Baby Food Market Overview:

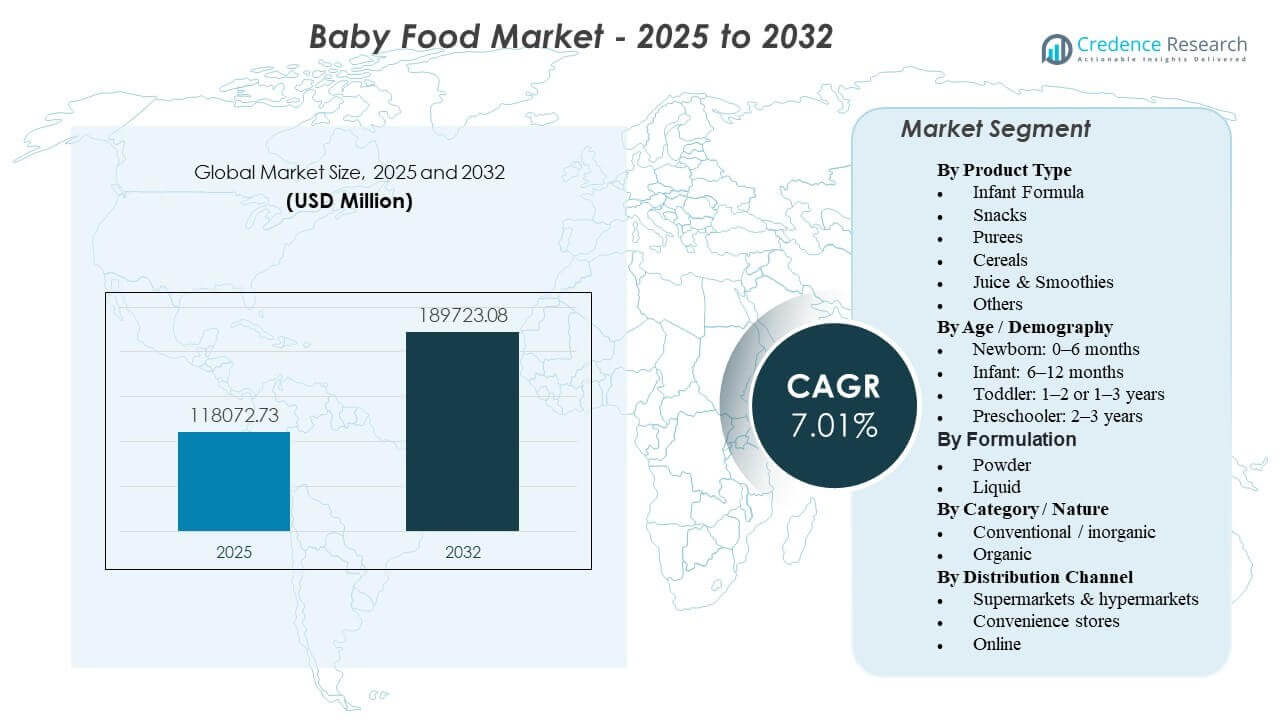

The global Baby Food Market size was estimated at USD 118,072.73 million in 2025 and is expected to reach USD 189,723.08 million by 2032, growing at a CAGR of 7.01% from 2025 to 2032. Growth is primarily driven by higher reliance on convenient, nutrition-assured feeding solutions as more households balance time constraints with a strong preference for trusted, standardized infant nutrition. Product innovation across functional formulations, clean-label positioning, and improved packaging convenience is also supporting premiumization and repeat purchases across key consumption occasions.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Baby Food Market Size 2025 |

USD 118,072.73 million |

| Baby Food Market, CAGR |

7.01% |

| Baby Food Market Size 2032 |

USD 189,723.08 million |

Key Market Trends & Insights

- The Baby Food Market reached USD 118,072.73 million in 2025, reflecting broad penetration across core infant and toddler nutrition categories.

- The market is projected to expand at a 7.01% CAGR during 2025–2032, supported by product innovation and channel expansion.

- Infant Formula accounted for 63.7% share in 2025, reinforcing its position as the primary revenue pool within baby nutrition.

- Organic products represented 58.3% share in 2025, indicating sustained preference for clean-label and traceable ingredient positioning.

- Asia Pacific contributed 43.7% share in 2025, supported by larger infant populations and rapid growth in modern retail availability.

Segment Analysis

Demand is shaped by a mix of nutrition assurance, convenience, and product trust, with caregivers seeking consistent quality across daily feeding routines. Product choices increasingly reflect stage-based nutrition needs, where early feeding prioritizes standardized formula and gentle digestion positioning, and later stages expand into textures, flavors, and self-feeding formats. Packaging and portability are also influencing purchasing behavior, as single-serve and on-the-go formats improve adoption across daycare, travel, and outside-the-home occasions.

Premiumization continues across both conventional and organic portfolios, driven by cleaner ingredient lists, transparency claims, and functional differentiation in early-life nutrition. As households broaden their product basket beyond formula, categories such as snacks, cereals, and purees benefit from frequent replenishment cycles and multi-occasion use. Channel strategy remains important, with physical retail supporting discovery and price promotions, and online platforms improving convenience through replenishment models and wider assortment access.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Infant Formula accounted for the largest share of 63.7% in 2025. This leadership is supported by its essential role in early-stage feeding, particularly when breastfeeding is supplemented or not feasible. Ongoing innovation in functional nutrition and specialized formulations also supports premium price points and brand loyalty. Additionally, routine, high-frequency consumption drives consistent volumes relative to more discretionary baby snack and puree purchases.

By Age / Demography Insights

Age-based demand shifts from nutrition standardization in early months to variety, texture progression, and self-feeding formats as children grow. Newborn and infant stages tend to emphasize gentle digestion, predictable nutrient delivery, and caregiver confidence in product safety and consistency. Toddler-stage consumption typically expands into a broader mix of snacks, cereals, and meal solutions, increasing category breadth and purchase frequency. Preschooler-stage products often overlap with toddler nutrition but emphasize taste acceptance, portioning, and convenient formats suited to active routines.

By Formulation Insights

Liquid accounted for the largest share of 44.6% in 2025. Ready-to-feed formats reduce preparation time and support usage during travel, daycare, and out-of-home occasions. Liquid products also benefit from portion control and consistency, which can reduce caregiver effort and dosing errors. Improvements in packaging convenience and shelf-stable solutions further widen availability across channels and support premium positioning.

By Category / Nature Insights

Organic accounted for the largest share of 58.3% in 2025. Organic positioning aligns with caregiver concerns about additives, residues, and ingredient transparency, strengthening willingness to pay for perceived safety and quality. The category benefits from broader retail shelf allocation and stronger brand differentiation through certification and traceability claims. Innovation beyond core purees into snacks and multi-stage feeding products continues to expand organic penetration across age groups.

By Distribution Channel Insights

Supermarkets & hypermarkets accounted for the largest share of 45.4% in 2025. Large-format retail supports one-stop purchasing, wider assortment access, and in-store visibility that influences trial and repeat buying. Promotions and bundling are especially relevant for high-frequency staples such as formula and cereals, reinforcing retail dominance. At the same time, online channels continue to gain importance through convenience, replenishment behavior, and expanded access to premium and specialty ranges.

Baby Food Market Drivers

Increasing reliance on convenient, time-saving feeding solutions

Caregiver routines increasingly favor products that reduce preparation time and improve portability. Ready-to-feed formats, portion packs, and travel-friendly packaging support usage across home and out-of-home occasions. This trend is reinforced by rising workforce participation and dual-income household structures that prioritize convenience. As a result, brands that combine ease-of-use with strong nutrition assurance gain repeat purchase momentum. Single-serve and resealable packaging also helps improve portion control and reduce wastage for caregivers.

- For instance, Tetra Pak’s aseptic carton systems for ready-to-feed liquid infant formula allow ambient storage and eliminate mixing, with portion packs widely adopted in hospital and travel channels to support on-the-go feeding without refrigeration.

Premiumization through functional and stage-specific nutrition

The market benefits from product differentiation tied to stage-based nutritional needs and functional positioning. Formulations that emphasize digestion comfort, nutrient completeness, and specialized needs strengthen brand preference and reduce switching. Premium lines also benefit from clearer labeling and product education that supports trust. This dynamic sustains higher average selling prices and expands value growth beyond volume increases. Clinically supported ingredients and targeted claims are increasingly used to justify premium pricing and strengthen caregiver confidence.

- For instance, Kendamil’s Stage 1 formula is formulated with a whey-to-casein ratio of about 60:40 for 0–6 months, while Stage 2 increases iron and protein for 6–12 months, and Stage 3 for 12–36 months further raises protein and casein for longer satiety, clearly segmenting formulations by age and function.

Strong consumer pull for clean-label and organic positioning

Ingredient transparency and simplified formulations are shaping purchase decisions across baby nutrition categories. Organic and clean-label products are often perceived as safer and better aligned with early-life health priorities, supporting sustained demand. Retailers also contribute by expanding shelf visibility and curated assortments for organic and natural ranges. This driver supports ongoing portfolio upgrades and product innovation. Greater scrutiny of sugar, additives, and processing is accelerating reformulation and clean-label upgrades across portfolios.

Expansion of modern retail and digital commerce access

Distribution improvements widen category availability and improve purchase frequency through easier access. Large-format retail supports discovery, promotions, and breadth of selection for multi-item baskets. Online channels strengthen convenience through home delivery, wider assortment access, and replenishment behavior for high-frequency products. Together, these channel dynamics strengthen penetration and sustain recurring demand. Subscriptions and auto-replenishment models are also improving repeat purchases, especially for infant formula and routine staples.

Baby Food Market Challenges

Pricing sensitivity remains a key constraint, particularly as premium and organic products carry higher price points that may limit adoption in cost-conscious households. Demand can also be influenced by shifting consumer perceptions around sugar content, additives, and processing levels, which increases scrutiny and can reshape brand preferences. Regulatory requirements for infant nutrition claims and labeling standards add compliance complexity and can slow the rollout of new formulations across geographies. Regulation differences across countries further increase compliance effort and time-to-market for new products.

- For instance, Consumer Reports’ 2025 testing of 41 baby formulas found detectable levels of heavy metals such as lead and arsenic in multiple products, prompting some parents to switch to brands that explicitly market reduced contaminant levels and tighter raw‑material testing protocols.

Supply-side pressures can affect product availability and pricing stability, especially for formula-heavy portfolios with complex ingredient inputs and strict quality controls. Retail competition and private-label expansion can compress margins in mature markets, particularly in supermarkets and hypermarkets where promotions are frequent. Brand trust remains critical, and any quality or recall event can trigger rapid reputational impact due to the high-sensitivity nature of infant nutrition. Input cost volatility (dairy, packaging) can intensify pricing pressure and margin management challenges for brands.

Baby Food Market Trends and Opportunities

Brands are expanding product portfolios with cleaner ingredient lists, simplified labeling, and claims focused on transparency and traceability. This trend supports premium positioning and improves differentiation across both mainstream and specialist players. Product innovation is also moving toward more convenient formats such as pouches, single-serve packs, and ready-to-feed options that fit modern feeding routines. Fortified and functional innovations (e.g., digestion or immunity positioning) are creating additional premiumization opportunities.

- For instance, Nestlé’s Gerber Organic Banana Mango Purée and Piltti fruit purées were moved into a single‑material polypropylene baby food pouch that is 100% recyclable through Gerber’s national TerraCycle program in the U.S. and broadly distributed in Finnish supermarkets, enabling complete material recovery within existing recycling streams.

Digital commerce is creating opportunities for subscription-based replenishment, personalized product discovery, and direct-to-consumer engagement. Premium and specialty categories benefit from online assortment depth and consumer reviews that influence switching behavior. There is also growing whitespace for products tailored to specific dietary preferences and sensitivities, supporting diversification within formula and complementary feeding ranges. Online channels also enable stronger lifecycle targeting from newborn to toddler stages, improving retention and repeat buying.

Regional Insights

North America

North America accounted for 19.9% share in 2025, supported by high per-capita spending and strong premiumization across formula and organic offerings. Mature retail infrastructure reinforces broad availability and frequent promotional activity, sustaining volume and value growth. The region also benefits from advanced product differentiation and brand competition across specialized nutrition needs. Demand remains closely tied to trust, safety assurance, and product consistency.

Europe

Europe represented 19.1% share in 2025, reflecting established consumption patterns and strong adoption of stage-based feeding products. The region shows sustained demand for clean-label positioning and quality assurance, supporting premium segments. Retail consolidation and strong supermarket penetration influence pricing dynamics and category visibility. Growth is supported by portfolio diversification and product upgrades aligned with evolving nutrition expectations.

Asia Pacific

Asia Pacific led with 43.7% share in 2025, driven by larger infant populations, expanding urban middle-class consumption, and rising penetration of modern retail. Demand is supported by brand preference for trusted nutrition solutions and expanding access to packaged baby food products. Product innovation and premiumization are increasingly visible in major markets, strengthening value growth. Online retail and improved distribution infrastructure further enhance category reach.

Latin America

Latin America held 9.6% share in 2025, supported by increasing modern retail availability and growing acceptance of packaged baby nutrition products. Demand growth is influenced by urbanization and improvements in retail access, although price sensitivity remains important. Brands that balance affordability with nutrition assurance are well-positioned for expansion. Portfolio strategies often emphasize value packs and accessible formats.

Middle East & Africa

Middle East & Africa accounted for 7.7% share in 2025, reflecting a smaller organized market base but rising demand in urban centers. Growth is supported by expanding retail networks and increasing availability of branded baby nutrition products. Product affordability and distribution coverage remain key adoption factors across many countries. Gradual premiumization is expected as higher-income segments expand and modern channels grow.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

Competition is shaped by strong brand trust requirements, portfolio breadth across life-stage nutrition, and frequent innovation cycles in formulation and packaging. Leading companies compete through product differentiation, clean-label positioning, and channel strength across supermarkets and online platforms. Portfolio strategies often balance mass-market affordability with premium organic and specialized nutrition lines. Marketing execution and product education also influence switching behavior in a category where caregivers prioritize safety and consistency.

Nestlé S.A. maintains a broad presence across early-life nutrition with multi-tier product portfolios spanning infant formula and complementary foods, supported by continuous formulation upgrades and category extensions. The company’s scale supports wide distribution coverage, consistent supply, and the ability to compete across both mainstream and premium segments. Ongoing innovation in functional nutrition strengthens positioning in high-value formula pools. Brand trust and portfolio breadth remain central to its competitive advantage.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories (Abbott Nutrition)

- Reckitt Benckiser Group plc (Mead Johnson Nutrition)

- The Kraft Heinz Company

- Royal FrieslandCampina N.V.

- Hero Group

- HiPP GmbH & Co.

- The Hain Celestial Group, Inc.

- Perrigo Company plc

- Bellamy’s Organic

- Bubs Australia Limited

- Kewpie Corporation

- Arla Foods

- Feihe International (China Feihe)

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In March 2026, Good Start | Dr. Brown’s infant formulas were recognized as “Baby Food Product of the Year” at the Baby Innovation Awards, highlighting the brand’s focus on innovation in infant nutrition and further elevating its profile within the global baby food market.

- In January 2026, Princes Group completed the acquisition of Italian baby food specialist Plasmon from The Kraft Heinz Company, securing brands such as Plasmon, Nipiol, BiAglut, Aproten, and Dieterba along with Kraft Heinz’s baby food production site in Latina, Italy, in a deal valued at about €120–124 million that strengthens Princes’ position in the European baby food market.

- In July 2025, New Princes Group (now operating as NewPrinces) first announced its agreement to acquire Kraft Heinz’s Italian baby food and nutrition arm, including the Plasmon business and related brands and facilities, marking the beginning of a strategic move to expand its footprint in premium and organic infant nutrition across Europe.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 118,072.73 million |

| Revenue forecast in 2032 |

USD 189,723.08 million |

| Growth rate (CAGR) |

7.01% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type Outlook: Infant Formula, Snacks, Purees, Cereals, Juice & Smoothies, Others; By Age / Demography Outlook: Newborn (0–6 months), Infant (6–12 months), Toddler (1–2 or 1–3 years), Preschooler (2–3 years); By Formulation Outlook: Powder, Liquid; By Category / Nature Outlook: Conventional / inorganic, Organic; By Distribution Channel Outlook: Supermarkets & hypermarkets, Convenience stores, Online |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Nestlé S.A., Danone S.A., Abbott Laboratories (Abbott Nutrition), Reckitt Benckiser Group plc (Mead Johnson Nutrition), The Kraft Heinz Company, Royal FrieslandCampina N.V., Hero Group, HiPP GmbH & Co., The Hain Celestial Group, Inc., Perrigo Company plc, Bellamy’s Organic, Bubs Australia Limited, Kewpie Corporation, Arla Foods, Feihe International (China Feihe) |

| No. of Pages |

335 |

Segments

By Product Type

- Infant Formula

- Snacks

- Purees

- Cereals

- Juice & Smoothies

- Others

By Age / Demography

- Newborn: 0–6 months

- Infant: 6–12 months

- Toddler: 1–2 or 1–3 years

- Preschooler: 2–3 years

By Formulation

By Category / Nature

- Conventional / inorganic

- Organic

By Distribution Channel

- Supermarkets & hypermarkets

- Convenience stores

- Online

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa