Bioinsecticides Market

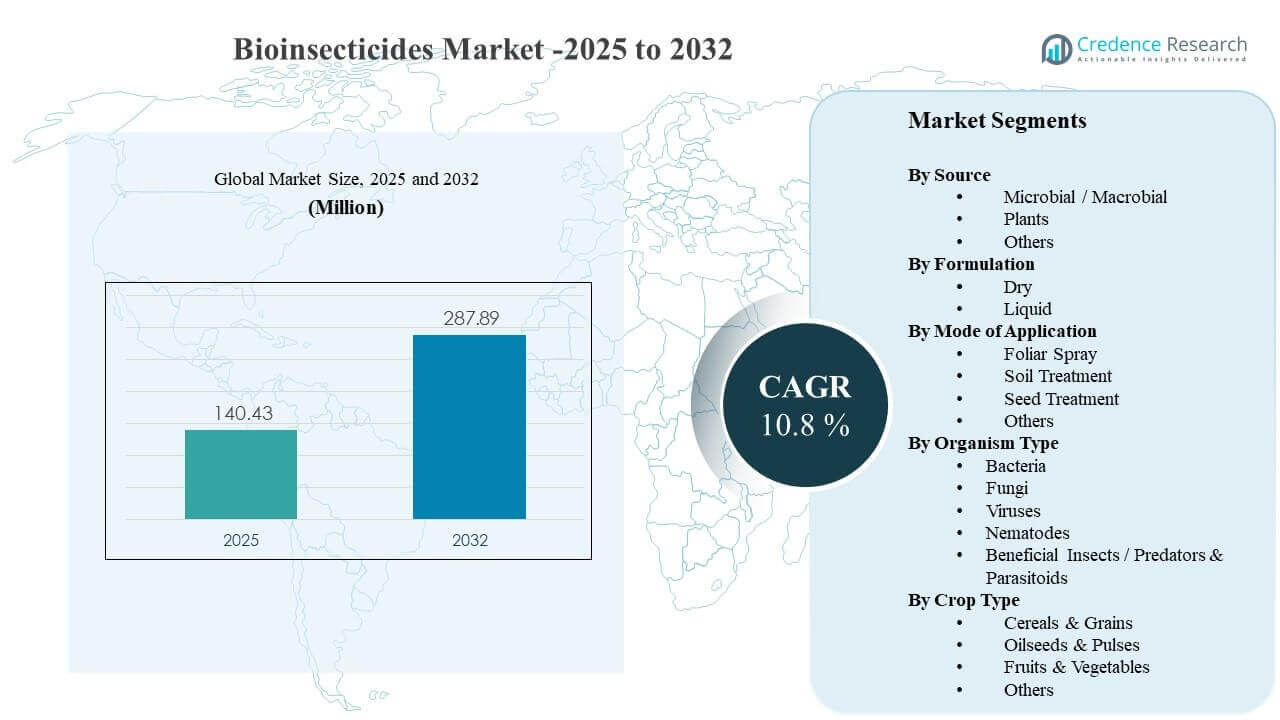

The global Bioinsecticides Market size was estimated at USD 140.43 million in 2025 and is expected to reach USD 287.89 million by 2032, growing at a CAGR of 10.8% from 2025 to 2032. Demand growth is primarily driven by the shift toward integrated pest management programs that prioritize residue compliance, resistance management, and selective control of target pests in both broad-acre and high-value crops. Bioinsecticides Market growth is also supported by product innovation in microbial actives and formulation technologies that improve field stability, handling, and compatibility with standard farm application systems across regions.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bioinsecticides Market Size 2025 |

USD 140.43 million |

| Bioinsecticides Market, CAGR |

10.8% |

| Bioinsecticides Market Size 2032 |

USD 287.89million |

Key Market Trends & Insights

- Microbial / Macrobial accounted for the largest share of 56.8% in 2025, supported by scalable production and strong fit with IPM programs.

- Foliar Spray held 43.1% share in 2025, reflecting continued preference for canopy targeting using conventional sprayer infrastructure.

- Cereals & Grains accounted for 32.2% share in 2025, driven by large acreage, recurring pest pressure, and repeat-season demand cycles.

- North America represented 34.9% share in 2025, supported by mature biological crop protection adoption and strong distribution networks.

- Bioinsecticides Market is projected to reach USD 287.89 million by 2032, reflecting sustained scaling across crop protection portfolios.

