| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Chemotherapy Induced Neutropenia Market Size 2024 |

USD 668.0 million |

| Chemotherapy Induced Neutropenia Market, CAGR |

3.27% |

| Chemotherapy Induced Neutropenia Market Size 2032 |

USD 865.7 million |

Market Overview

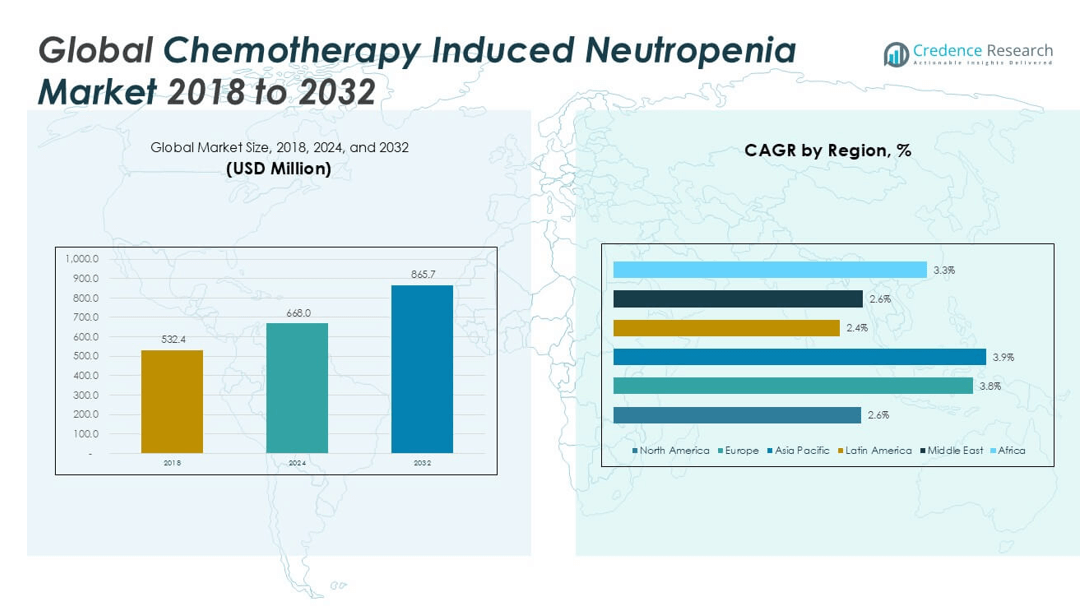

The Global Chemotherapy Induced Neutropenia Market is projected to grow from USD 668.0 million in 2024 to an estimated USD 865.7 million by 2032, with a compound annual growth rate (CAGR) of 3.27% from 2025 to 2032.

The market is driven by several key factors, including advancements in oncology treatment protocols, supportive government initiatives, and the rising awareness of neutropenia management. Trends such as the development of long-acting biologics, the introduction of pegylated granulocyte-colony stimulating factors (G-CSFs), and the growing preference for outpatient management of neutropenia cases are contributing to market evolution. Additionally, the entry of biosimilar drugs is helping lower treatment costs and improve accessibility in emerging economies, thereby enhancing market penetration.

Geographically, North America dominates the global chemotherapy induced neutropenia market due to its advanced healthcare infrastructure, high cancer prevalence, and favorable reimbursement policies. Europe holds a significant share, supported by robust clinical research and the presence of leading pharmaceutical companies. Meanwhile, Asia Pacific is expected to witness the fastest growth, driven by rising cancer incidences, increasing healthcare investments, and expanding access to biologic therapies. Key players in the market include Amgen Inc., Teva Pharmaceutical Industries Ltd., Pfizer Inc., Mylan N.V., and Coherus BioSciences, Inc.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The market is projected to grow from USD 668.0 million in 2024 to USD 865.7 million by 2032, registering a CAGR of 3.27% between 2025 and 2032.

- Rising global cancer prevalence and increased use of aggressive chemotherapy regimens are significantly boosting the demand for neutropenia management therapies.

- The adoption of long-acting G-CSFs and biosimilars is expanding due to their clinical efficiency, reduced dosing frequency, and lower treatment costs.

- Supportive healthcare policies, growing awareness of neutropenia risks, and improved oncology care infrastructure are driving market penetration.

- High costs of biologic therapies and uneven access in low- and middle-income regions continue to limit widespread adoption.

- North America held the largest market share in 2024, led by strong reimbursement systems and established oncology protocols.

- Asia Pacific is expected to witness the fastest growth through 2032, supported by rising cancer cases, healthcare investment, and biosimilar uptake.

Market Drivers

Rising Cancer Prevalence and Expanding Chemotherapy Use Accelerate Demand

The increasing global burden of cancer remains a primary driver for the Global Chemotherapy Induced Neutropenia Market. Growing awareness, early diagnosis, and evolving treatment protocols have led to a higher number of patients undergoing chemotherapy. These regimens often cause neutropenia, which raises the risk of life-threatening infections. Healthcare providers are increasingly recommending prophylactic treatments to mitigate this risk. This trend fuels the demand for granulocyte-colony stimulating factors (G-CSFs) and other supportive therapies. The market benefits from clinical guidelines that encourage neutropenia prevention in moderate-to-high risk patients. It continues to expand with rising treatment volumes and oncology spending worldwide.

- For instance, the World Health Organization reported that in 2024, over 20 million new cancer cases were diagnosed globally, with more than 12 million patients receiving chemotherapy, resulting in an estimated 5 million cases of chemotherapy-induced neutropenia requiring supportive care interventions.

Advancements in Biologics and Biosimilars Improve Market Accessibility

New biologics and biosimilars have transformed neutropenia management by offering effective, targeted therapies at more affordable prices. The approval and commercialization of biosimilar G-CSFs such as filgrastim and pegfilgrastim variants have broadened patient access, especially in cost-sensitive markets. The Global Chemotherapy Induced Neutropenia Market benefits from these developments through improved availability and lower financial barriers for both patients and payers. Biologics with extended half-life reduce the frequency of dosing and hospital visits, supporting wider adoption. Regulatory support for biosimilar pathways strengthens manufacturer confidence and drives innovation. This trend enhances treatment uptake across both developed and emerging healthcare systems.

- For instance, in 2024, Amgen and Sandoz collectively supplied over 35 million doses of biosimilar G-CSFs worldwide, significantly increasing access to neutropenia prevention therapies in both developed and emerging markets.

Government and Institutional Support Strengthens Adoption of Preventive Therapies

Public health agencies and oncology institutions are promoting the use of supportive care therapies to reduce hospitalizations and improve patient outcomes. Governments in North America and Europe have incorporated neutropenia management guidelines into cancer treatment policies. These actions positively influence the Global Chemotherapy Induced Neutropenia Market by encouraging standardized care protocols. Funding for cancer care programs and reimbursement schemes make preventive therapies more accessible. Hospitals and clinics now adopt risk-based assessment tools to identify high-risk patients early. Such institutional efforts ensure the sustained integration of neutropenia therapeutics into oncology practices.

Shift Toward Outpatient Care and Home Administration Drives Innovation

Healthcare systems worldwide are moving toward outpatient and home-based chemotherapy care to reduce hospital strain and lower treatment costs. This shift creates a need for convenient, long-acting neutropenia therapies that can be administered outside clinical settings. The Global Chemotherapy Induced Neutropenia Market responds with drug delivery innovations such as on-body injectors and prefilled syringes. These solutions support patient adherence and reduce complications. Pharmaceutical companies now focus on developing user-friendly formulations for safer self-administration. This outpatient trend aligns with payer interests and continues to influence drug development and distribution models.

Market Trends

Growing Adoption of Biosimilars Expands Access and Lowers Costs

The increasing availability of biosimilars is reshaping treatment options in the Global Chemotherapy Induced Neutropenia Market. Biosimilar versions of filgrastim and pegfilgrastim have received regulatory approval across key regions, including North America, Europe, and Asia Pacific. These alternatives offer similar clinical efficacy at reduced prices, helping healthcare systems manage costs more efficiently. Physicians and hospitals are shifting toward biosimilars due to strong clinical trial data and favorable reimbursement policies. It supports expanded access to neutropenia prevention therapies in both developed and resource-limited settings. Growing physician confidence and regulatory clarity continue to drive biosimilar adoption at scale.

- For instance, a 2024 survey by the IQVIA Institute reported that over 5 million doses of biosimilar filgrastim and pegfilgrastim were administered in the United States and Europe in 2023, with more than 1,200 hospitals and clinics adopting biosimilars as first-line options for chemotherapy-induced neutropenia.

Preference for Long-Acting Formulations Enhances Treatment Convenience

Long-acting G-CSF therapies are gaining popularity due to their ability to reduce dosing frequency and healthcare visits. Pegfilgrastim, for instance, allows for single-dose administration per chemotherapy cycle, improving patient compliance. The Global Chemotherapy Induced Neutropenia Market reflects this preference by increasing the share of long-acting products in total prescriptions. These therapies reduce logistical burdens for both patients and providers, especially in outpatient settings. Pharmaceutical companies are investing in extended-release and sustained-delivery platforms to meet this demand. It ensures safer and more efficient care pathways in cancer treatment protocols.

- For instance, according to a 2023 report from the National Comprehensive Cancer Network (NCCN), more than 2.4 million patients worldwide received long-acting G-CSF formulations, with pegfilgrastim accounting for over 65,000 new prescriptions in the United States alone during the year.

Integration of Risk-Based Prophylaxis Enhances Clinical Decision-Making

Oncologists now rely on risk-based models to guide prophylactic use of G-CSFs. Patient-specific factors such as age, cancer type, and chemotherapy intensity influence the decision to initiate neutropenia prevention. The Global Chemotherapy Induced Neutropenia Market aligns with this approach through the development of targeted therapy guidelines. This trend supports evidence-based medicine and reduces unnecessary use of high-cost interventions. Health systems gain from reduced hospitalizations, fewer infections, and improved treatment continuity. It promotes more personalized and cost-effective patient management.

Home-Based Drug Delivery Innovations Improve Patient Autonomy

Innovations in drug delivery technology are enabling patients to self-administer therapies safely at home. On-body injectors and prefilled autoinjectors are becoming standard for long-acting neutropenia drugs. The Global Chemotherapy Induced Neutropenia Market is adapting to this shift by promoting user-friendly designs and remote monitoring solutions. These devices reduce hospital dependency and support treatment in decentralized settings. Pharmaceutical companies are enhancing training programs and support services to ensure successful home administration. It improves quality of life for patients while easing pressure on healthcare infrastructure.

Market Challenges

High Cost of Biologic Therapies Limits Access in Price-Sensitive Markets

The high cost of originator biologics poses a significant barrier to treatment adoption, particularly in low- and middle-income countries. Many patients lack access to granulocyte-colony stimulating factors due to affordability issues and limited insurance coverage. The Global Chemotherapy Induced Neutropenia Market faces pressure from public health systems that struggle to finance these expensive therapies. Budget constraints and inconsistent reimbursement policies further hinder widespread usage. While biosimilars offer cost advantages, their adoption remains uneven due to regulatory delays and market entry barriers. It limits the full potential of preventive care in oncology settings across various regions.

- For instance, in the United States, a single treatment course of originator biologic filgrastim, used to prevent chemotherapy-induced neutropenia, can cost approximately $3,500, posing a significant financial barrier for many patients and healthcare systems.

Adverse Effects and Limited Awareness Impact Patient Compliance

Side effects such as bone pain, injection site reactions, and rare immunologic responses affect patient willingness to continue neutropenia treatment. Many patients are unaware of the risks associated with neutropenia or the benefits of early intervention. The Global Chemotherapy Induced Neutropenia Market must address these challenges through stronger patient education and clinician training. Inadequate awareness among healthcare providers in resource-limited settings leads to underutilization of available therapies. It creates inconsistencies in treatment practices and reduces adherence to evidence-based guidelines. Regulatory agencies and industry stakeholders must collaborate to close these knowledge gaps and improve treatment continuity.

Market Opportunities

Expansion of Biosimilar Portfolios Creates Opportunities in Emerging Markets

The increasing acceptance of biosimilars opens new growth avenues, especially in Asia Pacific, Latin America, and parts of Eastern Europe. Lower manufacturing costs and streamlined regulatory frameworks support broader market access. The Global Chemotherapy Induced Neutropenia Market can benefit from expanding biosimilar portfolios that meet international quality standards. It enables healthcare providers to treat more patients without exceeding budget constraints. Governments and private players are investing in local production capabilities to reduce dependency on imports. These developments create a favorable environment for biosimilar manufacturers to scale operations and penetrate untapped regions.

Integration of Digital Tools Enhances Patient Management and Market Reach

Digital health technologies, such as remote monitoring, e-prescriptions, and patient adherence apps, present new opportunities for improving treatment outcomes. Pharmaceutical companies can leverage digital platforms to support at-home care and engage patients more effectively. The Global Chemotherapy Induced Neutropenia Market can integrate these tools to ensure continuous therapy and minimize treatment interruptions. It allows real-time tracking of side effects and timely medical interventions, enhancing overall care quality. Collaborations between tech firms and healthcare providers can accelerate the development of tailored digital solutions. These advancements position the market for long-term growth through smarter, more connected care delivery models.

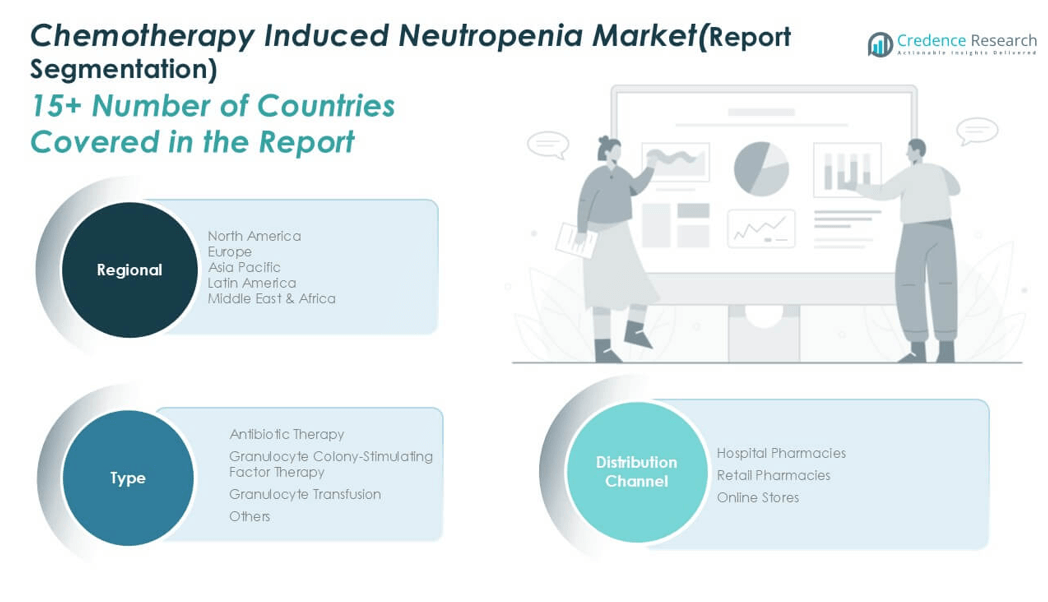

Market Segmentation Analysis

By Type

The Global Chemotherapy Induced Neutropenia Market is segmented into antibiotic therapy, granulocyte colony-stimulating factor (G-CSF) therapy, granulocyte transfusion, and others. Among these, G-CSF therapy holds the largest revenue share due to its proven clinical efficacy in preventing and managing neutropenia across various chemotherapy regimens. It supports rapid neutrophil recovery, reduces infection risk, and helps maintain chemotherapy dose intensity. Antibiotic therapy also plays a vital role, particularly in treating febrile neutropenia, though it is typically used reactively rather than preventively. Granulocyte transfusion remains limited to severe or refractory cases due to its complexity and logistical challenges. The market sees ongoing innovation in long-acting G-CSF formulations and biosimilars, which continue to influence segment dynamics.

- For instance, in 2023, more than 7 million chemotherapy cycles globally included G-CSF support, while antibiotic therapy was administered in over 3.5 million cases of febrile neutropenia (source: World Health Organization, IQVIA).

By Distribution Channel

Based on distribution channels, the Global Chemotherapy Induced Neutropenia Market is divided into hospital pharmacies, retail pharmacies, and online stores. Hospital pharmacies dominate the segment due to the critical nature of neutropenia treatment and the need for close clinical supervision. Most biologic therapies are administered in hospital or oncology center settings where monitoring and dosage adjustments are essential. Retail pharmacies account for a growing share, driven by rising outpatient care and the increasing availability of biosimilars. Online stores are emerging as a niche but expanding channel, especially in urban areas with advanced healthcare infrastructure. It supports broader access and convenience, particularly for refill prescriptions of long-acting therapies.

- For instance, in the United States, over 1,200 hospital pharmacies and 6,000 retail pharmacies dispensed G-CSF therapies for chemotherapy-induced neutropenia in 2023, with online stores processing more than 150,000 refill prescriptions nationwide (source: American Society of Health-System Pharmacists, FDA).

Segments

Based on Type

- Antibiotic Therapy

- Granulocyte Colony-Stimulating Factor Therapy

- Granulocyte Transfusion

- Others

Based on Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Stores

Based on Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America Chemotherapy Induced Neutropenia Market

North America accounted for the largest share in the Chemotherapy Induced Neutropenia Market in 2024, valued at USD 211.00 million, and is expected to reach USD 259.71 million by 2032, growing at a CAGR of 2.6%. This region held approximately 31.5% of the global market share in 2024. The market is driven by advanced healthcare infrastructure, a high incidence of cancer, and strong reimbursement support for supportive oncology care. The United States leads the regional market with robust adoption of long-acting G-CSF therapies and widespread access to biosimilars. Hospitals and oncology centers continue to expand their use of risk-based neutropenia prophylaxis. It maintains market growth through consistent funding for cancer treatment and preventive care programs.

Europe Chemotherapy Induced Neutropenia Market

Europe held a market value of USD 154.32 million in 2024, projected to reach USD 208.11 million by 2032, registering a CAGR of 3.8%. The region accounted for nearly 23.1% of the global Chemotherapy Induced Neutropenia Market share in 2024. Strong clinical research networks and well-established treatment guidelines support market development. Countries such as Germany, France, and the UK lead in biosimilar approvals and adoption. Public healthcare systems promote standardized neutropenia management protocols across oncology centers. It benefits from a stable regulatory environment and growing demand for cost-effective biologics.

Asia Pacific Chemotherapy Induced Neutropenia Market

Asia Pacific reached a market size of USD 190.54 million in 2024 and is expected to grow to USD 259.71 million by 2032, with the highest CAGR among all regions at 3.9%. This region captured around 28.5% of the global market share in 2024. Rapid growth in cancer cases, increasing healthcare expenditure, and broader access to biosimilars fuel regional expansion. Countries like China, Japan, and India are investing heavily in oncology infrastructure and biologic drug manufacturing. It is witnessing improved diagnosis rates and increased adoption of long-acting therapies. Government initiatives and private partnerships continue to strengthen treatment accessibility.

Latin America Chemotherapy Induced Neutropenia Market

Latin America recorded a market value of USD 57.25 million in 2024 and is projected to reach USD 69.26 million by 2032, reflecting a CAGR of 2.4%. The region represented about 8.6% of the global market share in 2024. Brazil and Mexico lead the market with expanding cancer treatment programs and improving drug access. Limited reimbursement coverage and affordability concerns still challenge widespread use of G-CSFs. The market is gradually shifting toward biosimilars due to economic constraints. It relies on foreign partnerships and regulatory reforms to enhance treatment availability.

Middle East Chemotherapy Induced Neutropenia Market

The Middle East market stood at USD 35.12 million in 2024 and is expected to grow to USD 43.28 million by 2032, with a CAGR of 2.6%. The region contributed roughly 5.2% to the global Chemotherapy Induced Neutropenia Market share in 2024. High-income countries such as Saudi Arabia and the UAE invest significantly in oncology care and biologics procurement. Access to long-acting G-CSFs is concentrated in urban specialty hospitals. It is influenced by government-led healthcare modernization initiatives. Awareness campaigns and regional collaborations aim to expand supportive cancer therapies across wider populations.

Africa Chemotherapy Induced Neutropenia Market

Africa had a market value of USD 19.73 million in 2024, projected to reach USD 25.62 million by 2032, growing at a CAGR of 3.3%. The region accounted for about 2.9% of the global market share in 2024. Rising cancer prevalence, limited but growing healthcare funding, and international aid programs are driving market entry. South Africa and Egypt represent key markets with relatively better access to oncology drugs. It faces challenges due to infrastructure gaps and workforce shortages. Increasing availability of biosimilars and NGO-supported treatment access programs present growth potential over the forecast period.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key players

- Merck & Co., Inc.

- Aurobindo Pharma

- GSK plc

- Coherus BioSciences

- Teva Pharmaceuticals Industries Ltd.

- BeyondSpring Pharmaceuticals Inc.

- Pfizer Inc.

- Amgen Inc.

- Sandoz Group AG

- Fresenius Kabi

Competitive Analysis

The Global Chemotherapy Induced Neutropenia Market is highly competitive, with key players focusing on biosimilar development, strategic partnerships, and geographic expansion. Companies such as Amgen Inc., Pfizer Inc., and Teva Pharmaceuticals dominate with well-established G-CSF product lines and global distribution capabilities. Emerging players like Coherus BioSciences and BeyondSpring Pharmaceuticals are gaining traction through innovative delivery systems and differentiated therapies. Sandoz Group AG and Fresenius Kabi strengthen competition by offering affordable biosimilars, expanding access in price-sensitive markets. It maintains a dynamic structure as companies invest in R\&D, pursue regulatory approvals, and strengthen commercial presence. Competitive advantage hinges on pricing, clinical outcomes, and brand recognition within oncology care.

Market Concentration and Characteristics

The Global Chemotherapy Induced Neutropenia Market exhibits moderate to high market concentration, with a few multinational pharmaceutical companies dominating the landscape through established biologic therapies and strong global distribution networks. It is characterized by a high level of regulatory oversight, patent-protected innovations, and a growing presence of biosimilars that challenge originator products. The market is driven by clinical efficacy, treatment safety, and pricing competitiveness. Companies differentiate themselves through long-acting formulations, advanced delivery mechanisms, and integrated patient support programs. Barriers to entry remain significant due to complex manufacturing requirements and strict regulatory standards. Strategic collaborations and R&D investments continue to shape product pipelines and market positioning.

Report Coverage

The research report offers an in-depth analysis based on Type, Distribution Channel and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Biosimilar adoption is expected to rise steadily, reducing treatment costs and increasing access in emerging and developed regions.

- Single-dose, extended-release formulations will become standard in oncology protocols due to convenience and better patient compliance.

- Use of remote monitoring tools and adherence apps will enhance treatment continuity and reduce hospital admissions.

- Strong healthcare investments, rising cancer incidence, and domestic biosimilar production will drive regional expansion.

- Future pipelines may include targeted immunostimulatory agents and supportive therapies with dual functions to optimize patient outcomes.

- Data-driven risk assessment models will shape neutropenia management, minimizing overtreatment and improving resource efficiency.

- Collaborations between governments, non-profits, and pharmaceutical firms will improve access in underserved regions.

- Regulatory incentives for biosimilars and supportive care drugs will accelerate product approvals and market entry.

- Patients will increasingly shift to self-administration using wearable injectors and prefilled syringes to reduce hospital dependency.

- Growing biosimilar approvals and innovative delivery systems will foster a more competitive, cost-conscious market environment.