Fuel Storage Tank Market Overview:

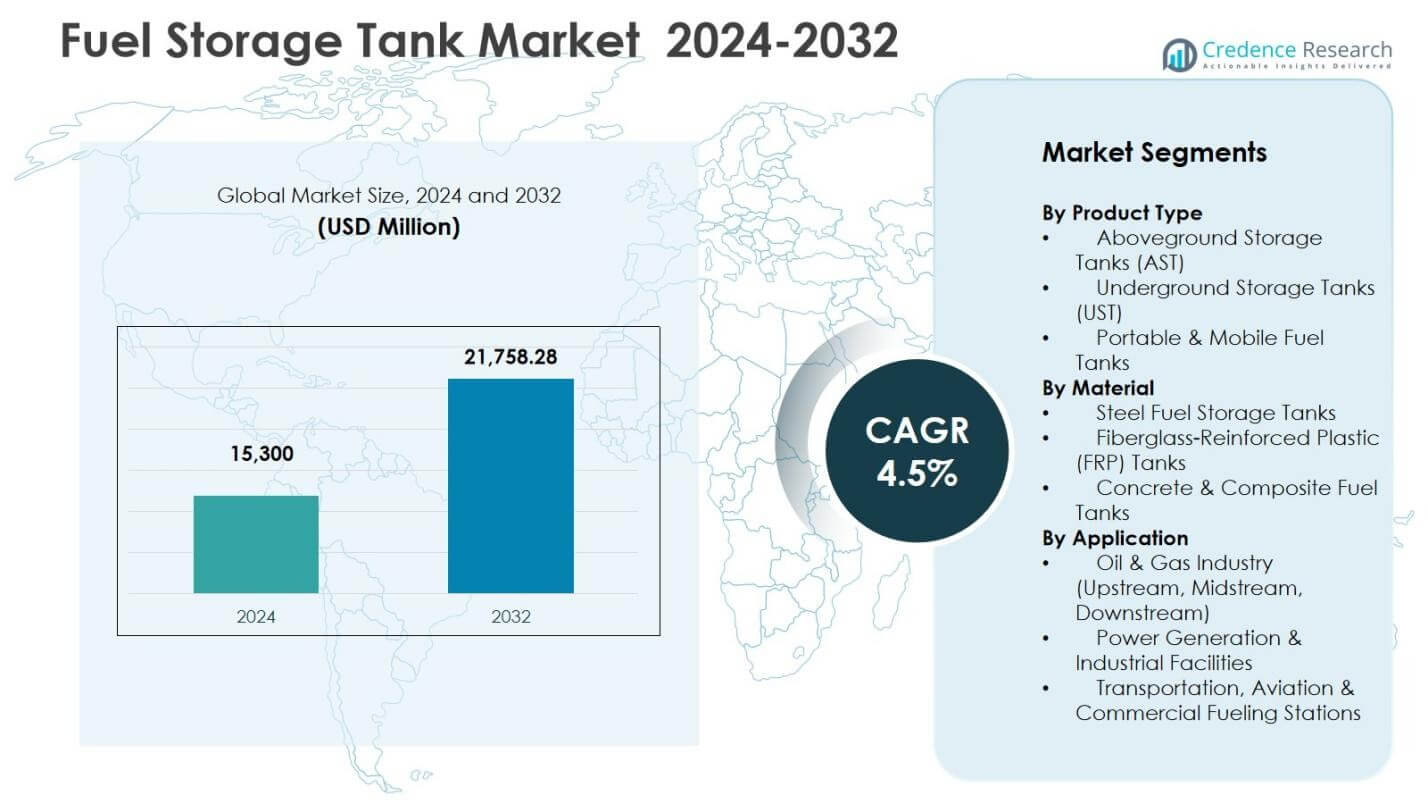

Fuel Storage Tank Market size was valued USD 15,300 Million in 2024 and is anticipated to reach USD 21,758.28 Million by 2032, at a CAGR of 4.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Fuel Storage Tank Market Size 2024 |

USD 15,300 million |

| Fuel Storage Tank Market, CAGR |

4.5% |

| Fuel Storage Tank Market Size 2032 |

USD 21,758.28 million |

Fuel Storage Tank Market Insights

- Market overview highlights strong demand for large-capacity storage infrastructure across oil and gas, power generation, and industrial facilities, with Aboveground Storage Tanks leading the market with a 56.2% share in 2024.

- Market drivers include refinery expansion, strategic fuel reserve development, modernization of terminal networks, and increasing adoption of durable steel and FRP tank systems to support safety, reliability, and long-term operational efficiency.

- Market trends indicate rising use of modular and portable storage tanks, integration of smart monitoring and leak-detection technologies, and product enhancement initiatives by leading manufacturers focusing on design improvement and lifecycle maintenance solutions.

- Regional analysis shows North America holding 31.6% share in 2024 due to strong infrastructure investment, Asia-Pacific accounting for 28.9% share with rapid industrial growth, and Europe contributing 23.8% share through regulatory-driven asset upgrades and storage expansion initiatives.

Fuel Storage Tank Market Segmentation Analysis:

By Product Type

The Fuel Storage Tank Market by product type is led by Aboveground Storage Tanks (AST), which accounted for 56.2% share in 2024, driven by easier installation, lower maintenance costs, and strong adoption across fuel depots and industrial facilities. Underground Storage Tanks (UST) continue to gain traction in urban and retail fueling environments, particularly where space optimization and safety compliance are priorities. Portable and mobile fuel tanks serve niche applications such as construction, mining, and remote power operations, supported by the rising demand for onsite refueling and flexible fuel logistics.

- For instance, ExxonMobil hired Matrix Service to construct four 500,000-barrel ASTs at its Webster Station in Texas, featuring domed external floating roofs for enhanced emission control and weather protection.

By Material

In the material segment, Steel Fuel Storage Tanks dominated the market with 61.7% share in 2024, owing to their structural strength, high durability, and suitability for large-capacity storage in oil and gas and industrial operations. Fiberglass-Reinforced Plastic (FRP) tanks are expanding their presence due to corrosion resistance, longer service life, and compliance with stringent environmental regulations. Concrete and composite tanks secure demand in infrastructure and stationary bulk storage applications, supported by safety standards and lifecycle cost advantages in long-term fuel storage environments.

- For instance, KBK Industries offers UL 1316-certified double-wall underground FRP fuel storage tanks for retail fuel stations, backed by a 30-year limited warranty. A&Z Company under OKET Group produces FRP double-wall underground fuel tanks with advanced 3DFF technology introduced from ZCL Canada, achieving the first UL certification for such tanks in China.

By Application

By application, the Oil & Gas Industry remained the leading segment with 48.9% share in 2024, supported by continuous investment across upstream, midstream, and downstream facilities, along with increasing global fuel storage capacity expansion initiatives. Power generation and industrial facilities represent the next major demand center, driven by backup fuel storage requirements and steady reliance on diesel and liquid fuels in industrial operations. Transportation, aviation, and commercial fueling stations continue to adopt modernized storage systems, supported by network expansion, regulatory upgrades, and rising aviation and logistics fuel consumption.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Fuel Storage Tank Market Overview

Key Growth Drivers

Expansion of Oil & Gas Infrastructure

The Fuel Storage Tank Market grows significantly due to continuous expansion of upstream, midstream, and downstream oil and gas infrastructure. Refinery capacity additions, strategic petroleum reserves, and terminal expansions increase the demand for large-capacity storage tanks across global energy networks. Rising consumption of diesel, gasoline, aviation fuel, and marine fuels strengthens investment in storage terminals and distribution hubs. Governments and energy companies prioritize storage infrastructure to enhance supply security and mitigate price volatility, while emerging economies accelerate tank demand through refinery modernization, logistics development, and bulk fuel storage initiatives supporting industrialization and energy trade activities.

- For instance, Dangote Petroleum Refinery is building eight new crude storage tanks with a combined 6.3 million-barrel capacity. This 41% expansion raises total storage from 2.4 billion liters to 3.4 billion liters, improving operational flexibility amid supply challenges.

Increasing Demand from Power Generation and Industrial Sectors

Fuel storage tanks experience strong adoption across power generation and industrial facilities due to the reliance on backup fuel systems, distributed power units, and captive energy generation. Diesel and liquid fuel storage remains essential for grid-support systems, remote industrial operations, and standby power plants. Growth in mining, manufacturing, and construction activities further drives demand for onsite and mobile fuel storage tanks. Industries adopt advanced storage solutions to ensure operational continuity, improve energy resilience, and meet safety compliance norms, while energy transition initiatives also create requirements for dual-fuel and hybrid storage infrastructure in industrial environments.

- For instance, Fuelquip Industries delivered a 110KL double-contained tank split into compartments for diesel, ultimate diesel, and AdBlue to support mining fleet operations. This setup ensures continuous fuel for heavy machinery in remote areas, minimizing refueling disruptions.

Rising Focus on Safety, Environmental Compliance, and Asset Modernization

Stringent environmental regulations and safety compliance standards drive the modernization and replacement of aging storage infrastructure, boosting demand for technologically advanced fuel storage tanks. Operators invest in double-wall tank systems, corrosion-resistant materials, leak-detection technologies, and secondary containment structures to reduce environmental risks and operational losses. Regulatory audits and safety inspections accelerate retrofitting and tank replacement programs across industrial, commercial, and transportation fuel facilities. The integration of monitoring systems, automation, and maintenance-focused tank designs enhances reliability and extends asset lifecycle, encouraging sustained investment in high-performance and regulation-compliant storage tank solutions worldwide.

Key Trends & Opportunities

Adoption of Advanced Materials, Smart Monitoring, and Modular Tank Designs

A major trend shaping the Fuel Storage Tank Market is the shift toward advanced materials, modular construction, and digital monitoring technologies. Steel and composite hybrid tanks, corrosion-resistant coatings, and FRP materials support longer service life and lower maintenance requirements, creating opportunities for material innovation. Smart tank monitoring systems with IoT sensors, predictive maintenance platforms, and automated fuel-level management enhance operational safety and efficiency. Modular and prefabricated storage tanks enable faster installation and scalability, particularly in industrial, defense, mining, and remote infrastructure projects, where cost-effective and rapidly deployable storage solutions are increasingly preferred.

- For instance, Extraco Composites offers UL-approved FRP fuel storage tanks with single and double-wall designs, where inner and outer walls plus ribs form a structural system rated for a minimum 30-year life under truck, soil, and vacuum loads.

Growing Opportunities in Aviation, Logistics, and Remote Fueling Applications

Expanding aviation networks, e-commerce logistics, and remote industrial operations create strong opportunities for fuel storage tanks across airports, fleet depots, and transportation hubs. Rising air traffic and aviation fuel consumption drive investments in bulk jet-fuel storage facilities and hydrant supply systems. Logistics and commercial fleet operators adopt mobile and portable fuel tanks to support onsite refueling and fleet efficiency. Remote construction, mining, and energy exploration activities require durable storage systems capable of operating in harsh environments, generating additional demand for portable, skid-mounted, and field-deployable storage tank solutions across global industrial and mobility sectors.

- For instance, Air bp introduced its next-generation mobile refueling units with digital fuel tracking for airport and ground fleet applications across Europe.

Key Challenges

Environmental Risks, Leakage Concerns, and Regulatory Compliance Burden

The Fuel Storage Tank Market faces significant challenges related to environmental risk management, leakage prevention, and regulatory compliance across multiple jurisdictions. Aging storage facilities increase risks of soil contamination, groundwater pollution, and hazardous emissions, leading to costly remediation and legal liabilities for operators. Compliance with evolving safety standards, tank inspection protocols, and emission control regulations requires continuous investment in monitoring, retrofitting, and infrastructure upgrades. Smaller facility operators experience financial pressure due to maintenance costs and regulatory documentation requirements, while stricter enforcement policies increase operational complexity across industrial and commercial fuel storage environments.

High Capital Costs, Installation Constraints, and Technical Skill Requirements

High initial capital investment for large-capacity and technologically advanced fuel storage tanks poses a challenge for cost-sensitive industries and developing-market operators. Installation complexity, site preparation requirements, and permitting approvals extend project timelines and increase deployment costs. Space limitations in urban and industrial locations restrict the adoption of conventional storage systems, driving the need for specialized engineering and customized tank configurations. Skilled workforce availability for installation, inspection, and maintenance remains limited in several regions, creating operational constraints and increasing dependency on specialized service providers for safe and compliant tank management.

Regional Analysis

North America

North America held a leading position in the Fuel Storage Tank Market and accounted for 31.6% share in 2024, driven by extensive oil and gas infrastructure, refinery expansions, and strong demand from power generation and industrial facilities. The United States dominates regional consumption due to strategic petroleum reserve capacity, terminal modernization programs, and investments in bulk fuel logistics. Canada supports market growth through upstream storage developments and energy production activities. Rising safety compliance standards, asset replacement initiatives, and technological adoption in monitoring and corrosion-resistant tank systems further strengthen market demand across industrial, commercial, and transportation fueling environments.

Europe

Europe accounted for 23.8% share in 2024, supported by regulatory-driven upgrades, environmental compliance initiatives, and modernization of legacy fuel storage infrastructure across industrial and transportation sectors. The region experiences strong demand from aviation fuel storage hubs, maritime fuel terminals, and district energy facilities. Western Europe leads adoption of advanced composite and double-wall tank systems, while Central and Eastern Europe invest in storage expansion linked to energy transition, backup fuel security, and industrial resilience. Increasing reliance on strategic fuel reserves and enhanced monitoring technologies reinforces sustained investments in safe, efficient, and regulation-compliant storage tank solutions across key markets.

Asia-Pacific

Asia-Pacific emerged as the fastest-growing regional market and accounted for 28.9% share in 2024, fueled by rapid industrialization, refinery expansion, and rising demand for storage infrastructure in China, India, and Southeast Asia. Large-scale investments in petrochemical projects, transport fuel networks, and power generation facilities accelerate deployment of aboveground and modular storage systems. Expanding aviation hubs, logistics corridors, and mining operations further strengthen demand for mobile and bulk storage tanks. Government programs supporting energy security, infrastructure upgrades, and capacity expansion initiatives continue to drive sustained market growth across upstream, midstream, and downstream fuel storage applications in the region.

Middle East & Africa

The Middle East & Africa region accounted for 10.7% share in 2024, driven by major crude storage hubs, refinery and petrochemical projects, and expansion of export-oriented fuel terminals. Gulf Cooperation Council countries invest heavily in strategic storage capacity, tank farm development, and terminal automation to support international energy trade flows. Africa contributes through rising demand from mining, power generation, and industrial infrastructure projects requiring onsite and backup fuel storage systems. Increasing emphasis on asset integrity, corrosion control, and environmental safety strengthens the adoption of engineered steel and composite tank solutions across key oil-producing and industrial economies.

Latin America

Latin America accounted for 5.0% share in 2024, supported by ongoing refinery modernization, offshore oil production activities, and expansion of transportation and aviation fueling infrastructure across Brazil, Mexico, and emerging regional markets. Investments in bulk fuel storage terminals, industrial energy facilities, and mining operations generate consistent demand for aboveground and mobile storage tanks. Government initiatives to enhance energy security and logistics efficiency drive new tank installations and capacity upgrades. Increasing adoption of regulatory-compliant storage systems, leak-prevention technologies, and lifecycle-focused maintenance solutions further strengthens market opportunities across commercial, industrial, and fuel distribution environments in the region.

Fuel Storage Tank Market Segmentations:

By Product Type

- Aboveground Storage Tanks (AST)

- Underground Storage Tanks (UST)

- Portable & Mobile Fuel Tanks

By Material

- Steel Fuel Storage Tanks

- Fiberglass-Reinforced Plastic (FRP) Tanks

- Concrete & Composite Fuel Tanks

By Application

- Oil & Gas Industry (Upstream, Midstream, Downstream)

- Power Generation & Industrial Facilities

- Transportation, Aviation & Commercial Fueling Stations

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Fuel Storage Tank Market features leading players such as CST Industries, McDermott International, PermianLide, Superior Tank Co., Containment Solutions Inc., DN Tanks, Balmoral Tanks, Western Global, TI Fluid Systems, and Plastic Omnium Group in the first line, reflecting a diversified mix of global industrial tank manufacturers and specialized storage solution providers. The market remains moderately consolidated, with players focusing on engineering strength, material innovation, corrosion-resistant designs, and regulatory-compliant storage technologies. Companies invest in capacity expansion, modular tank systems, and double-wall containment structures to address safety, durability, and environmental performance requirements across oil and gas, industrial, aviation, and logistics sectors. Strategic initiatives include mergers, terminal modernization partnerships, and product upgrades integrating smart monitoring, leak detection, and lifecycle-maintenance capabilities. Growing emphasis on asset integrity management and sustainability drives competition in FRP, composite, and hybrid steel tank solutions, while regional players enhance aftermarket services, installation support, and turnkey storage infrastructure offerings to strengthen market positioning.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- CST Industries, Inc.

- McDermott International, Inc.

- PermianLide

- Superior Tank Co., Inc.

- Containment Solutions Inc.

- DN Tanks

- Balmoral Tanks Ltd

- Western Global

- TI Fluid Systems plc

- Plastic Omnium Group

Recent Developments

- In February 2024, CST Industries, Inc. completed the acquisition of Ostsee Tank Solutions, enhancing its global storage tank and aluminum dome solutions portfolio.

- In May 2025, Bilfinger acquired UK-based nZero Group, including subsidiaries Orbital Gas Systems and Thyson Technology, to enhance its capabilities in advanced energy systems and gas technologies for fuel storage applications.

- In May 2025, TF Warren Group acquired Krueger Engineering and Manufacturing (KEMCO), a manufacturer of shell and tube heat exchangers, strengthening its position in storage tank-related markets for petrochemical and refining sectors.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Material, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will experience steady growth as governments and industries continue investing in storage infrastructure for fuel security and supply reliability.

- Manufacturers will focus on durable materials, corrosion-resistant designs, and lifecycle-optimized tank systems to improve safety and performance.

- The adoption of smart monitoring, automation, and remote inspection technologies will increase across industrial and commercial storage facilities.

- Replacement of aging storage assets and modernization of legacy tank farms will remain a major growth driver across developed and emerging markets.

- Demand from aviation, logistics, mining, and remote industrial applications will expand the use of mobile and modular fuel storage solutions.

- Environmental regulations and emission-control standards will accelerate adoption of double-wall, leak-proof, and secondary containment tank systems.

- Storage tank manufacturers will strengthen partnerships with EPC contractors and terminal operators to deliver turnkey infrastructure solutions.

- Emerging economies will invest in new refinery storage, distribution terminals, and reserve capacity to support industrialization and energy trade.

- Hybrid and composite tank materials will gain traction as industries prioritize durability, weight reduction, and maintenance efficiency.

- Aftermarket services, inspection programs, and asset-lifecycle management solutions will play a larger role in market competitiveness and customer value.