Market Overview

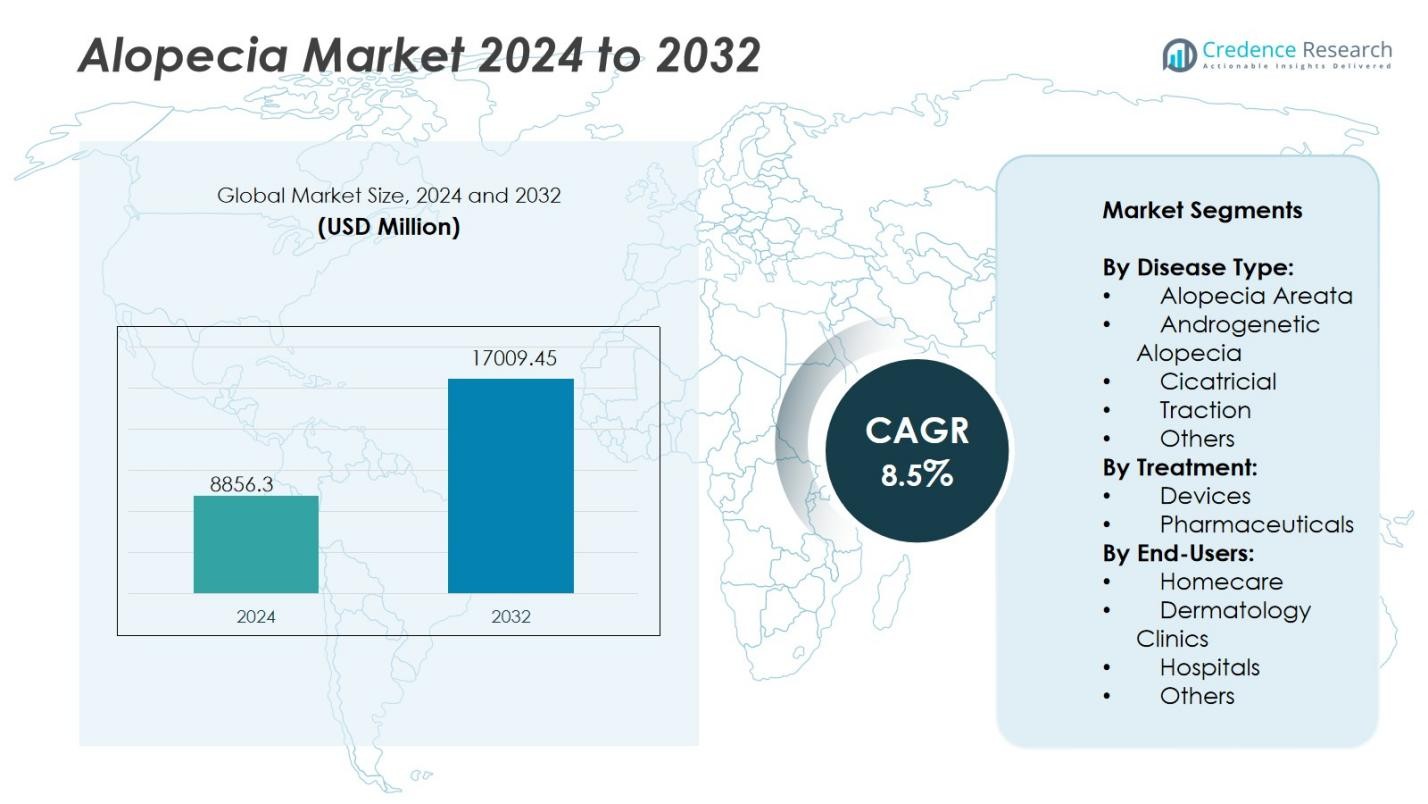

The Global Alopecia Market size was valued at USD 8856.3 million in 2024, and is anticipated to reach USD 17009.45 million by 2032, expanding at a CAGR of 8.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Alopecia Market Size 2024 |

USD 8856.3 Million |

| Alopecia Market, CAGR |

8.5% |

| Alopecia Market Size 2032 |

USD 17009.45 Million |

The competitive landscape of the Alopecia Market is shaped by key players including AbbVie Inc., Allergan, Lupin, Sanofi, Cipla Inc., Bayer AG, Merck & Co. Inc., Eli Lilly and Company, Mylan N.V., GlaxoSmithKline, Abbott, and F. Hoffmann-La Roche Ltd. These companies lead the market through innovations in pharmaceutical therapies, biologics, and non-invasive treatment devices. They are expanding clinical research for JAK inhibitors, stem cell therapies, and peptide-based formulations to enhance treatment efficacy. North America remains the leading region, holding a 38% market share in 2024, supported by advanced healthcare infrastructure, high treatment awareness, and strong R&D activities across the U.S. and Canada.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Global Alopecia Market was valued at USD 8856.3 million in 2024 and is projected to reach USD 45 million by 2032, growing at a CAGR of 8.5% during the forecast period.

- Rising cases of androgenetic alopecia and increasing awareness about early treatment are driving market demand, supported by improved access to dermatological care and advanced treatment options.

- Key trends include growing use of JAK inhibitors, stem cell therapy, and home-use laser devices that provide effective, non-invasive treatment solutions for patients.

- The market is competitive, with leading players such as AbbVie, Allergan, Bayer AG, Merck & Co. Inc., and Sanofi focusing on product innovation, R&D, and strategic collaborations to expand global reach.

- Regionally, North America leads with a 38% market share, followed by Europe at 27% and Asia-Pacific at 22%, while the pharmaceuticals segment holds a dominant 65% share due to high adoption of topical and oral treatments.

Market Segmentation Analysis:

Market Segmentation Analysis:

By Disease Type:

The Alopecia market is segmented into Alopecia Areata, Androgenetic Alopecia, Cicatricial, Traction, and Others. Androgenetic Alopecia dominates the segment, accounting for over 42% of the total market share in 2024. Its strong prevalence among both men and women and the rising adoption of advanced therapeutic options such as minoxidil and finasteride drive segment growth. Increased awareness of early treatment and growing aesthetic concerns further support its dominance. Meanwhile, Alopecia Areata is projected to show notable growth due to expanding R&D in autoimmune treatment approaches.

For instance,Nektar Therapeutics initiated a Phase 2b clinical trial in 2024 for rezpegaldesleukin, a novel biologic targeting immune system dysfunction in severe Alopecia Areata patients.

By Treatment:

Based on treatment, the market is classified into Devices and Pharmaceuticals. The Pharmaceuticals segment leads with a market share 65% in 2024, driven by the wide availability of topical, oral, and injectable formulations. The growing demand for FDA-approved drugs, such as JAK inhibitors and corticosteroids, supports expansion in this segment. Increasing prescription rates from dermatologists and new clinical trials for targeted therapies continue to strengthen pharmaceutical sales. Conversely, the devices segment, including laser therapy systems, is gaining attention for non-invasive and home-based treatment applications.

For instance, Sun Pharma’s oral JAK inhibitor Leqselvi received FDA approval in July 2024 for severe alopecia areata, marking a key development in targeted therapies.

By End Users:

The end-user segmentation includes Homecare, Dermatology Clinics, Hospitals, and Others. Dermatology Clinics dominate with 48% market share in 2024, attributed to specialized diagnostic facilities and professional treatment guidance. Patients prefer clinics for advanced hair restoration procedures, PRP therapies, and laser treatments offering higher efficacy. The availability of experienced dermatologists and customized therapy programs further fuels this dominance. The Homecare segment, however, is expanding rapidly due to the convenience of over-the-counter products, portable laser devices, and rising online retail availability.

Key Growth Drivers

Rising Prevalence of Hair Loss Disorders

The Alopecia market experiences strong growth due to a rising global incidence of hair loss. Factors such as stress, hormonal imbalance, pollution, and aging contribute to the growing number of cases worldwide. Studies show that androgenetic alopecia affects nearly half of men and a quarter of women by midlife. Expanding access to dermatological care and early diagnosis fuels treatment adoption. Increasing awareness campaigns and social acceptance of treatment options further support sustained market expansion.

For instance, Sun Pharmaceutical Industries launched LEQSELVI (deuruxolitinib) in the US in 2025, an FDA-approved oral treatment for severe alopecia areata, with clinical trials showing that nearly one-third of patients achieved almost complete hair regrowth within 24 weeks.

