Angola Oil and Gas Upstream Market Overview:

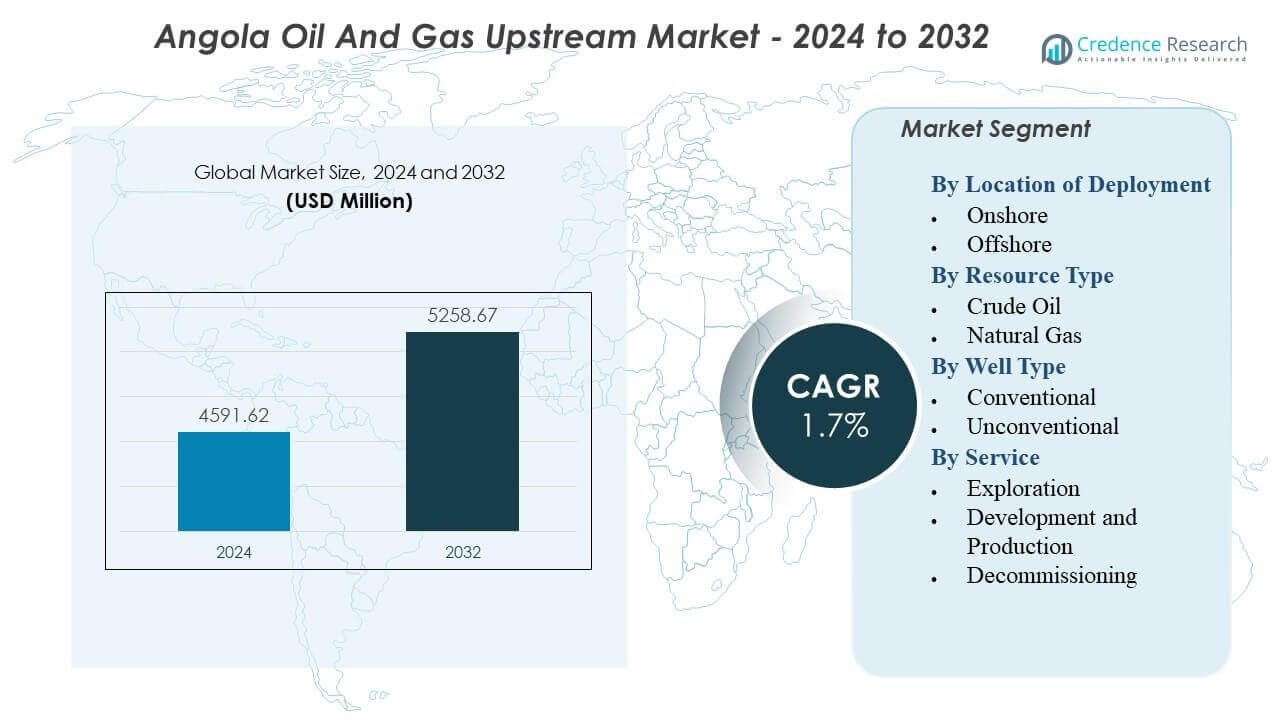

The Angola Oil and Gas Upstream Market is projected to grow from USD 4,591.62 million in 2024 to an estimated USD 5,258.67 million by 2032, with a compound annual growth rate (CAGR) of 1.7% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Angola Oil and Gas Upstream Market Size 2024 |

USD 4,591.62 million |

| Angola Oil and Gas Upstream Market, CAGR |

1.7% |

| Angola Oil and Gas Upstream Market Size 2032 |

USD 5,258.67 million |

Market expansion is driven by rising investments in offshore blocks, first-oil achievements from new FPSOs, and redevelopment programs across mature assets. The government supports upstream activity through improved licensing terms and faster approvals that encourage foreign participation. Operators adopt advanced subsea systems, digital monitoring, and enhanced recovery techniques to sustain production. Growing attention toward gas monetization and flare reduction improves long-term planning. These factors strengthen operational efficiency and build confidence among global investors.

Regional growth is dominated by offshore areas, which benefit from established infrastructure, high-producing reservoirs, and strong participation from major operators. Leading basins continue to deliver stable output and attract sustained capital expenditure due to favorable geology. Emerging regions offer new exploration prospects driven by improved seismic mapping and renewed investor interest. Onshore zones contribute smaller volumes but provide opportunities for lower-cost developments. This distribution highlights Angola’s strong offshore foundation and growing exploration momentum across selected frontier areas.

Angola Oil and Gas Upstream Market Insights:

- The Angola Oil and Gas Upstream Market is projected to grow from USD 4,591.62 million in 2024 to USD 5,258.67 million by 2032, reflecting a 1.7% CAGR during the forecast period.

- Rising offshore investment, new FPSO deployments, improved licensing terms, and stronger deepwater activity drive steady market expansion across key basins.

- Declining output from mature fields, high development costs, regulatory delays, and operational complexity in deepwater environments remain key restraints.

- Offshore regions dominate the market due to stronger reservoir potential, long-life assets, and major operator presence across deepwater and ultra-deepwater zones.

- Emerging frontier areas support new exploration interest, while onshore regions offer lower-cost opportunities for smaller operators seeking shorter project cycles.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Angola Oil and Gas Upstream Market Drivers

Growing Offshore Investments and Redevelopment of Mature Deepwater Assets

The Angola Oil And Gas Upstream Market gains strength from steady offshore spending across deepwater and ultra-deepwater fields. Operators focus on redevelopment plans that lift recovery from aging reservoirs. Companies use subsea upgrades and reservoir modeling to improve well output. The government supports investment through stable licensing terms and faster project approvals. International players expand drilling programs to secure long-term production. Enhanced recovery methods extend field life across strategic offshore clusters. New exploration blocks draw interest from established operators. The market benefits from a robust pipeline of redevelopment work that supports national production goals.

- For instance, TotalEnergies launched the Begonia project in Block 17/06, a five-well subsea tie-back to the Pazflor FPSO, which is engineered to add 30,000 barrels of oil per day to existing production by utilizing enhanced subsea multiphase pumping technology.

Supportive Policy Reforms and Improved Fiscal Framework for Investors

Revised petroleum laws help the upstream segment attract new capital. The government offers flexible contract terms that reduce entry barriers for global companies. Investors show stronger interest in marginal fields where development costs remain lower. Policy clarity helps operators plan multi-year drilling cycles. It creates confidence among consortiums pursuing high-potential offshore targets. Streamlined approvals reduce delays in project execution. Competitive tax structures help drive participation in new bidding rounds. Reforms strengthen investor sentiment and support long-term production stability.

- For instance, following the Presidential Decree 6/18 on marginal fields, Somoil (the largest private Angolan oil company) successfully increased production at the FS and FST onshore associations in the Congo Basin by 25% through a low-cost, multi-well workover program supported by reduced tax royalties.

Rising Exploration Success Across Key Basins Including Kwanza and Lower Congo

Recent exploration results create momentum across frontier zones and proven basins. Operators identify new geological prospects through seismic mapping. Deepwater blocks show higher discovery potential due to favorable reservoir structures. Companies expand appraisal programs to confirm recoverable reserves. Stronger exploration outcomes build confidence among global investors. It supports continued spending across licensed blocks. Multi-client seismic surveys improve basin understanding. Exploration gains help secure future production streams for national output.

Growing Use of Advanced Drilling Technologies and Subsea Production Systems

Technology adoption drives efficiency across complex offshore fields. Operators deploy high-spec rigs to cut drilling time and lower operational risks. Subsea tiebacks help monetize smaller discoveries at competitive cost. Digital tools support reservoir modeling and real-time well monitoring. It improves decision speed across drilling operations. High-pressure systems enhance performance in deeper formations. Remote operations centers guide field optimization. Technology strength raises production reliability and extends uptime across offshore clusters.

Angola Oil and Gas Upstream Market Trends

Shift Toward Deepwater Optimization and Life-Extension Strategies

The Angola Oil And Gas Upstream Market shows growing interest in maximizing output from mature deepwater hubs. Operators invest in asset integrity programs that maintain safe operations. Life-extension plans help delay decommissioning across costly offshore units. Companies improve subsea networks to raise flow efficiency. Digital twins track equipment health and guide maintenance schedules. Optimization programs cut production interruptions across high-value blocks. It supports stable offshore output in competitive market conditions. Long-term rehabilitation programs remain a core trend across mature reservoirs.

- For instance, TotalEnergies implemented a subsea multiphase pumping system at the CLOV field in Block 17, which successfully enabled the tie-back of the Cravo, Lirio, Orquidea, and Violeta fields to a single FPSO, maintaining a production plateau of 160,000 barrels of oil per day.

Expansion of Local Content Programs and Workforce Development

Local content policies shape procurement and workforce strategies. Training centers expand capacity for engineering and marine services. Companies allocate more work to local suppliers in fabrication and logistics. Stronger local engagement helps reduce operating costs for long-cycle projects. Workforce development programs support safer operations offshore. It builds national capabilities in drilling and field support. Local vendors take larger roles in inspection and maintenance activities. Increased participation strengthens domestic industry growth.

- For instance, Sonangol and its partners achieved a significant local content milestone during the Lifua-A project, where 100% of the 1,500-ton wellhead platform jacket was fabricated domestically at the Sonamet yard in Lobito, involving over 1 million man-hours of local labor.

Rising Adoption of Digital Tools for Production Optimization and Asset Monitoring

Digital transformation gains speed across upstream operations. Operators use real-time monitoring tools to guide field decisions. Predictive analytics reduce equipment downtime across remote assets. Digital well planning improves drilling accuracy and cost control. Remote operating centers support safe operations in deepwater blocks. It boosts efficiency in reservoir management. Sensors enhance subsea equipment reliability. Automation improves workflow coordination across complex upstream systems.

Growing Interest in Gas Development and Monetization Pathways

Gas-focused strategies gain traction due to diversification goals. Operators move toward flare reduction programs and gas gathering networks. New gas hubs support future LNG supply options. Appraisal programs target underdeveloped gas-rich structures. Smaller gas fields draw attention due to lower development risks. It supports broader energy transition plans within the sector. Gas reinjection helps stabilize reservoir pressure in producing oil fields. A clear shift toward gas value creation shapes long-term investment trends.

Angola Oil and Gas Upstream Market Challenges Analysis

Declining Production from Mature Fields and Rising Operational Complexity

The Angola Oil And Gas Upstream Market faces production declines across aging offshore wells. Operators struggle with higher water cuts and reduced reservoir pressure. Complex deepwater operations raise maintenance needs and technical risks. High costs hinder rapid redevelopment in marginal fields. It creates pressure on operators to manage resources efficiently. Limited new discoveries slow replacement of depleted reserves. Harsh offshore conditions add to supply chain challenges. Production declines require continuous investment to sustain national output.

Regulatory Delays, Cost Pressures, and Limited Infrastructure Expansion

Operators experience slower progress due to long approval cycles. Delays affect drilling timelines and field redevelopment planning. Cost pressure limits investment appetite in frontier zones. Infrastructure gaps impact efficient movement of equipment and personnel. Skilled workforce shortages raise operational risks during complex tasks. It increases dependency on external service providers. Volatile crude prices challenge long-term project funding. These hurdles reduce the pace of upstream expansion across strategic basins.

Angola Oil and Gas Upstream Market Opportunities

New Licensing Rounds, Frontier Basin Exploration, and Fresh Deepwater Potential

The Angola Oil And Gas Upstream Market sees strong opportunity from new bid rounds targeting fresh acreage. Frontier basins show higher exploration interest due to improved geological data. Operators evaluate new deepwater zones with competitive potential. Successful discoveries can strengthen national reserves and future output. It helps attract investment from leading global companies. Integrated seismic data supports more efficient exploration planning. Partnerships create shared risk across high-cost blocks. Expanding exploration can reshape long-term production prospects.

Gas Commercialization, Subsea Tieback Projects, and Low-Cost Marginal Field Development

Gas development creates gains for energy diversification efforts. Smaller gas discoveries can link to existing infrastructure through tieback routes. Operators use subsea tiebacks to lower development costs for remote fields. Marginal fields offer scope for rapid development with lighter investment. It supports new revenue streams in a stable regulatory environment. Gas-based projects reduce flaring volumes and enhance environmental compliance. Partnerships with global players help accelerate project execution. Strong potential exists for integrated gas value chains across key basins.

Angola Oil and Gas Upstream Market Segmentation Analysis:

By Location of Deployment

The Angola Oil And Gas Upstream Market shows strong activity in offshore zones where deepwater and ultra-deepwater fields drive national output. Offshore blocks attract major operators due to higher reserves and proven production systems. Onshore areas hold smaller reserves yet offer lower development costs and shorter project cycles. It supports balanced growth across mature and emerging reserves.

- For instance, Azule Energy (the BP-Eni joint venture) is currently executing the Agogo Integrated West Hub Development in Block 15/06, which utilizes 23 subsea wells and a massive FPSO to tap into deepwater reserves located at depths of approximately 1,700 meters.

By Resource Type

Crude oil production dominates the Angola Oil And Gas Upstream Market, supported by established offshore fields and continuous redevelopment programs. Operators invest in advanced technologies to sustain crude output from aging reservoirs. Natural gas gains attention due to rising demand for cleaner fuels and national plans to expand gas monetization. It creates long-term opportunities across gathering, processing, and export-focused projects.

- For instance, Chevron, through its subsidiary CABGOC, successfully commissioned the Sanha Lean Gas Connection (SLGC) project, which is designed to provide 480 million standard cubic feet of gas per day to the Angola LNG plant, significantly reducing routine flaring.

By Well Type

Conventional wells maintain the leading share in the Angola Oil And Gas Upstream Market, driven by strong offshore geology and favorable reservoir characteristics. Operators focus on interventions and improved recovery to extend well life. Unconventional prospects remain limited but draw growing interest from smaller players testing new basins. It offers future potential as technology adoption improves.

By Service

Exploration activities support reserve growth in the Angola Oil And Gas Upstream Market, driven by new licensing rounds and improved seismic mapping. Development and production services hold the largest share due to active offshore projects and long-term field programs. Decommissioning grows slowly as mature assets near end-of-life requirements. It encourages planning efforts that balance safety, cost, and regulatory compliance.

Segmentation:

By Location of Deployment

By Resource Type

By Well Type

- Conventional

- Unconventional

By Service

- Exploration

- Development and Production

- Decommissioning

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

The Angola Oil And Gas Upstream Market is dominated by offshore regions, holding nearly 75% of total production share due to strong deepwater and ultra-deepwater activity. These offshore zones attract global operators that deploy high-capacity FPSOs and advanced subsea systems. Strong well productivity and long reservoir life raise investment confidence across key offshore basins. It supports steady output despite natural declines in mature wells. Offshore regions remain the core engine of national hydrocarbon production and continue to secure the bulk of upcoming exploration spending.

Onshore regions account for roughly 15% of the market and focus on lower-cost developments across mature fields. Smaller operators lead most onshore programs where shorter drilling cycles support efficient project planning. Limited reserve size slows large-scale investment, yet new seismic surveys help identify pockets of untapped potential. The government encourages onshore interest through flexible terms for marginal fields. It creates opportunities for operators that target faster turnaround and reduced operational complexity.

Emerging basins, including select frontier zones, represent nearly 10% of the market and hold long-term strategic value. These areas attract attention due to evolving geological insights supported by modern seismic data. Frontier regions carry higher risk yet offer potential to diversify future production beyond mature offshore assets. Investors monitor resource estimates and regulatory clarity before entering early-stage blocks. It positions emerging basins as a future growth pillar when proven reserves expand and development costs stabilize.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- TotalEnergies SE

- Chevron Corporation

- ExxonMobil Corporation

- Azule Energy (BP / Eni Joint Venture)

- Sonangol Pesquisa & Produção (Sonangol P&P)

- Eni SpA

- BP Plc

- Petronas

- Sinopec (E&P Angola)

- Somoil SA

Competitive Analysis:

The Angola Oil And Gas Upstream Market features strong participation from international oil companies that lead major deepwater and ultra-deepwater developments. TotalEnergies, Chevron, ExxonMobil, Azule Energy, and Eni dominate production due to long-term block ownership and strong technical capabilities. These operators focus on high-return offshore zones where engineering strength and capital depth support complex field operations. It drives consistent investment across redevelopment, optimization, and infill drilling programs. National oil company Sonangol P&P maintains a growing role through partnerships and selective asset restructuring. Local companies such as Somoil expand their footprint in marginal fields where operational costs remain manageable. Global players compete through technology, drilling efficiency, subsea expertise, and robust project execution records. New licensing rounds encourage broader participation across exploration blocks. The competitive landscape reflects a blend of established majors, new joint ventures, and domestic operators shaping Angola’s long-term upstream trajectory.

Recent Developments:

- In July 2025, Azule Energy achieved first oil from the Agogo FPSO in Block 15/06 marking a significant new production milestone ahead of schedule and initiating a 15-year contract valued over USD 5 billion with Yinson Production.

- In July 2025, TotalEnergies started production from the BEGONIA offshore project in Angola, marking the first inter-block development with partners including Sonangol E&P and ANPG, adding significant capacity to existing FPSOs.

- In May 2024, Afentra completed its acquisition of a 12% non-operating interest in Block 3/05 and 16% in Block 3/05A from Azule Energy boosting its stakes to 30% and 21.33% respectively, including inherited crude oil stocks.

Report Coverage:

The research report offers an in-depth analysis based on Location of Deployment, Resource Type, Well Type, and Service. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Deepwater and ultra-deepwater assets will guide long-term expansion in the Angola Oil And Gas Upstream Market, supported by sustained operator commitment.

- New licensing rounds will draw stronger interest from global players seeking exploratory potential across key offshore and frontier basins.

- Redevelopment of mature fields will strengthen output stability, aided by improved subsea systems and digital monitoring tools.

- Gas-focused programs will expand as Angola advances monetization plans to diversify its upstream portfolio.

- Local content initiatives will push operators to increase domestic participation in engineering, fabrication, and logistics activities.

- Technology adoption, including predictive analytics and automation, will enhance drilling accuracy and reduce operational interruptions.

- Partnerships between national and international operators will help unlock complex reservoirs and extend field life.

- Onshore opportunities will grow slowly, offering short-cycle developments for smaller operators targeting cost-efficient assets.

- Decommissioning demand will rise as select mature fields approach end-of-life stages, creating a new service segment.

- Emerging basins will gain attention as seismic data improves and investors evaluate prospects for future production streams.