Animal Nutrition Market Overview:

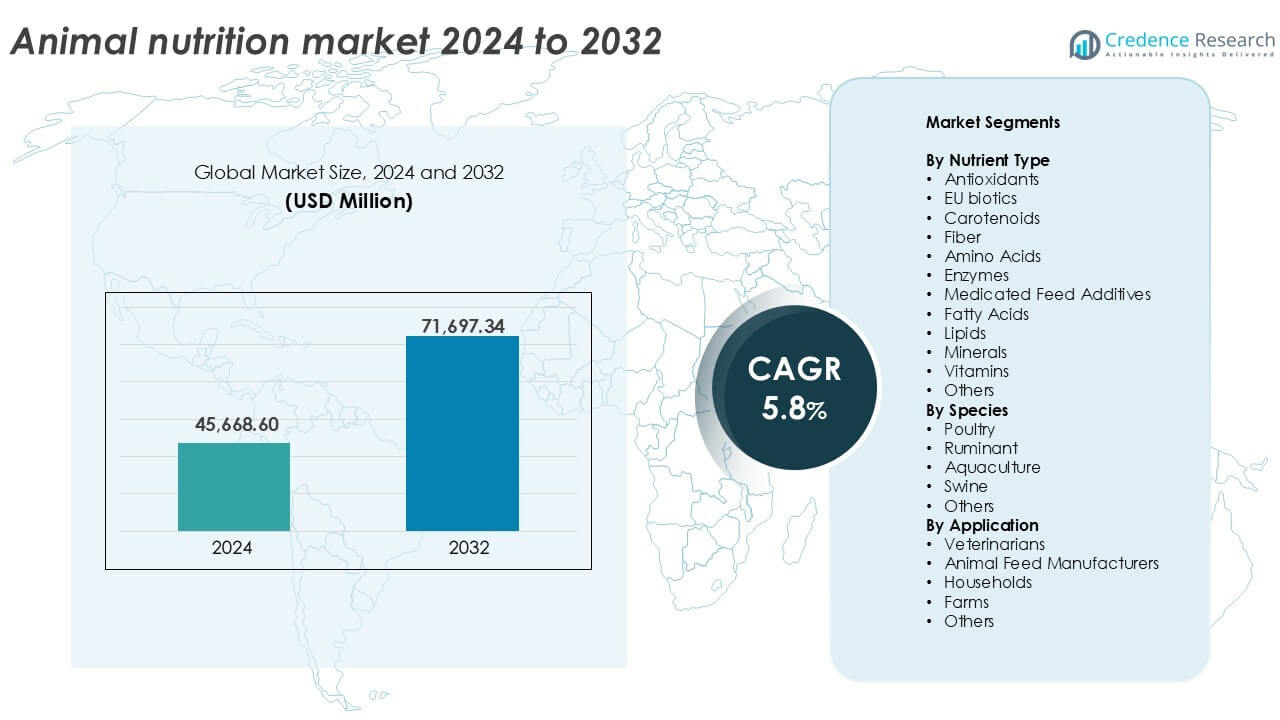

The Animal Nutrition Market size was valued at USD 45,668.60 million in 2024 and is anticipated to reach USD 71,697.34 million by 2032, at a CAGR of 5.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Animal Nutrition Market Size 2024 |

USD 45,668.60 million |

| Animal Nutrition Market, CAGR |

5.8% |

| Animal Nutrition Market Size 2032 |

USD 71,697.34 million |

Animal Nutrition Market Insights

- Rising demand for high-quality meat, dairy, and aquaculture products is driving the need for advanced, nutrient-rich feed solutions across global livestock sectors.

- Precision nutrition, sustainable feed additives, and antibiotic-free formulations are gaining traction as producers focus on animal health, performance, and regulatory compliance.

- Top players like ADM, DSM, Evonik, and Nutreco lead through innovation, partnerships, and expanded product lines, while regional manufacturers target cost-sensitive markets with tailored solutions.

- Asia Pacific dominates the market with 34% share, followed by North America at 27% and Europe at 23%; poultry leads by species with a 42% share, while amino acids hold over 28% of the nutrient type segment due to strong demand in growth-focused feed formulations.

Animal Nutrition Market Segmentation Analysis:

By Nutrient Type

Amino acids dominate the animal nutrition market by nutrient type, accounting for over 28% of the segment share in 2024. High demand for essential amino acids like lysine and methionine in poultry and swine diets drives this growth. These nutrients support muscle growth, feed conversion efficiency, and overall health. Enzymes and vitamins follow due to their roles in digestion and immunity enhancement. The rise of antibiotic-free animal feed boosts the adoption of natural additives such as EU biotics and antioxidants. Growth in functional and fortified feed continues to support the demand for diverse nutrient blends.

- For instance, threonine and tryptophan are increasingly used in swine and poultry diets to improve performance and feed efficiency.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Species

Poultry leads the market by species, capturing around 42% of the total segment share in 2024. Intensive poultry farming and rising broiler meat consumption drive the high use of nutritional products in this sub-segment. Nutrient-dense feed ensures fast weight gain and better egg production. Ruminants follow due to the growing dairy industry and rising milk yield requirements. Swine nutrition gains traction in Asia-Pacific, while aquaculture grows with increasing seafood demand and feed conversion efficiency needs. Each species segment reflects tailored nutrition needs aligned with productivity goals and health management.

- For instance, Evonik’s MetAMINO® DL-methionine (99% purity) is added to swine and poultry feeds to balance amino acids and support growth performance.

By Application

Animal feed manufacturers hold the largest share in the application segment, contributing nearly 47% in 2024. These manufacturers adopt advanced formulations to enhance feed efficiency, growth rates, and disease resistance. Demand rises with industrial livestock farming and mass-scale feed production. Farms also represent a growing segment due to integrated nutrition practices. Veterinarians influence high-value nutrition in therapeutic and preventive care diets. Households contribute to companion animal nutrition growth, especially in developed regions. Overall, the application of animal nutrition expands with rising focus on livestock health, yield optimization, and commercial feed solutions.

Key Growth Drivers

Intensification of Livestock Farming Practices

The shift toward industrial-scale livestock production significantly drives demand for animal nutrition products. High-output systems in poultry, swine, and ruminant farming require precision feed to support rapid growth, efficient weight gain, and improved reproductive performance. With limited grazing space and rising global meat consumption, producers depend on optimized feed formulas to sustain animal health and performance in confined environments. Feed conversion ratio (FCR) improvement remains a top priority, pushing demand for amino acids, enzymes, and tailored vitamin-mineral blends. Countries such as China, India, and Brazil are scaling up animal farming operations, further fueling the uptake of nutrient-dense feed additives. This trend supports long-term investment in advanced animal nutrition technologies and integrated feed management systems.

- For instance, Modern broiler chickens can reach a standard market weight of approximately 2.5 kg in about 35 to 42 days, with efficient feed conversion ratios typically ranging between 1.5 and 1.9 kg of feed per kg of weight gain, underscoring the critical role of precision nutrition and genetics in growth optimization.

Growing Demand for High-Quality Protein Sources

Rising global demand for meat, dairy, and aquaculture products directly supports the growth of the animal nutrition market. As consumer preferences shift toward protein-rich diets, livestock and fish production must meet stricter quality and safety standards. To achieve this, producers increasingly adopt feed additives that enhance growth rates, nutrient absorption, and immunity. High-protein output requires balanced and fortified feed formulas, especially in poultry and aquaculture sectors. The Asia-Pacific region, with expanding middle-class populations and increasing per capita meat consumption, sees rapid growth in this area. Animal nutrition solutions that improve yield quality such as better marbling in meat or higher egg-laying efficiency continue to gain traction among commercial producers aiming to capitalize on market demand.

- For instance, Cargill Animal Nutrition & Health operates in 40 countries and 280 locations, producing more than 62,000 tons of animal feed per day to support livestock and aquaculture nutrition goals.

Shift Toward Preventive Animal Health Management

Preventive health strategies in livestock management are accelerating the use of specialized animal nutrition. Growing regulatory restrictions on antibiotic use in feed have compelled producers to turn to natural alternatives such as prebiotics, probiotics, and enzymes. These help improve gut health, reduce disease incidence, and strengthen the immune system, minimizing veterinary intervention and mortality risks. Animal nutrition plays a central role in enhancing resistance to infections and improving overall wellbeing. Livestock producers now integrate nutrition as part of biosecurity and welfare protocols. This trend is particularly strong in Europe and North America, where consumer awareness around antibiotic-free meat and sustainability continues to shape procurement decisions. Feed companies are responding with functional products tailored to address species-specific health challenges.

Key Trends & Opportunities

Rising Adoption of Precision Nutrition Technologies

Technological advancements in feed formulation and delivery systems are transforming the animal nutrition landscape. Precision nutrition enables accurate, data-driven feed strategies tailored to species, growth stages, and production goals. Tools such as near-infrared spectroscopy (NIRS), micro-dosing systems, and digital herd management platforms help producers measure feed intake, monitor nutrient efficiency, and minimize waste. These technologies offer both economic and environmental benefits by optimizing feed cost while reducing emissions and nutrient runoff. Companies are developing AI-based solutions to customize feed at the individual or group level, especially in large-scale poultry and swine operations. This trend opens opportunities for tailored nutrition products and data-integrated feed services.

- For instance, Trouw Nutrition’s NutriOpt On-site Adviser recorded 356,000 desktop NIR scans in six months, enabling real-time feed quality insights that inform diet formulation and optimise feeding decisions.

Growth in Sustainable and Plant-Based Feed Ingredients

Sustainability concerns are driving interest in alternative feed ingredients with a lower environmental footprint. The use of algae, insect protein, fermented products, and plant-based substitutes is expanding across animal nutrition lines. These ingredients reduce dependency on traditional sources like fishmeal and soybean, which are linked to deforestation and overfishing. Feed manufacturers are investing in novel ingredient sourcing to align with ESG goals and circular economy models. Regulatory support for sustainable agriculture and consumer demand for eco-labeled meat and dairy also encourage adoption. The shift opens opportunities for innovation in nutritional content, digestibility, and species-specific efficacy using green and clean-label feed additives.

Key Challenges

Volatility in Raw Material Prices and Supply Chain Disruptions

The animal nutrition industry faces persistent challenges due to fluctuating prices of feed ingredients such as corn, soybean, and wheat. Supply chain disruptions from geopolitical conflicts, climate-induced crop failures, and trade restrictions often lead to unstable pricing and limited availability of key raw materials. This directly affects the production cost of compound feed and additives, pressuring profit margins for both feed manufacturers and livestock producers. Smaller operations, in particular, struggle to absorb cost fluctuations, which can lead to reduced nutritional input quality. Maintaining consistent supply and pricing remains a critical hurdle in sustaining long-term market growth.

Regulatory Barriers and Stringent Safety Standards

Stringent government regulations on feed additives, especially regarding antibiotic growth promoters and genetically modified organisms (GMOs), pose challenges for manufacturers. Regulatory bodies like the European Food Safety Authority (EFSA) and the U.S. FDA enforce complex approval processes and compliance requirements for new product launches. Navigating these frameworks can delay innovation and increase R&D costs. Furthermore, global variations in permitted ingredients and labeling standards complicate international trade. Companies must continually invest in safety trials, documentation, and certification to enter regulated markets. This creates entry barriers for smaller firms and slows down the rollout of new nutrition solutions.

Regional Analysis

North America

North America accounted for nearly 27% of the global animal nutrition market in 2024. The region benefits from intensive livestock farming, particularly in the U.S., where large-scale poultry, swine, and dairy operations dominate. High feed consumption, rising meat exports, and strong adoption of preventive health supplements support market expansion. Regulatory pressure on antibiotic usage boosts demand for natural feed additives like probiotics and enzymes. Technological advancements in precision feeding and widespread use of compound feed formulations further strengthen market presence. Canada’s growing aquaculture sector and Mexico’s expanding livestock base contribute to continued regional growth.

Europe

Europe held around 23% market share in 2024, driven by stringent regulations on animal welfare and feed safety. The region emphasizes antibiotic-free and organic animal nutrition, leading to rising adoption of EU biotics, fiber, and fortified additives. Countries like Germany, France, and the Netherlands lead in advanced livestock farming systems. Preventive health management and sustainability targets fuel innovation in feed ingredients and formulations. The shift toward plant-based and environmentally friendly feed components supports long-term growth. Aquaculture in Norway and poultry production in Eastern Europe contribute to segment-wise regional diversity and sustained demand for nutritional inputs.

Asia Pacific

Asia Pacific led the animal nutrition market with a 34% share in 2024, driven by large-scale livestock and aquaculture production. China, India, and Southeast Asia account for the bulk of demand due to expanding poultry, swine, and dairy industries. Rising protein consumption, rapid urbanization, and growing disposable incomes support feed volume and quality improvements. Producers in the region invest in fortified feed and enzyme supplements to boost productivity and feed efficiency. Government programs promoting livestock health and biosecurity fuel adoption of nutritional additives. Local manufacturers are increasingly partnering with global firms to enhance product innovation and scale.

Latin America

Latin America captured approximately 9% of the global market in 2024, supported by robust animal protein exports and a growing domestic demand for meat and dairy. Brazil and Argentina lead in cattle and poultry production, using specialized feed to support yield optimization. The region benefits from increasing industrialization of livestock farming and improved access to feed technologies. Swine and poultry segments show strong uptake of amino acids and enzymes. Expansion of aquaculture in Chile and Ecuador boosts demand for high-performance aquatic feed. Continued investments in feed mills and integrated farming systems will sustain market momentum.

Middle East & Africa

The Middle East & Africa region held around 7% share in 2024, reflecting gradual growth in livestock modernization. Countries like South Africa, Saudi Arabia, and Egypt show rising demand for compound feed and veterinary supplements. Regional players are investing in poultry and dairy production to improve food security and reduce import dependence. Climate challenges and limited arable land push demand for efficient feed solutions, including fortified minerals, enzymes, and fatty acids. Government support for local meat and dairy initiatives is encouraging the development of organized feed supply chains. Market growth remains steady with infrastructure improvements and nutritional awareness.

Market Segmentations:

By Nutrient Type

- Antioxidants

- EU biotics

- Carotenoids

- Fiber

- Amino Acids

- Enzymes

- Medicated Feed Additives

- Fatty Acids

- Lipids

- Minerals

- Vitamins

- Others

By Species

- Poultry

- Ruminant

- Aquaculture

- Swine

- Others

By Application

- Veterinarians

- Animal Feed Manufacturers

- Households

- Farms

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the animal nutrition market remains moderately consolidated, with key players focusing on innovation, strategic partnerships, and global expansion to strengthen their market positions. Companies like ADM, DSM, Evonik, and BASF lead through robust product portfolios and investment in feed additive research. These firms focus on amino acids, enzymes, and probiotics to meet rising demand for antibiotic alternatives and performance-enhancing feed solutions. Mid-sized players such as Kemin Industries, Alltech, and Adisseo compete through region-specific formulations and strong distribution networks. Chinese firms like Meihua Group and Global Bio-Chem expand rapidly in amino acid production, catering to cost-sensitive markets. Mergers and acquisitions, such as Nutreco’s partnerships with local producers, support portfolio diversification and market reach. Players are also investing in sustainability by integrating plant-based and precision nutrition technologies. Overall, competition remains driven by innovation, compliance with global feed standards, and the ability to serve diverse species and application requirements.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- CJ Group

- BASF

- Kemin Industries

- Novozymes

- Nutreco

- Novus International

- Global Bio-Chem

- Evonik

- Adisseo

- DSM

- DowDuPont

- Lonza

- Meihua Group

- Alltech

- Sumitomo Chemical

- Biomin

- ADM

Recent Developments

- In August 2025, ADM to launch new feed additive for dairy cows at SPACE 2025. The announcement: at SPACE 2025 (France), ADM will introduce a new feed additive aimed at improving milk yields; also showing “Digest Carb for Ruminants” and “Digestible Protein for Poultry” products/services.

- In August 2025, ADM streamlining soy protein production network. On 29 August 2025, ADM announced it would cease operations at its facility in Bushnell, Illinois, to strengthen efficiency by making more use of its recently recommissioned facility in Decatur, IL, and other sites. The plan is to streamline its soy protein production globally.

- In November 2024, dsm-firmenich’s Animal Nutrition & Health division partnered with Format Solutions, a leading provider of integrated formulation and feed ERP software, to quantify and manage the environmental impact of animal feed.

Report Coverage

The research report offers an in-depth analysis based on Nutrient Type, Species, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for protein-rich animal products will continue to drive feed innovation and nutrient adoption.

- Antibiotic-free and functional feed additives will gain traction across poultry and swine sectors.

- Precision nutrition technologies will support customized feed strategies for species and production stages.

- Sustainable and plant-based feed ingredients will see rising investment and adoption globally.

- Aquaculture nutrition will expand rapidly with increasing seafood demand and intensive farming.

- Regional manufacturers will focus on affordable and efficient feed formulations for local markets.

- Government policies promoting animal health and food security will support market expansion.

- Strategic mergers and partnerships will strengthen global supply chains and product portfolios.

- Digital monitoring and data-driven feed systems will enhance farm productivity and efficiency.

- Environmental regulations and climate-related challenges will influence feed sourcing and sustainability efforts.