Bioconjugation Market Overview;

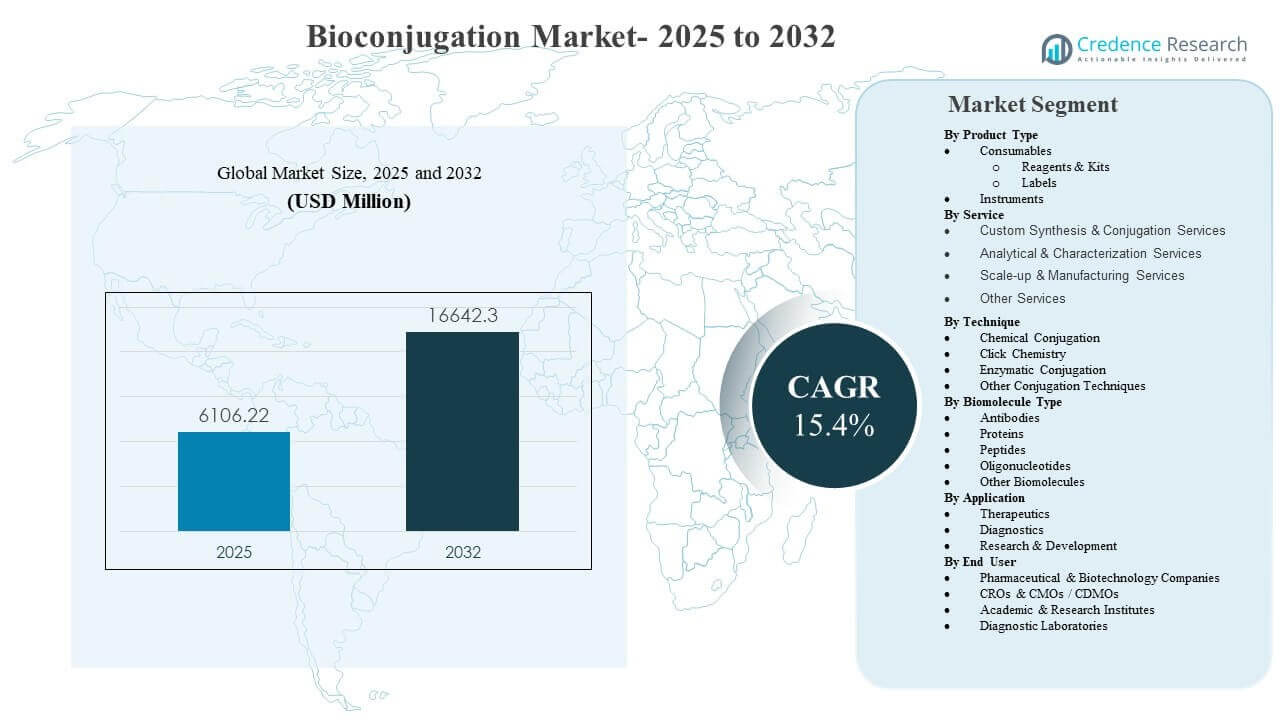

The global Bioconjugation Market size was estimated at USD 6106.22 million in 2025 and is expected to reach USD 16642.3 million by 2032, growing at a CAGR of 15.4% from 2025 to 2032. Demand is primarily driven by the rapid expansion of antibody drug conjugates and other targeted biologics that depend on reliable linker chemistry, reproducible conjugation, and scalable analytics from discovery to late-stage manufacturing. North America remains the largest geography in 2025, supported by a dense concentration of biopharma innovators, established CDMO capacity, and strong adoption of advanced life-science tools across R&D and regulated production environments.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bioconjugation Market Size 2025 |

USD 6106.22 million |

| Bioconjugation Market, CAGR |

15.4% |

| Bioconjugation Market Size 2032 |

USD 16642.3 million |

Key Market Trends & Insights

- The Bioconjugation Market is projected to expand from USD 6106.22 million (2025) to USD 16642.3 million (2032) at a 15.4% CAGR (2025–2032).

- North America accounted for 50.9% share in 2025, reflecting strong biopharma pipelines and mature bioprocess infrastructure.

- Consumables accounted for the largest share of 44.8% in 2025, supported by recurring demand for reagents, kits, and labeling chemistries.

- Therapeutics accounted for the largest share of 56.9% in 2025, driven by continued growth in targeted biologics and conjugate-based oncology programs.

- Chemical conjugation accounted for the largest share of 41.9% in 2025, underpinned by broad workflow compatibility and established protocols.

Segment Analysis

The Bioconjugation Market is shaped by two parallel demand centers: high-throughput discovery and clinically oriented scale-up. Consumables remain central to market momentum because conjugation and labeling workflows require repeated purchasing of reagents, kits, and dyes across method development, assay optimization, and quality testing. At the same time, the increasing complexity of bioconjugates elevates the importance of analytical and characterization steps, which lifts usage intensity across workflows that require reproducibility, stability profiling, and conjugate integrity verification.

Therapeutics is the largest application area because bioconjugation is a core enabling step for targeted modalities, including conjugate-based oncology programs that rely on controlled linker attachment and consistent product quality. Technique selection increasingly reflects the need for precision and manufacturability, with chemical conjugation continuing to lead due to its maturity and broad applicability across biomolecules. End-user demand is concentrated in pharmaceutical and biotechnology companies because pipeline ownership and clinical translation decisions are anchored in biopharma organizations, even when execution is partially outsourced to specialist partners.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Product Type Insights

Consumables accounted for the largest share of 44.8% in 2025. Consumables lead because conjugation and labeling activities require repeated purchases of reagents and kits across discovery, assay development, and quality testing workflows. Labels and chemistries are routinely used for detection, tracking, and functionalization steps that occur across multiple stages of development. Frequent method optimization and batch-to-batch verification also increase consumables pull-through compared with capital equipment replacement cycles.

Service Insights

Custom synthesis and conjugation services continue to gain attention because many programs require specialized handling of linkers, payloads, and controlled conjugation conditions. Analytical and characterization services remain critical for confirming conjugation efficiency, stability, and critical quality attributes across development stages. Scale-up and manufacturing services are increasingly relevant as more conjugate programs progress toward late-stage development and commercial readiness. Service demand is also strengthened by outsourcing strategies that prioritize speed, expertise, and access to regulated capabilities.

Technique Insights

Chemical conjugation accounted for the largest share of 41.9% in 2025. Chemical conjugation leads because established chemistries are broadly compatible with common biomolecules and are supported by mature protocols used across both research and production environments. The approach provides flexibility across payload types and is well integrated into standardized workflow kits and reagents. Continued investment in improved linker chemistries and better control strategies reinforces usage for programs that balance throughput, reproducibility, and manufacturability.

Biomolecule Type Insights

Antibodies remain the most prominent biomolecule type because antibody-based constructs are central to many targeted therapeutic strategies and immunoassay formats. Antibody conjugation is frequently required to enable delivery, detection, or potency enhancement, which keeps demand elevated across R&D and translational workflows. Peptides and proteins also sustain demand due to their roles in labeling, targeting, and diagnostic assay development. Oligonucleotides are increasingly relevant as nucleic-acid therapeutics and delivery innovations expand the need for stabilization and targeting conjugations.

Application Insights

Therapeutics accounted for the largest share of 56.9% in 2025. Therapeutics leads because targeted modalities increasingly rely on controlled conjugation to improve selectivity, reduce off-target exposure, and enhance efficacy. The scale-up requirements for therapeutic-grade conjugates also increase demand for repeatable processes and stringent analytical verification. Expanding oncology and precision medicine pipelines further strengthen therapeutic demand for robust conjugation chemistries and compatible manufacturing workflows.

End User Insights

Pharmaceutical & biotechnology companies accounted for the largest share of 46.9% in 2025. Pharmaceutical and biotechnology companies lead because pipeline ownership, clinical decision-making, and regulated development activities are concentrated within these organizations. Internal R&D groups require consistent conjugation workflows for discovery and optimization, and clinical teams require validated characterization to support progression decisions. Even when outsourcing is used, biopharma organizations remain the primary purchasing and specification-setting entities for tools, consumables, and service engagements.

Bioconjugation Market Drivers

Expansion of targeted therapeutics and conjugate pipelines

The Bioconjugation Market is driven by rising development of targeted therapeutics that require controlled attachment of payloads, labels, or functional groups. Growing use of conjugate-based modalities increases the need for repeatable chemistries, robust linkers, and validated workflows that can translate from discovery to regulated manufacturing. Program complexity also elevates demand for high-quality reagents and consistent conjugation performance across batches. These requirements sustain purchasing across consumables, instruments, and specialist services that support conjugate development.

- For instance, Abzena reports having developed more than 3,000 distinct linker–payload combinations to support antibody-drug conjugate programs from preclinical studies through commercial manufacturing, reflecting the breadth of chemistries required for targeted bioconjugates.

Increasing need for analytical validation and conjugate characterization

The Bioconjugation Market is supported by growing emphasis on confirming conjugation efficiency, stability, and critical quality attributes throughout development cycles. As conjugates become more complex, development teams require stronger analytical verification to maintain reproducibility and reduce downstream risk. Expanded characterization needs increase usage of instruments, assay reagents, and service-based analytical support. This dynamic strengthens demand across both in-house tool adoption and outsourced characterization models.

- For instance, a high‑throughput LC–MS workflow implemented with Protein Metrics’ Byos v5.4 software enabled automated processing of ADC biotransformation data over a 1.7–2.2 minute chromatographic window and produced quantification results that closely matched previous manual analyses while substantially reducing review time per dataset.

Outsourcing intensity for specialized conjugation and scale-up capabilities

The Bioconjugation Market benefits from outsourcing trends as companies seek specialized expertise for process development, scale-up, and regulated manufacturing preparation. Many organizations prefer external partners for complex conjugation workflows requiring specialized containment, linker handling, and method development. Outsourcing can reduce time-to-milestone for programs moving through clinical phases. As a result, services supporting custom synthesis, characterization, and manufacturing readiness gain strategic importance.

Broadening adoption across diagnostics and research workflows

The Bioconjugation Market is also driven by sustained adoption of labeling and conjugation methods in diagnostics and research environments. Assay development and biomarker detection routinely depend on labels, dyes, and conjugation kits that are used repeatedly across iterations. Research workflows increase demand for flexible chemistries that enable rapid method optimization and signal enhancement. These ongoing use cases create stable, recurring demand that reinforces consumables leadership.

Bioconjugation Market Challenges

The Bioconjugation Market faces challenges related to reproducibility and process control, particularly as programs demand tighter conjugation uniformity and robust stability performance. Variability in conjugation efficiency, linker attachment, or payload distribution can complicate development timelines and increase the need for additional characterization. These issues elevate development costs and place pressure on workflows to deliver consistent outcomes across batches. Complex handling requirements for certain payloads can further increase operational burden.

- For instance, Genentech reported that changing the antibody conjugation site from heavy‑chain position 115 to 114 in a next‑generation ADC reduced payload shedding by about six‑fold over a 72‑hour rat plasma stability study, illustrating how small process changes can dramatically improve conjugate stability and uniformity.

The Bioconjugation Market also encounters cost and capability barriers tied to specialized instrumentation, high-grade reagents, and advanced analytical workflows. Smaller organizations may rely on outsourcing because internal build-out can be capital intensive and operationally complex. Method standardization across multi-site programs can also be difficult when workflows vary across teams or vendors. Regulatory expectations for therapeutic-grade conjugates can heighten documentation and validation demands, increasing execution complexity.

Bioconjugation Market Trends and Opportunities

The Bioconjugation Market is seeing expanding interest in site-specific and precision conjugation approaches that improve product consistency and functional performance. Programs increasingly prioritize controlled attachment strategies that reduce heterogeneity and support better predictability in therapeutic outcomes. This trend increases opportunities for advanced reagents, next-generation linkers, and enabling analytics that support reliable control strategies. Vendors that offer workflow-integrated solutions can capture more value across development stages.

- For instance, Seagen’s site-specific ADC technology has enabled production of antibody–drug conjugates with tightly controlled drug‑to‑antibody ratios of 4.0 ± 0.1, which reduced batch‑to‑batch variability in binding activity to under 5 percent relative standard deviation across multiple clinical lots.

The Bioconjugation Market also presents opportunities through growing service integration, where providers combine custom synthesis, analytical characterization, and scale-up support under one operational umbrella. As pipeline timelines accelerate, integrated offerings can reduce handoffs and improve program continuity. Geographic expansion of advanced manufacturing capabilities strengthens regional access to conjugate development and supply readiness. Toolmakers and CDMOs that align offerings with late-stage manufacturability requirements are positioned to benefit.

Regional Insights

North America

North America accounted for 50.9% share in 2025, supported by a high concentration of biopharmaceutical innovators and strong adoption of advanced life-science tools. The region benefits from extensive clinical development activity and mature manufacturing ecosystems that require consistent conjugation workflows and validated analytics. A dense network of CROs, CDMOs, and specialized suppliers also supports rapid iteration and scale-up readiness.

Europe

Europe accounted for 26.3% share in 2025, driven by established biopharma R&D capacity and expanding biologics manufacturing footprints. Strong emphasis on quality systems and regulated production increases demand for analytical rigor and reproducible conjugation outcomes. Regional growth is reinforced by investments in advanced manufacturing capabilities and cross-border collaborations that support biologics and conjugate pipelines.

Asia Pacific

Asia Pacific accounted for 16.1% share in 2025, supported by expanding biopharma investment, growing contract manufacturing capacity, and increased adoption of advanced research tools. The region benefits from scaling biologics development programs and improving access to specialized conjugation and characterization services. Rising R&D intensity and manufacturing modernization create opportunities for both consumables and integrated service offerings.

Latin America

Latin America accounted for 4.2% share in 2025, with growth supported by expanding diagnostic usage and gradual strengthening of biopharma and research infrastructure. Market development is influenced by procurement constraints and variable access to specialized capabilities across countries. Demand is typically concentrated in major urban healthcare and research hubs where advanced assay and laboratory workflows are more prevalent.

Middle East & Africa

Middle East and Africa accounted for 2.5% share in 2025, with demand centered on select markets investing in healthcare modernization and laboratory capability build-out. Adoption is supported by gradual expansion of diagnostic testing capacity and growing research collaborations. The region remains comparatively smaller, with growth shaped by infrastructure development pace and access to specialized reagents and services.

Competitive Landscape

The Bioconjugation Market is characterized by competition between broad life-science tools providers and specialized service organizations that support conjugate development and manufacturing readiness. Companies compete through portfolio breadth across reagents, instruments, and workflow support, as well as through application-specific solutions that improve reproducibility and scalability. Differentiation is increasingly linked to enabling precision conjugation, strengthening analytical performance, and offering integrated development-to-manufacturing pathways. Strategic partnerships and capability expansion remain key approaches to improve coverage across therapeutic and diagnostic use cases.

Thermo Fisher Scientific maintains a broad footprint across conjugation reagents, labeling chemistries, and analytical workflows that support discovery through translational development. The company’s scale and product depth enable standardized workflows across multi-site programs and support repeatable performance across routine laboratory use. Thermo Fisher Scientific also benefits from alignment with biopharma and research customers seeking reliable consumables supply and compatible tool ecosystems. This positioning supports continued participation across both high-throughput research environments and regulated development workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Thermo Fisher Scientific

- Danaher Corporation

- Lonza Group

- Merck KGaA

- Sartorius AG

- AbbVie Inc.

- Agilent Technologies

- Bio-Rad Laboratories

- Catalent, Inc.

- Becton, Dickinson and Company (BD)

- Biosynth

- WuXi Biologics

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In October 2025, Invenra Inc. and Xcellon Biologics announced a collaboration to advance the development of bispecific and trispecific antibody drug conjugates (ADCs), leveraging Invenra’s B Body bispecific and T Body trispecific antibody discovery platforms together with Xcellon’s bioconjugation, ADC development, and manufacturing capabilities to generate and translate multispecific ADC candidates from discovery into preclinical and clinical development.

- In January 2025, Bio Rad Laboratories introduced its TrailBlazer Tag and TrailBlazer StarBright Dye Label Kits, a two kit system that allows researchers to conjugate StarBright dyes to virtually any antibody using SpyTag/SpyCatcher technology, simplifying custom antibody bioconjugation for high plex flow cytometry and fluorescent western blotting.

- In August 2024, Bio Rad Laboratories launched annexin V conjugated to eight StarBright dyes for flow cytometry, expanding its portfolio of ready to use fluorescent bioconjugates that enable more flexible and sensitive detection of early apoptotic cells in research applications.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 6106.22 million |

| Revenue forecast in 2032 |

USD 16642.3 million |

| Growth rate (CAGR) |

15.4% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type; By Service; By Technique; By Biomolecule Type; By Application; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Thermo Fisher Scientific, Danaher Corporation, Lonza Group, Merck KGaA, Sartorius AG, AbbVie Inc., Agilent Technologies, Bio-Rad Laboratories, Catalent, Inc., Becton, Dickinson and Company (BD), Biosynth, WuXi Biologics |

| No.of Pages |

332 |

Segmentation

By Product Type

By Service

- Custom Synthesis & Conjugation Services

- Analytical & Characterization Services

- Scale-up & Manufacturing Services

- Other Services

By Technique

- Chemical Conjugation

- Click Chemistry

- Enzymmatic Conjugation

- Other Conjugation Techniques

By Biomolecule Type

- Antibodies

- Proteins

- Peptides

- Oligonucleotides

- Other Biomolecules

By Application

- Therapeutics

- Diagnostics

- Research & Development

By End User

- Pharmaceutical & Biotechnology Companies

- CROs & CMOs / CDMOs

- Academic & Research Institutes

- Diagnostic Laboratories

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa