Aquatic Herbicides Market Overview:

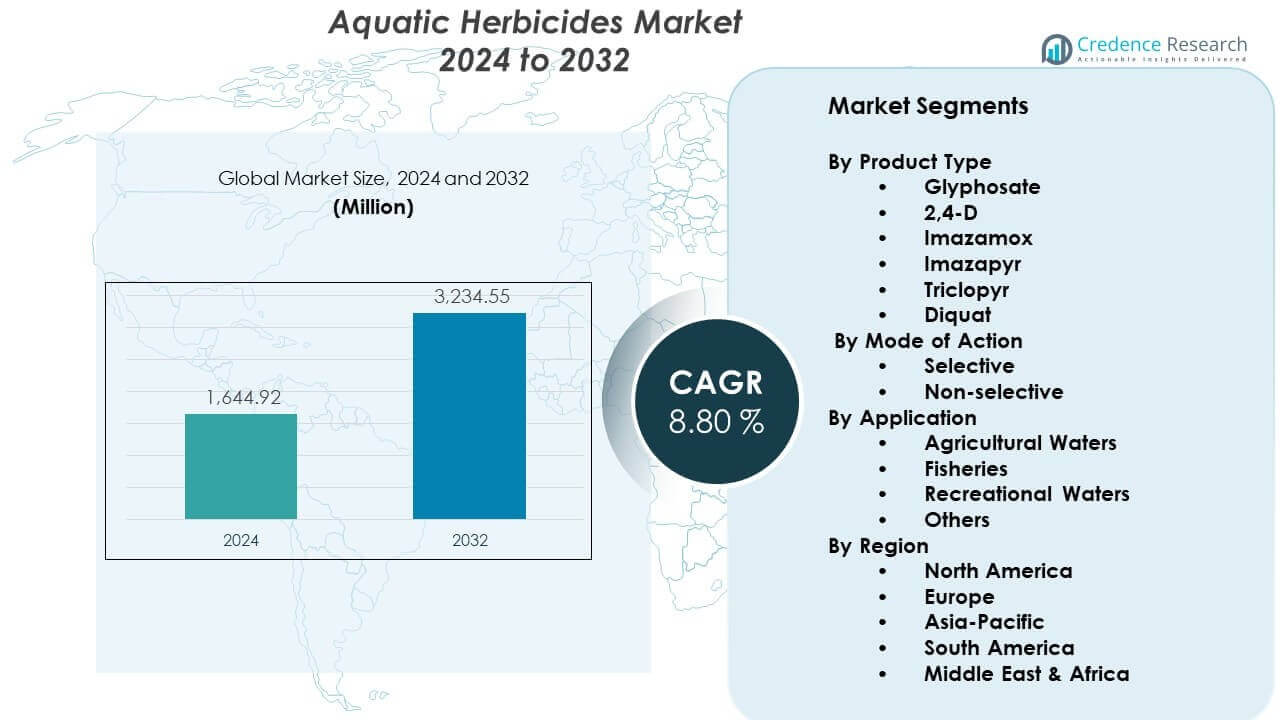

The Aquatic Herbicides Market is projected to grow from USD 1,644.92 million in 2024 to an estimated USD 3,234.55 million by 2032, with a compound annual growth rate (CAGR) of 8.80% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Aquatic Herbicides Market Size 2024 |

USD 1,644.92 million |

| Aquatic Herbicides Market, CAGR |

8.80% |

| Aquatic Herbicides Market Size 2032 |

USD 3,234.55 million |

The market expands due to stricter water management policies, rising awareness of ecological restoration, and the growing impact of invasive plant species on waterways. Manufacturers develop advanced formulations that enhance precision, reduce non-target effects, and support large-scale applications. Public agencies and private operators adopt integrated treatment programs that combine chemical, mechanical, and biological approaches. Improvements in regulatory approvals and higher investments in aquatic ecosystem maintenance further drive product deployment across developed and developing regions.

North America leads the Aquatic Herbicides Market due to established water management practices and strong adoption across municipal and agricultural sectors. Europe follows with increasing lake restoration projects and stringent environmental guidelines. The Asia Pacific region emerges as the fastest-growing market as countries strengthen aquatic weed control programs across rivers, reservoirs, and irrigation systems. Latin America and the Middle East & Africa show rising demand as expanding agriculture and fisheries activities require efficient weed management to maintain water quality and flow.

Aquatic Herbicides Market Insights:

- The Aquatic Herbicides Market is projected to grow from USD 1,644.92 million in 2024 to USD 3,234.55 million by 2032, reflecting a CAGR of 8.80%, driven by rising invasive weed pressure and expanding restoration programs.

- North America holds 40% of the market due to strong regulatory frameworks and recurring treatment programs, followed by Europe at 27% with strict environmental compliance, and Asia-Pacific at 24% supported by large water infrastructure systems.

- Asia-Pacific is the fastest-growing region with a 24% share, driven by expanding irrigation networks, aquaculture growth, and increased investment in reservoir maintenance.

- Selective herbicides account for around 55% of segment share due to their suitability for sensitive ecological zones and regulatory preference across developed regions.

- Non-selective herbicides represent about 45% of the market, supported by their broad-spectrum action and strong use in large restoration projects and dense weed infestations.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Aquatic Herbicides Market Drivers:

Strong Expansion Driven by Rising Invasive Weed Infestations

The Aquatic Herbicides Market grows steadily due to widespread weed outbreaks that limit water flow and reduce ecological balance. Many water bodies face dense vegetation that blocks sunlight penetration and reduces oxygen levels. Operators rely on targeted chemicals to restore water movement and protect aquatic habitats. It helps fisheries maintain stable production and preserve biodiversity. Public authorities support large programs to recover contaminated lakes and canals. Higher awareness among local users pushes demand for safer solutions. Strong adoption occurs in both commercial and municipal sectors. Product improvements enhance application speed and increase treatment success.

Growth Supported by Advancements in Selective and Systemic Herbicide Formulations

Continuous enhancement in selective and systemic products drives the Aquatic Herbicides Market toward wider acceptance. Manufacturers engineer molecules that target weeds without harming fish and desirable plants. Precision performance strengthens confidence among regulators and environmental groups. It encourages broader usage across complex watersheds and multi-species ecosystems. Longer residual action helps operators reduce treatment cycles. Better solubility improves efficiency in shallow and deep water zones. Research programs focus on resistance prevention to safeguard long-term efficacy. Many countries align guidelines to support safer and more compliant application.

- For instance, BASF’s imazapyr-based Habitat® formulation demonstrated greater than 95% suppression of invasive Phragmites in multi-state field trials conducted by NOAA and state agencies, while maintaining low toxicity to aquatic fauna under labeled conditions.

Rising Government Restoration Projects and Strong Public Investment Programs

Large-scale restoration plans fuel the Aquatic Herbicides Market, driven by national and regional policies focused on water quality. Many countries allocate budgets to revive degraded reservoirs and irrigation canals. Public agencies issue guidelines to control weed spread and maintain ecological function. It supports coordinated treatment campaigns across districts and states. Contractors receive long-term service agreements for scheduled interventions. Strong policy pressure encourages preventive action. Communities demand cleaner water for recreation and tourism. Environmental monitoring systems guide treatment selection and improve program outcomes.

- For instance, the Florida Fish and Wildlife Conservation Commission reported over 30,000 acres of invasive aquatic vegetation treated annually using herbicide programs supplied by multiple vendors, including Applied Biochemists and UPL, to restore navigation and protect flood-control infrastructure.

Increasing Adoption Across Agriculture, Hydropower, and Fisheries Infrastructure

Multiple industry sectors strengthen the Aquatic Herbicides Market as operational disruptions intensify. Hydropower plants use treatments to keep intakes free from clogging. Irrigation channels rely on clear pathways to support stable water delivery. It reduces crop losses and increases farm productivity. Fisheries protect breeding grounds from aggressive weed spread. Recreational lakes protect boating routes and tourism revenue. Industrial complexes maintain reservoir performance through structured treatment cycles. Rising cross-sector demand reinforces product development. Long-term asset maintenance strategies keep treatment requirements steady.

Aquatic Herbicides Market Trends:

Growing Shift Toward Eco-Friendly and Low-Residue Aquatic Herbicide Solutions

Environmental expectations influence the Aquatic Herbicides Market through demand for eco-safe products. End users seek formulations with predictable breakdown cycles and lower residue profiles. Regulators prefer treatments that support biodiversity protection goals. It accelerates interest in biologically derived molecules and non-persistent agents. Many suppliers expand portfolios to meet certification criteria. Clear labelling improves trust among community users. Water management firms test nature-compatible blends. Market traction increases for solutions designed for sustainable restoration.

Rising Use of Integrated Aquatic Vegetation Management Programs

Integrated approaches shape the Aquatic Herbicides Market as users combine mechanical, chemical, and biological tools. Many operators design long-term plans to limit recurring infestations. It supports better coordination between municipal teams and private contractors. Data-driven assessments help determine weed density and species impact. Tailored programs reduce excessive product use and improve ecological outcomes. Demand rises for digital mapping tools to support scheduling. Stakeholders value maintenance plans that reduce uncertainty. Broader use of integrated methods improves treatment consistency.

- For instance, the U.S. Army Corps of Engineers (USACE) documented improved vegetation control in the Lewisville Aquatic Ecosystem Project by integrating herbicide treatments with mechanical harvesting and sonar-based mapping, achieving measurable reductions in Hydrilla regrowth across multi-season cycles.

Higher Adoption of Remote Sensing, Drones, and Digital Monitoring Tools

Technology upgrades influence the Aquatic Herbicides Market through stronger analytical capability. Drones capture detailed weed distribution patterns. Satellite monitoring detects seasonal shifts that affect infestation levels. It supports precise treatment routes and reduces waste. Application boats use navigation inputs to enhance accuracy. Digital logs help operators track treatment intervals. Many agencies require monitoring data for compliance. Remote devices reduce manual surveys and lower safety risks.

Growing Interest in Resistance Management and Advanced Weed Control Science

Concerns about resistance shape the Aquatic Herbicides Market with strong focus on diversified treatment strategies. Research groups study genetic changes in invasive plants. It encourages rotation practices that preserve long-term herbicide performance. New chemistries undergo trials to maintain control levels. Technical advisors guide users on sequencing. Cooperative research programs promote data sharing. Training sessions improve field-level understanding. Wider awareness drives disciplined herbicide use.

- For instance, SePRO Corporation and the University of Florida’s Center for Aquatic and Invasive Plants conducted multi-year trials demonstrating that rotation of ProcellaCOR™ EC with Sonar® reduces Hydrilla regrowth and delays herbicide tolerance development, reinforcing best-practice resistance management protocols adopted by state agencies.

Aquatic Herbicides Market Challenges Analysis:

Regulatory Complexity, Environmental Scrutiny, and Compliance Pressure

Strict rules challenge the Aquatic Herbicides Market because many regions require multiple approvals before treatment. Public groups demand evidence of ecological safety. It increases documentation needs and slows rapid response to weed outbreaks. Diverse regulations limit product standardization across regions. Some areas restrict specific chemistries and reduce operator flexibility. Compliance checks raise operational costs. Shifts in future rules create uncertainty for suppliers. Long approval cycles interrupt treatment schedules.

Operational Constraints, Weather Variability, and Skill Limitations

Operational issues affect the Aquatic Herbicides Market when water conditions shift unexpectedly. Rain patterns alter treatment timing and reduce effectiveness. It weakens herbicide concentration when dilution occurs. Remote zones lack trained operators who understand species-based strategies. Debris accumulation blocks access for application boats. Complex infestations require repeated cycles that increase costs. Equipment downtime disrupts maintenance plans. Limited training tools reduce long-term treatment efficiency.

Aquatic Herbicides Market Opportunities:

Expansion of Restoration Contracts, Eco-Safe Technologies, and Long-Term Water Management Programs

Opportunities grow for the Aquatic Herbicides Market as public and private stakeholders expand restoration budgets. Governments support multi-year maintenance contracts that secure supplier revenue. It increases demand for eco-safe formulations. Private lakes and tourism areas invest in scheduled vegetation control. Technology-enabled methods support new service offerings. Training programs help build operator capability. Broader awareness spreads adoption across new regions. Water network upgrades keep demand stable.

Increasing Adoption Across Irrigation Systems, Fisheries, and Hydropower Assets

Infrastructure expansion strengthens opportunities for the Aquatic Herbicides Market across developing and developed regions. Irrigation networks depend on clear channels to maintain crop output. It drives authorities to widen seasonal treatment programs. Fisheries protect breeding habitats from weed dominance. Hydropower plants prevent blockages that hinder turbine performance. Recreational lakes promote weed-free waterways to support tourism. Emerging economies invest in larger reservoirs. Clean water systems increase economic and environmental value.

Aquatic Herbicides Market Segmentation Analysis:

By Product Type

The Aquatic Herbicides Market features a diversified product landscape with glyphosate, 2,4-D, imazamox, imazapyr, triclopyr, and diquat addressing different weed control needs. Glyphosate and 2,4-D dominate large-scale treatments where broad-spectrum activity is required. Imazamox and imazapyr support selective control programs in sensitive ecological zones. Triclopyr performs well against woody or emergent species that restrict water movement. Diquat delivers rapid action, which benefits operators facing urgent blockages. It provides flexibility for users who manage varied infestation levels. Product selection depends on species type, water conditions, and regulatory standards.

- For instance, Nufarm Ltd. reports that its diquat-based Reward® Landscape and Aquatic Herbicide achieves rapid knockdown of submersed weeds such as Hydrilla and Cabomba, with university field trials confirming visible reductions within 48–72 hours following application.

By Mode of Action

Mode of action influences product choice, with selective and non-selective mechanisms guiding weed control strategies. Selective modes interrupt specific plant pathways, enabling precise treatment with reduced ecological disturbance. Non-selective modes deliver full-spectrum control, which benefits areas with mixed-species dominance. It supports operators who require fast results for obstructed water channels. Regulatory preferences often shape adoption trends, especially where environmental protection standards are strict. Mode-of-action rotation reduces resistance risk. Users rely on expert assessment to align treatment method with infestation severity.

By Application

Applications define market growth, spanning agricultural waters, fisheries, recreational waters, and other managed systems. Agricultural waters require consistent weed control to maintain irrigation flow and reduce crop risk. Fisheries rely on clear habitats to protect breeding and feeding zones. It supports operators who monitor vegetation to sustain aquatic health. Recreational waters prioritize safe navigation and tourism appeal. Other applications include reservoirs and industrial water bodies where weed build-up disrupts operations. Diverse needs across these end-use areas drive continuous product refinement.

- For instance, the U.S. Bureau of Reclamation conducts routine aquatic vegetation control in irrigation canals within the Columbia Basin Project, using approved herbicides such as 2,4-D and diquat to manage obstructive weed growth documented to restrict water flow; these treatments support the agency’s broader canal maintenance objectives and are detailed in its operational and environmental compliance reports.

Segmentation:

By Product Type

- Glyphosate

- 2,4-D

- Imazamox

- Imazapyr

- Triclopyr

- Diquat

By Mode of Action

By Application

- Agricultural Waters

- Fisheries

- Recreational Waters

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

North America holds 40% of the Aquatic Herbicides Market, supported by strong investment in lake restoration, irrigation channels, and recreational water systems. Municipal agencies enforce structured weed control programs that guide application standards. It benefits from mature regulatory oversight that supports responsible usage across diverse water bodies. High awareness of invasive plant risks strengthens annual treatment budgets. Hydropower facilities and fisheries rely on consistent vegetation management to maintain performance. Recreational lakes require stable upkeep to support tourism and public activity.

Europe

Europe accounts for 27% of the Aquatic Herbicides Market, shaped by strict environmental policies and coordinated habitat restoration efforts. Countries adopt selective solutions to protect native species while reducing invasive weed pressure. It supports a predictable demand cycle across rivers, canals, and protected wetlands. Tourism-driven economies contribute to ongoing maintenance programs for recreational waters. Compliance regulations influence product formulations and limit certain chemistries. Cross-border river systems encourage regional cooperation in monitoring and treatment.

Asia-Pacific, South America, and Middle East & Africa

Asia-Pacific holds 24% of the Aquatic Herbicides Market and demonstrates strong growth due to expanding irrigation systems and large water-storage infrastructure. Hydropower reservoirs and aquaculture operations depend on structured vegetation control. South America captures 6% of demand, supported by agricultural water networks and fisheries that require clear passages. It experiences rising infestations in warm climates that favor invasive plant spread. The Middle East & Africa account for 3%, driven by reservoir maintenance needs and growing investment in water resource protection. Emerging markets adopt targeted herbicide use to protect infrastructure and support food production.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The Aquatic Herbicides Market features strong competition among global agrochemical leaders and specialized aquatic management firms. Companies focus on product innovation, regulatory alignment, and expanded service capabilities to strengthen their market positions. It enables suppliers to address varied ecological requirements and infestation patterns across regions. Leading players invest in advanced formulations that improve selectivity, reduce residue levels, and support compliance. Partnerships with water management agencies improve access to long-term treatment programs. Firms enhance distribution networks to reach emerging markets that require structured weed control. Competitive strategies emphasize sustainability, resistance management, and integrated water management solutions.

Recent Developments:

- In January 2026, Bayer AG signed a definitive agreement to divest its global Flubendiamide active ingredient business to Tagros Chemicals India. This strategic divestment allows Bayer to streamline its Crop Science portfolio and focus resources on its long-term innovation pipeline of next-generation chemical and biological solutions.

- In August 2024, ADAMA Ltd. reported the continued global rollout of its “differentiated product” portfolio as part of a three-year transformation plan (2024–2026). This strategy includes new registrations and launches designed to meet niche grower needs through innovative formulation technologies, reinforcing its position in the off-patent crop protection market.

Report Coverage:

The research report offers an in-depth analysis based on Product Type, Mode of Action, Application, and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Demand for selective herbicides is expected to increase as regulators promote solutions that protect native vegetation while supporting long-term water quality goals across managed ecosystems.

- Restoration programs for lakes, canals, and reservoirs will strengthen multi-year contract opportunities, creating stable demand for advanced herbicide formulations and integrated vegetation control services.

- Drone platforms and remote sensing tools will gain wider adoption to enhance mapping accuracy, reduce manual surveys, and help operators plan precise treatment routes across diverse water bodies.

- Resistance management strategies will become a priority as users adopt rotation methods and diversified chemistries to maintain effective control over persistent invasive species.

- Hydropower, irrigation, and aquaculture expansion will generate stronger application needs, encouraging operators to maintain clear waterways for energy output, crop yield, and aquatic productivity.

- Regulatory authorities will focus on safer formulations that limit residue levels, driving further innovation in low-toxicity products adapted for sensitive ecological zones.

- Rising aquaculture investments will accelerate vegetation management requirements, supporting habitat protection and the operational needs of commercial fisheries.

- Public investment in water conservation and ecological restoration will reinforce long-term growth by encouraging structured vegetation monitoring and treatment programs.

- Data-driven mapping tools, including AI-based modelling, will streamline treatment decisions and improve forecasting for seasonal weed outbreaks across complex water systems.

- Global awareness of invasive aquatic species will drive innovation cycles, supporting new herbicide research, improved product delivery methods, and sustainable application practices.