Agricultural Planting and Fertilizing Machinery Market Overview:

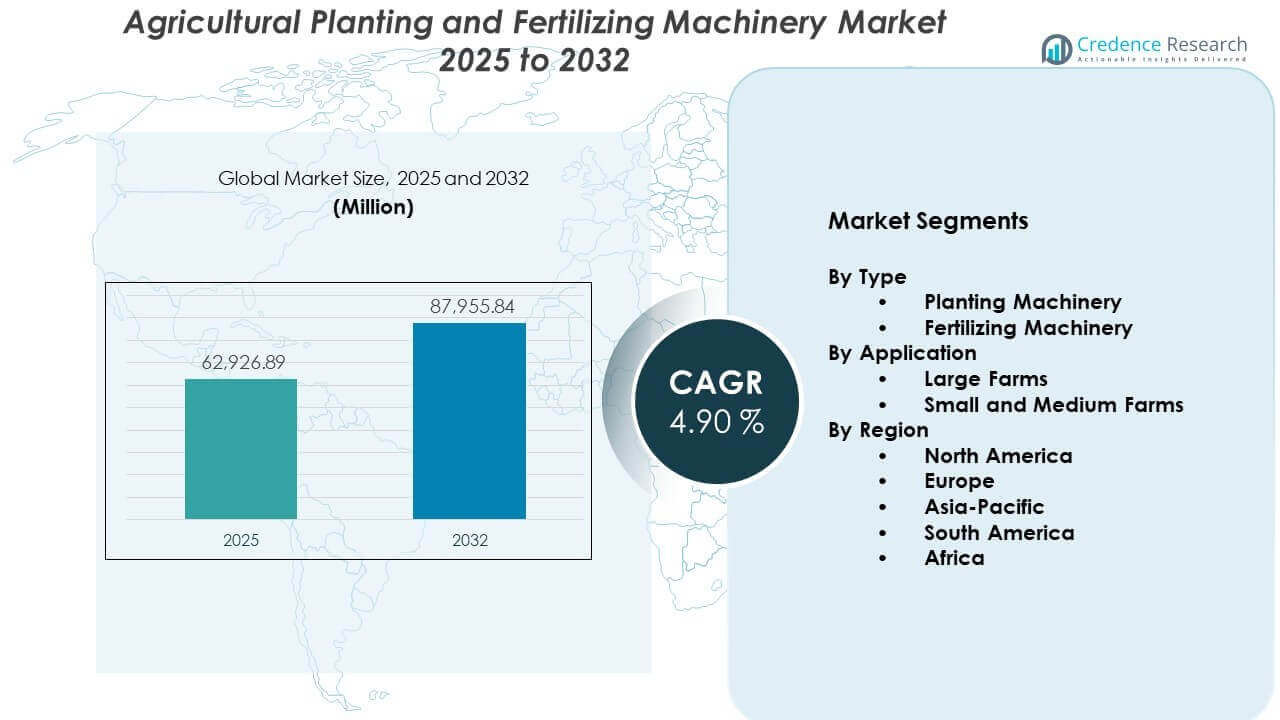

The Agricultural Planting and Fertilizing Machinery Market is projected to grow from USD 62926.89 million in 2025 to an estimated USD 87955.84 million by 2032, with a compound annual growth rate (CAGR) of 4.90% from 2025 to 2032.

Growth in the Agricultural Planting and Fertilizing Machinery Market reflects rapid mechanization across large farms and smallholder operations.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Agricultural Planting and Fertilizing Machinery Market Size 2025 |

USD 62926.89 million |

| Agricultural Planting and Fertilizing Machinery Market, CAGR |

4.90% |

| Agricultural Planting and Fertilizing Machinery Market Size 2032 |

USD 87955.84 million |

Agricultural Planting and Fertilizing Machinery Market Insights:

- Asia-Pacific holds about 32% share, North America about 28%, and Europe about 25%, dominating the market due to high mechanization, strong commercial farming, and extensive dealer and service networks.

- Asia-Pacific is the fastest-growing region with around 32% share, driven by government-backed mechanization schemes, expanding commercial crop acreage, and a shift from manual to machine-based planting and fertilizing.

- By type, Planting Machinery accounts for roughly 60% of the market, with Fertilizing Machinery holding about 40%, reflecting stronger investment priority in accurate seed placement and stand establishment.

- By application, Large Farms represent about 55% of demand, while Small and Medium Farms contribute around 45%, supported by rising access to credit, compact machinery platforms, and custom-hire service models.

Agricultural Planting and Fertilizing Machinery Market Drivers:

Rising Global Food Demand And Need For Higher Crop Yields

Growing population and dietary shifts toward higher-value crops increase pressure on farmland. Farmers must produce more from limited arable land. The Agricultural Planting and Fertilizing Machinery Market helps growers close yield gaps with precise seed and nutrient placement. Advanced planters improve stand uniformity and reduce seed wastage. Modern spreaders and applicators deliver accurate fertilizer doses to target zones. Equipment supports timely field operations within narrow planting windows. It enables farmers to respond quickly to weather shifts and market signals. Strong food security agendas in many countries keep demand for such machinery resilient.

- For instance, AGCO’s Precision Planting DeltaForce system helped prevent average corn yield losses of 14.3 bushels per acre in multi-year studies by maintaining optimal downforce and improving depth consistency across varied soil conditions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Mechanization Acceleration Driven By Rural Labor Shortages And Wage Inflation

Many farming regions face shrinking rural workforces and rising wages. Younger workers often move toward urban or service jobs. Growers adopt planting and fertilizing machines to reduce dependence on manual labor. The Agricultural Planting and Fertilizing Machinery Market gains momentum where seasonal labor is unreliable. High-capacity planters and nutrient applicators allow one operator to cover more hectares per day. Mechanization improves consistency in planting depth and row spacing. It cuts delays during critical sowing periods. Farmers see machinery as a long-term hedge against labor volatility.

- For instance, Kubota Corporation has developed autonomous tractors and rice transplanters that allow a single operator to manage multiple machines, reducing required man-hours by approximately 30% per hectare.

Supportive Government Policies, Subsidy Programs, And Access To Farm Credit

National and regional governments promote mechanization to improve farm income and food supply. Many countries offer purchase subsidies for planters and fertilizer applicators. Tax rebates and interest subventions lower ownership costs for farmers. The Agricultural Planting and Fertilizing Machinery Market benefits when public banks extend longer-tenure loans. Dedicated farm credit lines make high-value machinery accessible to small and mid-sized growers. Governments sometimes link support to adoption of efficient and low-emission equipment. Policy frameworks that protect domestic manufacturing also spur local production bases. It encourages new product launches tailored to regional agronomic needs.

Rising Focus On Sustainability, Resource Efficiency, And Environmental Compliance

Stricter rules on fertilizer runoff, emissions, and soil health shape equipment choices. Farmers seek machines that use nutrients more efficiently and cut losses. Precision applicators reduce overlap and minimize leaching into water bodies. The Agricultural Planting and Fertilizing Machinery Market aligns with sustainability goals by enabling site-specific input management. Planters reduce soil disturbance compared with repeated manual operations. Accurate nutrient placement supports better root development and fertilizer uptake. Adoption of such machinery helps growers meet sustainability certification demands. It also supports corporate supply chains that track environmental performance across contracted farms.

Agricultural Planting and Fertilizing Machinery Market Trends:

Rapid Integration Of Precision Agriculture Technologies Into Planting And Fertilizing Equipment

Manufacturers embed GPS guidance, auto-steering, and section control into new models. Farmers use yield maps and soil data to plan variable-rate seed and fertilizer programs. Controllers adjust seed spacing and nutrient flow on the move. The Agricultural Planting And Fertilizing Machinery Market sees strong demand for machines that connect with farm management software. Cloud platforms store field records and operation logs. Dealers offer remote monitoring and diagnostics for complex equipment. Data-driven decisions reduce overlaps and missed areas. It shifts machinery from standalone tools to integrated nodes in digital farm ecosystems.

- For instance, John Deere’s See & Spray™ Select system demonstrated up to a 77% reduction in non-residual herbicide use in fallow fields through targeted green-on-brown weed detection. In row-crop conditions, the See & Spray™ Ultimate platform typically cuts herbicide use by about two-thirds while maintaining effective weed control.

Growing Adoption Of Automation, Robotics, And Smart Control Systems In Field Operations

Equipment makers introduce semi-autonomous and fully autonomous planters in major grain belts. Smart sensors track seed drop accuracy and row performance in real time. Cameras and lidar support obstruction detection and path correction. The Agricultural Planting and Fertilizing Machinery Market tracks rising interest in robot swarms for small and fragmented plots. Drones assist in aerial fertilizer or micronutrient application in targeted zones. In-cab displays become more intuitive and support multilingual interfaces. Over-the-air software updates upgrade machine capabilities during life cycles. It allows manufacturers to sell performance improvements without hardware replacement.

- For instance, CNH Industrial expanded its autonomy capabilities by integrating Raven Autonomy™ features such as advanced perception sensors, autonomous steering, and the Slingshot® RTK network into its spreader platforms. This setup supports supervised autonomous operation while maintaining sub-inch GPS guidance during fertilizer application.

Shift Toward Low-Emission, Hybrid, And Electrified Machinery Platforms In Farm Fleets

Environmental targets push OEMs to rework powertrains for lower fuel use and emissions. Hybrid systems combine diesel engines with electric drives for better torque management. Battery-electric units emerge for smaller planters and applicators that operate near farms. The Agricultural Planting and Fertilizing Machinery Market begins to see interest in compatibility with biofuels and renewable diesel. Lighter designs reduce soil compaction and fuel consumption. Telematics track engine hours and idle time to optimize service intervals. Governments sometimes link incentives to adoption of cleaner powertrains. It reinforces investment in green research portfolios among leading manufacturers.

Expansion Of Service-Centric, Leasing, And Aftermarket Support Models For Farmers

Many growers prefer flexible access models over outright ownership. OEMs and dealers promote leasing, rental, and pay-per-use plans for high-end planters and applicators. Comprehensive service contracts cover maintenance, calibration, and software updates. The Agricultural Planting and Fertilizing Machinery Market benefits from bundled offerings that include operator training and agronomic advisory. Aftermarket upgrades, retrofit kits, and precision add-ons extend the life of installed machines. Digital platforms manage spare parts ordering and service scheduling. Seasonal support teams help farmers during peak planting and fertilizing windows. It builds long-term loyalty and stabilizes revenue for suppliers.

Agricultural Planting and Fertilizing Machinery Market Challenges Analysis:

High Initial Investment, Ownership Costs, And Limited Financing For Small And Marginal Farmers

Planters, seeders, and precision applicators require significant upfront capital. Many smallholders struggle to justify the cost against modest land holdings. Limited collateral reduces access to formal credit channels. The Agricultural Planting and Fertilizing Machinery Market faces resistance in regions where informal lending dominates. Interest rates can remain high for agricultural borrowers. Operating costs, including fuel, maintenance, and spare parts, add further pressure. Farmers may delay replacement cycles and rely on aging machinery. It slows the pace of technology renewal and reduces penetration of advanced models.

Technical Complexity, Skill Gaps, And Structural Barriers Within Fragmented Farming Systems

Modern machinery uses sophisticated electronics, sensors, and software. Many operators lack training to use advanced features effectively. Poor calibration reduces the benefits of precision systems. The Agricultural Planting and Fertilizing Machinery Market encounters obstacles in areas with fragmented land holdings and irregular field shapes. Large machines may not fit narrow plots or terraced land. Limited dealer networks and weak service infrastructure cause downtime during critical seasons. Availability of genuine parts can be inconsistent in remote areas. It creates hesitation among farmers who fear breakdown risk and costly repairs.

Agricultural Planting and Fertilizing Machinery Market Opportunities:

Rising Potential In Emerging Economies Through Affordable, Compact, And Smallholder-Focused Solutions

Rapid growth in commercial agriculture across Asia, Africa, and Latin America opens new demand. Farmers seek compact planters and multi-purpose applicators suited to smaller fields. The Agricultural Planting and Fertilizing Machinery Market can expand through low-cost models with core precision features. Localized manufacturing and assembly reduce prices and lead times. Shared ownership models and custom hire centers improve access for marginal farmers. Partnerships with microfinance institutions support tailored loan products. It creates strong momentum for inclusive mechanization in underserved regions.

Expansion Of Digital Ecosystems, Data Services, And Sustainable Product Portfolios

Integration of machinery with digital advisory platforms creates bundled value propositions. OEMs can offer agronomy support, weather alerts, and nutrient planning tools linked to machines. The Agricultural Planting and Fertilizing Machinery Market can tap carbon credit programs through equipment that improves input efficiency. Retrofits that enable variable-rate control on legacy machines open a replacement-lite path. Collaboration with fertilizer companies and cooperatives supports bundled input and machinery packages. It positions manufacturers to play a central role in sustainable and data-driven farming transitions.

Agricultural Planting and Fertilizing Machinery Market Segmentation Analysis:

By Type

The Agricultural Planting and Fertilizing Machinery Market divides neatly into planting machinery and fertilizing machinery, each serving distinct stages in the crop cycle. Planting machinery includes seeders, planters, and transplanters that improve seed placement accuracy and uniformity. These machines support higher germination rates and more consistent plant stands. Fertilizing machinery covers spreaders and applicators that deliver nutrients at controlled rates. It supports targeted application, lowers wastage, and enhances nutrient use efficiency. Demand for planting machinery stays strong in row crops and large-scale grain production. Fertilizing machinery gains traction where regulations and input costs push growers toward precision nutrient management.

- For instance, Mahindra & Mahindra introduced the PlantingMaster Paddy 4RO, a mechanized rice transplanter designed to deliver uniform seedling placement with high consistency across varied field conditions. Field demonstrations show that the machine offers far greater precision and uniformity than manual transplanting, improving planting speed and reducing labor requirements.

By Application

By application, the market splits between large farms and small and medium farms, each with specific performance needs and budget limits. Large farms prefer high-capacity, high-horsepower planters and applicators to cover extensive fields within tight windows. These operators focus on advanced electronics, telematics, and automation to optimize fleet use. Small and medium farms prioritize robust, compact, and multi-purpose equipment. It must offer ease of use and low maintenance while still delivering better accuracy than manual methods. Affordability and access to finance play a critical role in this segment. Local dealers, service networks, and shared-use models strongly influence adoption.

- For instance, large farms using the John Deere 1775NT 24-Row Planter have demonstrated high-speed planting at up to 10 mph while maintaining industry-leading singulation accuracy. Field evaluations confirm that its ExactEmerge™ technology sustains near-perfect seed placement across large acreages.

Segmentation:

By Type

- Planting Machinery

- Fertilizing Machinery

By Application

- Large Farms

- Small and Medium Farms

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America And Europe: Mature Mechanization Hubs With Strong Replacement Demand

North America holds around 28% share of the Agricultural Planting and Fertilizing Machinery Market, supported by high mechanization and strong adoption of precision agriculture. Large commercial farms invest heavily in high-capacity planters and advanced fertilizer applicators. It benefits from dense dealer networks, reliable financing, and rapid access to aftermarket services. Europe accounts for nearly 25% share, driven by technology-intensive farming systems and strict environmental regulations. European growers favor precision nutrient application to meet runoff and emission standards. Strong OEM presence and continuous product upgrades sustain replacement demand. Policy incentives for sustainable and low-emission machinery further support sales in both regions.

Asia-Pacific: Fastest-Growing Region With Expanding Commercial Agriculture Base

Asia-Pacific commands the largest regional share at roughly 32%, reflecting rapid expansion of mechanized agriculture in China, India, and Southeast Asia. The Agricultural Planting and Fertilizing Machinery Market in this region benefits from rising food demand and shrinking rural labor pools. Governments roll out subsidy schemes and credit programs that support planter and applicator purchases. Large rice, wheat, and corn belts in China and India create strong demand for mid- to high-horsepower machines. It also sees growing interest in compact and multi-purpose units for fragmented landholdings. Local manufacturing bases in China, India, and Japan help reduce equipment costs. Increasing adoption of precision features in premium segments enhances long-term growth prospects.

South America And Africa: High-Potential Growth Frontiers With Structural Challenges

South America holds around 9% share, anchored by large soy, corn, and sugarcane operations in Brazil and Argentina. Growers in these countries focus on high-productivity planters and fertilizer applicators for extensive row-crop systems. It gains support from export-driven agribusinesses that prioritize yield and operational efficiency. Africa represents nearly 6% share but offers significant long-term potential. Mechanization levels remain low, and many farmers still rely on manual or animal-drawn tools. Governments and development agencies promote affordable, durable machinery for small and medium farms. Growth depends on better rural finance, stronger dealer networks, and expansion of custom hire services across key African markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The Agricultural Planting and Fertilizing Machinery Market remains moderately consolidated, with John Deere, AGCO, CNH Industrial, Kubota, and Mahindra & Mahindra shaping global competition. These companies compete on seeding accuracy, nutrient placement efficiency, reliability, and total cost of ownership. It also faces strong rivalry in precision technologies, telematics, and integrated digital platforms. OEMs invest in R&D for variable-rate control, section shutoff, and automation to protect premium pricing. Regional manufacturers and implement specialists intensify pressure in price-sensitive smallholder segments. Dealer networks, financing support, and aftersales coverage act as major differentiators. Strategic partnerships with input suppliers and digital platforms extend ecosystem reach and deepen customer lock-in.

Recent Developments:

- In May 2025, CNH Industrial announced a new strategic business plan to refresh its entire tractor lineup, spanning from 20 to 700+ horsepower, with progressive introductions set to continue through 2026. In January 2026, the company confirmed plans for a new greenfield manufacturing plant in India, with groundbreaking expected later in the year, to bolster its “Make in India” initiative and focus on high-horsepower tractors and advanced farm machinery.

- In February 2025, John Deere (Deere & Company) introduced new planter technologies for its model year 2026 fleet, featuring active vacuum automation, seed-level sensing, and fertilizer-level sensing. These innovations are designed to maximize efficiency during tight planting windows by automatically adjusting vacuum levels to prevent skips and doubles in real-time. Additionally, in February 2026, the company named five new companies for its 2026 Startup Collaborator Program to accelerate advancements in AI-driven robotics and digital crop intelligence.

- In April 2024, AGCO Corporation officially launched PTx, a new brand representing its global precision agriculture portfolio. This launch followed the completion of a major joint venture with Trimble on April 1, 2024, to form PTx Trimble, which focuses on factory-fit and retrofit precision technologies across mixed fleets. More recently, in August 2025, AGCO debuted the first-ever Fendt stack-fold planter and the next generation of its high-horsepower tractor line at the Farm Progress Show.

Report Coverage:

The research report offers an in-depth analysis based on By Type and By Application. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand will rise as farmers seek higher yields, better input efficiency, and resilience to climate variability.

- Precision planting and variable-rate fertilizing will become standard features on new machinery platforms.

- Automation and semi-autonomous operation will reduce labor pressure during peak planting and fertilizing seasons.

- Emerging markets will drive unit growth through compact, affordable machines tailored for small and medium farms.

- Sustainability rules will favor equipment that limits fertilizer losses, reduces emissions, and protects soil health.

- Digital ecosystems will expand, linking machinery data with agronomy advice and farm management software.

- Flexible financing, leasing, and custom-hire models will widen access to advanced machinery for resource-constrained farmers.

- Retrofit kits will upgrade older fleets with guidance, control, and monitoring functions without full replacement.

- Industry consolidation will strengthen large OEM and dealer networks, while niche players focus on specialized crops.

- Partnerships between machinery firms, seed and fertilizer suppliers, and ag-tech providers will create integrated, outcome-focused solutions.