Market Overview:

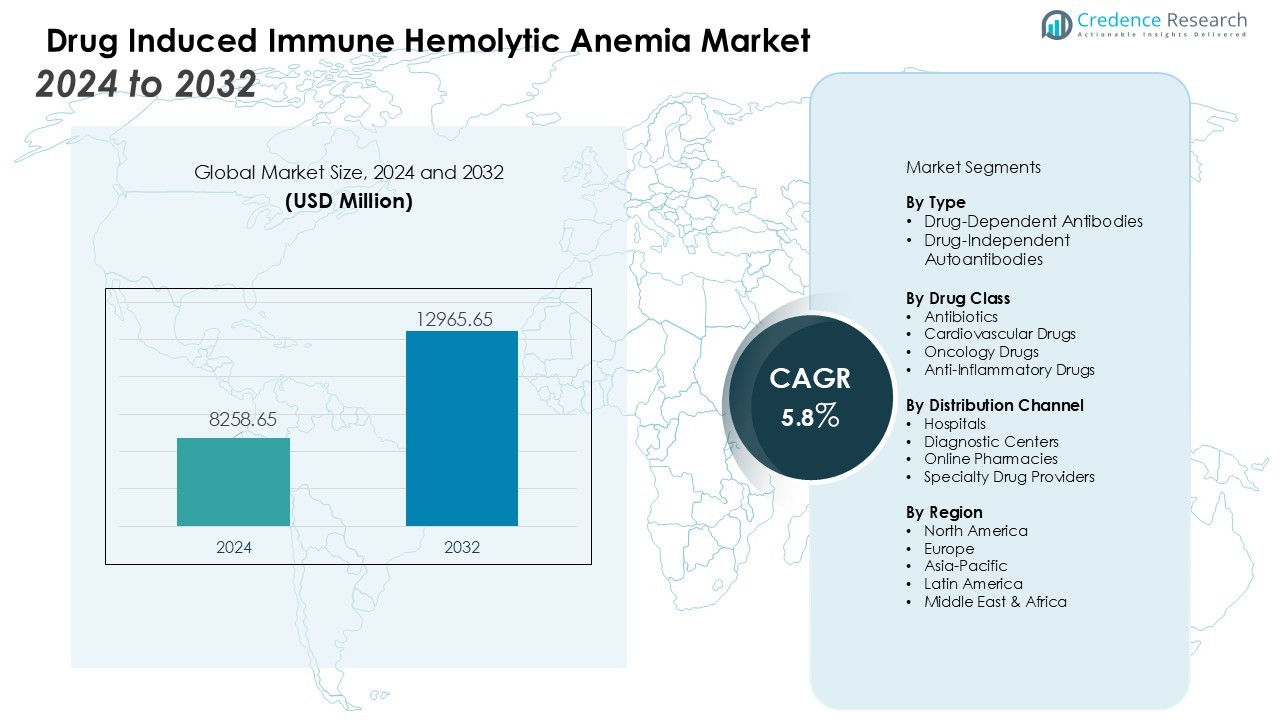

The drug induced immune hemolytic anemia market size was valued at USD 8258.65 million in 2024 and is anticipated to reach USD 12965.65 million by 2032, at a CAGR of 5.8 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Drug Induced Immune Hemolytic Anemia Market Size 2024 |

USD 8258.65 Million |

| Drug Induced Immune Hemolytic Anemia Market, CAGR |

5.8 % |

| Drug Induced Immune Hemolytic Anemia Market Size 2032 |

USD 12965.65 Million |

Market growth is driven by rising incidence of drug-related immune reactions, expanding use of high-risk therapeutics, and wider availability of Coombs testing, flow cytometry, and specialized antibody panels. Increased pharmacovigilance initiatives, stronger regulatory focus on adverse drug event reporting, and continuous updates to clinical management guidelines further support adoption of diagnostic and treatment pathways. Growing emphasis on personalized medicine and improved characterization of drug-antibody interactions enhances clinical decision-making and strengthens market progression.

Regionally, North America leads due to robust diagnostic infrastructure, high awareness, and strong reporting mechanisms. Europe follows with established transfusion medicine networks and standardized immunohematology practices. Asia-Pacific is poised for the fastest growth as healthcare modernization, improved laboratory capacity, and rising drug utilization increase detection and treatment rates across emerging economies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The drug induced immune hemolytic anemia market grows from USD 8258.65 million in 2024 to USD 12965.65 million by 2032, supported by a CAGR of 5.8% and strengthened by rising drug-related immune reactions.

- Increasing use of high-risk therapeutics, including antibiotics, NSAIDs, and oncology agents, boosts demand for early detection and advanced diagnostic workflows.

- Advancements in Coombs testing, flow cytometry, and automated platforms enhance diagnostic accuracy and accelerate case identification across hospital networks.

- Heightened pharmacovigilance efforts and stricter regulatory oversight improve adverse drug event reporting, raising confirmed DIIHA detection rates.

- Growing focus on personalized medicine and immunologic profiling supports safer prescribing practices and increases adoption of monitoring tools.

- Limited diagnostic awareness, complex antibody identification, and uneven access to advanced assays continue to restrict timely detection in low-resource settings.

- North America leads with strong diagnostic infrastructure, Europe progresses with standardized immunohematology networks, and Asia-Pacific records the fastest growth driven by expanding healthcare capacity.

Market Drivers:

Rising Exposure to High-Risk Therapeutic Drug Classes Strengthens Market Expansion

Growing prescription volumes of antibiotics, nonsteroidal anti-inflammatory drugs, and oncology agents elevate the frequency of immune-mediated hemolytic reactions. Increased dependence on combination pharmacotherapy widens the pool of patients vulnerable to drug-induced antibody formation. Clinicians monitor these drug classes more carefully, which supports earlier identification of DIIHA cases. The drug induced immune hemolytic anemia market benefits from this heightened vigilance because it drives demand for advanced diagnostic workflows.

- For example, Beckman Coulter offers the DxH 900 automated hematology analyzer, which processes up to 100 samples per hour, to provide advanced blood cell analysis.

Advancements in Immunohematology Diagnostics Improve Case Detection

Progress in Coombs testing, specialized antiglobulin assays, and flow cytometry improves diagnostic precision. Laboratories deploy automated platforms that shorten turnaround times and support high-volume screening. It enables clinicians to differentiate drug-dependent antibodies from other hemolytic causes with greater confidence. The drug induced immune hemolytic anemia market gains momentum through the adoption of these technologies across hospital networks.

- For Instance, The Ortho Vision analyzer focuses on automation and reducing manual steps rather than a high sample throughput rate. It achieves an average turnaround time of approximately 25 minutes for routine tests, with 95% of results available in under 40 minutes.

Intensified Pharmacovigilance and Regulatory Oversight Elevate Reporting Rates

Health authorities enforce stricter adverse event documentation standards, which improves visibility of DIIHA across therapeutic settings. Pharmacovigilance teams track drug-induced reactions more systematically, which increases confirmed case reporting. Hospitals integrate electronic monitoring systems that flag hemolytic patterns linked to specific drug exposures. The drug induced immune hemolytic anemia market advances when stronger oversight supports consistent data collection.

Growing Emphasis on Personalized Therapy and Safer Prescribing Practices Encourages Wider Adoption of Monitoring Tools

Clinicians prioritize tailored drug selection to minimize immune-mediated risks, which increases the use of patient-specific monitoring strategies. Genetic and immunologic profiling improves understanding of individual susceptibility to hemolysis. It encourages earlier intervention and more appropriate therapeutic adjustments. The drug induced immune hemolytic anemia market gains support from the shift toward precision-based clinical practice.

Market Trends:

Growing Integration of Advanced Diagnostic Technologies Reshapes Clinical Practice

Healthcare providers adopt high-sensitivity immunohematology platforms that improve the detection of drug-dependent antibodies. Automated Coombs testing systems shorten analysis time and reinforce laboratory efficiency. It supports broader screening in patients receiving high-risk drug classes and improves clinical confidence in differential diagnosis. Digital pathology and AI-supported image interpretation gain traction and enhance accuracy in complex hemolytic profiles. Hospitals invest in integrated data platforms that link laboratory findings with pharmacologic histories to refine decision support. The drug induced immune hemolytic anemia market reflects this shift toward technology-driven diagnostic precision and wider adoption of standardized testing workflows.

- For Instance, Bio-Rad Laboratories’ IH-1000 analyzer uses gel technology, which has shown high sensitivity in detecting weak IgG antibodies on red blood cells, often superior to manual tube testing. Automated Coombs testing systems like the IH-1000 shorten analysis time, reduce manual errors, and reinforce laboratory efficiency through lean automation and high throughput capabilities.

Rising Preference for Precision-Based Prescribing and Individualized Risk Stratification

Clinicians align therapeutic decisions with patient-specific immunologic and genetic markers to reduce hemolytic complications. Real-world evidence reporting strengthens predictive models that identify high-risk drug combinations. It supports dynamic treatment adjustments and reduces the likelihood of severe immune-mediated reactions. Pharmaceutical companies focus on developing safer formulations that demonstrate lower immunogenicity across routine clinical use. Clinical guidelines highlight structured monitoring pathways that enhance early recognition of hemolytic patterns. The drug induced immune hemolytic anemia market benefits from growing emphasis on precision care, which promotes consistent use of surveillance tools and risk mitigation strategies across healthcare systems.

- For instance, Roche developed the IDH1 R132H (MRQ-67) Rabbit Monoclonal Antibody test, which detects the specific R132H mutation in the IDH1 gene using immunohistochemistry for precise glioma treatment stratification.

Market Challenges Analysis:

Limited Diagnostic Awareness and Complexity of Antibody Identification Restrict Timely Detection

Clinicians and laboratory teams face challenges in recognizing early indicators of drug-dependent hemolysis, which delays intervention. Diagnostic complexity increases when antibody patterns mimic other immune-mediated conditions. It demands specialized expertise that many facilities do not possess. Inconsistent availability of advanced immunohematology assays widens the gap between detection needs and actual capabilities. Reporting accuracy suffers when low-resource centers rely on basic testing methods. The drug induced immune hemolytic anemia market encounters structural barriers that slow adoption of comprehensive diagnostic workflows.

Variability in Drug Response and Lack of Standardized Monitoring Pathways Limit Consistent Management

Patient responses differ widely due to individual immunologic profiles, which complicates risk assessment. Health systems struggle to implement uniform monitoring protocols across diverse clinical environments. It reduces the predictability of treatment decisions and raises the potential for recurrent hemolytic episodes. Limited clinical data for rare drug-induced reactions restricts the development of evidence-based guidelines. Pharmaceutical labeling often lacks detailed risk stratification insights that clinicians need. The drug induced immune hemolytic anemia market faces obstacles that stem from inconsistent clinical practices and fragmented real-world data.

Market Opportunities:

Expansion of Advanced Diagnostic Solutions Creates Strong Commercial Potential

Healthcare providers invest in high-sensitivity antibody detection platforms that support faster and more accurate identification of drug-induced hemolysis. AI-supported interpretation tools improve diagnostic confidence and reduce the burden on specialized laboratory personnel. It encourages broader screening of patients exposed to high-risk drug categories. Integrated clinical decision systems link laboratory data with medication records, which strengthens case management. Hospitals seek automated workflows that reduce manual errors and improve turnaround time. The drug induced immune hemolytic anemia market gains significant opportunities through growing demand for precision-driven diagnostic technologies.

Rising Focus on Personalized Therapy and Drug Safety Optimization Accelerates Innovation

Clinicians explore individualized monitoring pathways that align drug selection with patient-specific immunologic risk profiles. Pharmaceutical companies pursue safer formulations that demonstrate lower immunogenicity and fewer hemolytic triggers. It creates opportunities for collaborative research that evaluates real-world patient outcomes. Digital health platforms enable continuous tracking of adverse reactions, which expands data availability for predictive modeling. Healthcare systems prioritize safer prescribing frameworks that require reliable monitoring tools. The drug induced immune hemolytic anemia market benefits from a strong shift toward risk-based, patient-centered care strategies.

Market Segmentation Analysis:

By Type

The segment covers drug-dependent antibodies and drug-independent autoantibodies that trigger hemolytic reactions. Drug-dependent antibodies dominate due to high exposure to antibiotics, NSAIDs, and chemotherapeutic agents that frequently induce immune responses. It drives strong demand for specialized Coombs testing and advanced antibody characterization tools. Drug-independent autoantibodies form a smaller share, yet they require complex diagnostic pathways to distinguish them from primary autoimmune hemolytic anemia. Hospitals prioritize clear differentiation to guide appropriate treatment. The drug induced immune hemolytic anemia market reflects steady adoption of refined diagnostic methods across both antibody types.

- For instance, piperacillin, an antibiotic, has been clinically shown to induce drug-dependent antibodies that lead to severe hemolytic reactions, with documented cases of patients experiencing a drop in red blood cell count from 2.7 to 1.8 × 10^12/L after piperacillin exposure, requiring careful antibody monitoring for effective diagnosis and treatment.

By Drug Class

Antibiotics remain the leading drug class associated with immune-mediated hemolysis, driven by widespread prescribing in acute and chronic care. Cardiovascular drugs and oncology therapies form growing segments as their expanded use elevates immune sensitivity in vulnerable populations. It increases the requirement for close monitoring and targeted antibody detection. Anti-inflammatory drugs contribute a steady share due to known hemolytic risks in long-term use. Pharmacovigilance programs track these classes to support safer prescribing and stronger risk management.

- For Instance, Pfizer maintains a portfolio of anti-infective products and operates one of the world’s largest antimicrobial resistance (AMR) surveillance programs, known as the ATLAS database.

By Distribution Channel

Hospitals hold the largest share due to advanced laboratory capacity, rapid diagnostic access, and structured monitoring protocols. Diagnostic centers contribute meaningful growth as they adopt automated immunohematology systems to support outpatient testing demands. It helps clinicians manage suspected cases without hospitalization. Online pharmacies and specialty drug providers expand slowly through improved access to supportive medications. The drug induced immune hemolytic anemia market benefits from stronger integration between diagnostic providers and clinical care pathways.

Segmentations:

By Type

- Drug-Dependent Antibodies

- Drug-Independent Autoantibodies

By Drug Class

- Antibiotics

- Cardiovascular Drugs

- Oncology Drugs

- Anti-Inflammatory Drugs

By Distribution Channel

- Hospitals

- Diagnostic Centers

- Online Pharmacies

- Specialty Drug Providers

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Strong Diagnostic Infrastructure Positions North America at the Forefront of Market Growth

North America maintains a dominant position due to advanced immunohematology laboratories and high adoption of automated diagnostic platforms. Hospitals deploy standardized Coombs testing and flow cytometry tools that support rapid identification of drug-induced hemolysis. It strengthens timely intervention and reduces complications linked to high-risk drug exposure. Regulatory agencies enforce strict pharmacovigilance frameworks that enhance reporting consistency across healthcare systems. Clinical awareness remains high because physicians regularly monitor drug safety profiles and integrate decision-support tools into routine care. The drug induced immune hemolytic anemia market expands in the region as health systems prioritize diagnostic accuracy and adverse event prevention.

Established Clinical Networks and Strong Surveillance Programs Support Europe’s Steady Progress

Europe records steady growth driven by structured transfusion medicine networks and uniform diagnostic guidelines. National health systems invest in centralized laboratory services that improve access to specialized antibody detection. It encourages harmonized testing standards across public and private healthcare facilities. Pharmacovigilance programs maintain strong oversight of high-risk drug classes and ensure timely documentation of immune-mediated reactions. Research institutions collaborate with regulatory bodies to refine diagnostic algorithms and improve detection of rare hematologic events. The region benefits from continued emphasis on patient safety and the integration of digital monitoring platforms.

Expanding Healthcare Capacity Accelerates Adoption Across Asia-Pacific and Emerging Regions

Asia-Pacific shows the fastest growth due to rising drug utilization, expanding hospital infrastructure, and improved laboratory capabilities. Governments increase investments in diagnostic modernization, which strengthens early identification of hemolytic events linked to widely used antibiotics and oncology drugs. It supports greater awareness among clinicians who manage large patient populations with complex therapeutic needs. Private diagnostic chains adopt automated immunohematology systems that improve turnaround times and broaden testing access. Latin America and the Middle East & Africa follow similar trends as healthcare systems scale laboratory services and expand pharmacovigilance participation. The drug induced immune hemolytic anemia market gains long-term potential across these regions through capacity building and stronger clinical oversight.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Hoffmann-La Roche Ltd

- Viatris Inc.

- Teva Pharmaceutical Industries Ltd.

- Sanofi

- Lupin

- Johnson & Johnson Services, Inc.

- Novartis AG

- Incyte

- Rigel Pharmaceuticals, Inc.

- Alpine Immune Sciences

Competitive Analysis:

The competitive landscape reflects steady activity as diagnostic companies and pharmaceutical manufacturers strengthen their presence in niche hematology markets. Key players include F. Hoffmann-La Roche Ltd, Viatris Inc., Teva Pharmaceutical Industries Ltd., Sanofi, and Lupin. These companies invest in assay innovation, supportive therapeutics, and digital tools that enhance the detection and management of drug-induced hemolysis. It encourages broader adoption of high-sensitivity antibody testing, Coombs methodologies, and integrated clinical decision platforms. Strategic partnerships with hospitals and diagnostic networks help expand access to specialized immunohematology solutions. Market participants also pursue research initiatives that focus on drug safety optimization and improved adverse event surveillance. The drug induced immune hemolytic anemia market gains competitive momentum through technology-driven advancements and stronger alignment between clinical needs and product development pathways.

Recent Developments:

- In July 2025, Sanofi announced the acquisition of Vicebio, a vaccine biotech firm, to expand its respiratory vaccines portfolio, with closing expected in Q4 2025.

- In November 2025, Sanofi and Regeneron presented positive Phase 3 data on Dupixent for Allergic Fungal Rhinosinusitis (AFRS), marking a significant advancement in immunology treatment.

Report Coverage:

The research report offers an in-depth analysis based on Type, Drug Class, Distribution Channel and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The market will advance through wider adoption of automated immunohematology platforms that improve accuracy in detecting drug-dependent antibodies.

- Growing integration of AI-enabled diagnostic support will strengthen clinical interpretation and reduce diagnostic uncertainty.

- Pharmacovigilance programs will expand their datasets, which will enhance predictive modeling for high-risk drug combinations.

- Healthcare providers will implement stronger monitoring frameworks that support early intervention in vulnerable patient groups.

- Drug manufacturers will focus on safer formulations with reduced immunogenic potential across frequently prescribed therapies.

- Digital health systems will capture real-time hemolytic trends, which will support faster response pathways.

- Clinical guidelines will incorporate more detailed risk-stratification criteria that improve therapeutic decision-making.

- Diagnostic centers will adopt high-throughput testing platforms that increase screening capacity and shorten turnaround times.

- Research collaborations will explore advanced biomarker panels that refine differentiation between immune-mediated hemolysis types.

- The drug induced immune hemolytic anemia market will benefit from sustained innovation in diagnostic technology and expanded global awareness of drug safety.