rapid farm mechanization in China, India, and Southeast Asia supports this expansion. Governments across these countries invest in subsidized equipment and rural infrastructure. Rising tractor penetration and awareness of equipment care drive adoption of lubricants in mid-sized and small farms. Local manufacturers supply affordable mineral and blended lubricants to serve cost-sensitive markets. It helps increase lubricant accessibility across fragmented farming systems and seasonal crop cycles. Asia-Pacific remains central to future volume growth for global suppliers.

Rest-of-World Regions Offer Long-Term Growth Potential

The Rest-of-World segment, covering Latin America, the Middle East, and Africa, holds an 18% share of the Agricultural Lubricant Market. Brazil and Argentina lead in Latin America, supported by their large agribusiness sectors and expanding grain exports. Middle Eastern countries invest in precision agriculture and greenhouse farming, increasing demand for equipment lubricants. Africa remains under-mechanized but shows long-term potential due to land availability and rising food demand. Market penetration remains low due to infrastructure gaps and informal distribution. It creates room for targeted education and partnership models to accelerate adoption.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The Agricultural Lubricant Market features strong competition among global oil majors and regional suppliers. Leading players focus on product differentiation through advanced formulations and OEM-approved solutions. Companies compete on durability, performance under harsh field conditions, and extended drain intervals. Brand reputation and distribution strength in rural markets shape competitive positioning. Multinational firms leverage integrated supply chains and R&D capabilities to sustain product innovation. Regional manufacturers compete through price advantage and localized offerings. Strategic partnerships with equipment manufacturers enhance customer loyalty and aftermarket sales. It remains moderately consolidated, with global players holding strong brand influence across developed agricultural economies.

Recent Developments:

- In February 2026, Fuchs Petrolub SE (now FUCHS SE) strengthened its international presence by completing the full takeover of its joint venture, OPET FUCHS, in Türkiye. This follows the company’s January 2025 acquisition of Boss Lubricants, a specialist in open-gear and heavy-duty industrial lubricants, and a May 2025 investment of $39 million in a new state-of-the-art production facility in Brazil designed to produce over 50,000 tonnes of lubricants annually for the Latin American market.

- In January 2026, ExxonMobil Corporation announced that its first greenfield lubricant manufacturing plant in Raigad, Maharashtra, is moving toward full operational status following its initial startup at the end of 2025. The ₹900 crore facility has a capacity of 159,000 kilolitres (approximately 1 million barrels) annually, specifically designed to meet the growing demand for high-performance lubricants in India’s agricultural, industrial, and commercial vehicle sectors.

- In July 2025, Shell plc successfully completed the 100% equity acquisition of Mumbai-based Raj Petro Specialities from the Brenntag Group. This acquisition significantly expands Shell’s footprint in the agricultural and specialty lubricant sectors by integrating Raj Petro’s diverse portfolio of white oils and specialty products, supported by two major manufacturing plants in Chennai and Silvassa that serve over 100 countries globally.

- In March 2025, Chevron Corporation announced its entry as the first domestic producer of Group III+ base oils in North America, with production of its NEXBASE 4 XP grade scheduled to begin at its Pascagoula refinery in the fourth quarter of 2026. These advanced base oils are critical for formulating the next generation of premium agricultural and heavy-duty engine lubricants required by equipment manufacturers to meet the latest high-precision engine approvals.

Report Coverage:

The research report offers an in-depth analysis based on By Product Type, By Category Type, and By Farm Equipment segments. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising farm mechanization across developing nations will steadily increase lubricant consumption across tractors, combines, and sprayers.

- Adoption of high-performance synthetic lubricants will grow to meet longer drain intervals and advanced engine needs.

- Bio-based and biodegradable lubricants will gain wider market share due to growing regulatory mandates and environmental pressures.

- OEM collaborations will expand as manufacturers integrate lubricant recommendations into equipment sales and servicing packages.

- Investment in rural distribution channels will improve lubricant availability, especially in fragmented farm regions across Asia and Africa.

- Smart lubricant monitoring systems and digital service models will support predictive maintenance across large-scale agribusinesses.

- Growth in agri-exports and cash crop cultivation will increase demand for consistent equipment uptime, driving lubricant reliability needs.

- Local blending and private-label manufacturing will expand to address price-sensitive markets and regional product customization.

- New product development will focus on climate-specific lubricants that withstand extreme temperatures and dust exposure.

- Policy incentives for sustainable farming practices will strengthen the market for eco-certified and low-toxicity lubricant solutions.