Artificial Intelligence In Diagnostics Market Overview:

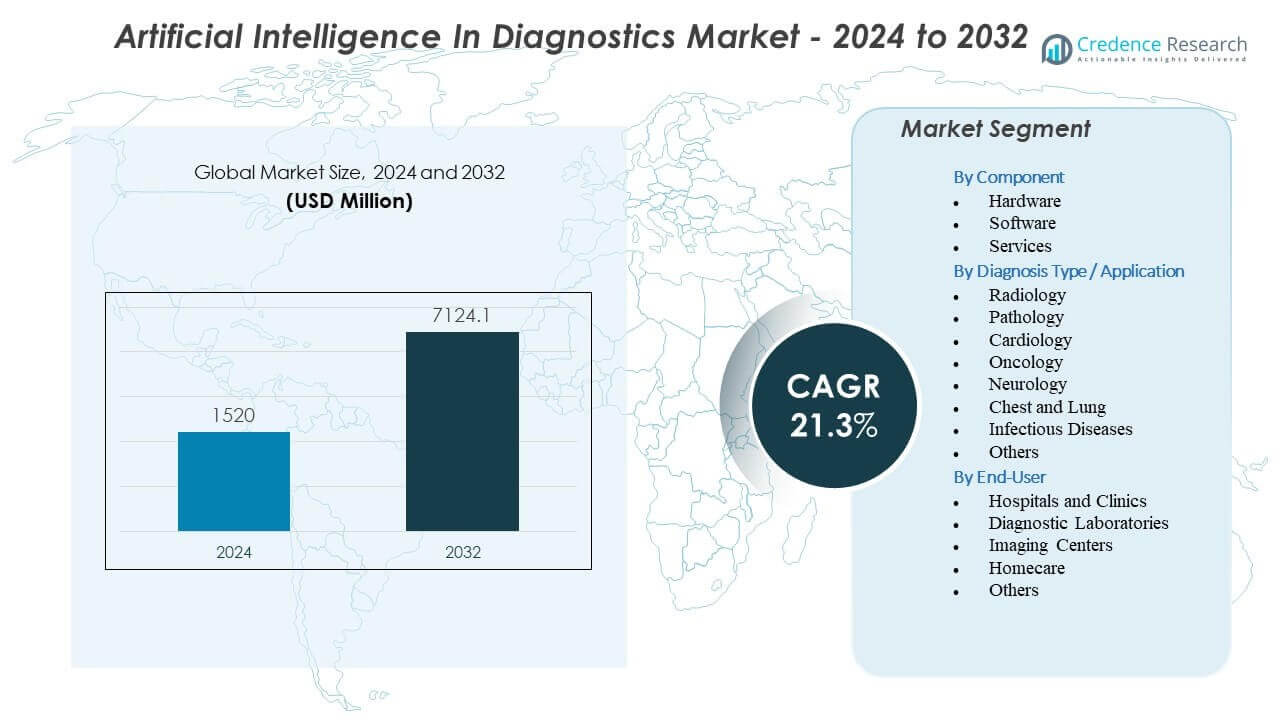

The Artificial Intelligence In Diagnostics Market is projected to grow from USD 1520 million in 2024 to an estimated USD 7124.1 million by 2032, with a compound annual growth rate (CAGR) of 21.3% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Artificial Intelligence In Diagnostics Market Size 2024 |

USD 1520 million |

| Artificial Intelligence In Diagnostics Market, CAGR |

21.3% |

| Artificial Intelligence In Diagnostics Market Size 2032 |

USD 7124.1 million |

Market drivers emerge from the rising demand for faster and more precise diagnostic workflows, supported by AI’s ability to detect subtle abnormalities across radiology, pathology, oncology, neurology, and cardiology use cases. Health systems adopt AI tools to reduce clinical workload and improve consistency across specialist teams. Developers create multimodal algorithms that combine imaging, clinical records, and molecular data to enhance diagnostic clarity. Hospitals invest in workflow automation that speeds triage for stroke and cardiac emergencies. Regulatory agencies support growth by approving well-validated diagnostic models. The market benefits from AI’s ability to deliver early alerts that improve clinical outcomes.

Regionally, North America leads due to mature digital infrastructure, strong regulatory support, and high adoption of AI-enabled diagnostic platforms. Europe follows with expanding clinical digitization and widespread integration of AI across pathology and radiology networks. Asia Pacific emerges as the fastest-growing region, driven by expanding healthcare systems, large patient volumes, and government-backed AI innovation programs. Latin America gains traction through increasing adoption in private hospitals seeking workflow optimization. The Middle East and Africa demonstrate gradual growth as providers modernize imaging infrastructure and explore AI to overcome specialist shortages.

Artificial Intelligence In Diagnostics Market Insights:

- The Artificial Intelligence In Diagnostics Market is projected to grow from USD 1520 million in 2024 to USD 7124.1 million by 2032, supported by a CAGR of 21.3%, reflecting rapid adoption across clinical settings.

- Rising demand for faster and more precise diagnostic workflows drives strong uptake of AI tools that enhance detection accuracy across radiology, pathology, oncology, neurology, and cardiology.

- Market restraints include limited interoperability, concerns around clinical validation, and the need for high-quality annotated datasets to ensure reliable performance across populations.

- North America leads due to advanced digital infrastructure and strong regulatory support for clinical AI, while Europe grows through widespread adoption in clinical imaging and pathology networks.

- Asia Pacific emerges as the fastest-expanding region as healthcare systems scale AI-enabled diagnostics to manage high patient volumes and strengthen early disease detection.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Artificial Intelligence In Diagnostics Market Drivers

Growing Clinical Need For Faster And More Accurate Diagnostic Decision Support

The Artificial Intelligence In Diagnostics Market gains strong momentum due to rising demand for high-precision clinical assessments across major disease areas. Hospitals depend on AI tools to reduce diagnostic variation and improve early disease detection. Radiology, pathology, and cardiology teams integrate supervised models to cut review time for complex scans. Health systems also prioritize AI to support overwhelmed diagnostic teams facing higher patient loads. Vendors design platforms to help clinicians improve workflow efficiency. Physicians trust these tools for second-read support in routine and emergency settings. The market benefits from advances in multimodal data models that raise diagnostic confidence.

- For instance, Lunit collaborated with Microsoft in July 2025 to deploy Azure-based AI models that enable radiologists to fine-tune cancer detection algorithms using site-specific data, a capability that has demonstrated up to a 20% reduction in false-positive findings in clinical environments.

Expanding Integration Of AI Algorithms Across Imaging Modalities And Clinical Specialties

Rapid integration of algorithms across CT, MRI, X-ray, and ultrasound pushes growth in the Artificial Intelligence In Diagnostics Market. Providers rely on automated tools to identify patterns linked to cancer, stroke, cardiac disease, and respiratory disorders. AI raises detection accuracy for small or complex lesions that are hard to identify manually. Hospitals invest in AI to reduce turnaround time for reports. Developers focus on clinically validated models approved across key regulatory markets. Imaging centers use these solutions to handle rising scan volumes. Clinicians view them as essential tools that help limit interpretation errors. Demand grows due to their ability to support targeted clinical decisions.

Rising Use Of Predictive And Risk-Stratification Models Across High-Burden Disease Areas

AI supports predictive insights that help clinicians manage disease progression and treatment response. The Artificial Intelligence In Diagnostics Market expands due to growing use of predictive tools for oncology, neurology, and cardiovascular care. Providers deploy models that score patient risk and highlight critical cases with greater precision. Hospitals want these insights to lower mortality and improve outcomes. Development teams build models that analyze historical and real-time data streams. Health systems use these capabilities to support proactive intervention for high-risk groups. Clinicians value risk scores that align with clinical guidelines. Predictive analytics strengthens decision support across entire diagnostic pathways.

Stronger Regulatory Support And Faster Approval Cycles For Clinical-Grade AI Tools

Global regulators support safe adoption of clinical AI through clear validation pathways. Faster approvals accelerate deployments across the Artificial Intelligence In Diagnostics Market. Health agencies push evidence-based standards that improve trust among hospitals. Vendors design transparent models to meet regulatory expectations. Hospitals adopt approved tools to strengthen quality across imaging and clinical workflow areas. These policies help expand AI access across public and private providers. Developers benefit from greater clarity during product design. The environment encourages broader investment in high-precision diagnostic platforms.

- For instance, the strategic $1 billion co-innovation lab announced by NVIDIA and Eli Lilly in January 2026 focuses on developing FDA-compliant “dry lab” models built on the BioNeMo platform to accelerate the validation of diagnostic biomarkers for neurodegenerative diseases.

Artificial Intelligence In Diagnostics Market Trends

Growing Shift Toward Multimodal And Cross-Disciplinary Diagnostic AI Platforms

The Artificial Intelligence In Diagnostics Market sees a shift toward platforms that combine imaging, pathology slides, genomics, and clinical records. Vendors design systems that unify data types into single diagnostic workflows. Hospitals want these platforms to simplify complex reviews. Multimodal insights improve diagnostic accuracy in cancer and neurological disorders. Clinicians gain deeper visibility into disease patterns. Development teams build AI tools that coordinate results from multiple specialties. This trend supports integrated care pathways across health systems. Adoption rises due to strong demand for consolidated diagnostic intelligence.

- For instance, Tempus has leveraged its Library platform to integrate clinical data from over 5.5 million de-identified patient records with molecular data; this multimodal approach allowed for the identification of actionable genetic alterations in 30% more patients compared to traditional single-modality testing in certain oncology cohorts.

Expansion Of Real-Time AI Triage And Emergency Response Support Tools

Real-time AI triage tools gain traction due to rising emergency case loads across stroke, trauma, and cardiac events. The Artificial Intelligence In Diagnostics Market benefits from fast alert systems that flag critical findings. Hospitals deploy AI to shorten response time and improve patient outcomes. Developers focus on real-time inference models ready for high-pressure care units. Platforms route high-risk cases to specialists without delay. Emergency teams trust these tools to support early intervention. Demand rises due to need for instant review across large imaging queues. Market growth accelerates through wider installation across major hospitals.

- For instance, Viz.ai demonstrated that its Viz LVO (Large Vessel Occlusion) platform reduced the time from initial hospital arrival to the start of neurointerventional treatment by an average of 66 minutes, facilitating a 2.5x increase in the number of patients receiving timely mechanical thrombectomies.

Increased Adoption Of Cloud-Based Diagnostic AI And Scalable Deployment Models

Cloud deployment gains favor due to lower hardware needs and easier scalability. The Artificial Intelligence In Diagnostics Market benefits from global cloud ecosystems that support remote reading and continuous updates. Providers prefer cloud platforms for faster deployment across multisite networks. Vendors design lightweight clients that integrate easily with imaging systems. Cloud tools support rapid model upgrades and broader collaboration between clinical teams. Health systems use these platforms to expand access for rural and remote sites. Demand increases due to better cost control and improved uptime. Cloud models strengthen long-term AI adoption.

Growing Use Of Large-Scale Foundation Models Trained On Medical Data

Foundation models trained on extensive medical datasets begin transforming diagnostic workflows. The Artificial Intelligence In Diagnostics Market benefits from models capable of interpreting varied imaging types with higher accuracy. These systems reduce training time for new applications. Hospitals seek models that adapt to new disease indications. Developers focus on federated learning frameworks that protect patient data. Clinicians value improved generalization across diverse patient populations. Health systems rely on these models for consistent performance across sites. The trend encourages broader integration of AI in routine diagnostics.

Artificial Intelligence In Diagnostics Market Challenges Analysis

Complex Regulatory, Ethical, And Validation Barriers Limiting Scaled Adoption Across Clinical Settings

The Artificial Intelligence In Diagnostics Market faces challenges tied to strict regulatory evaluation and clinical validation needs. Developers must demonstrate safety and explainability for approval. Hospitals demand evidence that models perform well across varied populations. Vendors struggle with access to large annotated datasets. Ethical concerns arise when models show bias. Clinicians express caution when model outputs conflict with clinical judgment. Integration teams also address concerns about data privacy. These barriers slow adoption across sensitive clinical workflows. The market works to improve transparency to build greater trust.

Workforce Adaptation, Technical Integration Issues, And Limited Interoperability Across Hospital Systems

Hospitals face difficulty training staff to use new AI tools at scale. The Artificial Intelligence In Diagnostics Market also encounters integration constraints across legacy imaging systems. IT teams must manage compatibility gaps, cybersecurity risks, and long deployment cycles. Clinicians want seamless interfaces that avoid workflow disruption. Vendors face hurdles aligning AI outputs with clinical reporting formats. Limited interoperability slows broad adoption across multisite networks. Health systems attempt to manage change while maintaining clinical productivity. These issues create friction that reduces the pace of market expansion.

Market Opportunities

Rising Demand For Precision Diagnostics And Personalized Medicine Across Major Disease Areas

The Artificial Intelligence In Diagnostics Market holds strong opportunities due to rapid growth in precision medicine programs. Hospitals want tools that support individualized risk scoring and therapy selection. Vendors build models that link imaging findings with genomic and molecular data. Clinicians value insights that guide tailored treatment decisions. Health systems expand investments in AI to support oncology, cardiology, and neurology pathways. Predictive features open new revenue opportunities for developers. The shift toward personalized care increases demand for advanced AI capabilities. This trend supports long-term market expansion.

Expansion Potential Across Underserved Regions, Remote Networks, And Digital-First Healthcare Models

Emerging markets present significant growth opportunities for the Artificial Intelligence In Diagnostics Market. Providers use AI to address shortages in specialist staff. Cloud-based tools help extend diagnostic support into remote clinics. Governments invest in digital health infrastructure to improve access. Vendors target these regions with scalable subscription models. Clinicians in underserved areas gain faster access to expert-level diagnostic support. Health systems rely on AI to reduce care delays. These dynamics create strong conditions for market acceleration across global regions.

Artificial Intelligence In Diagnostics Market Segmentation Analysis:

By Component Analysis

The Artificial Intelligence In Diagnostics Market advances through strong performance across hardware, software, and services. Hardware supports high-speed processing for imaging and sensor-driven diagnostics used in hospitals and labs. Software leads adoption due to powerful algorithms that improve detection accuracy and streamline clinical workflows. Services grow steadily because providers need integration support, staff training, and model validation to ensure consistent use across departments. It strengthens reliability and enables smooth deployment for both large and mid-size healthcare networks.

- For instance, NVIDIA has advanced diagnostic hardware through its Clara Holoscan platform; when paired with RTX A6000 GPUs, medical facilities can reach processing speeds exceeding 600 frames per second for real-time ultrasound AI inference, delivering a 10x increase in throughput compared with earlier hardware architectures.

By Diagnosis Type / Application Analysis

Diagnostic growth spans radiology, pathology, cardiology, oncology, neurology, chest and lung assessments, infectious diseases, and other specialty areas. The Artificial Intelligence In Diagnostics Market gains traction where AI improves visibility into complex patterns across CT, MRI, X-ray, digital slides, and ECG interpretations. Radiology and neurology remain strong due to high imaging volume and demand for rapid critical-case detection. Pathology benefits from slide-scanning automation, while oncology uses AI for tumor classification and monitoring. It supports fast and consistent evaluations across diverse clinical conditions.

By End-User Analysis

Hospitals and clinics dominate adoption because they manage large patient loads and require accurate, fast diagnostic tools. The Artificial Intelligence In Diagnostics Market expands across diagnostic laboratories and imaging centers that rely on AI to reduce manual workload and improve reporting speed. Homecare applications rise with connected devices and remote diagnostic tools that support early detection. Other users such as research institutes apply AI to develop new diagnostic pathways. It increases adoption across both centralized and decentralized care settings.

- For instance, Mayo Clinic integrated an AI-based ECG screening tool across its hospital network to identify patients at risk of Left Ventricular Systolic Dysfunction (LVSD); the system analyzed more than 100,000 patients and achieved an AUC of 0.93, enabling clinicians to identify twice as many high-risk individuals compared with standard care protocols.

Segmentation:

By Component

- Hardware

- Software

- Services

By Diagnosis Type / Application

- Radiology

- Pathology

- Cardiology

- Oncology

- Neurology

- Chest and Lung

- Infectious Diseases

- Others

By End-User

- Hospitals and Clinics

- Diagnostic Laboratories

- Imaging Centers

- Homecare

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the dominant share of the Artificial Intelligence In Diagnostics Market with an estimated 40–58%, driven by strong digital health adoption, advanced imaging infrastructure, and high investment in AI development. Hospitals integrate AI tools to support radiology, pathology, oncology, and neurology workflows across large patient volumes. Leading companies expand FDA-cleared models that improve diagnostic accuracy and reduce delays in care delivery. Research institutions support innovation through clinical trials and validation studies. It benefits from mature reimbursement pathways that support AI-enabled diagnostics. Continuous technology upgrades strengthen market leadership across the region.

Europe maintains the second-largest share with 25–30%, supported by strict quality standards, a strong clinical research ecosystem, and rapid expansion of AI-enabled health platforms. Healthcare providers adopt AI to improve workflow efficiency while meeting regulatory expectations for clinical safety. Government-led digital transformation programs accelerate integration across imaging centers and diagnostic laboratories. Vendors collaborate with academic hospitals to refine AI performance for varied population groups. It gains momentum through rising funding for precision diagnostics and cross-border health data initiatives. Adoption increases as providers prioritize automation for high-volume imaging workloads.

Asia-Pacific emerges as the fastest-growing region with a rising share of 15–20%, driven by expanding healthcare infrastructure, large patient pools, and rapid demand for automated diagnostic tools. China, Japan, South Korea, and India increase investment in medical AI to reduce workforce shortages and improve access to specialist-level diagnostics. Imaging centers and hospitals adopt cloud-based platforms that support scalable deployment. Startups and global vendors accelerate development through partnerships with leading medical institutions. It grows faster due to strong government support for AI adoption in digital health programs. Latin America and the Middle East & Africa hold smaller shares but show growing interest in remote diagnostics and scalable AI models.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Siemens Healthineers

- GE Healthcare

- NVIDIA Corporation

- Aidoc

- Google (Alphabet Inc.)

- Microsoft

- Digital Diagnostics Inc.

- Zebra Medical Vision

- Vuno Inc.

- PathAI

- Riverain Technologies

- IBM Watson Health

- AliveCor Inc.

- Imagen Technologies

- IDx Technologies Inc.

- Neural Analytics

Competitive Analysis:

The Artificial Intelligence In Diagnostics Market features strong competition among established medical technology companies, AI platform providers, and specialized diagnostic innovators. Global leaders such as Siemens Healthineers, GE Healthcare, NVIDIA, Google, Microsoft, and IBM expand portfolios with advanced imaging algorithms, cloud-based analytics, and clinical decision-support tools. These companies invest heavily in model accuracy, interoperability, and regulatory approvals to strengthen presence across hospitals and diagnostic networks. Startups including Aidoc, PathAI, Vuno, Digital Diagnostics, Riverain, and Imagen Technologies focus on narrow clinical domains such as oncology, neurology, cardiology, and chest analysis. It gains competitive depth through FDA-cleared solutions, rapid deployment cycles, and strong clinical partnerships. Vendors compete on algorithm performance, workflow integration, and scalability across diverse clinical environments. The landscape continues to evolve with mergers, collaborations, and innovation driven by demand for precise, fast, and reliable AI-enabled diagnostics.

Recent Developments:

- In January NVIDIA Corporation and Eli Lilly announced a co-innovation AI lab 2026, investing up to $1 billion over five years to advance drug discovery, including applications relevant to diagnostics through AI model development.

- In December 2025, Aidoc announced strategic partnerships with Cercare Medical and Circle CVI integrating advanced MR Perfusion and automated ASPECTS scoring into its aiOS™ platform to enhance neurosciences diagnostics for stroke care.

- In September 2025, Siemens Healthineers partnered with Aiforia Technologies to expand AI-driven solutions for digital pathology across European diagnostic labs through co-marketing and joint sales efforts.

- In July 2025, Microsoft collaborated with Lunit to advance AI-driven cancer diagnosis by co-developing customizable AI models on Azure and workflow automation tools for radiology.

Report Coverage:

The research report offers an in-depth analysis based on Component, Diagnosis Type / Application, End-User, and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Growing adoption of AI-driven imaging and pathology tools will enhance diagnostic speed and precision across high-burden diseases.

- Expansion of cloud-based diagnostic platforms will support scalable deployments across multisite hospital networks.

- Integration of multimodal data models will strengthen decision-support capabilities across oncology, neurology, and cardiology.

- Wider regulatory support will accelerate clinical validation and expand access to approved AI tools.

- Increased collaboration between technology firms and healthcare providers will improve workflow automation.

- Growth in smart hospital infrastructure will drive higher demand for real-time diagnostic insights.

- Rapid innovation in foundation models will broaden AI use across complex diagnostic scenarios.

- Rising integration of remote monitoring tools will support early detection outside traditional care settings.

- Expansion into emerging markets will increase global penetration of AI-based diagnostics.

- Strong investment in precision medicine will raise demand for predictive and risk-stratification applications.