Agricultural Robots and Mechatronics Market Overview:

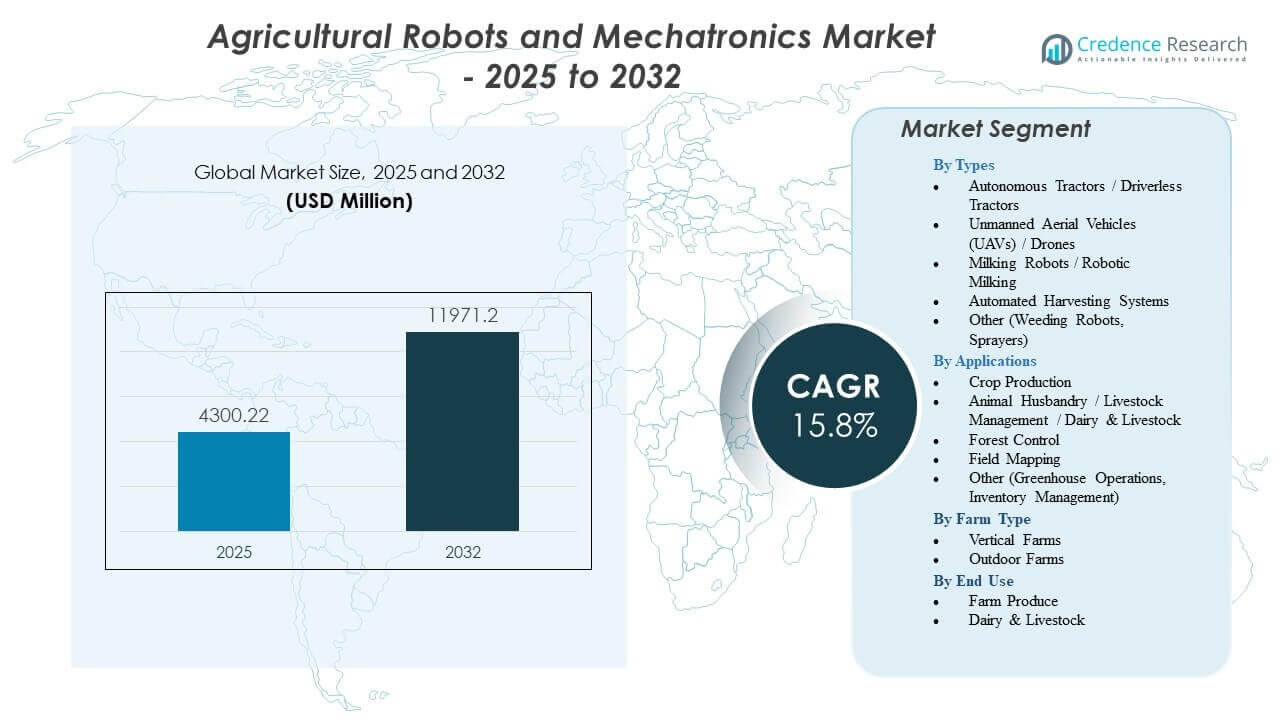

The Agricultural Robots and Mechatronics Market is projected to grow from USD 4300.22 million in 2025 to an estimated USD 11971.2 million by 2032, with a compound annual growth rate (CAGR) of 15.8% from 2025 to 2032.

| RT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Agricultural Robots and Mechatronics Market Size 2025 |

USD 4300.22 million |

| Agricultural Robots and Mechatronics Market, CAGR |

15.8% |

| Agricultural Robots and Mechatronics Market Size 2032 |

USD 11971.2 million |

Agricultural Robots and Mechatronics Market Insights:

- Labor shortages, rising precision-farming needs, and rapid advances in autonomous machinery continue to drive demand for intelligent robotic systems across crop and livestock operations.

- High upfront costs, technical complexity, and limited digital infrastructure in several regions restrain wider deployment, particularly across small and resource-constrained farms.

- North America leads adoption due to strong mechanization and early integration of autonomous tractors and dairy robots, while Europe grows through sustainability-driven investments and greenhouse automation.

- Asia Pacific emerges as the fastest-expanding region, supported by large agricultural bases, rising food demand, and government-backed initiatives promoting drones, field-mapping systems, and compact robotic platforms.

Agricultural Robots and Mechatronics Market Drivers

Rising Labor Shortages and Growing Dependence on Automated Field Operations

The Agricultural Robots and Mechatronics Market grows due to severe labor gaps across major farming regions. Producers rely on robotic platforms to handle repetitive tasks with steady precision. Farmers invest in automated harvesters to reduce crop loss during peak seasons. It supports higher yields by removing delays linked to manual work. Smart sensing systems improve task accuracy during planting and spraying cycles. Rising wages strengthen interest in robotic alternatives across large farms. Adoption grows in regions where migrant labor access continues to fall. It pushes manufacturers to design efficient autonomous units for daily operations.

- For instance, John Deere’s autonomous 8R tractor allows fully driverless tillage and field operations monitored through the Operations Center app, cutting labor hours by double-digit percentages in pilot deployments.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Strong Demand for Precision Agriculture and Data-Driven Decision Systems

Precision tools support farmers who seek targeted input use and higher output quality. Mechatronic systems gather real-time data that strengthens decision accuracy. It helps reduce waste through guided spraying and controlled irrigation. Robots map fields to detect soil variation across crop zones. Farmers use machine-guided routes that improve seeding accuracy across large fields. Better measurement tools reduce fertilizer overuse and protect soil health. Strong interest in digital dashboards drives wider sensor adoption. Producers shift toward robotic systems that provide round-the-clock monitoring.

Growing Adoption of Smart Machinery That Enhances Crop Health Management

Farmers use advanced robots to detect early stress signals in high-value crops. Vision systems identify disease patterns that manual inspection often misses. It allows faster treatment that protects yield quality. Robots support targeted pesticide use that cuts chemical exposure. Smart tractors guide field operations with consistent accuracy. Sensor-based tools help track moisture and nutrient levels across zones. It improves overall farm productivity through reliable precision. Adoption rises in regions with strict rules on crop protection.

Expansion of Autonomous Solutions for Large-Scale and High-Value Farming

Autonomous machines help operators manage vast fields with limited crew support. Robots carry out long tasks with steady performance during peak cycles. It lowers operational load on farmers who manage multiple crops. Smart fleet coordination tools improve field coverage and reduce idle hours. High-value crops benefit from advanced robots that handle delicate harvesting. Automated weed control units support sustainable farm practices. Strong interest from large producers accelerates platform upgrades. Vendors integrate AI modules that enhance navigation across varied terrain.

- For instance, Naïo Technologies’ autonomous weeding robots have logged over 50,000 operational hours in commercial farms, reducing manual weeding labor by up to 80%.

Agricultural Robots and Mechatronics Market Trends

Integration of AI, Vision Technology, and Predictive Analytics Across Platforms

The Agricultural Robots and Mechatronics Market experiences strong movement toward AI-enabled systems. Algorithms support rapid detection of crop anomalies across fields. It enables early intervention through predictive alerts. Advanced cameras capture precise imagery for structured analysis. Machine learning tools refine robot actions with each season. AI-guided tools improve pattern recognition for soil and crop health. Farmers adopt digital twins for field simulation tasks. Platforms expand to support complex multi-crop environments.

Shift Toward Modular and Scalable Robot Designs for Diverse Farm Sizes

Manufacturers release modular robots that adapt to small and large farms. Units support multiple attachments for tilling, spraying, and scouting. It helps farmers upgrade systems without replacing core machinery. Scalable platforms lower investment risks for early adopters. Compact robots gain traction in orchards and greenhouses. Larger systems enter open-field farming that demands high power. Flexible design supports year-round usage across crop cycles. Interest grows in lightweight mechatronics that reduce soil impact.

Rapid Adoption of Robotics in Greenhouse, Orchard, and Specialty Crop Sectors

Specialty crop growers use robots to manage delicate handling needs. Vision-guided harvesting tools support accurate picking for fruit clusters. It reduces damage during peak harvest periods. Greenhouse automation supports plant monitoring and climate checks. Robots assist with spacing, pruning, and nutrient delivery tasks. Orchard platforms handle rugged terrain with stronger mechanical arms. Specialty crop farms adopt automation faster due to rising labor costs. Demand rises for robots that support continuous crop cycles.

- For instance, Harvest CROO Robotics’ strawberry-harvesting robot can pick a plant every 8 seconds using a 16-arm system designed to harvest up to 8 acres per day during active trials.

Growing Use of Collaborative Robots and Fleet-Managed Autonomous Systems

Farmers use collaborative robots to support shared tasks with human workers. Systems improve workflow speed across planting and sorting tasks. It reduces physical strain during long farm hours. Fleet management tools coordinate multiple robots across fields. Connectivity platforms track movement, battery use, and work cycles. Autonomous swarms support weed removal and health scouting. Farmers gain better visibility into operations through cloud dashboards. Interest rises in platforms that communicate across mixed equipment fleets.

- For instance, Autonomous Solutions Inc. (ASI) deploys its Mobius fleet-management software to coordinate multiple autonomous tractors simultaneously, allowing centralized control of speed, routing, and task execution across large fields.

Agricultural Robots and Mechatronics Market Challenges Analysis

High Upfront Costs and Limited Access to Advanced Infrastructure

The Agricultural Robots and Mechatronics Market faces barriers linked to high investment requirements. Farmers hesitate when return cycles extend across several seasons. It pressures smaller farms that lack financing support. Many regions lack stable connectivity for advanced robotic features. Uneven digital adoption slows integration of mechatronic tools. Training needs rise because robots require skilled operators. Maintenance expenses add pressure on low-margin producers. Limited awareness across rural regions slows early adoption.

Technical Complexity, Safety Concerns, and Reliability Issues in Harsh Environments

Robots operate in unpredictable outdoor conditions that strain mechanical parts. Dust, moisture, and uneven soil impact precision systems. It creates reliability challenges for long-duration field use. Safety concerns rise when autonomous units work near human crews. Complex machinery requires trained technicians for repair tasks. Integration with legacy tractors and tools slows smooth adoption. Sensor calibration issues affect task accuracy during peak operations. Farmers seek platforms that handle varied environments with stable performance.

Agricultural Robots and Mechatronics Market Opportunities

Expansion of Autonomous Platforms Into Emerging Regions With Large Farm Bases

The Agricultural Robots and Mechatronics Market sees strong opportunity across regions upgrading their farm systems. Emerging markets pursue automation to improve crop yield stability. It creates space for cost-effective robots tailored to local needs. Vendors design rugged units for tropical and semi-arid zones. Governments support modernization with subsidy programs and training. Large farm operators test autonomous fleets for seasonal operations. Wide crop diversity gives vendors room to introduce specialized robots. Interest grows in analytics platforms that support long-term planning.

Rising Demand for Sustainable Farming and Low-Chemical Production Methods

Demand grows for robots that reduce chemical exposure during crop care. Spot-spraying systems target only affected areas, saving input use. It supports global shifts toward sustainable farming standards. Mechanical weeders reduce reliance on herbicides across large fields. Energy-efficient robots appeal to farms seeking lower emissions. Precision tools help maintain soil health during multi-crop rotations. Adoption grows in farms pursuing certification for clean-label produce. Vendors expand features that enhance sustainable output quality.

Agricultural Robots and Mechatronics Market Segmentation Analysis:

By Types

The Agricultural Robots and Mechatronics Market sees strong traction across multiple robotic platforms that support precision and labor-efficient farming. Autonomous tractors guide field tasks with steady consistency and reduce manual burden across large farms. UAVs improve scouting, spraying, and real-time surveillance for diverse crops. Milking robots strengthen dairy workflows with predictable performance and better hygiene control. Automated harvesting systems support high-value crops that require careful handling. Other platforms, including weeding robots and sprayers, target specific farm pain points where precision tools deliver measurable gains. The type mix gives producers flexibility to adopt systems that match crop scale, budget limits, and labor needs.

By Applications

The Agricultural Robots and Mechatronics Market expands across broad application areas that enhance productivity in field and livestock operations. Crop production leads demand where robots support seeding, weeding, spraying, and harvesting. It improves consistency across wide field zones and lowers input waste. Animal husbandry applications gain momentum as robotic milking and livestock monitoring strengthen farm output and welfare. Forest control uses autonomous units for mapping and vegetation checks. Field mapping tools support early diagnosis of soil and crop stress. Other uses in greenhouse operations and inventory tasks create steady adoption across controlled environments.

- For instance, Lely’s Astronaut A5 robotic milking system performs over 2.5 million milkings per day globally, improving consistency and cow health monitoring across dairy operations.

By Farm Type

The Agricultural Robots and Mechatronics Market supports both vertical and outdoor farms that deploy automation for improved accuracy and lower labor needs. Vertical farms rely on robotic systems for nutrient delivery, plant spacing, and continuous monitoring. It helps maintain predictable yields within controlled structures. Outdoor farms adopt autonomous tractors, drones, and harvesting robots to manage large land areas with fewer workers. Both farm types use mechatronics to cut operating delays and improve long-term efficiency.

- For instance, Iron Ox’s robotic vertical farming platform automates plant movement and nutrient analysis with millimeter-level precision, enabling consistent output in closed-loop growing environments.

By End Use

The Agricultural Robots and Mechatronics Market serves two major end-use groups that adopt automation for higher output stability. Farm produce users focus on robots for planting, spraying, and harvesting across diverse crops. It supports uniform quality and stronger operational control throughout the season. Dairy and livestock users invest in milking robots and automated monitoring systems to improve productivity and animal care. Both end-use groups depend on reliable robotic systems that reduce labor intensity and strengthen daily workflows.

Segmentation:

By Types

- Autonomous Tractors / Driverless Tractors

- Unmanned Aerial Vehicles (UAVs) / Drones

- Milking Robots / Robotic Milking

- Automated Harvesting Systems

- Other (Weeding Robots, Sprayers)

By Applications

- Crop Production

- Animal Husbandry / Livestock Management / Dairy & Livestock

- Forest Control

- Field Mapping

- Other (Greenhouse Operations, Inventory Management)

By Farm Type

- Vertical Farms

- Outdoor Farms

By End Use

- Farm Produce

- Dairy & Livestock

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds a leading share of the Agricultural Robots and Mechatronics Market, supported by rapid adoption of autonomous tractors and advanced dairy automation systems. Strong investment in precision agriculture platforms strengthens regional leadership. It benefits from widespread drone regulation frameworks that support large-scale field automation. High labor shortages across farming hubs push producers toward long-term robotic solutions. Strong collaboration between ag-tech startups and equipment manufacturers accelerates new deployments. The region maintains a market share of 32–34%, supported by consistent technology upgrades.

Europe secures the second-largest share, driven by strong sustainability policies and early adoption of mechatronic tools. The Agricultural Robots and Mechatronics Market grows in the region due to strong investment in dairy robotics and greenhouse automation. It benefits from strict environmental rules that encourage low-chemical and precision farming practices. Major countries integrate robotics into orchard, vineyard, and livestock operations. Workforce scarcity strengthens the shift toward automated harvesting and field-mapping systems. Europe holds a market share of 28–30%, supported by strong regulatory alignment and digital farming uptake.

Asia Pacific emerges as the fastest-growing region, driven by expanding farm mechanization across China, Japan, India, and Southeast Asia. The Agricultural Robots and Mechatronics Market gains traction across small and medium farms that seek scalable robotic systems. It benefits from rising food demand and limited labor availability in high-density agricultural zones. Major economies promote subsidies for smart farming technologies. Drone usage expands quickly due to flexible regulatory reform and strong domestic manufacturing. Asia Pacific holds a market share of 26–28%, while showing the highest growth momentum.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Deere & Company (John Deere)

- AGCO Corporation

- CNH Industrial N.V.

- Lely

- DJI

- Trimble Inc.

- Kubota Corporation

- Naïo Technologies

- Blue River Technology

- Harvest CROO Robotics

- Autonomous Solutions Inc.

- Harvest Automation

- Ecorobotix

- Agrobot

- Yanmar Holdings Co., Ltd.

- GEA Group

- Clearpath Robotics

Competitive Analysis:

The Agricultural Robots and Mechatronics Market features strong competition among global equipment manufacturers, robotics firms, and ag-tech innovators. Companies focus on autonomous navigation, precision spraying, and robotic harvesting solutions that support large-scale adoption. It encourages vendors to expand AI, sensing, and machine-vision capabilities across product lines. Leading players invest in modular platforms that reduce operating costs for medium-size farms. Competitors strengthen aftermarket service networks to address maintenance and training gaps. Mergers and partnerships support faster integration of digital tools, data analytics, and robotic fleets. Firms pursue regional expansion strategies that target high-demand segments such as dairy automation, drone-based mapping, and autonomous tractors.

Recent Developments:

- In January 2026, AGCO Brands secured seven 2026 AE50 Awards from the American Society of Agricultural and Biological Engineers (ASABE) for engineering excellence in products like the Fendt 1000 Vario Gen4 high-horsepower tractor with autonomy-ready capability, the PTx Trimble OutRun autonomy kit, and Precision Planting’s MiraSense seed sensing system, highlighting advancements in autonomous tools and precision agriculture.

- In January 2025, Deere & Company introduced its Next Generation Perception Autonomy Kits, enabling tractors and sprayers to operate driverlessly with advanced camera and Light Detection and Ranging (LIDAR) systems.

- In October 2025, AGCO Corporation announced plans for a limited release of its OutRun autonomous grain cart and tillage system in 2026, compatible with Fendt 900 Series and John Deere tractors, enhancing operator-free operations in field applications.

Report Coverage:

The research report offers an in-depth analysis based on Types, Applications, Farm Type, and End Use. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Agricultural Robots and Mechatronics Market will expand through wider adoption of autonomous machinery across medium and large farms.

- Demand will grow for AI-driven sensing systems that improve field diagnostics and reduce manual decision errors.

- Robotic harvesting platforms will reach higher precision levels that support delicate crop categories.

- Livestock automation will gain traction with increased investment in milking robots and continuous monitoring tools.

- Drone-based operations will strengthen through improved regulations and better imaging capabilities.

- Vertical farms will integrate compact mechatronics that deliver consistent performance within controlled structures.

- Outdoor farms will scale autonomous tractors for long-duration tasks across diverse terrains.

- Greenhouse operators will adopt multifunctional robots that improve plant spacing and routine care.

- Fleet-managed robotic systems will expand through cloud-connected platforms that support real-time task coordination.

- Global adoption will rise as labor shortages intensify and producers pursue higher efficiency with reliable automated systems.