Bioherbicides Market Overview:

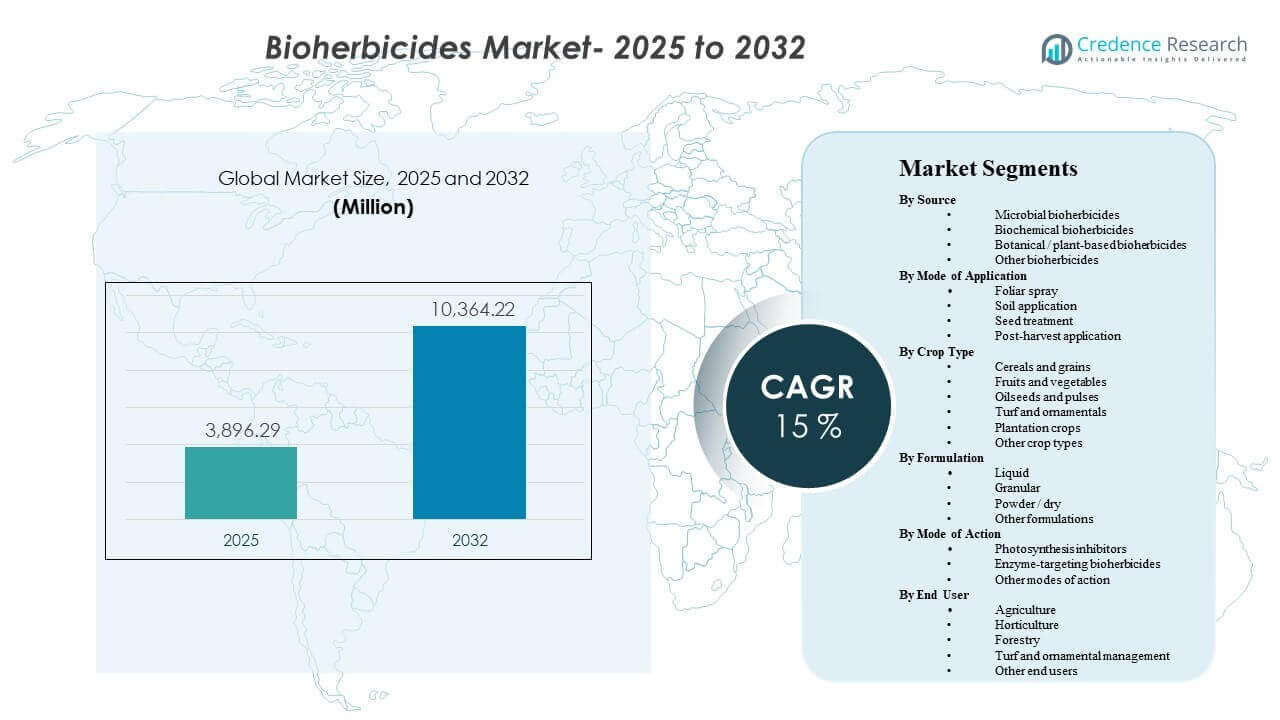

The global Bioherbicides Market size was estimated at USD 3,896.29 million in 2025 and is expected to reach USD 10,364.22 million by 2032, growing at a CAGR of 15% from 2025 to 2032. Regulatory tightening around synthetic herbicides and rising residue sensitivity in food supply chains are accelerating the adoption of biological weed management solutions across large-acre crops and specialty farming systems. North America continues to represent the largest regional revenue pool, supported by established biological input penetration, product availability, and stronger on-farm trialing ecosystems that speed commercialization and repeat usage.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bioherbicides Market Size 2025 |

USD 3,896.29 million |

| Bioherbicides Market, CAGR |

15% |

| Bioherbicides Market Size 2032 |

USD 10,364.22 million |

Key Market Trends & Insights

- The Bioherbicides Market is projected to expand from USD 3,896.29 million in 2025 to USD 10,364.22 million by 2032 at a CAGR of 15% during 2025–2032.

- North America represented 35.4% of global revenue in 2025, reflecting higher penetration of biological crop inputs and more frequent integration into integrated weed management programs.

- Microbial bioherbicides accounted for the largest share of 47.6% in 2025, supported by broadened product pipelines and compatibility with residue-sensitive and organic production systems.

- Seed treatment represented 42.8% in 2025, indicating strong preference for early-season, operationally efficient application formats that fit existing seed processing workflows.

- Agriculture end users accounted for 76.9% in 2025, driven by broad-acre volume demand and increasing pressure to diversify modes of action across weed management programs.

Segment Analysis

Bioherbicides adoption is increasingly shaped by end-user demand for residue-compatible weed management and by regulatory constraints that limit the use of certain synthetic herbicide actives. Market traction is strongest where biological inputs can be integrated into established agronomic workflows, including seed treatment and conventional spray programs, without materially increasing labor or operational complexity. Buyers typically evaluate products on field consistency across geographies, stability in storage and handling, and fit within resistance-management programs that require rotation and diversification of modes of action.

Product positioning is also shifting from “alternative inputs” to “program components,” where bioherbicides are used alongside cultural controls and selective chemistries to stabilize weed pressure across the season. This shift supports higher repeat usage in broad-acre agriculture, while specialty crop systems adopt bioherbicides to protect market access and compliance with buyer residue specifications. Formulation innovation remains central, as performance and shelf-life expectations directly influence distributor confidence and farm-level willingness to scale deployments.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Source Insights

Microbial bioherbicides accounted for the largest share of 47.6% in 2025. The segment leads because microbial actives are widely positioned for compatibility with residue-sensitive programs and for integration into integrated pest and weed management practices. Product development focus on strain selection, stability, and reproducible field performance supports broader label expansion across crop types. Microbial options also benefit from growing distribution familiarity and increasing comfort among agronomists in recommending biological modes of action.

By Mode of Application Insights

Seed treatment accounted for the largest share of 42.8% in 2025. This approach leads because it offers targeted delivery early in the crop cycle and fits standardized seed-processing operations without requiring additional field passes. Seed-applied formats can improve practicality on large-acre farms by reducing dependence on narrow in-season spray windows. The segment also benefits from the ability to combine bioherbicides with other seed-applied biologicals and crop protection inputs as part of integrated programs.

By Crop Type Insights

Fruits and vegetables accounted for the largest share of 28.2% in 2025. The segment leads because specialty crops face tighter residue requirements and higher value-at-risk per hectare, which supports willingness to adopt biological weed management. Short harvest intervals and strict retail and export specifications encourage the use of inputs aligned with stewardship and compliance needs. Frequent weed pressure cycles also favor solutions that can be applied as part of broader crop health and market-access strategies.

By Formulation Insights

Liquid formulations remain a widely preferred format because they align with established mixing, handling, and spray coverage practices in commercial farming systems. Liquid products can reduce friction in adoption by fitting existing equipment and operator habits, particularly where farms aim to maintain throughput during peak operational periods. Formulation performance is often assessed through stability, shelf life, and consistency across temperature and humidity conditions. Continued formulation innovation supports expansion into additional crop labels and application settings.

By End User Insights

Agriculture accounted for the largest share of 76.9% in 2025. The segment leads because broad-acre cropping drives the highest volume demand and is increasingly adopting biological tools to complement resistance-management strategies. Commercial agriculture also benefits from stronger dealer networks and larger-scale trialing, which can validate performance and support repeat purchasing. Integration into integrated weed management programs helps agriculture users balance efficacy expectations with stewardship, residue, and regulatory considerations.

Bioherbicides Market Drivers

Regulatory and residue-driven shift toward biological weed management

Restrictions and tighter oversight around synthetic herbicide actives are increasing the need for alternative weed control options that align with compliance and stewardship requirements. Bioherbicides benefit from positioning as residue-compatible tools that support buyer and export expectations, especially in sensitive supply chains. This dynamic supports stronger pull from specialty crops and gradually expands into broad-acre programs where integrated approaches are prioritized. As compliance pressure increases, farms are more likely to allocate budget to biological solutions that help protect market access.

- For instance, Belchim’s Beloukha Agricultural Herbicide contains 680 g/L pelargonic acid, is rainfast in 1 hour, and its Australian label states that withholding periods are not required when used as directed.

Resistance management and diversification of modes of action

Rising herbicide resistance pressure is pushing farms and advisors to diversify weed control approaches and reduce reliance on single-mode programs. Bioherbicides provide additional biological modes of action that can be incorporated into rotation strategies. This strengthens adoption where integrated weed management programs are already used, including combinations of chemical, biological, and cultural controls. Over time, greater resistance complexity increases the value of complementary solutions that can be deployed across multiple stages of the crop cycle.

- For instance, Harpe Bio reports more than 1,000 field and greenhouse trials, and in a South Dakota post-emergence evaluation its Harpe/saflufenacil tank mix delivered 88 percent control of lambsquarter at 3 days after application versus 73 percent for saflufenacil alone, while yellow foxtail control reached 78 percent at 7 days after application versus 0 percent for saflufenacil alone.

Expansion of organic and biologically aligned production practices

Growth in organic farming and the broader shift toward biologically aligned production practices support demand for weed control solutions compatible with certification and sustainability goals. Bioherbicides are increasingly evaluated as part of total biological input programs that include biostimulants and biopesticides. This supports multi-product bundling through distributors and advisers and can accelerate repeat adoption once performance is proven. The effect is especially visible in high-value crop systems where buyer requirements are strict and operational budgets can support specialized inputs.

Improving product performance through formulation and R&D investments

Ongoing R&D is improving bioherbicide stability, shelf life, application compatibility, and field consistency, which are central to scale-up decisions. Better formulations reduce adoption friction for distributors and growers by improving handling, storage, and reliability. Product development also supports expanded crop labels and broader geographic applicability, improving addressable market size. As performance consistency improves, bioherbicides are more likely to transition from niche applications into standard program components.

Bioherbicides Market Challenges

Bioherbicides adoption is constrained by variability in field performance across climates, soil types, and weed species, which can increase perceived risk for large-acre deployments. Buyers often demand predictable outcomes comparable to conventional herbicides, and inconsistent results can limit repeat purchasing. Shelf-life limitations and sensitivity to storage conditions can create distribution challenges, especially in regions with less developed cold chain or inventory turnover constraints. These factors increase the importance of formulation stability and strong agronomic support.

- For instance, Albaugh states that its plant-derived Beloukha bioherbicide shows visible effects within 2 hours and is rainfast within 2 hours, yet the company also notes that it works faster in sunny, hot weather and performs best at a 5% to 8% spray concentration, underscoring how even commercial products remain sensitive to field conditions and application parameters.

Cost and application complexity can also limit scale in price-sensitive farming contexts, particularly when bioherbicides require more precise timing or multiple applications. Growers may hesitate when the total program cost rises without clearly quantified yield or compliance benefits. Limited awareness and varying adviser confidence can slow diffusion in regions where biological inputs are newer. Registration timelines and label restrictions may further limit immediate expansion into new geographies and crop categories.

Bioherbicides Market Trends and Opportunities

Bioherbicides are increasingly being integrated into full-season weed management programs rather than positioned as stand-alone replacements. This creates opportunity for program-based selling, where suppliers emphasize compatibility with other biologicals, selective chemistries, and cultural controls. Wider adoption of integrated weed management approaches supports demand for products that can be used at multiple crop stages. Seed treatment deployment is also enabling earlier-season positioning and operational efficiency, increasing the addressable base in broad-acre cropping.

Product innovation is expanding into improved formulations, targeted delivery, and more robust microbial and botanical pipelines that aim to reduce performance variability. Growth opportunities are strongest where residue sensitivity is high and where buyers face strong compliance pressure, including specialty crops and export-oriented supply chains. Increasing distributor focus on sustainable input portfolios supports stronger channel visibility for biological weed control. As agronomic data accumulates from field trials, the market is positioned to broaden use cases and increase repeat adoption.

- For instance, Harpe Bioherbicide Solutions states that its plant extract-based platform has been evaluated in more than 1,000 global field and greenhouse trials, while its first issued patent, U.S. Patent No. 11,771,095, covers specific combinations of plant extracts and enhanced combinations with other synthetic or natural herbicides, and the company says these molecules are being formulated for pre-emergent, post-burndown, and desiccation applications.

Regional Insights

North America

North America accounted for 35.4% of global revenue in 2025. Regional demand is supported by established biological input penetration, stronger agronomic advisory ecosystems, and wider product availability through mature distribution networks. Adoption is reinforced by integrated weed management practices and increasing focus on resistance management. Commercial-scale trialing and better service coverage support repeat usage once performance is validated.

Europe

Europe represented 27.1% of global revenue in 2025. Demand is reinforced by strong sustainability and stewardship expectations, along with stringent compliance requirements that encourage biological alternatives in weed management programs. Adoption is supported by established professional farming systems and distributor-led product validation. The region also benefits from increasing integration of biological solutions into broader crop protection and regenerative agriculture frameworks.

Asia Pacific

Asia Pacific accounted for 20.7% of global revenue in 2025. Growth is supported by expanding adoption of biologically aligned inputs, increasing professionalization in horticulture and plantation crops, and rising emphasis on export quality standards. Market expansion is influenced by improving access to biological products and advisory support. Wider demonstration programs and localized formulations are important for addressing performance variability across diverse climates and cropping systems.

Latin America

Latin America contributed 9.8% of global revenue in 2025. The region benefits from large agricultural acreage and increasing interest in sustainable input portfolios, particularly where resistance management and stewardship are gaining importance. Adoption is stronger where commercial farms and export chains prioritize compliance and product traceability. Distribution reach and localized agronomy support remain key determinants of scale.

Middle East & Africa

Middle East and Africa held 7.0% of global revenue in 2025. Market development is influenced by uneven distribution infrastructure and varying levels of biological input penetration. Adoption tends to be stronger in export-oriented horticulture and high-value crop systems where compliance and residue considerations are critical. Expansion opportunities improve as product availability, agronomic support, and stewardship frameworks become more consistent.

Competitive Landscape

Competition in the bioherbicides market centers on product performance consistency, formulation stability, and the ability to support growers with agronomic guidance that enables reliable outcomes. Suppliers differentiate through crop-label breadth, application flexibility, channel partnerships, and integration positioning within integrated weed management programs. Portfolio strategies increasingly emphasize combining microbial and botanical pipelines with delivery formats that align to standard farm operations such as seed treatment and conventional spraying. Market participants also use collaborations, registration progress, and portfolio expansion to strengthen distribution access and reinforce credibility with advisers and growers.

FMC Corporation’s approach is typically anchored in expanding crop protection portfolios and strengthening commercialization capabilities through regional product launches and targeted solutions for major crops. The company’s presence and channel reach support faster adoption when new products align with large-acre agronomic workflows and resistance-management needs. Continued innovation in weed control and adjacent crop protection categories helps reinforce positioning across both broad-acre and specialty crop systems. Product and market development efforts also benefit from strong distribution coverage and support infrastructure that can accelerate field validation and repeat purchasing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- FMC Corporation

- Seipasa

- Marrone Bio Innovations

- Emery Oleochemicals

- Verdesian Life Sciences

- Hindustan Bio-Tech

- MycoLogic Inc.

- Engage Agro USA

- Special Biochem Pvt. Ltd.

- Bioherbicides Australia Pty Ltd.

- Ecopesticides International, Inc.

- Certis / Certis Biologicals

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In March 2025, Moa Technology announced a new partnership with Italian natural products company NAICONS to screen 70,000 micro-bacterial extracts in search of safe and effective biological herbicide leads, with Moa taking exclusive rights to develop any herbicides discovered through the collaboration.

- In May 2025, Contact BioSolutions announced that FireHawk Bioherbicide received regulatory approval from California’s Department of Pesticide Regulation, allowing the company to sell the product in the state as a fast-acting alternative weed-control solution.

- In June 2025, FireHawk Bioherbicide made its debut at the 2025 American Public Gardens Association Conference, where Contact BioSolutions showcased the product to public garden, horticulture, and sustainability professionals as an alternative to traditional weed control.

- In August 2025, Contact BioSolutions announced EPA approval and the launch of FireHawk Bioherbicide Super Concentrate, positioning it as a next-generation weed-control product for professional land-care use

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 3,896.29 million |

| Revenue forecast in 2032 |

USD 10,364.22 million |

| Growth rate (CAGR) |

15% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Source; By Mode of Application; By Crop Type; By Formulation; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

FMC Corporation; Seipasa; Marrone Bio Innovations; Emery Oleochemicals; Verdesian Life Sciences; Hindustan Bio-Tech; MycoLogic Inc.; Engage Agro USA; Special Biochem Pvt. Ltd.; Bioherbicides Australia Pty Ltd.; Ecopesticides International, Inc.; Certis / Certis Biologicals |

| No.of Pages |

339 |

Segmentation

By Source

- Microbial bioherbicides

- Biochemical bioherbicides

- Botanical / plant-based bioherbicides

- Other bioherbicides

By Mode of Application

- Foliar spray

- Soil application

- Seed treatment

- Post-harvest application

By Crop Type

- Cereals and grains

- Fruits and vegetables

- Oilseeds and pulses

- Turf and ornamentals

- Plantation crops

- Other crop types

By Formulation

- Liquid

- Granular

- Powder / dry

- Other formulations

By End User

- Agriculture

- Horticulture

- Forestry

- Turf and ornamental management

- Other end users

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa