Biorational Pesticides Market Overview:

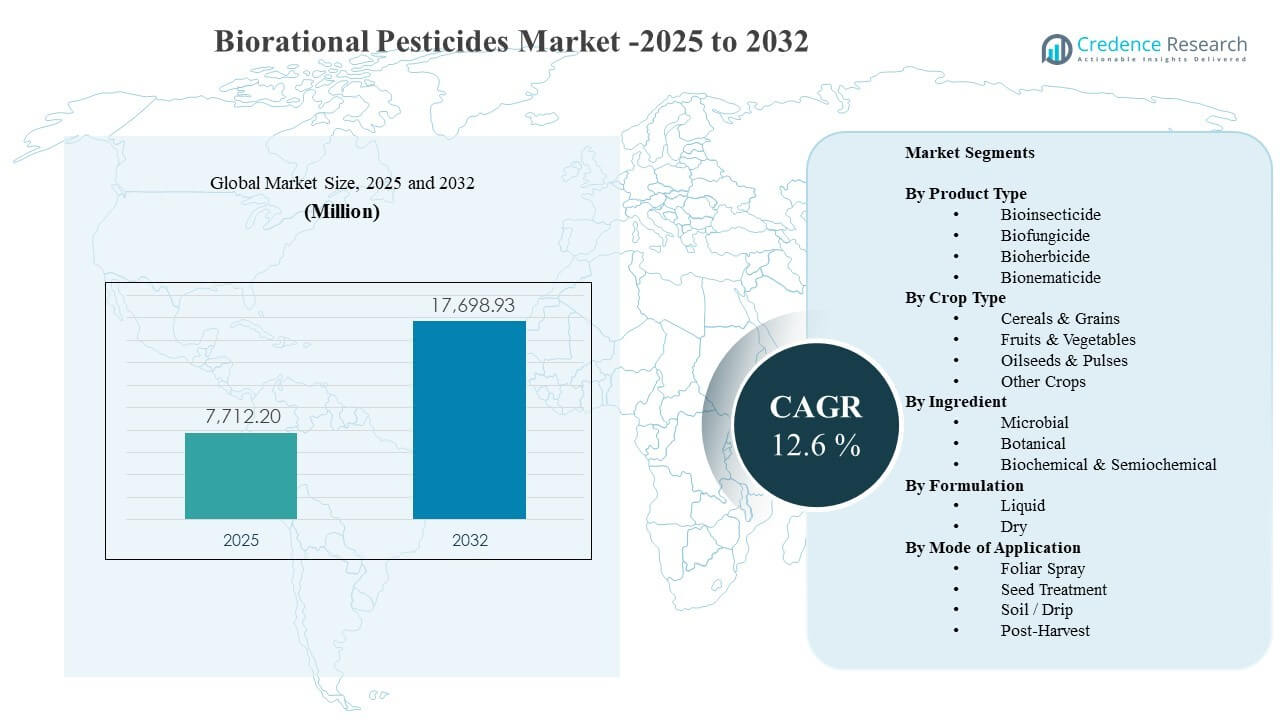

The global Biorational Pesticides Market size was estimated at USD 7,712.2 million in 2025 and is expected to reach USD 17,698.93 million by 2032, growing at a CAGR of 12.6% from 2025 to 2032. Demand is primarily driven by growers and agribusinesses seeking effective pest and disease control solutions that align with residue limits, integrated pest management practices, and sustainability-linked procurement requirements across high-value crops. Adoption is also supported by wider product availability through established input channels and improving confidence in biological performance under diverse field conditions.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biorational Pesticides Market Size 2025 |

USD 7,712.2 million |

| Biorational Pesticides Market, CAGR |

12.6% |

| Biorational Pesticides Market Size 2032 |

USD 17,698.93 million |

Key Market Trends & Insights

- The Biorational Pesticides Market is projected to expand at a CAGR of 6% during 2025–2032, reflecting accelerated penetration across conventional and sustainable farming programs.

- Microbial ingredients accounted for the largest share of 9% in 2025, supported by strong efficacy profiles and fit with IPM rotations.

- Bioinsecticide products held the leading share of 6% in 2025, indicating continued prioritization of insect control in residue-sensitive crop programs.

- Liquid formulations represented 0% share in 2025, reflecting easier handling and compatibility with existing spray systems.

- Foliar spray accounted for 3% share in 2025, as foliar application remains the most widely adopted method for fast response to pest pressure.

Segment Analysis

The Biorational Pesticides Market is expanding as agricultural decision-makers increase preference for targeted solutions that support resistance management and compliance with evolving residue expectations. Higher adoption in fruits and vegetables is linked to export-oriented value chains and tighter retailer requirements, which increase emphasis on crop-safe inputs and shorter pre-harvest intervals. Buyers also prioritize products that integrate into IPM programs, including solutions compatible with beneficial insects and biological control strategies.

Commercial traction is strengthening as formulation stability improves and as suppliers widen labeling across crops and geographies. Microbial and botanical platforms are increasingly positioned as rotation tools to reduce dependence on conventional chemistries, particularly where resistance pressure is elevating the cost of control. Distribution partnerships, agronomy advisory support, and demonstrated field performance across seasons are improving repeat adoption and expanding usage beyond niche organic applications.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Bioinsecticide accounted for the largest share of 44.6% in 2025. Bioinsecticide leadership is supported by persistent insect pressure across major cropping systems and the need for rotation options to manage resistance. Bioinsecticides also align well with residue-sensitive programs in horticulture where market access depends on compliance and repeatable quality. Wider availability through mainstream farm input channels and clearer application guidance are reinforcing adoption across commercial farms.

By Crop Type Insights

Fruits & Vegetables represented the most commercially attractive crop segment in 2025 due to higher value per hectare and stronger residue sensitivity across retail and export programs. Growers in horticulture often require flexible solutions that can be deployed close to harvest without compromising compliance or quality. Pest and disease incidence in intensive production cycles increases demand for rotation-friendly inputs that protect yield and appearance. Advisory-driven purchasing and tighter buyer specifications also improve willingness to adopt biorational products.

By Ingredient Insights

Microbial ingredients accounted for the largest share of 71.9% in 2025. Microbial solutions lead due to targeted biological modes of action and strong alignment with IPM strategies that emphasize ecosystem compatibility. Improved formulations and better storage stability are addressing earlier barriers related to shelf life and field consistency. Expanded crop registrations and broader commercial validation are increasing confidence among growers and advisors, which supports higher repeat usage across seasons.

By Formulation Insights

Liquid formulations accounted for the largest share of 68.0% in 2025. Liquid products lead because liquid handling integrates smoothly with existing spray operations and simplifies dosing and mixing at farm level. Liquids can support better coverage and adherence for foliar programs when operational speed matters. Distributors and applicators also favor liquids due to simpler logistics and fewer adoption frictions compared with some dry formats. Ongoing formulation innovation is improving stability for biological actives in liquid forms.

By Mode of Application Insights

Foliar spray accounted for the largest share of 57.3% in 2025. Foliar application remains the dominant route because foliar spraying provides rapid deployment during active pest or disease events and fits established farm practice. Foliar programs also enable flexible scheduling across crop stages and multiple cycles, which supports repeat treatment patterns. Compatibility with tank-mix planning and broader equipment availability further strengthens foliar use across diverse farm sizes.

Biorational Pesticides Market Drivers

Rising residue compliance pressure across high-value crops

Residue compliance requirements across retail and export channels are increasing demand for biorational pesticides in fruits and vegetables and specialty crops. Supply chains increasingly expect predictable compliance with maximum residue limits and reduced reliance on higher-toxicity chemistries. Biorational products offer a route to maintain market access without compromising harvest timing and crop quality. Agribusiness procurement practices that incorporate sustainability metrics are reinforcing adoption. Greater buyer scrutiny across fresh produce is translating into faster portfolio expansion for biorational suppliers.

- For instance, Certis Belchim stated that its IPM programs developed with major producer cooperatives in Spain targeted residue-free produce, while some supermarket chains were requiring residues 33% to 50% below legal MRLs and limiting residue profiles to just three to five products.

Resistance management needs and IPM expansion

Resistance pressure is rising for several pest and disease complexes, increasing the need for rotation tools with differentiated modes of action. Biorational pesticides are increasingly integrated into IPM programs to reduce selection pressure and preserve the efficacy of existing chemistries. Many growers are combining biologicals with monitoring, beneficial insects, and cultural controls to stabilize outcomes. Advisory-led programs are accelerating adoption by translating field performance into repeatable playbooks. Wider availability and clearer label guidance are enabling more consistent deployment across regions.

- For instance, BASF reported for Velifer biological insecticide that when applications began at 2.5 whiteflies per leaf, control reached 60%, whereas control fell to 40% when starting pressure was 15 whiteflies per leaf, highlighting the importance of early IPM-based deployment.

Product innovation and improved formulation performance

Advances in formulation and delivery are improving field reliability for microbial and biochemical actives. Better stability, improved shelf life, and more user-friendly formats reduce operational friction at farm level. Innovation is also supporting broader crop registrations and more flexible application timing. These improvements help biorational pesticides compete more effectively in conventional farming systems where performance expectations are high. As reliability improves, growers increase willingness to allocate larger shares of crop protection budgets to biorational products.

Channel expansion and commercial scale-up by major suppliers

Large crop protection companies and specialized biological suppliers are strengthening route-to-market through partnerships, acquisitions, and expanded distribution coverage. Expanded dealer networks and agronomy support programs improve product trial rates and adoption persistence. Commercial scale-up also improves product availability during peak seasons and reduces lead-time constraints. Training and advisory support help match products to crop stage and pest pressure, improving outcomes. These commercialization efforts increase trust and broaden penetration across farms beyond early adopters.

Biorational Pesticides Market Challenges

Performance variability under different environmental conditions remains a key adoption barrier for parts of the biorational pesticides portfolio. Temperature, humidity, UV exposure, and application timing can influence efficacy, which increases dependence on correct use practices and advisory support. Some growers remain cautious when immediate knockdown expectations are high, particularly in severe infestation periods. Storage and handling requirements for certain biological actives can add operational complexity for distributors and farms. Price sensitivity in some regions can slow switching when conventional alternatives appear cheaper per application.

- For instance, IPL Biologicals states that its microbial solutions provide shelf life of up to 24 months even under unfavorable storage conditions, and the company reports more than 50 innovative microbial solutions supported by 13 patented innovations, highlighting how formulation and strain-selection technology are being used to improve stability and field performance consistency.

Regulatory pathways and registration complexity can also constrain pace of innovation and commercialization in certain countries. Label expansion across crops and pests requires time and localized field data, which can delay scaling for new products. Fragmented standards across markets complicate cross-border commercialization and can increase compliance costs. Competitive intensity is rising as more suppliers enter biological and biochemical categories, which increases pricing pressure and raises expectations for demonstrated performance. Farm-level education and consistent agronomy support remain essential to sustain repeat adoption.

Market Trends and Opportunities

Biorational pesticides adoption is increasingly driven by integrated programs that combine biological products with precision scouting, digital decision support, and targeted application scheduling. This trend improves product performance consistency and strengthens the value proposition for growers that require reliable outcomes. Demand is also rising for products positioned as rotation tools rather than niche replacements, supporting broader usage across conventional farms. Companies that bundle advisory services and training with product delivery are improving retention. Growth opportunities are strongest where high-value crop acreage and export requirements are expanding.

- For instance, Viscon’s EVA Scoutr greenhouse robot detects pests and diseases as small as 0.012 mm, recognizes more than 15 pests and diseases, and maps infestations with accuracy of up to ±10 cm, demonstrating how digital scouting infrastructure can improve timing and consistency in biological crop protection programs.

Portfolio expansion through microbial, botanical, and biochemical innovation is creating opportunities to address wider pest and disease spectra. Improved formulations, new strains, and combinations with compatible inputs are widening practical use windows. Post-harvest applications and seed treatment programs are emerging as additional areas of interest due to quality preservation needs and early-stage crop protection. Expansion in controlled-environment agriculture is supporting demand for low-residue solutions that protect yield and appearance. Broader distribution partnerships can accelerate access in emerging regions and unlock new customer segments.

Regional Insights

North America

North America accounted for 37.6% of revenue in 2025, supported by mature biologicals distribution, strong adoption of IPM programs, and residue-driven requirements in high-value crops. Commercial farms and integrated supply chains prioritize products that help maintain compliance and protect quality outcomes. Advisory infrastructure and product training improve correct use and reinforce repeat purchasing. Portfolio expansion by major suppliers is also improving availability and widening crop coverage.

Europe

Europe represented 22.3% share in 2025, supported by tighter regulatory direction and strong emphasis on sustainable crop protection practices. Procurement in many markets favors solutions aligned with reduced chemical loads and ecosystem compatibility. Adoption is stronger in horticulture and specialty crops where residue and certification requirements shape input selection. Tendering and distributor influence can affect brand positioning, making field performance validation critical.

Asia Pacific

Asia Pacific held 22.1% share in 2025, supported by expanding intensive agriculture, rising focus on export compliance, and increasing investment in modern crop protection practices. Adoption varies by country due to differences in farm structure, affordability, and advisory access. Growth momentum is supported by portfolio localization and expanding distribution coverage. Increased awareness of resistance management is also improving acceptance of rotation-friendly biorational solutions.

Latin America

Latin America accounted for 11.4% share in 2025, supported by large commercial farming footprints, high pest pressure, and growing biological adoption in export-linked crops. Grower interest is increasing where biological solutions improve program sustainability and support resistance management strategies. Adoption is strongest where distributors provide agronomy support and product availability is reliable during peak seasons. Competitive activity is increasingly focused on scaling biological portfolios and strengthening channel presence.

Middle East & Africa

Middle East and Africa represented 6.6% share in 2025, supported by expanding horticulture production, greenhouse cultivation, and quality-driven supply chains in selected markets. Adoption is still developing due to channel fragmentation and variable access to advisory support. Demand is increasing where low-residue solutions are needed for export and premium retail programs. Suppliers that provide training and stable product supply can accelerate penetration.

Competitive Landscape

Competition in the Biorational Pesticides Market is shaped by portfolio breadth, field reliability, channel access, and the ability to support growers with agronomy guidance for correct deployment. Leading suppliers compete by expanding microbial and biochemical platforms, strengthening distribution partnerships, and integrating products into IPM positioning. Differentiation often depends on consistency across environmental conditions, label breadth across crops and pests, and the availability of technical support. Strategic acquisitions and collaborations are increasingly used to accelerate pipeline expansion and improve commercialization scale.

Valent BioSciences is positioned as a specialist biologicals supplier with emphasis on proven biological actives and practical deployment in commercial agriculture programs. The company focus typically centers on expanding crop coverage, strengthening technical advisory support, and aligning solutions with IPM frameworks that emphasize rotation and compatibility with beneficial organisms. Commercial traction is reinforced through distributor engagement and seasonal program planning that supports repeat applications. Continued product development and field validation remain important to maintain differentiation as competition intensifies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In January 2026, BASF Agricultural Solutions announced an agreement to acquire AgBiTech, a company focused on biological insect control solutions. BASF said it will take full ownership of AgBiTech, including its portfolio, intellectual property, manufacturing operations, R&D facilities, and personnel, with closing expected in the first half of 2026 subject to regulatory approval.

- In November 2025, Syngenta Crop Protection and Amoéba SA signed a memorandum of understanding to develop and commercialize biocontrol solutions for cereals and field crops in the EU and UK. The partnership is initially focused on wheat diseases such as septoria tritici blotch and yellow rust, and the companies said they aim to negotiate a definitive distribution agreement by spring 2026.

- In November 2025, Corteva announced nature-inspired insect-control solutions and described the move as the company’s first bioinsecticide launch. Corteva said the new offering is designed to help farmers control insects and protect crop yield, marking a notable product-launch update in biological crop protection.

- In July 2025, Bayer expanded its partnership with M2i Group to distribute pheromone-based biological crop protection products beyond Europe and Africa and to strengthen their global biologicals collaboration. Bayer said the broader agreement builds on its earlier distribution arrangement for selected M2i products used in crops such as stone and pome fruits, tomatoes, and grapes.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 7,712.2 million |

| Revenue forecast in 2032 |

USD 17,698.93 million |

| Growth rate (CAGR) |

12.6% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type, By Crop Type, By Ingredient, By Formulation, By Mode of Application |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Valent BioSciences; Bayer AG; Syngenta Group; BASF SE; Certis Biologicals; FMC Corporation; UPL Limited; Koppert Biological Systems; Corteva Agriscience; Novonesis |

| No.of Pages |

325 |

Segmentation

By Product Type

- Bioinsecticide

- Biofungicide

- Bioherbicide

- Bionematicide

By Crop Type

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

- Other Crops

By Ingredient

- Microbial

- Botanical

- Biochemical

- Others

By Formulation

By Mode of Application

- Foliar Spray

- Seed Treatment

- Soil / Drip

- Post-Harvest

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa