Market Overview:

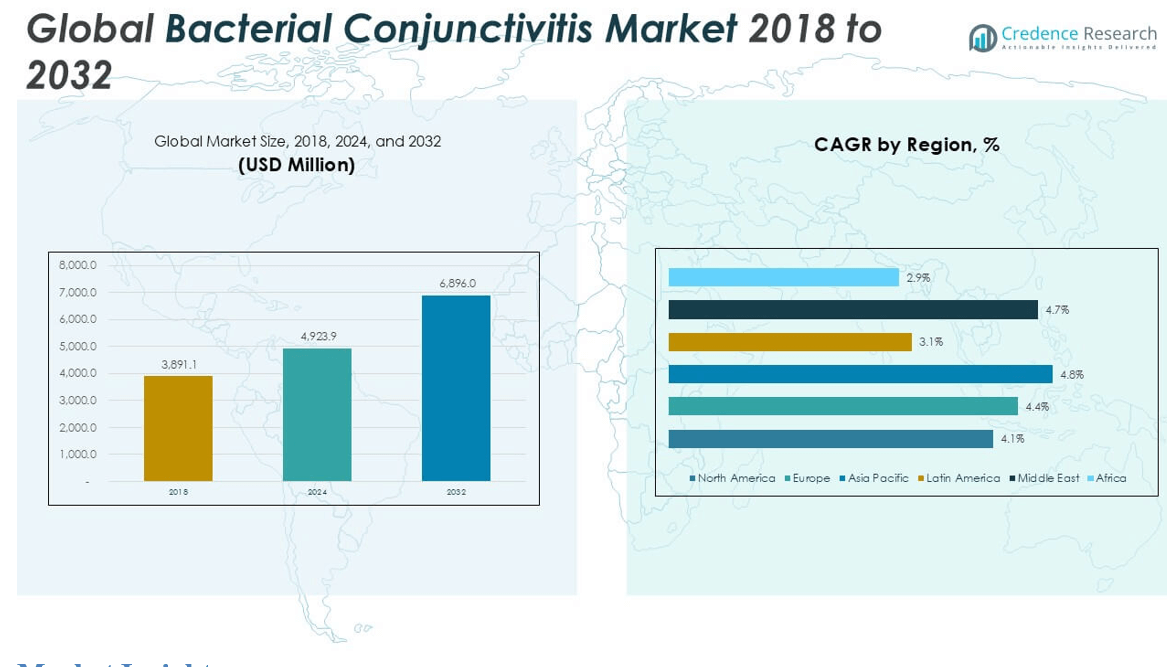

The Bacterial Conjunctivitis market size was valued at USD 3,891.1 million in 2018 and increased to USD 4,923.9 million in 2024. It is anticipated to reach USD 6,896.0 million by 2032, growing at a CAGR of 4.33% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Bacterial Conjunctivitis Market Size 2024 |

USD 4,923.9 million |

| Bacterial Conjunctivitis Market, CAGR |

4.33% |

| Bacterial Conjunctivitis Market Size 2032 |

USD 6,896.0 million |

The bacterial conjunctivitis market is highly competitive, with key players including Actavis Plc., Akorn, Inc., Bayer AG, F. Hoffmann-La Roche Ltd., Merck & Co., Inc., Novartis AG, Pfizer, Inc., Santen Pharmaceutical Co., Ltd., and Cipla Ltd. These companies drive market growth through robust product portfolios, strategic mergers, and continuous R&D in ophthalmic antibiotics. Novartis AG and Pfizer, Inc. maintain a strong presence globally due to their extensive distribution networks and advanced formulations. Asia Pacific emerged as the leading region in 2024, accounting for 32.4% of the global market share, fueled by high population density, rising infection rates, and improved healthcare access. North America and Europe followed, supported by early diagnosis practices and widespread availability of branded therapies.

Market Insights

- The Bacterial Conjunctivitis market was valued at USD 3,891.1 million in 2018, reached USD 4,923.9 million in 2024, and is projected to grow to USD 6,896.0 million by 2032, at a CAGR of 4.33% during the forecast period.

- Market growth is driven by increasing incidence of bacterial eye infections, rising awareness of eye hygiene, and the growing demand for fast-acting topical antibiotics.

- Key trends include the shift toward preservative-free formulations and growing adoption of online pharmacies and e-prescription services across developed and developing countries.

- The market is competitive with leading players such as Novartis AG, Pfizer, Bayer AG, and Cipla Ltd. focusing on new product development, strategic collaborations, and global expansion; however, rising antibiotic resistance and misuse pose major restraints.

- Asia Pacific held the largest regional share at 32.4% in 2024, while fluoroquinolones dominated the drug class segment due to their broad-spectrum efficacy.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

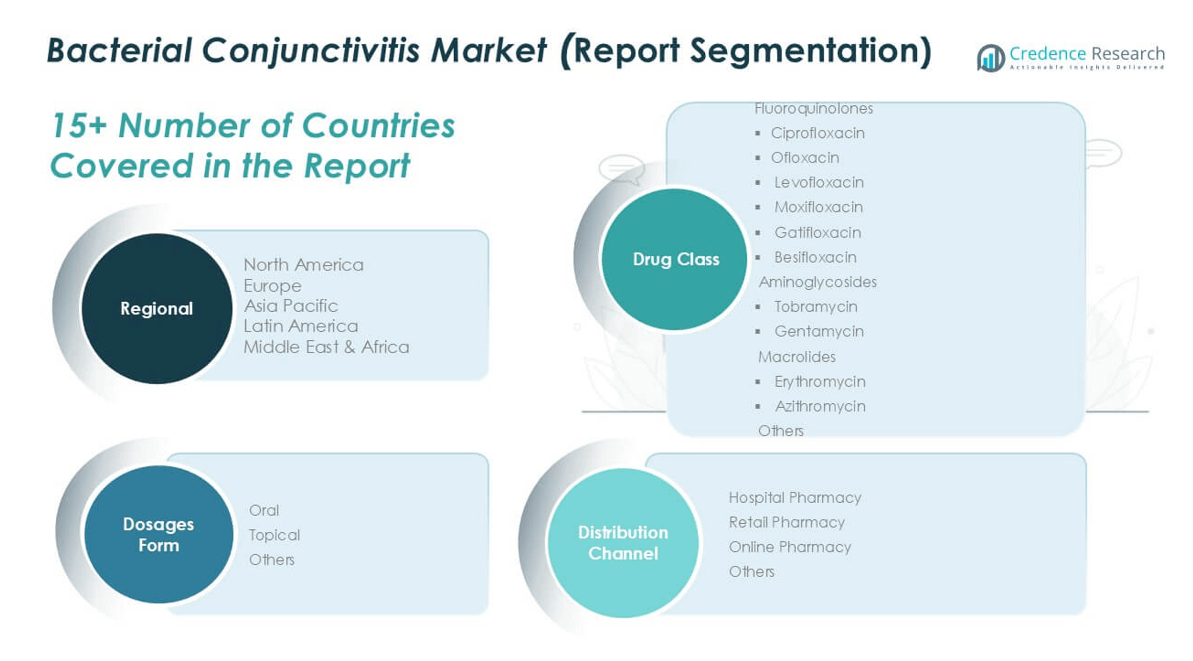

By Drug Class

The Fluoroquinolones segment holds the dominant position in the Bacterial Conjunctivitis market, accounting for the largest market share in 2024. Within this class, Moxifloxacin is the most widely prescribed due to its broad-spectrum activity, rapid bactericidal action, and low resistance profile. Other popular fluoroquinolones include Levofloxacin and Ciprofloxacin, which are often used in acute cases. The increasing prevalence of antibiotic-resistant bacterial strains is driving demand for newer-generation fluoroquinolones. Meanwhile, Macrolides such as Azithromycin are preferred in pediatric patients due to better tolerability. Aminoglycosides remain effective in hospital settings, but their use is more limited due to potential toxicity.

- For instance, Alcon’s Vigamox (Moxifloxacin 0.5% ophthalmic solution), launched in the U.S., reported over 2 million prescriptions filled annually during its peak usage years, demonstrating its clinical preference in outpatient treatments.

By Dosage Form

Topical formulations dominate the dosage form segment of the Bacterial Conjunctivitis market, holding the largest revenue share in 2024. Eye drops and ointments are widely preferred due to their localized application, faster therapeutic response, and reduced systemic side effects. The topical route ensures high drug concentration at the site of infection, which enhances clinical outcomes and reduces the risk of systemic resistance. Oral formulations are mainly used for severe or recurrent infections, especially when associated with systemic conditions. The “Others” category, including injectable forms, represents a minor share and is used only in rare, complicated cases.

- For instance, Bausch + Lomb’s Besivance (besifloxacin ophthalmic suspension 0.6%) achieved over 500,000 prescriptions within the first 18 months of its U.S. launch, validating strong adoption of topical fluoroquinolone formulations.

By Distribution Channel

Retail pharmacies represent the leading distribution channel in the Bacterial Conjunctivitis market, capturing the largest market share in 2024. This dominance is attributed to easy accessibility, widespread availability of over-the-counter antibiotic eye drops, and the preference of patients for walk-in purchases. Hospital pharmacies follow, especially in inpatient or emergency care scenarios where prescriptions are dispensed immediately. Online pharmacies are witnessing steady growth due to increased digitalization, rising consumer convenience, and discounts offered on prescription medications. Hypermarkets and supermarkets hold a smaller share, typically limited to OTC products, while the “Others” category remains relatively niche.

Market Overview

Rising Incidence of Bacterial Eye Infections

The increasing global prevalence of bacterial conjunctivitis, particularly in densely populated and developing regions, is a key growth driver for the market. Poor hygiene practices, high pollution levels, and seasonal outbreaks contribute to the frequent occurrence of eye infections. Additionally, school-going children and the elderly population are more susceptible to these infections, which amplifies the demand for effective treatment solutions. As awareness grows around early diagnosis and treatment, the demand for antibacterial eye drops and ointments continues to surge, boosting market expansion.

- For instance, in 2023, Cipla Ltd. reported the production of over 82 million units of ophthalmic antibiotic formulations from its Indore and Goa facilities alone, reflecting its aggressive scaling in response to rising demand across South Asia and Africa.

Advancements in Antibiotic Therapies

Ongoing advancements in antibiotic formulations, including the development of broad-spectrum and low-resistance drugs, are significantly driving market growth. Pharmaceutical companies are investing in R&D to introduce next-generation fluoroquinolones and macrolides with enhanced efficacy and reduced side effects. These innovations cater to both acute and chronic bacterial eye infections, improving patient compliance and outcomes. The availability of combination therapies and preservative-free eye drops also expands treatment options, thereby encouraging healthcare providers to recommend newer, more effective solutions to a wider range of patients.

- For instance, Santen Pharmaceutical Co., Ltd. invested ¥12.3 billion in R&D in FY2023, a portion of which supported the clinical trials of its preservative-free antibiotic-corticosteroid combination eyedrop, STN1013001, currently in Phase III trials across Europe and Asia.

Growing Accessibility to Healthcare and Pharmacies

Improved access to healthcare infrastructure and pharmacy services, particularly in emerging economies, supports market growth. The expansion of retail and online pharmacies allows patients to obtain treatments conveniently and affordably. Government initiatives aimed at enhancing eye care services, along with the proliferation of telemedicine and e-prescriptions, have made it easier for patients to seek timely interventions. This increased accessibility drives the overall demand for conjunctivitis medications and encourages early treatment, reducing complications and improving disease management rates across regions.

Key Trends & Opportunities

Rising Preference for Preservative-Free Formulations

A growing trend in the market is the shift toward preservative-free antibiotic eye drops, which are gaining popularity due to better safety profiles and lower risk of ocular surface damage with prolonged use. These formulations are especially beneficial for patients with chronic conjunctivitis or sensitive eyes, expanding their applicability. Manufacturers are seizing this opportunity by developing single-dose units and preservative-free multi-use bottles, which are expected to capture significant market share as consumer awareness about eye health increases.

- For instance, Théa Pharmaceuticals’ Hyabak eye drops, which are preservative-free, reached distribution in over 70 countries, with annual sales exceeding 15 million units, showcasing global demand for safer alternatives.

Growth of Online Pharmacies and E-prescription Platforms

The rapid expansion of digital health services and online pharmacies presents a major opportunity in the Bacterial Conjunctivitis market. Consumers are increasingly turning to e-commerce platforms for the convenience of home delivery and access to a wider range of products. E-prescription systems further streamline the process, enabling physicians to directly prescribe medications, which patients can quickly purchase online. This trend is particularly strong in urban areas and among younger demographics, offering pharmaceutical companies a lucrative distribution channel to tap into.

- For instance, 1mg (now Tata 1mg) in India reported over 100,000 monthly orders for ophthalmic products in 2023, indicating the rapid digital shift in drug accessibility for conditions like conjunctivitis.

Key Challenges

Antibiotic Resistance and Misuse

The growing concern over antibiotic resistance poses a major challenge to the Bacterial Conjunctivitis market. Overprescription, self-medication, and inappropriate use of antibiotics have contributed to reduced drug efficacy, prompting regulatory scrutiny and restricted usage. Healthcare professionals are under increasing pressure to follow antibiotic stewardship protocols, which may limit the indiscriminate use of commonly prescribed treatments. This challenge necessitates continuous innovation and monitoring of drug effectiveness to maintain therapeutic relevance.

Lack of Awareness and Delayed Diagnosis

In many low-income and rural regions, a lack of awareness about bacterial conjunctivitis symptoms and the importance of early treatment delays diagnosis and intervention. Patients often misidentify symptoms or resort to traditional remedies, exacerbating the condition. This delay not only affects recovery but can also increase the risk of complications and disease spread. Public health campaigns and better patient education are critical to overcoming this challenge and ensuring prompt access to appropriate medical care.

Regulatory and Approval Hurdles

Obtaining regulatory approvals for new ophthalmic formulations can be time-consuming and complex, especially in highly regulated markets like the U.S. and Europe. Stringent safety and efficacy standards, along with costly clinical trials, create entry barriers for new players and delay product launches. These regulatory constraints can limit market growth and discourage smaller companies from investing in innovative treatments, ultimately slowing the pace of therapeutic advancement in the sector.

Regional Analysis

North America

North America accounted for the largest regional share in the bacterial conjunctivitis market, valued at USD 1,072.38 million in 2018, and is projected to reach USD 1,843.29 million by 2032, growing at a CAGR of 4.1%. The region held approximately 27.2% of the global market in 2024, driven by advanced healthcare infrastructure, high awareness levels, and the widespread availability of prescription medications. The United States leads the market due to robust diagnosis rates, insurance coverage, and access to ophthalmic care. Continued innovations in topical antibiotics and a strong pharmaceutical presence further support regional market expansion.

Europe

Europe represented a significant share in the bacterial conjunctivitis market, with a market value of USD 921.02 million in 2018, reaching USD 1,648.13 million by 2032, at a CAGR of 4.4%. In 2024, the region contributed to around 23.8% of the global market. The demand is supported by increasing cases of eye infections, aging population, and adoption of preservative-free ophthalmic formulations. Germany, the UK, and France are key contributors, benefiting from efficient healthcare systems and regulatory support for safe antibiotic use. Growth is further bolstered by rising telemedicine practices and access to over-the-counter eye care products.

Asia Pacific

Asia Pacific emerged as the fastest-growing regional market for bacterial conjunctivitis, with a market size of USD 1,223.74 million in 2018, expanding to USD 2,328.07 million by 2032, at a robust CAGR of 4.8%. The region accounted for the largest market share of 32.4% in 2024, driven by high population density, growing healthcare awareness, and increasing cases of infectious diseases. Countries like China, India, and Japan are leading the demand due to the expansion of ophthalmology clinics, rising healthcare investments, and improved access to retail pharmacies. Government initiatives to improve eye health are also supporting regional market growth.

Latin America

Latin America held a modest share in the bacterial conjunctivitis market, valued at USD 397.28 million in 2018 and expected to reach USD 597.88 million by 2032, registering a CAGR of 3.1%. In 2024, the region captured around 9.6% of the global market. Growth in the region is supported by improving healthcare infrastructure and increased availability of affordable antibiotics. Brazil and Mexico remain the key markets, driven by urban population growth and rising awareness of ocular health. However, market expansion is somewhat restrained by limited healthcare access in remote areas and lower diagnosis rates compared to developed regions.

Middle East

The Middle East bacterial conjunctivitis market stood at USD 185.99 million in 2018, with projections to reach USD 344.80 million by 2032, growing at a CAGR of 4.7%. The region contributed approximately 4.9% of the global market share in 2024. The growth is primarily fueled by rising demand for ophthalmic treatments, urbanization, and increased availability of branded and generic eye care products. Gulf countries like the UAE and Saudi Arabia are investing in healthcare modernization, which supports early diagnosis and treatment of eye infections. Rising digital pharmacy services and medical tourism are also enhancing market penetration in the region.

Africa

Africa accounted for the smallest share of the bacterial conjunctivitis market, with a value of USD 90.66 million in 2018, expected to reach USD 133.78 million by 2032, growing at a CAGR of 2.9%. In 2024, the region held roughly 2.2% of the global market share. Limited access to eye care services, lack of awareness, and a shortage of healthcare professionals continue to hinder growth. However, non-governmental health initiatives, public awareness campaigns, and improving retail pharmacy networks are gradually contributing to better market outreach. South Africa leads in regional sales, followed by Nigeria and Kenya, supported by improving urban healthcare infrastructure.

Market Segmentations:

By Drug Class

- Fluoroquinolones

- Ciprofloxacin

- Ofloxacin

- Levofloxacin

- Moxifloxacin

- Gatifloxacin

- Besifloxacin

- Aminoglycosides

- Macrolides

- Erythromycin

- Azithromycin

- Others

By Dosage Form

By Distribution Channel

- Hypermarkets and Supermarkets

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the bacterial conjunctivitis market is characterized by the presence of several established pharmaceutical companies actively engaged in developing, manufacturing, and marketing ophthalmic antibiotics. Key players such as Actavis Plc., Akorn, Inc., Bayer AG, F. Hoffmann-La Roche Ltd., Merck & Co., Inc., Novartis AG, Pfizer, Inc., Santen Pharmaceutical Co., Ltd., and Cipla Ltd. dominate the market through robust product portfolios and global distribution networks. These companies focus on expanding their presence via strategic collaborations, product launches, and R&D investments aimed at developing next-generation antibiotics with reduced resistance profiles. The market also witnesses increasing emphasis on preservative-free formulations and combination therapies to improve treatment outcomes and patient compliance. Furthermore, competition is intensifying due to the entry of generic drug manufacturers offering cost-effective alternatives, especially in price-sensitive regions. Innovation, brand recognition, and regulatory approvals remain key differentiators as companies strive to gain a competitive edge in this evolving and highly fragmented market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Actavis Plc.

- Akorn, Inc.

- Bayer AG

- Hoffmann-La Roche Ltd.

- Merck & Co., Inc.

- Novartis AG

- Pfizer, Inc.

- Santen Pharmaceutical Co., Ltd.

- Cipla Ltd.

Recent Developments

- In January 2023, Harrow Health acquired the U.S. commercial rights to five Novartis ophthalmic products, including a bacterial conjunctivitis treatment, for a total of $175 million. The deal involved an upfront payment of $130 million and a potential $45 million milestone payment related to TRIESENCE. The acquired products include VIGAMOX(bacterial conjunctivitis treatment), MAXIDEX (steroid eye drop), and TRIESENCE (steroid injection).

- In May 2022, Santen Pharmaceutical’s legal entity was granted approval by the National Medical Products Administration (NMPA) in China to use Verkazia for the treatment of severe vernal keratoconjunctivitis (VKC) in children and adolescents aged four years and older.

Market Concentration & Characteristics

The Bacterial Conjunctivitis Market exhibits moderate market concentration, with a mix of global pharmaceutical giants and regional players. Leading companies such as Novartis AG, Pfizer, Bayer AG, and Cipla Ltd. hold significant market shares due to their established product portfolios, broad geographic presence, and strong distribution networks. It features a high degree of therapeutic standardization, with fluoroquinolones dominating treatment protocols due to their broad-spectrum efficacy. The market remains prescription-driven in developed economies, while over-the-counter availability is more common in developing regions. Product differentiation is limited, making pricing and brand reputation key competitive factors. Regulatory compliance and antibiotic stewardship influence market dynamics, especially in Europe and North America. Growth in the sector stems from rising infection rates, improved healthcare access, and expanding retail and online pharmacy networks. Market players focus on topical formulations, particularly preservative-free solutions, to meet patient preferences and address safety concerns. While the market benefits from recurring demand and wide applicability across age groups, challenges such as antibiotic resistance and regulatory hurdles impact growth potential.

Report Coverage

The research report offers an in-depth analysis based on Drug Class, Dosage Form, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The bacterial conjunctivitis market is expected to witness steady growth driven by increasing prevalence of eye infections globally.

- Demand for topical antibiotics will continue to dominate due to their ease of application and rapid therapeutic response.

- Fluoroquinolones will remain the preferred drug class owing to their broad-spectrum antibacterial activity and low resistance profile.

- Preservative-free and combination eye drop formulations are likely to gain wider acceptance among both patients and healthcare providers.

- Asia Pacific is projected to lead market expansion due to rising healthcare investments and increasing awareness of ocular hygiene.

- Online pharmacies and e-prescription platforms will play a greater role in distribution, enhancing accessibility and convenience.

- Key players are expected to focus on strategic collaborations, product innovation, and emerging market penetration to strengthen their market position.

- Regulatory emphasis on antibiotic stewardship will influence prescribing patterns and promote responsible drug use.

- Pediatric and elderly patient populations will drive demand for safer and more tolerable ophthalmic formulations.

- Technological advancements in diagnostic tools will enable early detection and prompt treatment, supporting overall market growth.