Market Overview

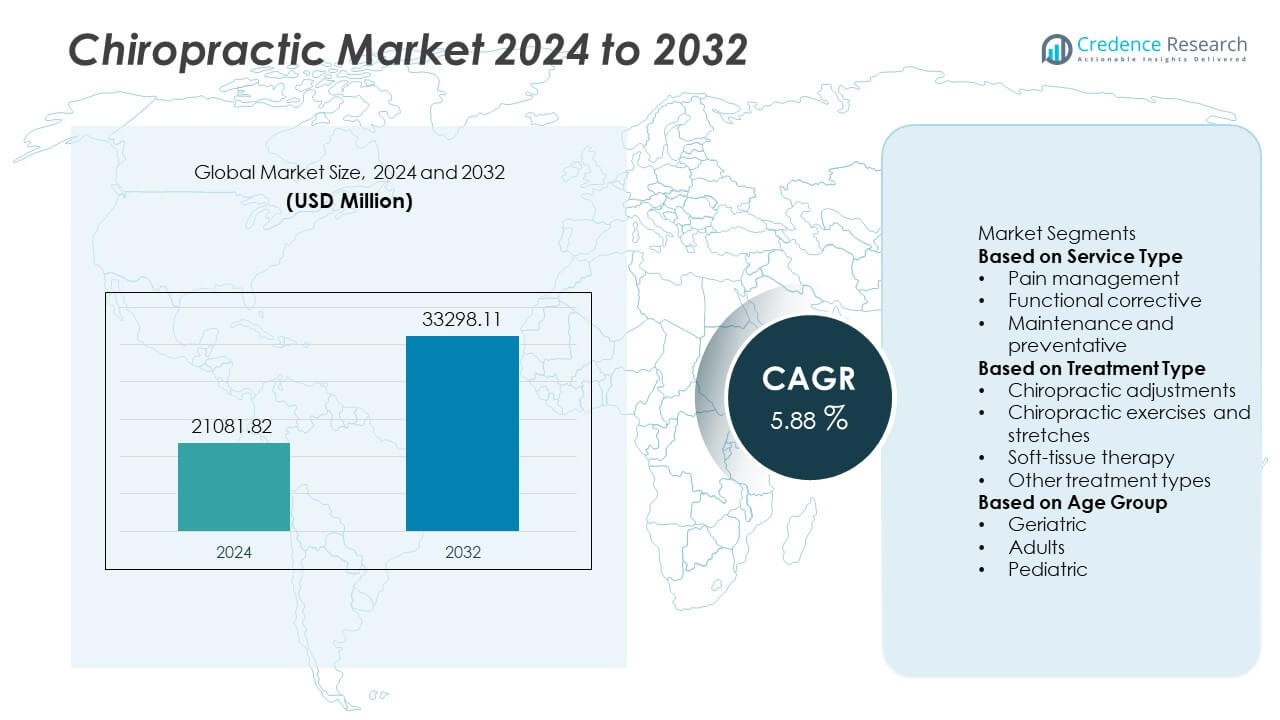

The Chiropractic Market was valued at USD 21,081.82 million in 2024 and is projected to reach USD 33,298.11 million by 2032, growing at a CAGR of 5.88% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Chiropractic Market Size 2024 |

USD 21,081.82 Million |

| Chiropractic Market, CAGR |

5.88% |

| Chiropractic Market Size 2032 |

USD 33,298.11 Million |

The chiropractic market is driven by prominent players such as Optimal Health Chiropractic, Life Chiropractic Centers, Atlas Chiropractic & Wellness, Activator Methods International, MH Sub I, LLC., AlignLife Systems, MaxLiving, HealthSource America’s Chiropractor, American Chiropractic Clinics, and Chiro One Wellness Center. These companies focus on offering personalized treatment programs, wellness-based chiropractic care, and digital posture assessment solutions. North America leads the market with a 43.6% share in 2024, supported by a high number of licensed practitioners and strong insurance coverage. Europe follows with a 27.4% share, driven by increasing preventive healthcare adoption, while Asia-Pacific, holding 20.8% share, is expanding rapidly with rising demand for non-invasive and holistic pain management solutions.

Market Insights

Market Insights

- The chiropractic market was valued at USD 21,081.82 million in 2024 and is projected to reach USD 33,298.11 million by 2032, registering a CAGR of 5.88% during the forecast period.

- Rising prevalence of musculoskeletal disorders, spinal misalignments, and chronic pain is driving the demand for non-invasive and drug-free chiropractic treatments. The pain management segment leads with a 52.4% share, supported by increasing adoption among adults and athletes.

- Digital health integration, AI-based posture analysis, and preventive wellness programs are key trends shaping market growth across clinics and wellness centers.

- Major players such as Optimal Health Chiropractic, Life Chiropractic Centers, MaxLiving, and HealthSource America’s Chiropractor focus on service expansion, digitalization, and patient-centered care models to strengthen market presence.

- North America dominates with a 43.6% share, followed by Europe at 27.4%, and Asia-Pacific with 20.8%, driven by growing awareness of holistic healthcare and advanced clinical infrastructure.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Service Type

The pain management segment dominates the chiropractic market, accounting for nearly 52.4% share in 2024. Its dominance is driven by the rising prevalence of chronic back pain, neck pain, and musculoskeletal disorders among working adults. Increasing awareness of non-invasive pain relief therapies has boosted patient preference for chiropractic adjustments over surgical procedures. The segment also benefits from higher demand among athletes and aging populations seeking drug-free pain management. Clinics offering customized pain therapy programs and posture correction treatments further contribute to sustained growth in this category.

- For instance, Chiro One Wellness Centers integrates motion-analysis technology and posture tracking to enhance musculoskeletal recovery outcomes. The company has clinics across several U.S. states and is recognized as a key player in the chiropractic care market.

By Treatment Type

The chiropractic adjustments segment leads the market with around 46.8% share in 2024, supported by its proven effectiveness in spinal alignment and pain reduction. Adjustments help improve mobility, relieve muscle tension, and enhance nervous system function. Growing use of manual and instrument-assisted techniques has strengthened its adoption among patients with musculoskeletal and posture-related issues. Integration of advanced diagnostic imaging and real-time assessment tools has improved treatment accuracy. Increasing practitioner availability and favorable insurance coverage continue to drive demand across both developed and emerging regions.

- For instance, Activator Methods International has trained approximately 150,000 licensed professionals worldwide in its instrument-assisted chiropractic technique, and the company’s flagship Activator V device is the first FDA-registered and FDA-cleared cordless electronic chiropractic adjustment instrument available today.

By Age Group

The adult segment holds the largest share of about 58.7% in 2024, fueled by high incidences of occupational stress, sedentary lifestyles, and sports-related injuries. Adults seek chiropractic services for pain management, posture correction, and preventive care. Growing corporate wellness programs and ergonomic health awareness have also boosted the adoption of chiropractic therapies. The geriatric group is expanding rapidly as aging populations experience higher rates of joint stiffness and degenerative conditions. Pediatric treatments are gaining attention for early spinal alignment and postural correction, though they represent a smaller market segment.

Key Growth Drivers

Rising Prevalence of Musculoskeletal Disorders

The growing incidence of musculoskeletal conditions such as back pain, neck pain, and joint stiffness is a major driver of the chiropractic market. Sedentary lifestyles, poor posture, and long working hours have increased the demand for non-surgical pain relief solutions. Chiropractic care offers effective, drug-free treatment that appeals to patients seeking holistic alternatives. With aging populations and growing awareness of spinal health, demand for chiropractic services continues to expand across hospitals, clinics, and rehabilitation centers globally.

- For instance, an observational study covering 852 chronic low back pain patients and 705 chronic neck pain patients found the average number of visits per month was 2.3, and the average duration of pain history among these patients was 14 years before seeking chiropractic care.

Growing Adoption of Non-Invasive Therapies

The increasing preference for non-invasive and cost-effective treatments is fueling market growth. Patients are shifting from conventional pain management involving medications or surgery to chiropractic therapies that offer long-term relief and improved mobility. Healthcare providers are incorporating chiropractic care into multidisciplinary treatment programs for chronic pain and physical rehabilitation. The reduced recovery time and minimal side effects of chiropractic treatments make them a favorable option in modern wellness care.

- For instance, HealthSource America is a prominent chiropractic franchise network that utilizes a comprehensive approach including non-invasive adjustments and rehabilitation, with various locations monitoring patient improvement and recovery efficiency.

Expansion of Chiropractic Clinics and Insurance Coverage

The rapid establishment of specialized chiropractic clinics and growing insurance support are accelerating market expansion. Governments and private insurers are increasingly recognizing chiropractic care as a legitimate form of treatment, improving accessibility. The rise of wellness centers and franchise-based chiropractic chains has strengthened patient reach in urban areas. Moreover, integration of digital appointment systems, teleconsultation, and outcome tracking tools has enhanced patient experience, boosting overall adoption rates globally.

Key Trends & Opportunities

Integration of Digital Health and AI Tools

Technological advancements such as digital posture assessment, AI-based spinal analysis, and wearable health trackers are transforming chiropractic practices. These tools enable real-time monitoring, personalized treatment plans, and enhanced diagnostic precision. Clinics adopting AI-integrated diagnostic systems are improving patient outcomes while reducing manual workload. The trend toward data-driven chiropractic care is opening new opportunities for technology providers and expanding the market’s appeal among tech-savvy consumers.

- For instance, AlignLife Systems utilized the PostureScreen Mobile platform across some clinics, using photographic-based analysis to assess posture, which can be a reliable and valid screening tool in clinical settings when anatomical landmarks are carefully identified.

Rising Demand for Preventive and Wellness Care

A growing emphasis on preventive health and lifestyle management is creating new growth opportunities for chiropractors. Patients are increasingly seeking maintenance and corrective treatments to prevent future injuries and maintain spine health. The global wellness movement, combined with corporate health initiatives, is driving demand for routine chiropractic checkups. The trend toward holistic wellness and physical therapy integration supports long-term growth prospects for the chiropractic sector.

- For instance, MaxLiving operates over 160 clinics across North America, offering structured wellness programs based on its “5 Essentials” approach that includes spinal adjustments, customized exercise routines, and nutritional counseling to promote long-term preventive spine care and physical well-being.

Key Challenges

Limited Awareness and Misconceptions

Despite growing adoption, limited public awareness and misconceptions about chiropractic treatment effectiveness hinder market growth. Many patients remain unaware of its therapeutic benefits or associate it with unregulated alternative medicine. In several developing countries, lack of formal training and certification programs also reduces credibility. Increasing educational campaigns and professional standardization efforts are essential to improve trust and expand patient acceptance.

Regulatory and Reimbursement Barriers

The absence of uniform regulations and inconsistent reimbursement policies remain major challenges. In many regions, chiropractic services face limited insurance coverage, making them less accessible to lower-income patients. Licensing restrictions and differing regional laws also affect practice expansion. Establishing clear regulatory frameworks and broadening reimbursement structures will be critical for ensuring sustainable growth and global standardization within the chiropractic market.

Regional Analysis

North America

North America dominates the chiropractic market with a 43.6% share in 2024, supported by a well-established healthcare system, high awareness of spinal health, and a strong presence of licensed practitioners. The United States leads the region, driven by increasing adoption of chiropractic treatments for pain management and sports injuries. Insurance coverage for chiropractic services and the integration of wellness programs in corporate healthcare further enhance market growth. Canada also contributes significantly through expanding clinical infrastructure and growing acceptance of non-invasive therapies among patients seeking long-term musculoskeletal care.

Europe

Europe holds a 27.4% share in 2024, driven by rising demand for preventive healthcare and non-surgical treatments. Countries such as Germany, the United Kingdom, and France are leading adopters of chiropractic care, supported by growing patient awareness and favorable regulatory frameworks. The increasing prevalence of lifestyle-related back and neck disorders has accelerated the adoption of spinal manipulation therapies. Expanding chiropractic education programs and recognition of chiropractic treatment within national health systems continue to strengthen the market presence across the region, with steady patient inflow into private and wellness clinics.

Asia-Pacific

Asia-Pacific accounts for a 20.8% share in 2024, fueled by rising disposable income, urbanization, and growing awareness of alternative therapies. Countries like Australia, Japan, China, and India are witnessing a surge in chiropractic clinic establishments, driven by increasing cases of chronic pain and posture-related issues. Expanding middle-class populations and the influence of Western wellness trends are boosting acceptance of chiropractic treatments. The presence of international chiropractic associations and training institutions is helping standardize practices and increase trust among patients across emerging Asian economies, supporting market expansion.

Latin America

Latin America represents a 5.1% share in 2024, led by Brazil, Mexico, and Argentina. The growing burden of musculoskeletal conditions and sports-related injuries has raised demand for chiropractic therapies. Increasing collaboration between chiropractors and physiotherapists has enhanced clinical outcomes and patient confidence. Although awareness levels are moderate, expanding private clinics and the entry of trained practitioners are improving accessibility. Governments are gradually recognizing chiropractic services as part of complementary healthcare, which is expected to support long-term growth across urban centers and medical tourism hubs in the region.

Middle East & Africa

The Middle East & Africa region holds a 3.1% share in 2024, driven by rising healthcare investments and growing interest in holistic pain management. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are witnessing increased establishment of chiropractic centers within multidisciplinary clinics. The market benefits from the rising expatriate population and expanding wellness tourism. However, limited practitioner availability and lack of public awareness continue to restrain faster growth. Ongoing efforts to regulate chiropractic practice and integrate it into mainstream healthcare are expected to strengthen regional adoption.

Market Segmentations:

By Service Type

- Pain management

- Functional corrective

- Maintenance and preventative

By Treatment Type

- Chiropractic adjustments

- Chiropractic exercises and stretches

- Soft-tissue therapy

- Other treatment types

By Age Group

- Geriatric

- Adults

- Pediatric

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis of the chiropractic market highlights the presence of major players such as Optimal Health Chiropractic, Life Chiropractic Centers, Atlas Chiropractic & Wellness, Activator Methods International, MH Sub I, LLC., AlignLife Systems, MaxLiving, HealthSource America’s Chiropractor, American Chiropractic Clinics, and Chiro One Wellness Center. These companies focus on expanding service portfolios, improving patient outcomes, and adopting digital health tools for advanced posture and spinal analysis. The market remains moderately fragmented, with leading players emphasizing franchise-based expansion and personalized wellness programs. Strategic partnerships, marketing initiatives, and integration of AI-driven diagnostics are enhancing competitiveness. Moreover, investments in training programs, teleconsultation, and patient engagement technologies are helping strengthen brand visibility and client retention. Growing focus on preventive and holistic care positions these providers strongly in meeting evolving consumer preferences for non-invasive and evidence-based chiropractic treatments.

Key Player Analysis

- Optimal Health Chiropractic

- Life Chiropractic Centers

- Atlas Chiropractic & Wellness

- Activator Methods International

- MH Sub I, LLC.

- AlignLife Systems

- MaxLiving

- HealthSource America’s Chiropractor

- American Chiropractic Clinics

- Chiro One Wellness Center

Recent Developments

- In October 2025, Chiro One Wellness Center began accepting select Medicare and Medicaid plans in Kansas and Missouri clinics, expanding access for seniors and families.

- In December 2024, AlignLife Systems was featured in Newsweek for its expansion and care model, highlighting national growth momentum.

- In August 2024, Chiro One Wellness Center opened a clinic inside Cleveland University-Kansas City’s Professional Building in Overland Park, Kansas.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Service Type, Treatment Type, Age Group and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for chiropractic care will grow as awareness of non-invasive pain management increases.

- Integration of AI and digital posture analysis tools will enhance treatment precision and outcomes.

- Preventive and wellness-based chiropractic programs will gain popularity among working adults.

- Expansion of franchise-based clinics will improve accessibility in both developed and emerging markets.

- Insurance coverage for chiropractic treatments will strengthen adoption and patient affordability.

- Collaborations with physiotherapy and rehabilitation centers will boost multidisciplinary care models.

- Online consultations and digital scheduling platforms will streamline patient engagement.

- Aging populations will drive higher demand for chronic pain and mobility-related chiropractic services.

- Educational and certification programs will expand, improving practitioner quality and global standardization.

- Focus on holistic, evidence-based, and personalized treatment approaches will shape the market’s long-term growth.