Banking as a Service Platform Market Overview:

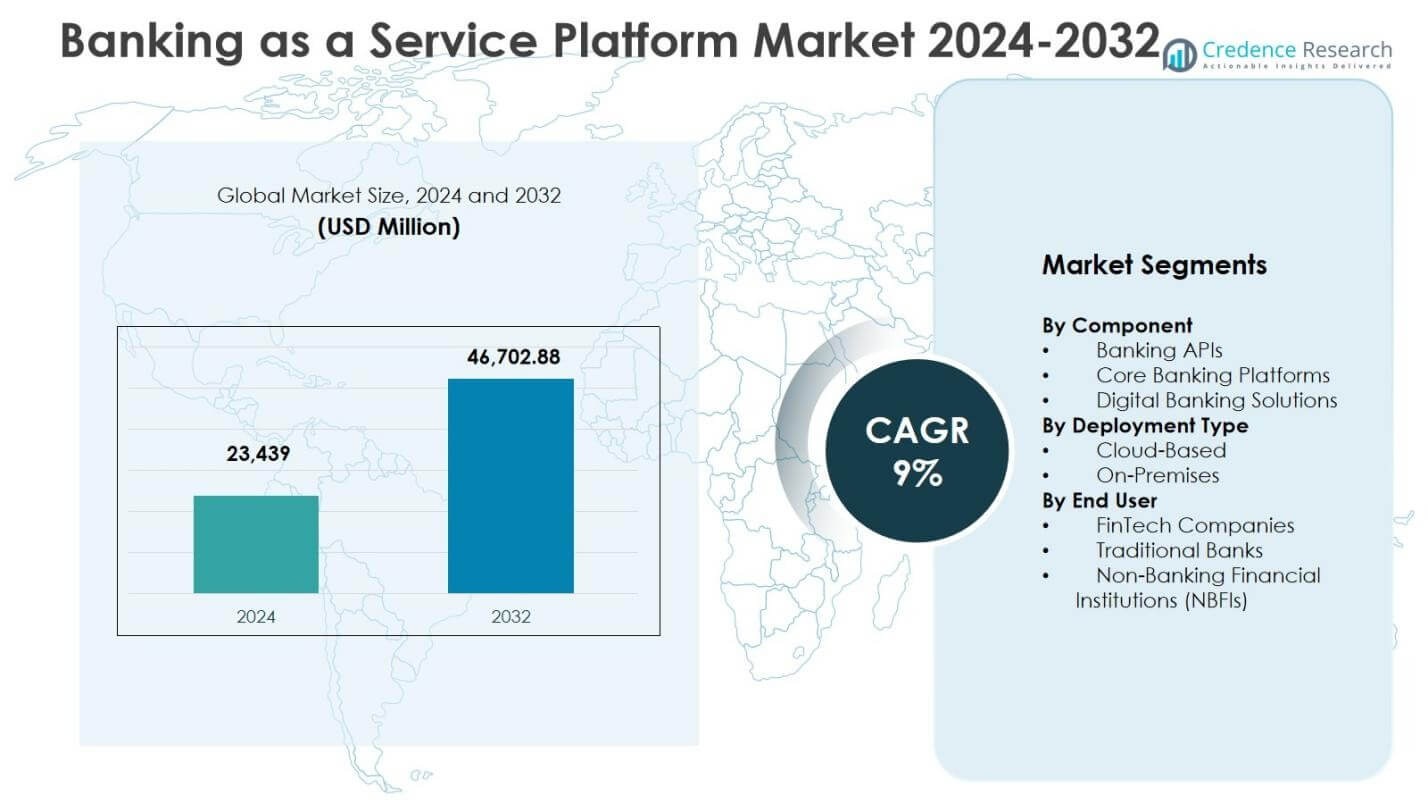

Banking as a Service Platform Market size was valued USD 23,439 Million in 2024 and is anticipated to reach USD 46,702.88 Million by 2032, at a CAGR of 9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Banking as a Service Platform Market Size 2024 |

USD 23,439 million |

| Banking as a Service Platform Market, CAGR |

9% |

| Banking as a Service Platform Market Size 2032 |

USD 46,702.88 million |

Banking as a Service Platform Market Insights

- Market growth is driven by rapid adoption of digital banking, FinTech expansion, cloud-based deployment, and supportive regulatory frameworks promoting open banking and API integration.

- Key trends include integration of AI, machine learning, and advanced analytics for predictive insights and personalized financial services, as well as the expansion of embedded finance and ecosystem partnerships across non-financial platforms.

- The market is led by players such as Mambu, Solaris SE / Solarisbank AG, Railsr, ClearBank, Green Dot, Stripe, Antier Solutions, Nadcab Labs, PayPal, and MatchMove Pay, focusing on innovation, security, and scalable solutions.

- North America dominates with 36.8% share, Europe holds 28.4%, Asia-Pacific accounts for 22.1%, Latin America 7.6%, and Middle East & Africa 5.1%, reflecting regional adoption of cloud-based and API-driven platforms.

Banking as a Service Platform Market Segmentation Analysis:

By Component:

The Banking as a Service Platform market is segmented into Banking APIs, Core Banking Platforms, and Digital Banking Solutions. In 2024, Banking APIs emerged as the dominant sub-segment, accounting for 42.5% of the market share, driven by the increasing demand for seamless integration of financial services, faster product development, and enhanced customer experience. Core Banking Platforms and Digital Banking Solutions held 33.2% and 24.3% shares, respectively, supported by digital transformation initiatives and modernization of legacy banking systems. The adoption of APIs enables FinTechs and traditional banks to expand services efficiently, fueling overall market growth.

- For instance, ClearBank delivers a single API for real-time payments, account management, and Faster Payments integration, powering eCommerce and fintech startups with cloud-based scalability.

By Deployment Type:

The market is categorized into Cloud-Based and On-Premises deployment types. Cloud-Based solutions dominate the market with a 61.4% share in 2024, propelled by scalability, cost efficiency, and rapid deployment advantages. On-Premises deployment accounts for 38.6% of the market, primarily favored by traditional banks and NBFIs requiring higher control over data security and regulatory compliance. The growing adoption of cloud infrastructure in banking, coupled with increasing demand for remote financial services, drives the preference for cloud-based BaaS solutions across global markets.

- For instance, Solarisbank became Germany’s first fully cloud-based bank by deploying Mambu’s API-enabled core banking platform on AWS, enabling scalable lending services and partner integrations after a four-month implementation.

By End User:

The Banking as a Service Platform market serves FinTech Companies, Traditional Banks, and Non-Banking Financial Institutions (NBFIs). In 2024, FinTech Companies dominate with a 48.7% market share, benefiting from the need to launch innovative financial products rapidly and enhance customer engagement. Traditional Banks hold 35.1% of the market, leveraging BaaS to modernize legacy systems and expand digital offerings. NBFIs account for 16.2%, driven by the desire to offer embedded financial services without extensive infrastructure investment. The overall growth is fueled by digital banking adoption and regulatory support for open banking initiatives.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rapid Adoption of Digital Banking and FinTech Expansion

The growth of the Banking as a Service Platform market is propelled by the rapid adoption of digital banking and the expansion of FinTech companies. Financial institutions and startups increasingly leverage BaaS platforms to launch innovative products, enhance customer experience, and reduce time-to-market. The rising demand for mobile banking, embedded finance, and seamless digital payments drives platform adoption. In 2024, this driver contributes significantly to market expansion, particularly in North America and Europe, where regulatory frameworks and consumer preference for digital services accelerate the deployment of Banking APIs, core banking modernization, and cloud-based solutions.

- For instance, Mambu empowers banks and fintechs with its cloud-native core banking platform, enabling rapid launches of digital products and embedded finance solutions through API-first architecture.

Regulatory Support and Open Banking Initiatives

Favorable regulatory policies and open banking initiatives globally act as a key growth driver for the Banking as a Service Platform market. Governments and financial authorities encourage the sharing of financial data through APIs, fostering innovation and competition. These regulations enable FinTechs and banks to offer customized financial products, facilitate secure transactions, and expand their service portfolio without heavy infrastructure investment. Open banking initiatives in Europe, North America, and Asia-Pacific have accelerated platform adoption, allowing institutions to integrate with multiple partners efficiently and enhancing financial inclusivity for consumers and businesses alike.

- For instance, under the UK’s PSD2 framework, Finexer’s FCA-authorised platform connects to 99% of UK banks, enabling businesses to deploy payment initiation and data services 2-3 times faster while ensuring regulatory compliance.

Cost Efficiency and Scalability through Cloud Deployment

Cloud-based deployment of Banking as a Service Platforms provides significant cost efficiency and scalability, fueling market growth. Cloud solutions reduce the need for extensive on-premises infrastructure, lowering operational costs while enabling rapid scaling to meet growing customer demand. Financial institutions benefit from flexible integration, automated updates, and minimal IT maintenance. In 2024, cloud adoption drives over 60% of market activity, especially among FinTechs and emerging banks, supporting expansion into new geographies. The ability to deploy and scale services quickly in response to dynamic market conditions reinforces the preference for cloud-based BaaS solutions and accelerates overall market adoption.

Key Trends & Opportunities

Integration of AI, Machine Learning, and Advanced Analytics

The Banking as a Service Platform market is witnessing the integration of AI, machine learning, and advanced analytics, creating opportunities for smarter financial services. These technologies enable predictive insights, fraud detection, personalized customer engagement, and automated decision-making. Providers leverage data-driven analytics to offer tailored banking solutions, optimize operations, and improve risk management. In 2024, institutions increasingly adopt AI-powered BaaS platforms to enhance product offerings, streamline workflows, and gain competitive advantage. The trend of embedding AI-driven features presents opportunities for FinTechs and banks to differentiate themselves, increase customer retention, and drive operational efficiency across multiple service lines.

- For instance, JPMorgan Chase deployed its COiN platform, which leverages AI to analyze commercial loan agreements in seconds tasks that once took 360,000 hours annually extracting terms and flagging risks with high accuracy.

Expansion of Embedded Finance and Ecosystem Partnerships

Embedded finance and strategic ecosystem partnerships are emerging as key trends in the Banking as a Service Platform market. Companies integrate banking services directly into non-financial applications, such as e-commerce, ride-sharing, and retail platforms, enhancing user convenience and engagement. This trend creates significant growth opportunities for BaaS providers to expand their footprint beyond traditional banking channels. Partnerships with technology platforms, FinTechs, and merchants enable seamless payments, lending, and account management. In 2024, embedded finance adoption accelerates revenue streams for both providers and end-users, allowing BaaS platforms to capitalize on the growing demand for integrated financial experiences across industries.

- For instance, Shopify embeds payments and multiple credit products, including term loans and revenue-based financing via Shopify Capital, directly into its merchant platform, with WebBank acting as its BaaS provider to underwrite and originate the loans using merchants’ transaction data.

Key Challenges

Data Security, Privacy, and Regulatory Compliance

Data security, privacy, and compliance present significant challenges for the Banking as a Service Platform market. BaaS providers handle sensitive financial and personal information, making them susceptible to cyberattacks, fraud, and data breaches. Ensuring compliance with diverse regulatory frameworks across multiple regions, including GDPR in Europe and consumer protection laws in North America and Asia-Pacific, adds complexity. In 2024, stringent data protection requirements increase operational costs and necessitate advanced security measures. Providers must invest in encryption, multi-factor authentication, and secure API protocols while balancing innovation and compliance, creating ongoing challenges in managing risk without limiting service offerings.

Integration with Legacy Systems and Technical Complexity

Integrating Banking as a Service Platforms with legacy banking systems remains a major challenge. Traditional banks often rely on outdated core systems that are difficult to modernize, leading to technical complexity, increased implementation time, and higher costs. In 2024, these integration challenges hinder seamless API connectivity, real-time data processing, and platform scalability. Providers must invest in middleware, system redesign, and skilled IT resources to ensure smooth integration. The complexity of aligning legacy infrastructure with modern cloud-based or API-driven solutions slows adoption, especially among established financial institutions, creating barriers to market growth despite strong demand for digital transformation.

Regional Analysis

North America

North America leads the Banking as a Service Platform market with a 36.8% share in 2024, driven by advanced financial infrastructure, high FinTech adoption, and supportive regulatory frameworks. The presence of key players such as Stripe, Green Dot, and PayPal accelerates market growth, while demand for digital banking solutions, cloud-based deployment, and embedded finance fuels expansion. U.S. and Canada witness significant investments in Banking APIs and core banking modernization. Rapid adoption of mobile banking, open banking initiatives, and partnerships between FinTechs and traditional banks further reinforce North America’s dominant position, positioning the region for sustained growth through 2032.

Europe

Europe holds a 28.4% share of the Banking as a Service Platform market in 2024, primarily driven by regulatory support through PSD2 and open banking directives. Countries such as the UK, Germany, and France are early adopters of API-based banking solutions, enabling FinTechs and traditional banks to innovate efficiently. The rising trend of embedded finance and cloud-based deployment enhances operational efficiency and customer engagement. Leading BaaS providers like Solarisbank AG and Railsr strengthen the ecosystem through strategic partnerships and technological innovation. Continuous investment in digital banking infrastructure ensures Europe maintains a strong growth trajectory throughout the forecast period.

Asia-Pacific

Asia-Pacific accounts for 22.1% of the Banking as a Service Platform market in 2024, fueled by rapid FinTech expansion, increasing smartphone penetration, and government initiatives promoting digital payments. Countries like China, India, and Australia are witnessing significant adoption of cloud-based BaaS platforms to provide innovative financial services. Rising demand for digital wallets, lending platforms, and embedded finance in e-commerce drives market growth. Regional players and international BaaS providers collaborate to expand service offerings, enabling financial inclusion and improving operational efficiency. The growing middle-class population and increasing digital literacy contribute to sustained market momentum across Asia-Pacific.

Latin America

Latin America holds a 7.6% share of the Banking as a Service Platform market in 2024, supported by the growing FinTech ecosystem and increasing demand for digital banking solutions. Countries such as Brazil, Mexico, and Argentina focus on financial inclusion, mobile banking adoption, and API-based services. Cloud deployment is becoming a preferred choice due to cost-effectiveness and scalability. Partnerships between local banks and BaaS providers facilitate seamless integration of digital services, including payments and lending. Despite regulatory and infrastructure challenges, the region demonstrates steady growth driven by rising smartphone penetration, increasing digital literacy, and the need for accessible financial solutions.

Middle East & Africa

The Middle East & Africa region accounts for 5.1% of the Banking as a Service Platform market in 2024, driven by emerging FinTech hubs in the UAE, Saudi Arabia, and South Africa. Investments in digital banking infrastructure, mobile payments, and cloud-based BaaS solutions accelerate adoption. Government initiatives promoting financial inclusion and innovation provide a favorable environment for platform deployment. Regional banks increasingly partner with global BaaS providers to deliver customized financial services. The growing demand for digital wallets, lending platforms, and embedded finance solutions among tech-savvy populations supports market expansion, positioning the region for incremental growth during the forecast period.

Banking as a Service Platform Market Segmentations:

By Component

- Banking APIs

- Core Banking Platforms

- Digital Banking Solutions

By Deployment Type

By End User

- FinTech Companies

- Traditional Banks

- Non-Banking Financial Institutions (NBFIs)

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Banking as a Service Platform market includes key players such as Mambu, Solaris SE / Solarisbank AG, Railsr, ClearBank, Green Dot, Stripe, Antier Solutions, Nadcab Labs, PayPal, and MatchMove Pay. These companies focus on expanding their service portfolios through cloud-based solutions, Banking APIs, and digital banking platforms to cater to FinTechs, traditional banks, and NBFIs. Strategic partnerships, mergers, and acquisitions enable providers to strengthen geographic presence and integrate advanced technologies such as AI, machine learning, and advanced analytics. The market is characterized by high innovation, with firms investing heavily in security, compliance, and scalable infrastructure. North America and Europe remain dominant regions due to early adoption and supportive regulatory frameworks. Companies differentiate through embedded finance offerings, real-time payments, and customizable solutions, while competition intensifies around API integration, cost efficiency, and seamless customer experience to capture a growing digital banking and FinTech market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Mambu

- Solaris SE / Solarisbank AG

- Railsr (formerly Railsbank)

- ClearBank

- Green Dot

- Stripe

- Antier Solutions

- Nadcab Labs

- PayPal (BaaS offerings)

- MatchMove Pay

Recent Developments

- In November 2025, BKN301, a fintech architecture provider offering digital banking platforms integral to Banking as a Service (BaaS), acquired Planky, a UK-based company specializing in AI-powered financial analytics and open banking solutions.

- In October 2025, Mambu also launched a composable banking approach for North American credit unions, enabling them to modernize legacy systems with modular infrastructure and enhance digital services.

- In October 2025, Mambu extended its multi‑year partnership with Krom Bank, renewing a five‑year agreement to accelerate digital banking innovation and expand financial product offerings in Indonesia.

Report Coverage

The research report offers an in-depth analysis based on Component, Deployment Type, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Banking as a Service Platform adoption will continue to grow rapidly driven by digital transformation across financial services.

- Cloud-based BaaS solutions will see increased deployment due to scalability and cost efficiency.

- FinTech companies will remain the primary adopters, expanding innovative financial products and services.

- Integration of AI, machine learning, and advanced analytics will enhance personalization and risk management.

- Embedded finance across e-commerce, retail, and non-financial platforms will create new growth opportunities.

- Open banking initiatives and regulatory support will drive cross-border API-based services.

- Traditional banks will increasingly modernize legacy systems using BaaS to remain competitive.

- Strategic partnerships and collaborations between BaaS providers and financial institutions will strengthen market presence.

- Security, privacy, and compliance solutions will remain critical to support market expansion.

- Emerging markets in Asia-Pacific, Latin America, and Middle East & Africa will witness accelerated BaaS adoption.