Segment Analysis

Bioinsecticides Market adoption is closely linked to buyer requirements for effective pest control outcomes alongside tightening residue expectations in food value chains. Growers and crop advisors increasingly position bioinsecticides as rotational tools within integrated programs to reduce resistance pressure from conventional insecticides and protect yield stability. Purchasing decisions typically emphasize consistency under field conditions, ease of application using existing equipment, and compatibility with other crop protection inputs to avoid operational complexity.

Bioinsecticides Market demand is also influenced by the performance sensitivity of biological actives to environmental factors such as UV exposure, humidity, and temperature, which increases the importance of formulation improvements and clear application protocols. Protected cultivation and high-value horticulture often show stronger uptake because controlled conditions support biological efficacy and because market access is frequently tied to low-residue compliance. Over the forecast period, portfolio expansion by large agrochemical players and specialized biological firms is expected to strengthen access, education, and product availability across regions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Source Insights

Microbial / Macrobial accounted for the largest share of 56.8% in 2025. Microbial solutions tend to lead because they can be produced at scale, standardized for quality, and deployed through established farm spray practices. Microbial bioinsecticides also align well with resistance-management strategies due to targeted modes of action and suitability for rotation programs. Ongoing improvements in formulation stability and shelf life are supporting broader field adoption across multiple crop types.

By Formulation Insights

Liquid formulations lead adoption patterns in many use cases because liquid products are typically easier to dose, mix, and apply using conventional spray systems. Liquid formats also support flexible tank-mix and coverage requirements in foliar programs where canopy pests are the primary target. Formulation advancements such as stickers, dispersants, and stabilizers are improving persistence and reducing performance variability in field conditions. Dry formulations remain important where storage, transport, and longer shelf life are prioritized.

By Organism Type Insights

Organism type selection is primarily shaped by pest spectrum, crop environment, and application timing requirements. Bacterial bioinsecticides remain widely used in programs targeting specific insect groups, particularly where repeat application schedules are common. Fungal solutions can be favored in protected cultivation and humidity-supportive conditions, supporting uptake in horticulture and greenhouse segments. Viruses, nematodes, and beneficial insects are increasingly used in targeted, high-value, and controlled-environment pest management programs where selectivity and non-target safety are prioritized.

By Mode of Application Insights

Foliar Spray accounted for the largest share of 43.1% in 2025. Foliar delivery leads because it provides direct contact with canopy pests and integrates smoothly into routine spray schedules across crop stages. Foliar application also fits existing equipment ecosystems and allows practical adjustments to dose and timing based on pest pressure and weather conditions. Compatibility with IPM rotations further supports foliar use as a repeatable application route for biological insect control.

By Crop Type Insights

Cereals & Grains accounted for the largest share of 32.2% in 2025. This segment leads because large planted acreage and recurring insect pressure create steady seasonal demand for pest control inputs. Bioinsecticides in cereals and grains are increasingly used to complement conventional programs and reduce resistance risk over multi-season cycles. Wider IPM adoption, combined with sustainability commitments across supply chains, continues to strengthen penetration in staple crops.

Bioinsecticides Market Drivers

Expansion of integrated pest management programs

Bioinsecticides Market growth is supported by the expanding adoption of integrated pest management across commercial farming systems. IPM programs prioritize rotation and selectivity to manage resistance and reduce broad-spectrum chemical dependence. Bioinsecticides provide targeted control options that can be sequenced with conventional chemistries to maintain efficacy over time. Advisory-led adoption models and clearer field protocols are improving grower confidence in biological performance. Bioinsecticides Market demand rises as IPM becomes embedded in procurement and compliance frameworks.

Increasing importance of residue compliance in food supply chains

Bioinsecticides Market demand is reinforced by stricter residue expectations across domestic retail and export-driven supply chains. Low-residue programs encourage growers to adopt biological inputs that reduce the risk of exceeding limits in sensitive crops. Fruits, vegetables, and other high-value segments often face the highest compliance pressure, accelerating biological adoption. Buyers also value solutions that help maintain market access without compromising pest control objectives. Bioinsecticides Market growth strengthens as traceability and compliance requirements become more standardized.

Product innovation in microbial actives and formulation stability

Bioinsecticides Market growth is increasingly tied to product innovation that improves consistency under field conditions. Stabilized formulations, improved shelf life, and better tolerance to UV and temperature variation reduce performance variability for growers. Enhanced adjuvant systems and improved dispersion behavior also support more reliable field coverage. These improvements reduce switching costs and training requirements for new users. Bioinsecticides Market adoption improves when product reliability approaches conventional expectations.

- For instance, a recent Bacillus thuringiensis microcapsule formulation incorporating semiconductor quantum dots maintained 57.77% spore viability after 96 hours of UV exposure compared with 33.74% in a non‑microcapsule SQD formulation and 31.25% in an unprotected control while increasing larval mortality to 71.22% versus 42.34% and 38.42% respectively, demonstrating how advanced formulation technology directly improves field performance.

Portfolio expansion and commercialization scale from leading suppliers

Bioinsecticides Market expansion benefits from the commercialization scale of established crop protection companies and specialized biological providers. Larger players can accelerate product registration, expand distribution footprints, and invest in demonstration trials that improve adoption. Portfolio breadth also allows suppliers to position bioinsecticides within integrated product programs across crops and pest profiles. Increased access to technical support and advisory services improves repeat purchasing behavior. Bioinsecticides Market growth gains momentum as commercialization capabilities expand across regions.

- For instance, BASF’s Agricultural Solutions division is broadening its BioSolutions portfolio covering biological products to reduce residues and manage resistance and, through the announced acquisition of AgBiTech’s biological insect control business, is scaling registration, distribution, and technical support for bioinsecticides across multiple regions.

Bioinsecticides Market Challenges

Bioinsecticides Market adoption faces challenges related to performance variability under changing environmental conditions and differences in farm practices. Biological actives may require more precise timing, repeat application schedules, and storage discipline to deliver consistent outcomes. Grower expectations shaped by fast-acting chemical controls can create dissatisfaction if biological performance is not positioned correctly. Operational complexity increases when compatibility with other inputs is unclear. Bioinsecticides Market penetration can slow when extension and advisory support is limited.

Bioinsecticides Market growth is also constrained by supply chain and scale-up complexities for certain biological actives, including maintaining viable counts, quality consistency, and cold-chain requirements in some cases. Regulatory pathways can be time-consuming and differ significantly across regions, affecting product availability and launch pacing. Pricing and perceived value can be barriers in price-sensitive markets, especially in broad-acre crops with tight margins. Counterfeit and low-quality products can also erode trust and delay adoption. Bioinsecticides Market participants must address these constraints through quality control and farmer education.

- For instance, commercial entomopathogenic nematode products from suppliers such as Koppert must be held continuously at 35–43 °F (about 2–6 °C), with no deviation from this range, because temperature excursions irreversibly reduce viability and field performance.

Bioinsecticides Market Trends and Opportunities

Bioinsecticides Market trends increasingly reflect a shift toward combination programs that pair biologicals with compatible chemistries to enhance control consistency. Suppliers are investing in protocols and decision-support tools to optimize timing, dose, and rotation strategies for growers. Adoption is rising in protected cultivation and high-value crop systems where environmental control improves biological performance. Product positioning increasingly emphasizes resistance management benefits and compatibility with sustainability certification requirements. Bioinsecticides Market opportunity expands as biologicals become standard components of IPM toolkits.

- For instance, compatibility studies on parasitoids and bioinsecticides have shown that combining Ganaspis kimorum with Beauveria bassiana increased Drosophila suzukii mortality by 1.87 times compared to the microbial alone, and with Bacillus thuringiensis by 1.74 times, supporting more data-driven rotation programs.

Bioinsecticides Market opportunities are also emerging from advancements in formulation science, including improved UV protectants, microencapsulation, and better on-leaf persistence. Expansion of local manufacturing and distribution partnerships can improve availability and reduce logistical barriers in emerging markets. Increased private and public support for sustainable agriculture practices can accelerate training and adoption at scale. Growth potential strengthens in export-oriented supply chains where compliance and residue considerations are central to procurement. Bioinsecticides Market participants can capture value by improving reliability and lowering adoption complexity.

Regional Insights

North America

Bioinsecticides Market in North America held 34.9% share in 2025, supported by mature IPM adoption and strong supplier presence. Commercial farming systems and advisory networks support trialing and repeat use of biological products across multiple crops. Bioinsecticides are increasingly used to manage resistance pressure and improve residue outcomes in sensitive value chains. Distribution strength and technical support availability improve penetration in both broad-acre and specialty crops.

Europe

Bioinsecticides Market in Europe accounted for 29.8% share in 2025, supported by tighter pesticide regulations and strong demand for low-residue production. High-value horticulture and protected cultivation drive frequent bioinsecticide use due to compliance needs and controlled environments. Adoption is reinforced by established biological crop protection programs and advisory support. Supplier innovation and portfolio expansion continue to support product availability and category growth.

Asia Pacific

Bioinsecticides Market in Asia Pacific represented 23.6% share in 2025, reflecting increasing adoption across large agricultural economies. Growth is supported by rising awareness of sustainable pest management and increased focus on reducing chemical load in export-linked crops. Protected cultivation expansion and intensification of horticulture also improve biological uptake. Wider access to training, improved distribution, and localized production can accelerate future adoption across diverse farming systems.

Latin America

Bioinsecticides Market in Latin America accounted for 7.1% share in 2025, supported by large-scale commercial agriculture and increasing biological penetration in crop protection programs. Export-oriented farming encourages residue-aware programs in several high-value crop categories. Demand is also shaped by resistance management needs in intensive row crop systems. Growth potential improves as suppliers expand field support and adapt formulations to local climatic conditions.

Middle East & Africa

Bioinsecticides Market in Middle East & Africa held 4.6% share in 2025, supported by expanding horticulture, protected cultivation, and export-focused production in select markets. Adoption is influenced by the need for residue compliance and improved pest management in high-value crops. Distribution reach, affordability, and farmer education remain key adoption determinants. Wider availability of trusted products and technical guidance can improve penetration over the forecast period.

Competitive Landscape

Bioinsecticides Market competition is shaped by a mix of large crop protection companies and specialized biological providers focused on microbial actives, formulation technology, and crop-specific positioning. Leading participants compete through portfolio breadth, regulatory approvals, distribution partnerships, and technical advisory support that improves on-farm outcomes. Differentiation is increasingly linked to formulation stability, compatibility with IPM rotations, and validated efficacy across key pests and crop environments. Strategic partnerships and acquisitions are used to accelerate pipeline development and improve commercialization scale.

BASF SE is positioned to strengthen bioinsecticide reach through portfolio expansion strategies that complement broader biological crop protection offerings. BASF SE focus areas typically include scaling proven biological actives, improving formulation performance, and expanding market access through established distribution channels. BASF SE also benefits from integration capabilities that can connect biological offerings with crop-specific recommendations and stewardship programs. BASF SE competitive advantage improves when field support and product reliability translate into repeat grower adoption across key crop systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BASF SE

- Bayer AG

- Syngenta

- Corteva Agriscience

- Valent BioSciences

- Certis USA

- Nufarm

- Marrone Bio Innovations

- Novozymes

- BioWorks

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In January 2026, BASF Agricultural Solutions announced that it had reached an agreement to acquire AgBiTech, a specialist in biological insect control solutions, in a move aimed at strengthening BASF’s global portfolio in bioinsecticides and sustainable crop protection; the transaction is expected to close in the first half of 2026, subject to regulatory approvals.

- In November 2025, FA Bio revealed that it is launching a bioinsecticide discovery and development project in collaboration with Bayer, a partnership that validates FA Bio’s microbial discovery platform and is intended to accelerate the commercialization of new bioinsecticide solutions that support yield protection and soil health in regenerative agriculture systems.

- In December 2025, Corteva Agriscience introduced Goltrevo, its first bioinsecticide based on a novel strain of Beauveria bassiana to control sap‑feeding and chewing insects, marking a strategic expansion of the company’s biological crop protection portfolio alongside a new next‑generation insecticide designed to provide sustainable, resistance‑breaking pest control across major crops.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 140.43 million |

| Revenue forecast in 2032 |

USD 287.89 million |

| Growth rate (CAGR) |

10.8% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Source Outlook: Microbial / Macrobial, Plants, Others; By Formulation Outlook: Dry, Liquid; By Organism Type Outlook: Bacteria, Fungi, Viruses, Nematodes, Beneficial Insects / Predators & Parasitoids; By Mode of Application Outlook: Foliar Spray, Soil Treatment, Seed Treatment, Others; By Crop Type Outlook: Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Others |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

BASF SE; Bayer AG; Syngenta; Corteva Agriscience; Valent BioSciences; Certis USA; Nufarm; Marrone Bio Innovations; Novozymes; BioWorks |

| No. of Pages |

328 |

Segmentation

By Source

- Microbial / Macrobial

- Plants

- Others

By Formulation

By Organism Type

- Bacteria

- Fungi

- Viruses

- Nematodes

- Beneficial Insects / Predators & Parasitoids

By Mode of Application

- Foliar Spray

- Soil Treatment

- Seed Treatment

- Others

By Crop Type

- Cereals & Grains

- Oilseeds & Pulses

- Fruits & Vegetables

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa