| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Australia Cardiovascular Devices Market Size 2024 |

USD 535.07 Million |

| Australia Cardiovascular Devices Market, CAGR |

7.4% |

| Australia Cardiovascular Devices Market Size 2032 |

USD 1,017.51 Million |

Market Overview

The Australia Cardiovascular Devices Market is projected to grow from USD 535.07 million in 2024 to an estimated USD 1,017.51 million by 2032, with a compound annual growth rate (CAGR) of 7.4% from 2025 to 2032. This growth trajectory is driven by increasing incidences of cardiovascular diseases, expanding geriatric population, and rising healthcare expenditures.

Key drivers influencing the market include lifestyle-related health issues such as obesity, hypertension, and diabetes, which are prevalent across a broad age spectrum in Australia. Trends such as the adoption of wearable cardiac monitors, the integration of artificial intelligence in diagnostic imaging, and the proliferation of catheter-based interventions are shaping the competitive landscape. Furthermore, favorable regulatory frameworks and fast-track approvals for innovative cardiovascular devices are accelerating product adoption across hospitals and specialty clinics.

Geographically, major metropolitan regions including Sydney, Melbourne, and Brisbane lead in cardiovascular device consumption, driven by well-established healthcare systems and higher patient awareness. However, regional and rural areas are gradually witnessing growth through telemedicine and mobile health initiatives. Key players operating in the Australian cardiovascular devices market include Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Edwards Lifesciences Corporation, and Biotronik SE & Co. KG, each contributing to technological advancement and improved patient care across the country.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Australia Cardiovascular Devices Market is projected to grow from USD 535.07 million in 2024 to USD 1,017.51 million by 2032, registering a CAGR of 7.4% from 2025 to 2032.

- The global cardiovascular devices market is projected to grow from USD 72,115.60 million in 2024 to USD 133,700.94 million by 2032, with a CAGR of 7.1% from 2025 to 2032, driven by increasing cardiovascular diseases and advancements in medical technology.

- Growth is driven by the increasing prevalence of cardiovascular diseases, a rising aging population, and greater healthcare spending nationwide.

- The integration of AI, wearable monitors, and minimally invasive devices is enhancing early diagnosis, treatment precision, and patient outcomes.

- High costs of advanced devices and limited access to specialized care in remote regions continue to hinder equitable market growth.

- Supportive government policies and streamlined TGA approval pathways are encouraging innovation and faster adoption of new cardiovascular technologies.

- New South Wales and Victoria dominate the market with a combined share exceeding 50%, driven by robust healthcare infrastructure and urban demand.

- Expanding telehealth services and local manufacturing initiatives are opening new growth avenues, particularly in rural and underserved areas.

Report Scope

This report segments the Australia Cardiovascular Devices Market as follows:

Market Drivers

Rising Prevalence of Cardiovascular Diseases and Lifestyle Disorders

One of the primary drivers fueling the growth of the Australian cardiovascular devices market is the increasing incidence of cardiovascular diseases (CVDs), including coronary artery disease, heart failure, arrhythmias, and hypertension. These conditions have become more common due to sedentary lifestyles, unhealthy dietary habits, tobacco use, and high levels of stress—factors that contribute significantly to the growing burden of heart-related ailments in the country. For instance, 1.3 million people in Australia were living with heart, stroke, and vascular disease in 2022. The prevalence of these conditions has increased slightly since 2001, with 5.2% of the population affected. Additionally, ischemic heart diseases were the leading cause of death in Australia in 2022, while cerebrovascular diseases (including stroke) ranked fourth. Lifestyle-related disorders such as obesity and diabetes are also rising, further intensifying the risk of developing cardiovascular complications. The increasing need for early diagnosis, continuous monitoring, and effective treatment of these chronic conditions has led to a surge in demand for a broad range of cardiovascular devices, including stents, pacemakers, defibrillators, and advanced imaging tools. Healthcare providers are focusing on preventive and interventional strategies to reduce the morbidity and mortality associated with heart disease, which is translating into greater adoption of technologically sophisticated cardiovascular equipment. This trend is also supported by greater public awareness and government initiatives promoting heart health, routine screenings, and the use of wearable cardiac monitoring devices.

Technological Advancements and Adoption of Minimally Invasive Procedures

Technological innovation in cardiovascular devices is another critical growth driver. The Australian healthcare system has shown a rapid shift towards minimally invasive and non-invasive cardiac procedures, supported by the development of advanced medical devices such as transcatheter aortic valve replacement (TAVR) systems, bioresorbable vascular scaffolds, next-generation drug-eluting stents, and remote cardiac monitoring tools. Australia has been at the forefront of groundbreaking cardiovascular technology. For instance, in 2024, researchers at Monash University developed next-generation implantable heart devices aimed at improving patient outcomes for heart failure, which affects 500,000 Australians, with 50,000 new diagnoses annually. Additionally, St Vincent’s Hospital Sydney successfully performed Australia’s first durable total artificial heart implant in November 2024, marking a significant milestone in cardiac care. Furthermore, the integration of artificial intelligence (AI), machine learning (ML), and robotics in cardiovascular diagnostics and surgical interventions is enhancing precision and efficiency. AI-driven cardiac imaging and decision support tools are enabling earlier detection of heart conditions and personalized treatment planning. Australia’s strong research ecosystem and collaboration between academia, private manufacturers, and public health organizations are fostering rapid adoption of these technologies in clinical settings. As healthcare facilities continue to invest in advanced cardiovascular equipment and digital health platforms, the market is expected to grow significantly in response to evolving clinical demands and patient expectations.

Growing Geriatric Population and Increasing Healthcare Expenditure

Australia’s aging population is playing a pivotal role in driving demand for cardiovascular devices. As per government data, the proportion of Australians aged 65 and over is projected to continue rising, leading to a higher prevalence of age-related cardiac disorders such as arrhythmias, heart valve disease, and chronic heart failure. Elderly patients often require long-term monitoring and treatment, which boosts the demand for implantable devices like pacemakers, cardiac resynchronization therapy (CRT) devices, and defibrillators. The expansion of healthcare coverage, rising per capita health expenditure, and improvements in reimbursement policies are also contributing to increased accessibility to high-end cardiac care. Government-led programs, such as Medicare and the Pharmaceutical Benefits Scheme (PBS), provide financial assistance and subsidize costs for critical treatments and devices. This growing affordability, coupled with the development of specialized cardiac centers and multidisciplinary clinics, is facilitating higher adoption of cardiovascular technologies across both public and private healthcare sectors. Moreover, patients and caregivers are becoming more informed and proactive, further strengthening the market’s momentum.

Favorable Regulatory Environment and Government Initiatives

The regulatory framework and proactive government support in Australia offer a conducive environment for the cardiovascular devices market. The Therapeutic Goods Administration (TGA) oversees the approval and regulation of medical devices and has implemented streamlined processes to accelerate the approval of innovative cardiovascular technologies. The Australian Government also supports medical research and clinical trials through institutions like the National Health and Medical Research Council (NHMRC), which funds projects aimed at improving cardiovascular outcomes. In addition, national health campaigns focused on cardiovascular disease prevention and management—such as the Heart Foundation’s community awareness programs and the expansion of mobile health services in rural regions—have helped promote early diagnosis and timely interventions. These initiatives are helping bridge the healthcare gap between urban and remote areas, creating new growth avenues for device manufacturers and healthcare providers. Strategic investments in digital health, telecardiology, and infrastructure development further reinforce Australia’s readiness to adopt and expand the use of cardiovascular devices. This stable regulatory landscape and policy-driven support ensure long-term market sustainability and continuous innovation in cardiac care delivery.

Market Trends

Surge in Demand for Wearable and Remote Cardiac Monitoring Devices

A significant trend reshaping the Australian cardiovascular devices market is the increasing adoption of wearable and remote cardiac monitoring solutions. With a growing focus on preventive care and early detection, healthcare providers and patients alike are shifting towards non-invasive, continuous monitoring technologies that offer real-time insights into cardiac health. Devices such as smartwatches with ECG functionality, portable Holter monitors, and remote telemetry systems have gained considerable traction. These solutions are especially beneficial for elderly patients, individuals with chronic heart conditions, and those residing in rural areas with limited access to cardiology services. The rise of digital health platforms and telemedicine is further fueling this trend, allowing clinicians to remotely monitor patients’ heart rhythms, detect abnormalities early, and intervene proactively. Integration with cloud-based data systems and artificial intelligence (AI)-powered analytics enables more accurate diagnosis and personalized treatment planning. This evolution in cardiac monitoring not only enhances patient outcomes but also reduces the burden on hospital resources by enabling outpatient care and early interventions. For instance, wearable ECG monitors allow continuous tracking of heart rhythms, helping detect arrhythmias early and prevent severe cardiac events. As Australia’s healthcare system continues to emphasize digital transformation, wearable and remote monitoring devices are expected to become an integral part of chronic disease management and post-operative follow-up protocols.

Advancements in Minimally Invasive Cardiovascular Interventions

Minimally invasive procedures are gaining momentum in Australia’s cardiovascular devices market, driven by patient demand for faster recovery and reduced procedural risks. Techniques such as transcatheter aortic valve replacement (TAVR), percutaneous coronary interventions (PCI), and catheter-based ablation therapies are witnessing increased adoption across both public and private hospitals. These procedures, often supported by advanced imaging technologies and robotic assistance, offer precise navigation, reduced trauma, and lower post-operative complications compared to traditional open-heart surgeries. Australia’s well-equipped healthcare infrastructure and skilled interventional cardiologists are facilitating the wider implementation of these methods. Additionally, manufacturers are introducing next-generation devices—such as bioresorbable scaffolds, drug-coated balloons, and steerable catheters—that further enhance clinical outcomes and procedural safety. The National Cardiac Registry reports that PCI procedures in Australia have a 98% survival rate within 30 days and 93% of procedures result in a positive outcome. The growing acceptance of minimally invasive surgeries is also supported by favorable reimbursement policies and educational campaigns aimed at both patients and healthcare professionals. For instance, robotic-assisted cardiac procedures allow greater precision and stability, reducing procedural complications and improving recovery times. As awareness about these options increases, more individuals with structural heart defects, arrhythmias, and coronary artery diseases are opting for less invasive treatments. This trend not only contributes to the efficiency of cardiovascular care delivery but also expands the patient pool by making interventions viable for older or high-risk patients previously deemed inoperable.

Integration of Artificial Intelligence and Advanced Imaging Technologies

The integration of artificial intelligence (AI) and advanced imaging solutions is revolutionizing cardiovascular diagnostics and device performance across Australia. AI is being increasingly used to interpret diagnostic images, predict cardiac events, and assist in clinical decision-making with higher precision. Machine learning algorithms can now analyze ECG patterns, echocardiograms, and cardiac MRI scans with speed and accuracy, reducing diagnostic errors and facilitating earlier interventions. AI also plays a critical role in optimizing workflow efficiency, patient triage, and treatment planning, especially in busy cardiology departments. Simultaneously, the deployment of cutting-edge imaging modalities—such as 3D echocardiography, intravascular ultrasound (IVUS), and optical coherence tomography (OCT)—is enhancing real-time visualization during interventional procedures. These tools enable cardiologists to assess arterial plaque, stent placement, and valve positioning with greater accuracy. In research settings, AI is supporting the development of predictive models for heart disease risk assessment, contributing to more targeted therapies. The Australian government’s support for digital health and innovation, combined with hospital investment in AI infrastructure, is accelerating the uptake of these technologies. As these intelligent systems evolve, they are expected to become indispensable tools for clinicians, driving higher diagnostic confidence and improved cardiovascular outcomes nationwide.

Focus on Local Manufacturing and Supply Chain Resilience

Amid global supply chain disruptions and increasing dependence on imported medical devices, Australia is witnessing a shift toward local manufacturing and supply chain resilience in the cardiovascular sector. The COVID-19 pandemic exposed vulnerabilities in international sourcing, prompting both government and private players to prioritize domestic production of essential healthcare technologies. Local manufacturers are now exploring partnerships with global medical device companies to produce cardiovascular equipment—including diagnostic catheters, pacemaker components, and surgical tools—within Australia. This shift not only ensures timely availability of critical devices but also reduces lead times, import costs, and logistical complexities. The government’s support through grants, regulatory facilitation, and R\&D funding is encouraging innovation in homegrown medical technology. Additionally, local manufacturing helps align products more closely with Australian clinical guidelines, patient demographics, and environmental standards. Universities and research institutions are also collaborating with startups to develop indigenous technologies tailored to national needs. As this trend strengthens, Australia is likely to build a more self-reliant and robust cardiovascular devices ecosystem that enhances public health security, stimulates economic growth, and contributes to sustainable healthcare delivery in the long term.

Market Challenges

High Cost of Advanced Cardiovascular Devices and Limited Accessibility in Remote Regions

One of the major challenges confronting the Australia cardiovascular devices market is the high cost associated with advanced medical technologies. Sophisticated devices such as implantable cardioverter defibrillators (ICDs), drug-eluting stents, and transcatheter heart valves involve significant procurement, maintenance, and procedural costs. These expenses often place a financial strain on healthcare providers and limit widespread adoption, particularly in public hospitals with constrained budgets. Although Australia’s Medicare and private insurance systems offer partial reimbursement for many cardiovascular procedures, patients may still bear out-of-pocket expenses for devices not fully covered under existing policies. For instance, some advanced cardiovascular implants require additional post-operative monitoring and specialized follow-up care, which further increases the overall financial burden. This situation creates disparities in access to high-quality cardiac care, especially among economically disadvantaged populations. Moreover, the issue of accessibility becomes even more pronounced in rural and remote areas of Australia, where healthcare infrastructure is less developed and specialist services are limited. While urban centers like Sydney and Melbourne benefit from state-of-the-art cardiac facilities, regional communities frequently face delays in diagnosis and treatment due to a shortage of cardiologists, insufficient diagnostic equipment, and limited surgical capabilities. Mobile health initiatives and telecardiology services have been introduced to bridge this gap, but logistical, technological, and funding constraints continue to hinder full-scale implementation. As a result, many patients in these areas remain underserved, creating a need for more equitable distribution of resources and targeted policy interventions.

Regulatory Complexity and Lengthy Approval Timelines for Innovative Devices

The regulatory environment in Australia, while rigorous and patient-safety-oriented, poses challenges for the timely introduction of innovative cardiovascular devices. The Therapeutic Goods Administration (TGA) enforces comprehensive evaluation and compliance standards, often resulting in extended approval timelines. For manufacturers, especially smaller firms or startups, the process of gaining market access can be resource-intensive and time-consuming. Clinical trials, documentation requirements, and post-market surveillance obligations demand substantial investment in time, expertise, and capital. This regulatory burden can discourage innovation and delay the availability of cutting-edge technologies to healthcare providers and patients. Additionally, the evolving nature of international regulations and efforts to harmonize standards—particularly with the European Union Medical Device Regulation (EU MDR)—adds further complexity to compliance for global companies operating in the Australian market. Delays in approvals can also hinder procurement cycles and impact public and private healthcare budgets, which depend on predictable device availability for treatment planning. While the TGA has taken steps to streamline certain processes, including fast-tracking life-saving devices, significant challenges remain in achieving regulatory agility without compromising safety. The need to balance innovation with compliance continues to shape the strategic decisions of manufacturers, often prompting them to prioritize other regions with faster regulatory pathways. Addressing these regulatory challenges is critical for maintaining Australia’s competitiveness and responsiveness in the global cardiovascular technology landscape.

Market Opportunities

Expansion of Digital Health and AI-Driven Cardiac Care Solutions

The rapid digitization of healthcare presents a significant opportunity for growth in Australia’s cardiovascular devices market. With the increasing integration of digital health technologies such as remote monitoring systems, AI-enabled diagnostic tools, and mobile health applications, healthcare providers are better positioned to deliver timely and personalized cardiac care. This digital shift supports early detection, continuous monitoring, and data-driven decision-making, especially for patients with chronic heart conditions. As Australia continues to invest in telehealth infrastructure and digital transformation, manufacturers have the opportunity to develop and deploy smart cardiovascular devices that seamlessly interface with electronic health records (EHRs) and cloud-based platforms. These innovations are particularly beneficial in improving access to specialized cardiac services in remote and underserved regions.

Rising Demand for Preventive and Home-Based Cardiac Care

Australia’s aging population and growing awareness of cardiovascular health are driving increased demand for preventive care and home-based health solutions. Patients are seeking convenient, non-invasive devices that support proactive health management and reduce the need for frequent hospital visits. This trend opens doors for companies offering wearable cardiac monitors, portable ECG devices, and user-friendly diagnostic kits. Additionally, as public health campaigns emphasize lifestyle modification and early intervention, there is growing market potential for devices that support fitness tracking, heart rate monitoring, and blood pressure regulation. Manufacturers that can deliver accurate, affordable, and easy-to-use solutions tailored for home settings stand to gain a competitive edge in this evolving landscape. This opportunity aligns with Australia’s broader healthcare objective of decentralizing care while enhancing patient engagement and outcomes.

Market Segmentation Analysis

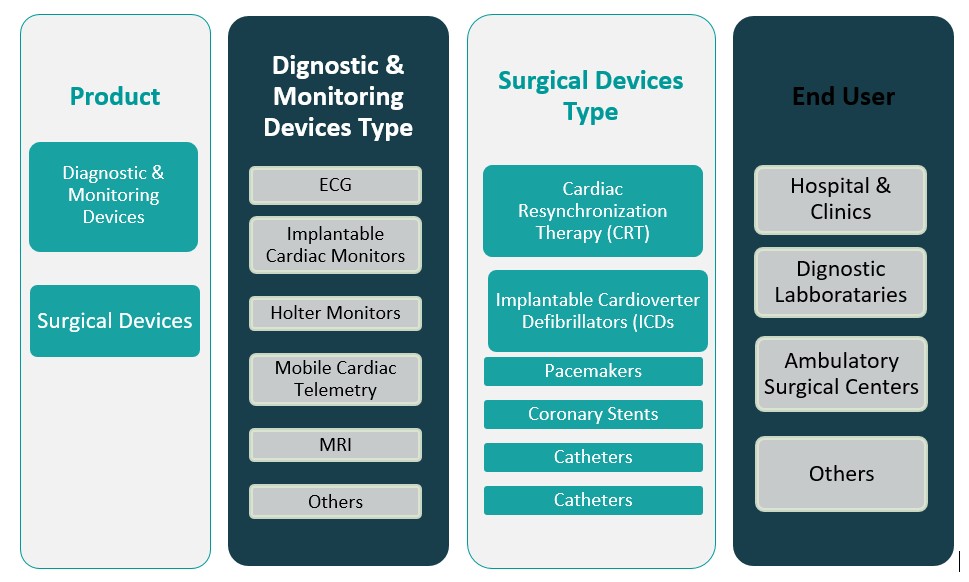

By Product

The Australia cardiovascular devices market is segmented into diagnostic & monitoring devices and surgical devices. Diagnostic and monitoring devices, which include ECG systems, Holter monitors, event monitors, and wearable cardiac monitors, have seen increasing adoption due to the shift towards preventive care and early disease detection. These devices enable continuous monitoring and timely identification of cardiac irregularities, which is essential for managing chronic cardiovascular conditions. On the other hand, surgical devices, such as stents, pacemakers, defibrillators, and heart valves, account for a significant share of the market owing to the rising number of interventional and corrective cardiac procedures. The advancement of minimally invasive surgical tools and catheter-based interventions has further accelerated the demand for technologically advanced surgical devices across Australian healthcare facilities.

By End User

In terms of end users, hospitals and clinics represent the largest segment, driven by their access to skilled personnel, comprehensive cardiac care infrastructure, and advanced surgical technologies. These facilities typically perform complex procedures such as coronary artery bypass grafting and heart valve replacements, which require sophisticated cardiovascular equipment. Diagnostic laboratories also contribute substantially to market demand by supporting early-stage cardiovascular assessments and ongoing patient monitoring through non-invasive testing. Ambulatory surgical centers are emerging as a vital segment due to their growing focus on cost-effective outpatient procedures, short recovery times, and reduced hospitalization costs. Additionally, the “Others” segment, which includes rehabilitation centers and specialty heart care centers, is gradually expanding as awareness of post-operative cardiac care and chronic disease management increases among patients.

Segments

Based on Product

- Diagnostic & Monitoring Devices

- Surgical Devices

Based on End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Others

Based on Diagnostic & Monitoring Devices Type

- ECG

- Implantable Cardiac Monitors

- Holter Monitors

- Mobile Cardiac Telemetry

- MRI

- Others

Based on Surgical Devices Type

- Cardiac Resynchronization Therapy (CRT)

- Implantable Cardioverter Defibrillators (ICDs

- Pacemakers

- Coronary Stents

- Catheters

Based on Region

- New South Wales

- Victoria

- Queensland

Regional Analysis

New South Wales (32%)

New South Wales (NSW) holds the largest market share, accounting for 32% of the total cardiovascular devices market. This dominance is driven by the presence of world-class hospitals, academic medical centers, and advanced research institutions concentrated in Sydney and surrounding urban areas. The state’s investment in digital health technologies, early adoption of minimally invasive procedures, and a large aging population further support the robust demand for both diagnostic and surgical cardiovascular devices.

Victoria (26%)

Victoria follows closely, representing 26% of the market share. With Melbourne serving as a major healthcare hub, Victoria benefits from a strong network of public and private hospitals, highly skilled cardiologists, and a supportive policy environment that encourages innovation and clinical research. The state also prioritizes preventive health measures, contributing to the increasing uptake of wearable cardiac monitors and diagnostic tools that facilitate early intervention and long-term disease management.

Key players

- Abbott

- GE HealthCare

- Edwards Lifesciences Corporation

- Siemens Healthcare GmbH

- BIOTRONIK SE & Co. KG

- Canon Medical Systems Asia Pte. Ltd.

- Cardinal Health

- Medtronic

- Boston Scientific Corporation

- Cochlear Limited

- Clarity Medical

- Sonoscape Australia

- Life Systems Medical

Competitive Analysis

The Australia cardiovascular devices market is highly competitive, characterized by the presence of both global leaders and regional players. Major multinational corporations such as Abbott, Medtronic, Boston Scientific, and GE HealthCare dominate the market with their expansive product portfolios, strong R\&D capabilities, and advanced technological offerings. These companies leverage global expertise to provide cutting-edge solutions, including minimally invasive devices, implantables, and diagnostic imaging systems. Edwards Lifesciences and BIOTRONIK specialize in structural heart and electrophysiology devices, respectively, contributing to innovation in niche segments. Meanwhile, regional and specialized firms like Clarity Medical, Sonoscape Australia, and Life Systems Medical play a critical role in enhancing accessibility and offering tailored solutions for local healthcare providers. As competition intensifies, companies are focusing on strategic partnerships, local manufacturing, and digital integration to expand their footprint and meet Australia’s evolving cardiovascular care needs.

Recent Developments

- In February 2025, Abbott issued a safety notification for certain Assurity and Endurity pacemakers due to potential epoxy mixing issues during manufacturing, which could lead to device malfunction.

- In April 2025, GE HealthCare launched the Revolution™ Vibe CT system featuring Unlimited One-Beat Cardiac imaging and AI solutions, enhancing cardiac imaging capabilities.

- In April 2025, Medtronic reported promising evidence for its Affera™ pulsed field ablation technologies in treating atrial fibrillation patients.

- In May 2024, Siemens Healthineers announced new cardiology applications with artificial intelligence for the Acuson Sequoia ultrasound system, including a new 4D transesophageal (TEE) transducer for cardiology exams.

- In February 2025, Philips developed a miniaturized intracardiac transducer, enabling higher-resolution views of cardiac structures and functions, benefiting structural heart disease and electrophysiology procedures.

- In March 2025, Boston Scientific announced the acquisition of SoniVie Ltd. to expand its interventional cardiology therapies offerings with ultrasound-based renal denervation technology.

- In June 2024, Biovac Institute entered a partnership with Sanofi to locally manufacture inactivated polio vaccines in Africa, aiming to serve the potential needs of over 40 African countries.

Market Concentration and Characteristics

The Australia cardiovascular devices market exhibits a moderate to high level of market concentration, dominated by a few global players such as Abbott, Medtronic, Boston Scientific, and GE HealthCare, who command significant market share due to their technological expertise, wide-ranging product portfolios, and established distribution networks. These multinational companies are often the first to introduce innovative devices, benefiting from strong brand recognition and trusted clinical performance. The market is characterized by a growing preference for minimally invasive technologies, increasing demand for remote and wearable monitoring devices, and rising integration of digital health solutions. While urban centers have high device penetration due to advanced healthcare infrastructure, rural areas still face accessibility challenges, offering opportunities for expansion. The regulatory environment remains stringent yet supportive of innovation, and public-private collaborations continue to shape market dynamics. As the healthcare sector increasingly emphasizes value-based care and preventive cardiology, the market is evolving towards more patient-centric, data-driven, and cost-effective device solutions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Product, End User, Diagnostic & Monitoring Devices Type, Surgical Devices Type and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will witness increased adoption of remote cardiac monitoring devices, driven by the expansion of telehealth services and demand for continuous, at-home patient care.

- Artificial intelligence will play a pivotal role in enhancing diagnostics, risk prediction, and decision-making, improving accuracy and efficiency in cardiovascular care delivery.

- The shift toward minimally invasive procedures will continue, boosting demand for catheter-based interventions and image-guided surgical devices.

- Improved healthcare outreach and government funding will enable deeper market penetration into Australia’s underserved rural and remote regions.

- Leading manufacturers will intensify research efforts to develop next-generation cardiovascular devices with improved functionality, biocompatibility, and patient outcomes.

- The growing awareness of heart disease prevention will drive adoption of wearable technologies and early diagnostic tools among health-conscious consumers.

- Streamlined regulatory processes and faster approval pathways are expected to support quicker market entry for innovative cardiovascular devices.

- Partnerships between government agencies, healthcare providers, and device manufacturers will facilitate infrastructure development and device accessibility.

- Advances in data analytics and genomics will enable more personalized treatment plans, influencing device design and therapeutic approaches.

- Australia will likely see growth in domestic production of cardiovascular devices, reducing import dependence and strengthening supply chain resilience.