Advancements in Treatment Technologies

Rapid innovation in medical devices and pharmaceuticals continues to drive the Alopecia market. Developments in JAK inhibitors, stem cell therapy, and low-level laser devices improve hair regrowth outcomes and patient experience. Modern technologies enable targeted and less invasive treatments with minimal side effects. The introduction of portable home-use laser caps and AI-guided treatment programs enhances convenience and accessibility. These advancements strengthen consumer trust, accelerating adoption across both clinical and homecare segments.

For instance, Shiseido has successfully developed and clinically validated a hair regenerative therapy using autologous dermal stem cells (S-DSC®), which was launched in Japan in July 2024 to promote hair regrowth in patients with pattern baldness.

Increasing Cosmetic and Psychological Awareness

Rising concern about appearance and confidence loss due to hair thinning boosts market demand. Growing awareness about the psychological effects of alopecia encourages individuals to pursue timely treatment. Media influence and celebrity endorsements normalize discussions about hair loss, driving higher product usage. Expanding social media marketing and aesthetic wellness trends have significantly increased the demand for hair restoration solutions. This shift is especially strong among young professionals seeking visible and non-invasive treatments.

Key Trends & Opportunities

Growing Demand for Personalized Therapies

Personalized medicine presents a major opportunity in the Alopecia market. Advanced genetic and molecular diagnostics help physicians design customized treatment plans for better outcomes. AI-driven analysis of patient profiles enables precision targeting of drugs and devices. This approach reduces side effects, improves satisfaction, and enhances long-term adherence. The trend is prompting pharmaceutical companies and clinics to expand offerings focused on individualized hair restoration programs.

For instance, Alys Pharmaceuticals is advancing ALY-101, an intradermal injectable JAK1 siRNA-lipid conjugate, through a phase 2a trial for Alopecia Areata, marking the first clinical study of a genetic medicine program in dermatology and aiming to address the root causes of autoimmune hair loss.

Expansion of Homecare Treatment Solutions

Consumer preference for convenient, at-home treatments is rapidly expanding. Portable laser devices, topical foams, and prescription-free products are increasingly popular due to affordability and privacy. The rise of e-commerce and digital health platforms makes access to such solutions easier. Smart connected devices that monitor progress are also gaining popularity. This shift toward self-managed care provides manufacturers opportunities to introduce innovative, user-friendly products with proven results.

For instance, Cutera’s AviClear acne device received FDA clearance as a prescription-free laser treatment that reduces acne and future breakout severity without pain mitigation.

Key Challenges

High Cost of Advanced Therapies

High treatment costs remain a major barrier to widespread market adoption. Advanced therapies such as PRP, stem cell procedures, and biologics involve expensive equipment and specialized expertise. In most countries, these procedures lack insurance reimbursement, making them inaccessible for many patients. The financial burden discourages long-term adherence and limits penetration in emerging economies. Reducing costs through technological efficiency and broader coverage is essential for future growth.

Limited Long-Term Treatment Efficacy

Sustaining hair regrowth remains challenging, as many therapies show inconsistent long-term outcomes. Patients often experience relapse once treatments stop, lowering confidence in existing solutions. The unpredictable nature of alopecia, driven by autoimmune and genetic factors, complicates clinical management. Limited understanding of disease mechanisms restricts breakthrough innovation. Continuous research into root causes and multi-modal therapies is needed to improve reliability and patient retention.

Regional Analysis

North America

North America leads the Alopecia market with a market share of 38% in 2024, driven by high disease awareness, advanced healthcare infrastructure, and widespread access to dermatological treatments. The region benefits from strong adoption of FDA-approved drugs, innovative devices, and early integration of biotechnology-based therapies. Increasing consumer spending on aesthetic treatments and the strong presence of key pharmaceutical companies further fuel growth. The U.S. dominates regional sales due to robust R&D funding, supportive reimbursement frameworks, and rising demand for non-invasive and home-use treatment solutions.

Europe

Europe holds a market share of 27% in 2024, supported by strong healthcare systems and growing emphasis on clinical dermatology. Demand for alopecia treatments is rising across the United Kingdom, Germany, France, and Italy due to expanding access to prescription drugs and regenerative therapies. The increasing popularity of cosmetic and minimally invasive procedures also contributes to growth. European pharmaceutical manufacturers are investing heavily in stem cell and peptide-based solutions. Rising aging populations and social acceptance of medical aesthetics further drive the regional market outlook.

Asia-Pacific

The Asia-Pacific region accounts for 22% of the market share in 2024, emerging as the fastest-growing regional segment. Rising disposable incomes, expanding medical tourism, and growing awareness of hair restoration treatments contribute to strong market performance. Countries like China, Japan, South Korea, and India are witnessing increasing adoption of laser therapies, topical formulations, and hair transplant procedures. Local manufacturers are entering the market with cost-effective and herbal-based solutions. Rapid urbanization, coupled with lifestyle-related hair loss and government focus on healthcare modernization, boosts the regional demand.

Latin America

Latin America captures a market share of 8% in 2024, supported by increasing awareness of aesthetic treatments and improving healthcare infrastructure. Brazil and Mexico are key contributors due to growing demand for affordable pharmaceuticals and clinical hair restoration procedures. The rise in disposable incomes and social acceptance of cosmetic care encourage adoption of both professional and at-home solutions. Expanding dermatology clinics and local product availability drive the market’s gradual expansion. Strategic partnerships between global brands and regional distributors are enhancing accessibility across emerging Latin American economies.

Middle East & Africa

The Middle East & Africa region represents a market share of 5% in 2024, with steady growth led by improving healthcare standards and increasing interest in cosmetic enhancement. Wealthy urban centers such as the UAE and Saudi Arabia are major demand hubs for advanced treatment devices and clinical services. Rising hair loss cases due to climatic conditions and dietary factors are driving awareness initiatives. Expanding private healthcare investments and the entry of multinational cosmetic brands strengthen product reach. However, limited affordability and uneven access to specialized care remain key challenges in rural areas.

Market Segmentations:

By Disease Type:

- Alopecia Areata

- Androgenetic Alopecia

- Cicatricial

- Traction

- Others

By Treatment:

By End-Users:

- Homecare

- Dermatology Clinics

- Hospitals

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Alopecia Market includes major players such as AbbVie Inc., Allergan, Lupin, Sanofi, Cipla Inc., Bayer AG, Merck & Co. Inc., Eli Lilly and Company, Mylan N.V., GlaxoSmithKline, Abbott, and F. Hoffmann-La Roche Ltd. These companies focus on developing advanced therapies, including JAK inhibitors, stem cell-based solutions, and biologics aimed at achieving higher treatment efficacy with fewer side effects. Strategic mergers, acquisitions, and product innovations are driving competitive intensity in the market. Firms are investing heavily in research and clinical trials to expand their product pipelines and secure regulatory approvals. Many players are also leveraging digital health platforms and e-commerce networks to enhance patient reach and improve therapy adherence. The increasing emphasis on cost-effective, patient-centric, and non-invasive treatment options further shapes the competition, positioning innovation and affordability as key success factors in the global Alopecia market.

Key Player Analysis

- AbbVie Inc.

- Allergan

- Lupin

- Sanofi

- Cipla Inc.

- Bayer AG

- Merck & Co. Inc.

- Eli Lilly and Company

- Mylan N.V.

- GlaxoSmithKline

- Abbott

- Hoffmann-La Roche Ltd.

Recent Developments

- In July 2025, Sun Pharmaceutical Industries launched Leqselvi (deuruxolitinib) in the United States for adults suffering from severe alopecia areata.

- In October 2025, Pelage Pharmaceuticals secured USD 120 million in Series B funding to advance its topical hair-regrowth drug PP405 targeting androgenetic alopecia.

- In October 2025, Veradermics completed an oversubscribed USD 150 million Series C round to progress VDPHL01, a potential first non-hormonal oral therapy for hair regrowth in both men and women.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Disease Type, Treatment, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Alopecia market will experience steady growth driven by increasing global awareness and early diagnosis.

- Pharmaceutical innovation focusing on JAK inhibitors and stem cell therapies will expand treatment choices.

- Demand for personalized and genetic-based therapies will shape future product development.

- Non-invasive and home-use devices will become preferred solutions for many consumers.

- Digital health platforms will improve patient monitoring and access to dermatological consultations.

- Collaborations between pharmaceutical firms and biotech startups will accelerate R&D efforts.

- Emerging economies will see faster adoption due to growing healthcare investments.

- Focus on gender-neutral treatment options will attract broader consumer segments.

- Companies will emphasize cost-effective formulations to increase accessibility in developing regions.

- Regulatory approvals for new biologics and innovative therapies will strengthen market confidence.