| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Big Data in Healthcare Market Size 2024 |

USD 38,165.37 million |

| Big Data in Healthcare Market, CAGR |

14.17% |

| Big Data in Healthcare Market Size 2032 |

USD 1,18,362.87 million |

Market Overview

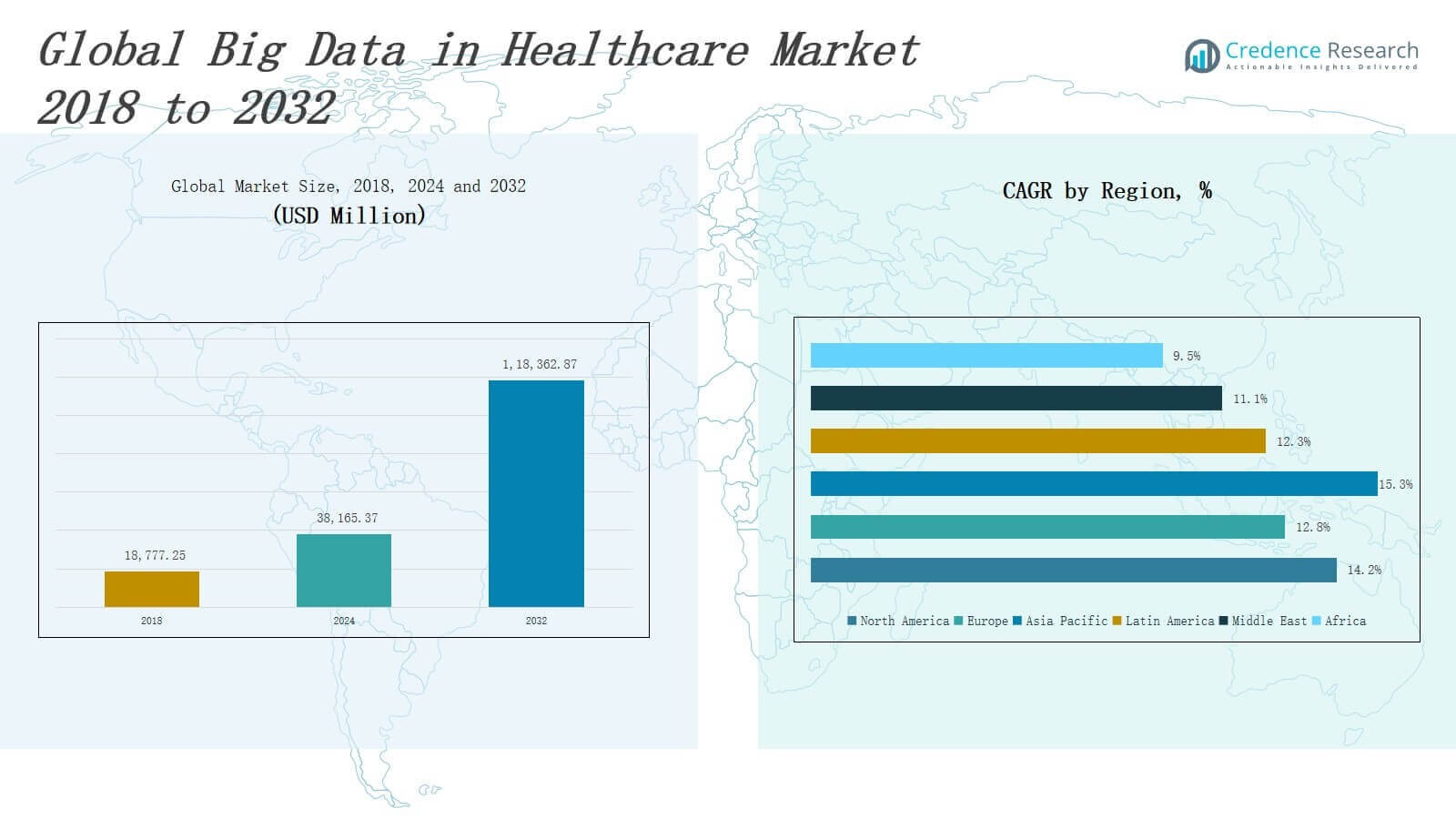

The Big Data in Healthcare Market size was valued at USD 18,777.25 million in 2018 to USD 38,165.37 million in 2024 and is anticipated to reach USD 1,18,362.87 million by 2032, at a CAGR of 14.17 % during the forecast period.

The Big Data in Healthcare Market is driven by the increasing demand for cost-effective and value-based care, rapid digital transformation, and growing volumes of healthcare data from electronic health records (EHRs), wearables, and remote monitoring systems. Healthcare providers are leveraging big data analytics to improve clinical decision-making, enhance patient outcomes, and streamline operations. The rise in chronic diseases and personalized medicine fuels demand for predictive analytics and real-time data processing. Additionally, government initiatives promoting data interoperability and the integration of artificial intelligence and machine learning into health IT systems are accelerating adoption. Cloud-based analytics platforms are gaining traction for their scalability and ability to manage unstructured and structured data securely. Moreover, the shift toward preventive care and population health management is prompting organizations to utilize big data for early disease detection and risk stratification. Strategic partnerships among healthcare firms, IT providers, and research institutions continue to shape innovation and expand the market’s application scope.

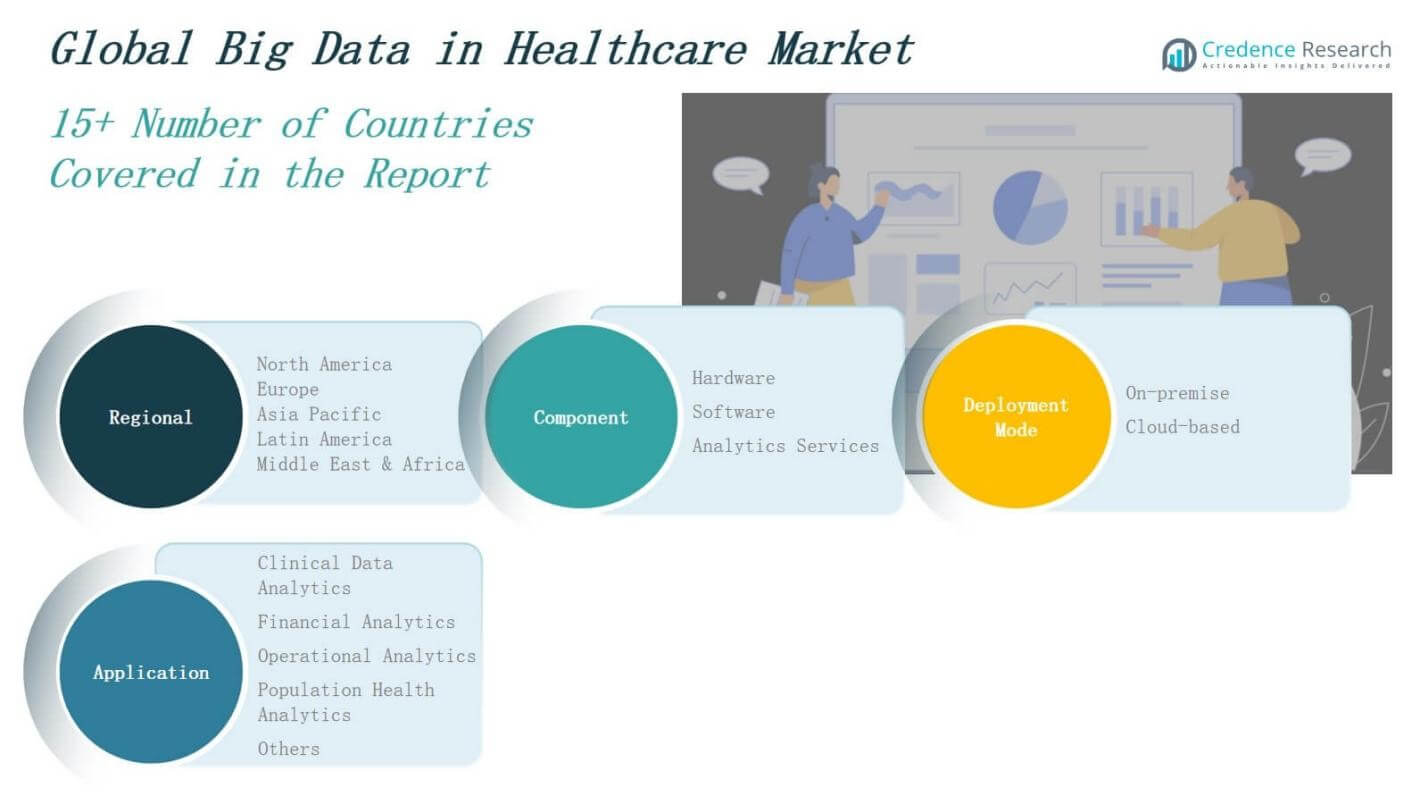

The Big Data in Healthcare Market spans six major regions: North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. North America leads the market due to robust digital infrastructure and strong investment in health IT, followed by Europe with growing precision medicine initiatives. Asia Pacific shows the fastest growth, driven by large patient populations and rising healthcare digitization. Latin America, the Middle East, and Africa present emerging opportunities through public health reforms and mobile health adoption. Key players operating across these regions include Amazon Web Services (AWS), Microsoft, Oracle, IBM, Accenture, Teradata, Tata Elxsi, Altamira.ai, Nagarro, Nous Infosystems, Athena Global Technologies, Akka Technologies, and Atom Consultancy Services. These companies compete through cloud-based solutions, AI integration, and regional expansion strategies tailored to local healthcare systems and regulatory landscapes.

Market Insights

- The Big Data in Healthcare Market is projected to grow from USD 18,777.25 million in 2018 to USD 1,18,362.87 million by 2032, registering a CAGR of 14.17%.

- Value-based care models and personalized medicine are accelerating demand for analytics that improve clinical outcomes and reduce costs.

- Healthcare data volumes from EHRs, wearables, and telehealth platforms are driving real-time analytics adoption and operational efficiency.

- Cloud-based platforms and AI-powered tools support scalable, secure data management and predictive healthcare applications.

- Key players include AWS, Microsoft, Oracle, IBM, Accenture, Teradata, Tata Elxsi, and Altamira.ai, focusing on AI integration and regional expansion.

- North America holds the largest share; Asia Pacific shows the fastest growth; Europe, Latin America, the Middle East, and Africa contribute through digital health reforms.

- Privacy regulations, data silos, and interoperability remain market challenges, but public-private partnerships and regulatory support are enabling progress.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Value-Based and Personalized Healthcare

The Big Data in Healthcare Market is fueled by the global transition toward value-based care models focused on improving patient outcomes while reducing costs. Healthcare providers are using data analytics to personalize treatment plans and optimize clinical workflows. Big data enables early identification of at-risk populations and supports precision medicine strategies. Governments and insurers are encouraging data-driven reimbursement models. It empowers clinicians to shift from reactive to proactive care. The ability to aggregate and analyze vast patient datasets enhances diagnostic accuracy, leading to more targeted interventions.

- For instance, Carrum Health’s value-based care model enabled a patient named Frank to undergo hip replacement surgery with a coordinated care team, resulting in a shorter hospital stay, faster rehabilitation, and lower costs compared to traditional fee-for-service approaches.

Expansion of Digital Health Infrastructure and Data Sources

The increasing adoption of electronic health records (EHRs), wearable devices, and telehealth platforms significantly boosts data generation, driving the Big Data in Healthcare Market. It captures a continuous stream of structured and unstructured data, creating new opportunities for advanced analytics. Integration of IoT in healthcare enhances real-time monitoring and remote patient management. Cloud computing supports scalable storage and faster processing. Healthcare systems rely on big data platforms to manage this growing digital footprint. Interoperable systems strengthen data sharing and collaboration among stakeholders.

- For instance, Neko Health launched a full-body scanning system that non-invasively collects thousands of health data points in minutes, including high-resolution 3D skin images and cardiovascular measurements.

Advancements in AI, Machine Learning, and Predictive Analytics

AI and machine learning integration in healthcare analytics is transforming how organizations extract insights from large datasets, driving the Big Data in Healthcare Market. Predictive models help forecast disease progression, optimize resource allocation, and support clinical decision-making. Natural language processing enables analysis of unstructured clinical notes. It enhances diagnostic tools and population health strategies. Hospitals are adopting AI-powered platforms to identify treatment gaps. These technologies increase operational efficiency and reduce error margins in diagnosis and care delivery.

Government Initiatives and Regulatory Support

Policy frameworks and government mandates are playing a crucial role in accelerating the Big Data in Healthcare Market. National healthcare IT programs promote digitization and data standardization across care settings. Regulatory bodies support secure data exchange through mandates like HIPAA and GDPR. Funding initiatives encourage data-driven innovation and research collaboration. It incentivizes public-private partnerships for big data projects. These efforts build trust in digital health systems and encourage widespread adoption of analytics tools.

Market Trends

Growing Integration of Predictive Analytics in Clinical Workflows

Healthcare providers are increasingly incorporating predictive analytics into daily clinical operations to support early diagnosis and treatment planning. The Big Data in Healthcare Market benefits from tools that analyze historical and real-time data to identify trends and forecast patient outcomes. It helps detect chronic disease risks, reduce hospital readmissions, and optimize treatment protocols. Hospitals use these insights to allocate resources more effectively and minimize unnecessary procedures. Predictive models support triage and emergency care decisions with greater accuracy.

- For instance, Corewell Health implemented AI-driven predictive analytics to identify patients at high risk of hospital readmission; by proactively addressing behavioral, clinical, and social factors, they prevented 200 readmissions and saved $5 million in costs.

Rising Use of Wearables and Remote Monitoring Devices

Wearables and IoT-enabled health devices are transforming data collection, contributing significantly to the Big Data in Healthcare Market. Patients and healthcare providers rely on these devices for continuous tracking of vital signs, fitness levels, and chronic conditions. It enables remote care management and supports early intervention. These data streams feed analytics platforms to deliver actionable insights in real time. Demand for home-based care further increases wearable usage. Integration with EHR systems improves visibility into patient behavior outside clinical settings.

- For instance, Apple Watch Series 4 and later models feature FDA-cleared ECG monitoring, allowing users to detect signs of atrial fibrillation and share real-time heart data with healthcare providers.

Adoption of Cloud-Based Big Data Platforms

Organizations are shifting toward cloud-based infrastructures to store, manage, and analyze growing healthcare datasets, advancing the Big Data in Healthcare Market. Cloud platforms offer scalability, cost-efficiency, and improved data accessibility across departments and institutions. It supports faster deployment of analytics applications and reduces the burden of on-premise infrastructure. Cloud adoption facilitates cross-border research collaboration and real-time analytics. Providers ensure compliance through secure architectures and encryption protocols. Hybrid and multi-cloud environments are also gaining traction for data flexibility.

Emphasis on Data Interoperability and Standardization

The push for interoperability is shaping the Big Data in Healthcare Market, with stakeholders seeking to harmonize diverse data sources. Interoperable systems allow seamless data exchange between labs, clinics, hospitals, and payers. It improves care coordination and eliminates data silos. Standardized formats and health information exchanges ensure data consistency. Industry bodies and governments are establishing protocols to enforce interoperability mandates. Unified data access strengthens population health insights and enables more precise public health strategies.

Market Challenges Analysis

Data Privacy, Security, and Compliance Risks

The Big Data in Healthcare Market faces critical challenges related to patient data privacy, security breaches, and regulatory compliance. Healthcare data is highly sensitive, making it a prime target for cyberattacks and unauthorized access. Organizations must navigate complex regulations such as HIPAA, GDPR, and national data protection laws, which vary across regions. It increases the burden on providers to implement robust data governance frameworks and encryption protocols. Limited cybersecurity expertise in some institutions compounds these risks. Compliance failures can lead to reputational damage and legal penalties.

Data Integration and Interoperability Barriers

Integrating diverse datasets from EHRs, imaging systems, wearable devices, and legacy platforms remains a major obstacle in the Big Data in Healthcare Market. Many healthcare systems still operate in silos, creating fragmented data landscapes that hinder holistic analysis. Inconsistent data formats, lack of standardization, and incompatible technologies slow down integration efforts. It impacts the ability to generate real-time insights and make data-driven decisions. Interoperability requires not only technical alignment but also coordinated efforts across stakeholders. Resolving these issues is essential to unlocking the full potential of big data.

Market Opportunities

Expansion of Precision Medicine and Genomic Analytics

The Big Data in Healthcare Market presents strong opportunities in precision medicine, where analytics platforms can interpret genetic, clinical, and behavioral data to customize treatment plans. The growing availability of genomic sequencing data fuels demand for advanced analytics tools that support personalized therapies. Pharmaceutical companies and research institutions are investing in data-driven drug discovery and biomarker identification. It enables faster clinical trial design and improved patient targeting. Real-time analysis of multi-omics data can transform rare disease diagnostics. This trend opens doors for partnerships between tech firms and life sciences organizations.

Emergence of AI-Powered Decision Support Systems

Artificial intelligence integration into healthcare analytics platforms offers significant opportunities for growth in the Big Data in Healthcare Market. AI tools can automate data interpretation, assist in clinical decision-making, and reduce diagnostic errors. Hospitals and clinics can adopt intelligent systems to support triage, imaging analysis, and treatment recommendations. It improves operational efficiency and patient care outcomes. Investment in AI-driven predictive and prescriptive analytics is rising globally. This momentum enables scalable deployment of smart health solutions across public and private healthcare ecosystems.

Market Segmentation Analysis:

By Component

The Big Data in Healthcare Market is segmented into hardware, software, and analytics services. Hardware supports data storage and processing infrastructure, including servers and networking equipment. Software holds a dominant share due to rising adoption of data management, visualization, and analytics platforms across hospitals and clinics. It enables real-time data access and streamlines operations. Analytics services are gaining traction, with healthcare organizations relying on expert support for predictive modeling, risk assessment, and custom reporting solutions.

- For instance, Mount Sinai Health System uses advanced analytics software to analyze medical histories and lab results, enabling proactive management of chronic diseases and early identification of high-risk patients.

By Deployment Mode

Deployment in the Big Data in Healthcare Market is categorized into on-premise and cloud-based models. On-premise solutions remain preferred in institutions prioritizing full control over data security and compliance. However, cloud-based deployment is expanding rapidly due to its scalability, cost efficiency, and remote accessibility. It allows seamless integration with wearable tech and mobile applications. Cloud platforms also support collaboration among research institutions and care providers, promoting faster innovation in health analytics.

- For instance, Pfizer leverages Amazon Web Services (AWS) cloud infrastructure to accelerate the development and testing of new medicines, including facilitating the rapid global rollout of the COVID-19 vaccine by enabling secure data sharing and real-time collaboration among research teams worldwide.

By Application

The application segment includes clinical data analytics, financial analytics, operational analytics, population health analytics, and others. Clinical data analytics leads the market, offering actionable insights to improve diagnostics, treatment protocols, and patient outcomes. Financial analytics supports cost control and fraud detection in billing and insurance. Operational analytics enhances workflow efficiency and resource utilization. Population health analytics enables early disease detection and better chronic care management. The others segment covers R&D optimization and public health surveillance

Segments:

Based on Component

- Hardware

- Software

- Analytics Services

Based on Deployment Mode

Based on Application

- Clinical Data Analytics

- Financial Analytics

- Operational Analytics

- Population Health Analytics

- Others

Based on Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

The North America Big Data in Healthcare Market size was valued at USD 7,926.25 million in 2018 to USD 15,937.29 million in 2024 and is anticipated to reach USD 49,568.60 million by 2032, at a CAGR of 14.2% during the forecast period. North America holds the largest share of the Big Data in Healthcare Market, driven by strong digital infrastructure, early adoption of health IT, and favorable government initiatives. The U.S. leads in terms of investment in healthcare analytics, supported by federal programs encouraging value-based care and EHR optimization. Canada and Mexico are also increasing healthcare digitization efforts. It benefits from a robust presence of leading cloud service providers and tech-driven healthcare startups. Strong regulatory frameworks and high R&D spending further support regional growth.

Europe

The Europe Big Data in Healthcare Market size was valued at USD 3,536.51 million in 2018 to USD 6,797.74 million in 2024 and is anticipated to reach USD 19,188.12 million by 2032, at a CAGR of 12.8% during the forecast period. Europe represents a significant share in the Big Data in Healthcare Market, supported by rising demand for precision medicine, aging population, and chronic disease management. Countries like Germany, the UK, and France are advancing health analytics initiatives through public-private partnerships and digital health strategies. It is reinforced by strong data protection regulations such as GDPR, which influence the design of compliant analytics platforms. Research collaborations and AI investments also drive the expansion of data infrastructure across the region.

Asia Pacific

The Asia Pacific Big Data in Healthcare Market size was valued at USD 5,844.04 million in 2018 to USD 12,494.01 million in 2024 and is anticipated to reach USD 42,019.41 million by 2032, at a CAGR of 15.3% during the forecast period. Asia Pacific is the fastest-growing region in the Big Data in Healthcare Market, fueled by large patient populations, increasing healthcare investments, and rapid digital transformation. China, Japan, and India are at the forefront of analytics adoption, with growing government support for AI and smart health technologies. It benefits from expanding telemedicine and mobile health services that generate high data volumes. Public health initiatives and disease surveillance programs further accelerate market development. The region attracts global players due to its scale and emerging innovation hubs.

Latin America

The Latin America Big Data in Healthcare Market size was valued at USD 830.59 million in 2018 to USD 1,665.80 million in 2024 and is anticipated to reach USD 4,531.73 million by 2032, at a CAGR of 12.3% during the forecast period. Latin America shows steady growth in the Big Data in Healthcare Market, supported by efforts to modernize healthcare infrastructure and improve access to digital tools. Brazil and Mexico lead regional adoption, integrating analytics for population health and hospital management. It is seeing increased investment in cloud computing and health informatics. Regional health systems are prioritizing efficiency and transparency through real-time data monitoring. Government-backed digitization programs contribute to market expansion across urban and semi-urban settings.

Middle East

The Middle East Big Data in Healthcare Market size was valued at USD 436.20 million in 2018 to USD 794.74 million in 2024 and is anticipated to reach USD 1,991.28 million by 2032, at a CAGR of 11.1% during the forecast period. The Middle East market is advancing through smart healthcare projects and national eHealth strategies. Gulf countries such as the UAE and Saudi Arabia are investing in AI and cloud infrastructure to enhance service delivery. It benefits from public-private collaborations and pilot projects in predictive diagnostics. Hospitals in the region are increasingly deploying analytics platforms to optimize operations and manage chronic disease burdens. Cross-border research and medical tourism also support market activity.

Africa

The Africa Big Data in Healthcare Market size was valued at USD 203.66 million in 2018 to USD 475.81 million in 2024 and is anticipated to reach USD 1,063.73 million by 2032, at a CAGR of 9.5% during the forecast period. Africa represents an emerging opportunity within the Big Data in Healthcare Market, led by mobile health expansion and international aid for healthcare innovation. Countries like South Africa, Kenya, and Egypt are deploying data solutions in disease tracking and telehealth. It faces infrastructure and interoperability challenges but is making progress through public health partnerships and donor-funded programs. Digital health startups are introducing low-cost, scalable analytics platforms. Regional governments are promoting technology to strengthen primary care delivery and health surveillance systems.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Accenture

- Amazon Web Services (AWS)

- Microsoft

- Oracle

- Teradata

- Tata Elxsi

- Akka Technologies

- ai

- Athena Global Technologies

- Atom Consultancy Services (ACS)

- Nagarro

- Nous Infosystems

Competitive Analysis

The Big Data in Healthcare Market features a competitive landscape driven by rapid technological advancements, strategic partnerships, and platform innovations. Leading players such as Amazon Web Services (AWS), Microsoft, Oracle, and IBM focus on expanding cloud-based analytics offerings and AI-driven tools. It reflects growing demand for scalable, secure data platforms across clinical and administrative functions. Companies like Accenture and Tata Elxsi provide specialized consulting and integration services tailored to healthcare institutions. Startups and mid-sized firms are introducing niche solutions in population health and predictive analytics. Market participants invest in R&D, data security enhancements, and regional expansion to strengthen their market position. Competitive differentiation hinges on interoperability, regulatory compliance, and ability to deliver actionable insights from large, diverse datasets. Strategic mergers and collaborations continue to shape the market, allowing companies to accelerate innovation and broaden their service portfolios.

Recent Developments

- In 2024 Epic Systems partnered with Mayo Clinic and Abridge to develop generative AI tools that summarize nurse–patient conversations and embed them directly into electronic health records.

- In July 2025, Nordic Capital acquired Arcadia Solutions, a leading healthcare data analytics firm, to expand AI-driven population health capabilities.

- In January 2025, Servier expanded its partnership with Google Cloud to integrate AI and generative AI across drug development, production, and patient care systems.

- In April 2025, MedeAnalytics launched Health Fabric™ on the Snowflake AI Data Cloud to offer a next-generation platform for secure data collaboration and real-time healthcare analytics.

Market Concentration & Characteristics

The Big Data in Healthcare Market exhibits moderate to high market concentration, with a mix of global technology giants and specialized healthcare analytics firms shaping the competitive landscape. Leading companies such as Amazon Web Services, Microsoft, IBM, and Oracle hold substantial market share due to their extensive cloud capabilities, AI integration, and scalable platforms. It features rapid innovation cycles driven by demand for predictive analytics, population health management, and personalized care solutions. The market is characterized by strong regulatory influence, with data privacy, interoperability, and compliance standards playing a central role in product development and deployment. It supports high barriers to entry due to the need for robust infrastructure, advanced analytics capabilities, and domain expertise. Strategic collaborations between healthcare providers, technology vendors, and research institutions are common, enabling integrated offerings and accelerated time-to-market. The market also reflects growing demand for real-time data processing, patient-centric tools, and cross-platform compatibility in both developed and emerging regions.

Report Coverage

The research report offers an in-depth analysis based on Component, Deployment Mode, Application and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for AI-powered analytics tools will increase to support faster diagnostics and personalized treatment planning.

- Healthcare providers will adopt more real-time data platforms to enhance clinical decision-making and patient monitoring.

- Cloud-based solutions will gain traction due to their scalability, cost efficiency, and support for remote care.

- Integration of genomic and clinical data will advance precision medicine and targeted therapy development.

- Governments will implement stronger data interoperability frameworks to promote seamless information exchange.

- Predictive analytics will play a critical role in population health management and early disease detection.

- Investment in cybersecurity infrastructure will rise to address growing concerns around patient data privacy.

- Wearables and IoT medical devices will generate more actionable health data for analytics platforms.

- Public-private partnerships will expand to accelerate digital transformation in healthcare systems.

- Emerging markets will witness rapid adoption of big data tools driven by mobile health initiatives and infrastructure upgrades.