Bio decontamination Market Overview:

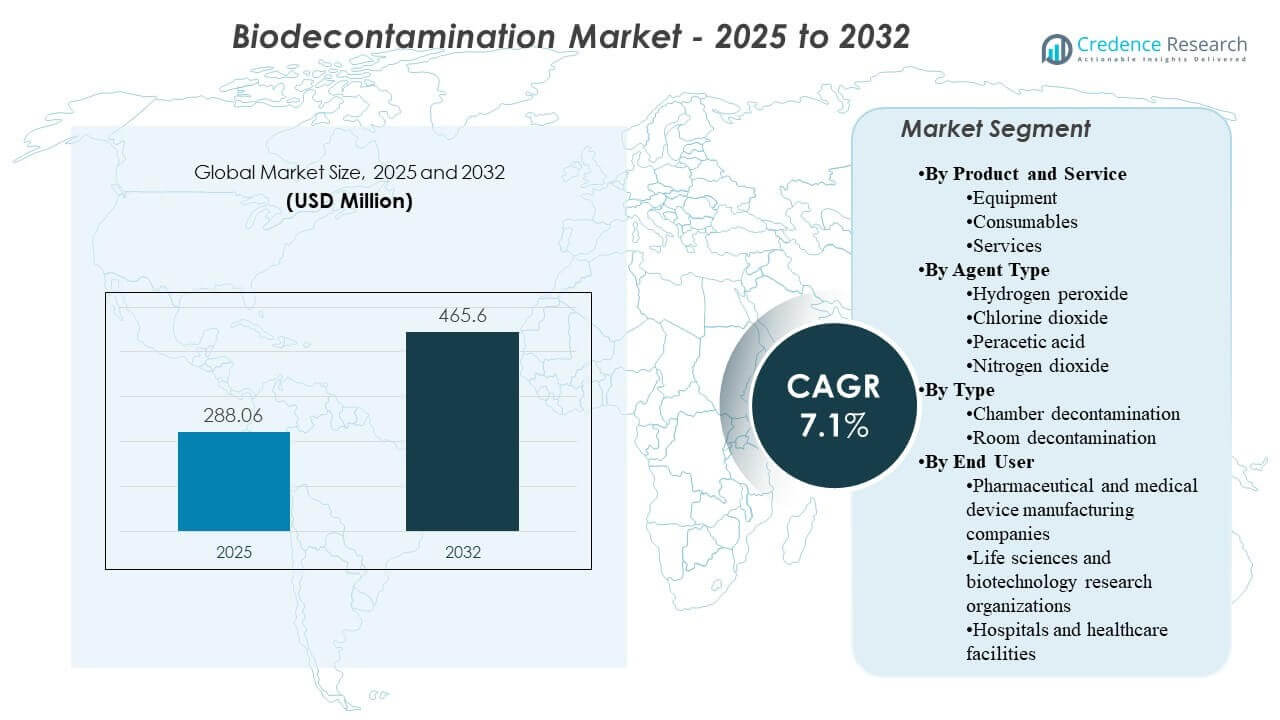

The global Bio decontamination Market size was estimated at USD 288.06 million in 2025 and is expected to reach USD 465.6 million by 2032, growing at a CAGR of 7.1% from 2025 to 2032. Growth is primarily driven by stricter contamination-control expectations across regulated manufacturing and critical healthcare environments, where audit-ready, repeatable decontamination cycles reduce batch-risk, downtime, and non-compliance exposure. Demand is also supported by capacity expansion in biologics, sterile fill-finish, and advanced research facilities, which increases the installed base of cleanrooms, isolators, and controlled areas that require routine bio decontamination.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bio Decontamination Market Size 2025 |

USD 288.06 million |

| Bio Decontamination Market, CAGR |

7.1% |

| Bio Decontamination Market Size 2032 |

USD 465.6 million |

Key Market Trends & Insights

- The Biodecontamination Market is projected to expand from USD 288.06 million (2025) to USD 465.6 million (2032) at a 7.1% CAGR (2025–2032).

- North America accounted for 41.30% of global revenue in 2025, reflecting high cleanroom density and compliance-driven adoption.

- Equipment held 47.6% share in 2025, supported by demand for validated, automated cycles and installed-base expansion in GMP environments.

- Hydrogen peroxide captured 49.9% share in 2025, driven by broad acceptance in regulated workflows and repeat-cycle suitability for rooms and enclosures.

- Chamber decontamination represented 59.2% share in 2025, indicating preference for controlled, repeatable treatment in enclosed spaces and transfer pathways.

Segment Analysis

The Biodecontamination Market is shaped by buyer preferences that prioritize validated microbial efficacy, repeatable cycle performance, and documentation that supports audits and facility qualification. Procurement decisions often emphasize operational fit, including cycle time, safety controls, material compatibility, and integration with facility workflows that limit production disruption. Biodecontamination deployments are increasingly evaluated as part of contamination-risk management, especially where sterile manufacturing, cleanroom operations, and high-criticality healthcare zones require reliable, standardized processes.

The Biodecontamination Market also reflects a mix of capital equipment demand and recurring consumption cycles, where installed systems drive ongoing use of consumables and service support. End users favor solutions that reduce manual variability and provide predictable outcomes across rooms, isolators, and chambers. Adoption remains strongest where contamination events carry high financial or patient-safety consequences, encouraging investment in automated biodecontamination methods and trained service delivery models.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product and Service Insights

Equipment accounted for the largest share of 47.6% in 2025. Equipment leads because automated systems enable repeatable cycle execution and verification aligned with regulated operating standards. Equipment adoption is strengthened by cleanroom expansion and modernization, where facilities require standardized decontamination across multiple zones and shifts. Equipment-led deployments also support long-term operating efficiency by improving consistency versus manual approaches and enabling faster, more controlled turnaround in critical spaces.

By Agent Type Insights

Hydrogen peroxide accounted for the largest share of 49.9% in 2025. Hydrogen peroxide-based approaches lead due to broad acceptance in regulated environments and suitability for repeat-cycle biodecontamination of rooms and enclosures. Agent selection is influenced by efficacy expectations, residue profile, safety procedures, and compatibility with sensitive equipment and materials. Hydrogen peroxide maintains strong positioning because buyers value established protocols, validation familiarity, and scalable deployment models across manufacturing and healthcare settings.

By Type Insights

Chamber decontamination accounted for the largest share of 59.2% in 2025. Chamber systems lead because they provide a controlled environment for consistent, repeatable biodecontamination cycles with clear verification pathways. Chamber formats align well with workflows involving enclosed assets, material transfer, and equipment handling where process control is critical. Chamber adoption is further supported by the need to reduce variability and improve cycle reproducibility in high-criticality contamination-control operations.

By End User Insights

Pharmaceutical and medical device manufacturing companies accounted for the largest share of 46.4% in 2025. This end-user group leads because regulated manufacturing relies on validated contamination-control processes to protect product sterility, batch integrity, and compliance outcomes. Biodecontamination demand rises with expansion of biologics, sterile manufacturing, and controlled environments that require routine, documented cycles. These buyers also tend to invest in standardized platforms and services that reduce operational risk and support consistent outcomes across multiple suites and facilities.

Bio Decontamination Market Drivers

Expansion of regulated manufacturing capacity and controlled environments

The Biodecontamination Market expands as pharmaceutical and medical-device manufacturers increase controlled-area capacity and tighten contamination-control practices. Cleanrooms, isolators, and sterile production zones require repeatable biodecontamination cycles to support batch integrity and compliance. Facility expansions increase the installed base of spaces requiring routine treatment, which supports both equipment adoption and recurring consumption cycles. Suppliers benefit as buyers seek solutions that integrate verification and documentation into standard operating procedures.

- For instance, Thermo Fisher Scientific’s Rochester facility already operated 10 daily cleanrooms, and MECART delivered an additional 20,000-square-foot GMP medical-device cleanroom there in under four months, showing how every controlled-space expansion increases the number of environments that need scheduled decontamination and documented release procedures.

Stronger compliance and quality expectations across life sciences operations

The Biodecontamination Market growth is supported by heightened expectations for audit-ready processes and predictable outcomes. Quality systems increasingly require standardized cycle performance, documented verification, and consistent execution across sites. Automated biodecontamination supports these needs by reducing human variability and enabling repeatable cycle control. Compliance-led procurement also favors vendors that provide robust validation support, operator training, and lifecycle service capabilities.

- For instance, STERIS states that its VHP 1000ED biodecontamination unit delivers a validated 6-log bioburden reduction cycle and uses automatic pressure control, leak testing, and onboard sensors for process monitoring, while also backing deployments with on-site operator training, installation, and qualification services.

Rising contamination-risk sensitivity in healthcare and critical facilities

The Biodecontamination Market is driven by infection-control priorities in hospitals and healthcare facilities, especially in high-risk zones and during heightened infection-prevention cycles. Healthcare operators value approaches that can reduce bioburden with reliable outcomes while minimizing disruption to clinical workflows. Adoption is also influenced by safety controls, ease of verification, and predictable turnaround time. These requirements increase demand for room and chamber solutions that can be deployed with clear procedures and measurable cycle outcomes.

Shift toward automation, verification, and service-supported deployments

The Biodecontamination Market benefits from a broader move toward automation in contamination-control workflows. Buyers increasingly prefer systems with controlled dosing, programmable cycles, and built-in monitoring that improves repeatability and operational efficiency. Service-supported models grow where facilities aim to reduce internal workload and ensure consistent execution by trained teams. Automation and service integration also strengthen adoption in multi-site operations that require standardized processes across regions and facility types.

Bio Decontamination Market Challenges

The Biodecontamination Market faces challenges linked to implementation complexity, where cycle design, facility airflow conditions, and space constraints can affect deployment speed and outcome consistency. End users may require specialized validation, staff training, and procedural alignment before scaling routine biodecontamination across multiple zones. Budget constraints can slow adoption in cost-sensitive healthcare settings, especially when decision makers prioritize short-term cost over lifecycle risk reduction.

The Biodecontamination Market also encounters operational hurdles related to agent handling, safety protocols, and material compatibility across diverse facility assets. Some sites require upgrades to monitoring, ventilation, or workflow design to support frequent cycles without impacting throughput. Supplier differentiation is challenged by proof requirements, where buyers demand strong verification practices and consistent field performance. These factors can lengthen sales cycles and increase the importance of technical support and service quality.

- For instance, Noxilizer reports that its nitrogen dioxide sterilization technology operates at 10°C to 30°C, typically uses NO2 exposure times of less than 1 hour, and delivers door-to-door cycle times of 6 to 12 hours, while also listing compatibility across materials, which shows why buyers closely assess safety handling, cycle fit, and material response before adoption.

Bio Decontamination Market Trends and Opportunities

The Biodecontamination Market shows increasing preference for solutions that combine automated cycle execution with verification indicators and documentation workflows. Buyers are aligning biodecontamination with broader quality-management systems, which raises demand for traceable cycle records and repeatable performance across sites. Opportunities expand for vendors that offer integrated platforms, training, and service delivery that reduces operational burden. Standardization across multi-facility operators also supports scalable deployments and recurring revenue from consumables and services.

The Biodecontamination Market is also seeing broader use cases beyond core cleanroom environments as contamination-control practices extend into adjacent controlled areas and transfer pathways. Modular facility growth and flexible manufacturing setups increase the need for adaptable systems that can be deployed across varying room sizes and operating constraints. Product positioning increasingly emphasizes cycle efficiency, operational safety, and compatibility with sensitive equipment. Vendors that can shorten downtime and improve workflow fit are better positioned to capture new adoption pockets.

- For instance, the STERIS VHP® VICTORY™ Biodecontamination Unit is engineered to handle single rooms of up to 566 m³ (20,000 ft³), and when up to 10 units are networked via Ethernet, the combined system can simultaneously decontaminate spaces of up to 5,000 m³ (175,000 ft³), with a hydrogen peroxide injection rate range of 5–35 g/minute and an airflow capability spanning 24–118 scfm.

Regional Insights

North America

North America accounted for 41.30% revenue share in 2025, supported by high density of regulated pharmaceutical and medical-device manufacturing and strong emphasis on standardized contamination-control processes. Demand is reinforced by cleanroom expansions, modernization programs, and quality-system expectations that favor repeatable, audit-ready biodecontamination cycles. The region also benefits from established service ecosystems and higher adoption of automation in critical facility operations.

Europe

Europe held an estimated 25.20% share in 2025, supported by a large base of GMP manufacturing sites and mature contamination-control standards across life sciences operations. Adoption is strengthened by quality-driven procurement and increased utilization of validated, standardized decontamination workflows. Market activity is concentrated in hubs with strong pharmaceutical manufacturing and biotechnology research infrastructure, supporting both equipment upgrades and recurring cycle demand.

Asia Pacific

Asia Pacific represented an estimated 21.10% share in 2025, reflecting rapid expansion of pharmaceutical manufacturing, biotechnology research capacity, and controlled-environment investments. Growth is supported by increasing standardization of quality and contamination-control practices across major production and research hubs. Adoption varies by country and facility maturity, but accelerating cleanroom buildouts and modernization initiatives support a growing installed base for routine biodecontamination.

Latin America

Latin America captured an estimated 6.40% share in 2025, driven by expanding regulated manufacturing footprints and improving healthcare infection-control practices. Adoption is typically concentrated in larger markets and leading hospital networks, where facilities prioritize contamination-risk reduction and process consistency. Budget sensitivity and uneven infrastructure modernization can moderate adoption pace, but growth opportunities expand as quality standards and controlled-environment capacity increase.

Middle East & Africa

Middle East & Africa accounted for an estimated 6.00% share in 2025, supported by healthcare modernization and selective growth in localized pharmaceutical manufacturing. Demand is concentrated in regions investing in advanced hospitals, laboratory infrastructure, and controlled environments. Adoption is influenced by availability of service capability, training, and facility readiness, creating opportunities for suppliers offering turnkey deployment and operational support.

Competitive Landscape

Competition in the Biodecontamination Market is shaped by differentiation in validated cycle performance, operational safety features, integration with facility workflows, and strength of service delivery. Companies compete on their ability to deliver repeatable outcomes across diverse environments, including cleanrooms, chambers, and patient-care settings. Commercial positioning also relies on lifecycle support, training, and documentation tools that help buyers maintain compliance and reduce operational variability. Partnerships and channel expansion remain important for scaling installations and supporting multi-site operators.

STERIS plc maintains a strong positioning in the Biodecontamination Market by emphasizing engineered solutions for controlled environments and repeatable, validated cycle execution aligned with regulated workflows. The company’s approach typically focuses on integrating biodecontamination into broader contamination-control strategies that support facility qualification and ongoing operations. STERIS plc also benefits from service and support capabilities that help end users standardize practices across facilities. This specialization supports adoption in high-criticality manufacturing and research environments where consistency and documentation are central procurement requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- STERIS plc

- Ecolab

- Bioquell

- TOMI Environmental Solutions, Inc.

- JCE Biotechnology

- Fedegari Autoclavi S.p.A.

- Noxilizer, Inc.

- ClorDiSys Solutions, Inc.

- Howorth Air Technology Limited

- Zhejiang Tailin Bioengineering Co., Ltd.

- Solidfog Technologies

- Cherwell Laboratories

- AM Instruments S.r.l.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, INDUS announced that its subsidiary M.BRAUN Inertgas-Systeme GmbH signed a purchase agreement to acquire Amira S.r.l., an Italian specialist in vaporized hydrogen peroxide biodecontamination solutions with more than 20 years of experience in laboratory and production sterilization and decontamination.

- In March 2025, TOMI Environmental Solutions announced a new OEM partnership with Pharma Biotech System Components/Pharmatech System Ltd. (PBSC) to strengthen its SteraMist Integrated System for high-containment material transfer and cleanroom decontamination applications. The company said the collaboration would add pass-through hatches and chambers engineered for optimized decontamination cycles, expanding SteraMist use in pharmaceutical, research, containment, and hospital environments.

- In January 2024, STERIS introduced a new line of hydrogen peroxide-based bio-decontamination systems designed with improved efficiency and faster cycle times to meet rising demand in healthcare and biotech settings.

- In January 2024, Allentown LLC acquired ClorDiSys for an undisclosed amount to expand its offerings in decontamination, disinfection, and sterilization services for biomedical research and life science markets.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 288.06 million |

| Revenue forecast in 2032 |

USD 465.6 million |

| Growth rate (CAGR) |

7.1% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product and Service Outlook: Equipment, Consumables, Services; By Agent Type Outlook: Hydrogen peroxide, Chlorine dioxide, Peracetic acid, Nitrogen dioxide; By Type Outlook: Chamber decontamination, Room decontamination; By End User Outlook: Pharmaceutical and medical device manufacturing companies, Life sciences and biotechnology research organizations, Hospitals and healthcare facilities |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

STERIS plc; Ecolab; Bioquell; TOMI Environmental Solutions, Inc.; JCE Biotechnology; Fedegari Autoclavi S.p.A.; Noxilizer, Inc.; ClorDiSys Solutions, Inc.; Howorth Air Technology Limited; Zhejiang Tailin Bioengineering Co., Ltd.; Solidfog Technologies; Cherwell Laboratories; AM Instruments S.r.l. |

| No. of Pages |

324 |

Segmentation

By product and service

- Equipment

- Consumables

- Services

By agent type

- Hydrogen peroxide

- Chlorine dioxide

- Peracetic acid

- Nitrogen dioxide

By type

- Chamber decontamination

- Room decontamination

By end user

- Pharmaceutical and medical device manufacturing companies

- Life sciences and biotechnology research organizations

- Hospitals and healthcare facilities

By region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa