Market Overview

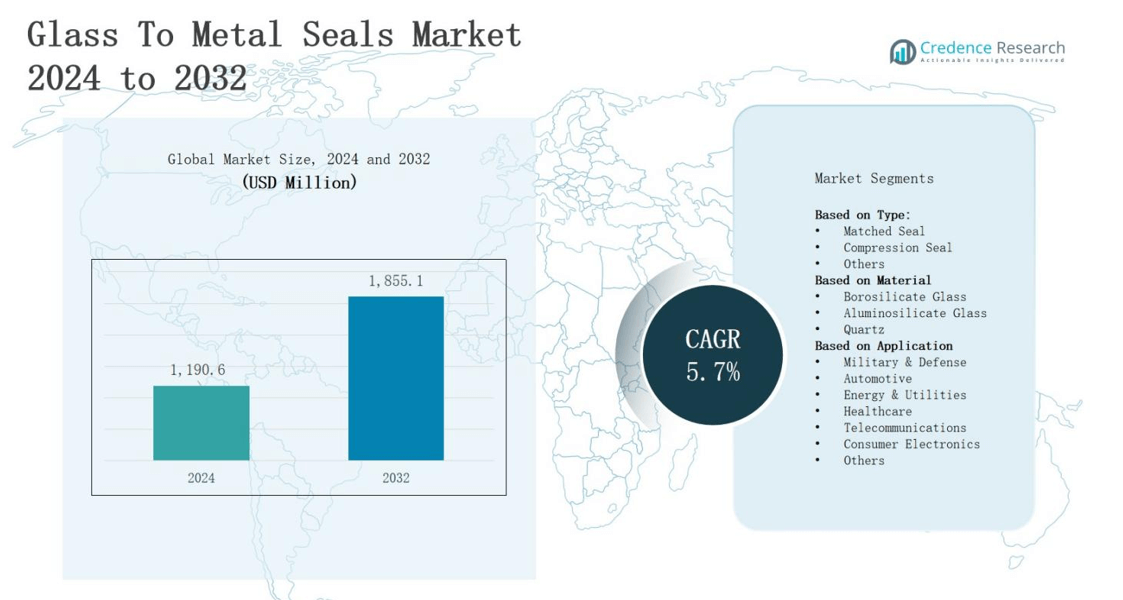

The glass to metal seals market is projected to grow from USD 1,190.6 million in 2024 to USD 1,855.1 million by 2032, registering a CAGR of 5.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Glass To Metal Seals Market Size 2024 |

USD 1,190.6 million |

| Glass To Metal Seals Market, CAGR |

5.7% |

| Glass To Metal Seals Market Size 2032 |

USD 1,855.1 million |

Market growth in the glass to metal seals sector is driven by rising demand for hermetic sealing solutions in electronics, aerospace, automotive, and defense applications, where reliability and durability are critical. Increasing adoption in medical devices, semiconductor packaging, and optoelectronic components is boosting demand, supported by advancements in material engineering for enhanced thermal and mechanical performance. Trends include the development of miniaturized and high-strength seals for compact electronic devices, growing use in electric vehicles for battery and sensor protection, and the integration of advanced manufacturing techniques to improve precision, efficiency, and cost-effectiveness in large-scale production.

The glass to metal seals market spans North America, Europe, Asia-Pacific, and the Rest of the World, each contributing distinct strengths. North America leads with strong aerospace, defense, and medical sectors, while Europe benefits from advanced automotive, renewable energy, and precision engineering industries. Asia-Pacific drives growth through large-scale electronics, automotive, and semiconductor manufacturing. The Rest of the World sees demand from energy, defense, and healthcare projects. Key players include AMETEK Inc., Kyocera, Egide Group, Amkor Technology Inc., Emerson Fusite, Hermetic Solutions Group LLC, and Rosenberger Hochfrequenztechnik GmbH & Co. KG.

Market Insights

- The glass to metal seals market is projected to grow from USD 1,190.6 million in 2024 to USD 1,855.1 million by 2032, at a CAGR of 5.7%, driven by its critical role in ensuring hermetic sealing in demanding applications.

- Rising demand from aerospace, defense, and automotive sectors is fueled by its ability to withstand extreme temperatures, pressure variations, and vibration while ensuring long-term reliability.

- Expanding use in electronics and semiconductor packaging supports device longevity, operational efficiency, and protection against contaminants in high-performance applications.

- Healthcare adoption is increasing due to its biocompatibility, durability under sterilization, and reliability in medical implants, diagnostic tools, and life-support systems.

- Advancements in material science and manufacturing techniques enhance strength, corrosion resistance, and thermal compatibility, enabling customization for specialized industrial requirements.

- Challenges include high manufacturing costs, material compatibility issues in extreme environments, and limited standardization across industries, which can delay large-scale deployment.

- Regional shares stand at North America 32%, Europe 27%, Asia-Pacific 29%, and Rest of the World 12%, with key players including AMETEK Inc., Kyocera, Egide Group, Amkor Technology Inc., Emerson Fusite, Hermetic Solutions Group LLC, and Rosenberger Hochfrequenztechnik GmbH & Co. KG.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand in Aerospace, Defense, and Automotive Applications

The glass to metal seals market experiences significant growth due to its critical role in ensuring hermetic sealing for aerospace, defense, and automotive components. It provides exceptional resistance to extreme temperatures, pressure variations, and vibration. Demand rises from applications in avionics, missile systems, and vehicle sensors requiring long-term reliability. It enables robust performance in harsh environments. The technology supports safety-critical systems, reducing risks of component failure. Its adoption strengthens compliance with stringent industry standards.

- For instance, SCHOTT’s glass-to-metal seals are widely used in automotive airbags and sensor connectors, ensuring long-term reliability in safety-critical systems.

Expanding Use in Electronics and Semiconductor Packaging

The glass to metal seals market benefits from rapid advancements in electronics and semiconductor packaging. It ensures airtight and moisture-resistant sealing for sensitive components such as transistors, diodes, and optoelectronic devices. This improves product lifespan and operational efficiency. Growing miniaturization trends in consumer electronics drive the need for precise and compact sealing solutions. It helps protect against performance degradation from contaminants. Its reliability attracts investment from high-tech manufacturing sectors. Demand is accelerating in telecom and data processing applications.

- For instance, Elan Technology employs glass ceramic composites with adjustable coefficients of thermal expansion for glass-to-metal hermetic seals used in semiconductor diodes and reed switches.

Growing Adoption in Medical Devices and Healthcare Technology

The glass to metal seals market gains momentum from the healthcare sector, where it ensures hermetic sealing for medical implants, diagnostic tools, and surgical instruments. It provides biocompatibility and durability under sterilization conditions. This enhances patient safety and device longevity. Expanding use in implantable sensors and life-support systems fuels market growth. It meets strict regulatory standards for medical applications. Increased healthcare infrastructure investment globally boosts demand. Technological improvements continue to expand its application potential in medical engineering.

Advancements in Material Science and Manufacturing Techniques

The glass to metal seals market sees expansion due to breakthroughs in material science and precision manufacturing. It now offers higher strength, improved thermal expansion compatibility, and better corrosion resistance. Advanced techniques enhance production efficiency and quality consistency. Manufacturers focus on cost optimization while maintaining performance integrity. It enables customization for specialized applications across industries. Continuous R&D investment drives innovation in sealing materials. Enhanced design flexibility supports integration into emerging high-performance and safety-critical technologies.

Market Trends

Increasing Demand for Miniaturized and High-Precision Seals

The glass to metal seals market is witnessing a strong shift toward miniaturized and high-precision components driven by the growth of compact electronics, medical implants, and aerospace instruments. It supports the production of smaller yet more reliable devices by ensuring consistent hermetic sealing. Manufacturers are refining tolerances to meet advanced design requirements. Demand from IoT devices and micro-sensors further accelerates this trend. It strengthens component protection against environmental stress. The push for lightweight designs amplifies market opportunities.

- For instance, KYOCERA’s glass-hermetic feedthrough connectors are compact, high-density, and operate at RF frequencies up to 110 GHz, enabling small, high-speed optical and communications modules.

Integration into Electric Vehicle and Battery Technologies

The glass to metal seals market benefits from the expanding electric vehicle sector, where it plays a key role in battery safety, sensor protection, and electronic control units. It enables stable performance under fluctuating temperatures and electrical loads. Adoption grows as automakers enhance EV range and safety. The technology supports high-voltage insulation needs in advanced battery packs. It prevents moisture and gas ingress that can compromise performance. The EV industry’s rapid growth sustains this long-term demand trend.

Advances in Material Engineering and Coating Technologies

The glass to metal seals market is experiencing significant advancements in material engineering, with improved alloys and glass compositions enhancing thermal compatibility and corrosion resistance. It benefits from specialized coatings that increase seal longevity and performance in aggressive environments. Industries such as defense and oil & gas adopt these innovations to meet demanding operational requirements. It reduces maintenance needs while improving system reliability. This trend aligns with the global focus on high-performance and durable sealing solutions.

- For instance, Hermetic Seal Technology uses high-quality metals such as 52 alloy, stainless steel, and Inconel combined with proprietary glass formulations, employing advanced techniques like glass smelting and resistance welding to ensure hermetic seals that withstand harsh environments, meeting stringent military standards.

Adoption of Automated and High-Throughput Manufacturing Processes

The glass to metal seals market is embracing automated production lines and high-throughput manufacturing techniques to improve efficiency and precision. It allows faster turnaround times without compromising quality. Robotics and CNC machining enhance repeatability, supporting large-scale, complex designs. Adoption is rising in sectors where rapid prototyping and customization are essential. It ensures competitive pricing while meeting diverse industry specifications. This shift supports consistent growth in both established and emerging application areas worldwide.

Market Challenges Analysis

High Manufacturing Costs and Complex Production Requirements

The glass to metal seals market faces constraints from high manufacturing costs driven by precision engineering demands, advanced materials, and stringent quality controls. It requires specialized equipment and skilled labor, which increases operational expenses. Small and medium-scale manufacturers often struggle to compete with large players capable of achieving economies of scale. Limited access to advanced raw materials further intensifies cost pressures. It also demands strict process monitoring to maintain consistent sealing performance. Price sensitivity in certain application sectors can hinder wider adoption.

Material Compatibility and Performance Limitations in Extreme Environments

The glass to metal seals market encounters challenges related to matching thermal expansion properties between glass and metal under extreme operational conditions. It is susceptible to performance degradation if exposed to rapid temperature fluctuations or aggressive chemical environments. Certain applications, such as deep-sea exploration and space technology, require specialized variants that are costly and difficult to produce. It demands extensive testing to ensure reliability in harsh environments. Limited standardization across industries complicates large-scale deployment. These factors can delay adoption in emerging high-performance markets.

Market Opportunities

Expanding Applications in Renewable Energy and Electric Mobility

The glass to metal seals market is positioned to benefit from the rapid expansion of renewable energy systems and electric mobility solutions. It provides critical sealing for high-voltage connectors, sensors, and control units in solar, wind, and electric vehicle applications. Growing investment in battery technology and energy storage infrastructure fuels demand for advanced sealing solutions. It supports operational reliability in challenging environmental conditions. The shift toward cleaner energy solutions creates sustained growth potential. Manufacturers can capitalize by developing customized, high-durability products for these sectors.

Growth Potential in Medical Technology and Advanced Electronics

The glass to metal seals market offers significant opportunities within medical technology and advanced electronics manufacturing. It ensures hermetic sealing for life-critical devices such as pacemakers, defibrillators, and diagnostic instruments. Rising demand for miniaturized, high-performance electronic components drives adoption in semiconductor and optoelectronic applications. It enhances device longevity and operational efficiency by preventing contamination and degradation. Increasing healthcare investments worldwide expand the addressable market. Manufacturers focusing on precision engineering and biocompatible materials can gain a competitive edge in these high-value segments.

Market Segmentation Analysis:

By Type

The glass to metal seals market is segmented into matched seals, compression seals, and others. Matched seals hold a significant share due to their precise thermal expansion compatibility, ensuring high reliability in aerospace, defense, and medical applications. Compression seals are widely used in high-pressure and harsh environmental conditions, particularly in energy and automotive sectors. It offers strong mechanical bonding and cost-effective production. The “others” category includes specialized designs for niche applications requiring customized performance specifications.

- For instance, Schott AG pioneers the use of glass-ceramic to metal seals for high-temperature applications in solid oxide fuel cells (SOFCs), where their seals maintain structural integrity and thermal resistance in energy sector components.

By Material

The market is categorized into borosilicate glass, aluminosilicate glass, and quartz. Borosilicate glass dominates due to its thermal resistance and chemical stability, making it suitable for electronics and industrial equipment. Aluminosilicate glass is preferred in high-strength applications such as defense and heavy machinery. Quartz serves in high-frequency and precision devices in telecommunications and scientific instruments. It provides excellent optical clarity and durability under extreme conditions. Material choice depends on performance requirements and environmental exposure.

- For example, quartz is favored in scientific instruments like UV cuvettes and tube furnace liners where high melting point and optical properties are critical.

By Application

The market covers military and defense, automotive, energy and utilities, healthcare, telecommunications, consumer electronics, and others. Military and defense applications lead due to strict reliability standards and demand for long-lasting hermetic seals. Automotive and energy sectors show rising adoption driven by electric vehicle growth and renewable energy projects. Healthcare applications leverage it for critical medical devices. Telecommunications and consumer electronics benefit from its protective capabilities in miniaturized, high-performance devices. Emerging uses in industrial automation expand its market potential.

Segments:

Based on Type:

- Matched Seal

- Compression Seal

- Others

Based on Material

- Borosilicate Glass

- Aluminosilicate Glass

- Quartz

Based on Application

- Military & Defense

- Automotive

- Energy & Utilities

- Healthcare

- Telecommunications

- Consumer Electronics

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds 32% share of the glass to metal seals market, driven by strong demand in aerospace, defense, and advanced electronics manufacturing. It benefits from a well-established industrial base and high adoption of hermetic sealing technologies in military equipment, telecommunications, and medical devices. The region’s automotive industry increasingly integrates these seals into electric and hybrid vehicles. It also gains from ongoing investment in renewable energy projects. Regulatory standards emphasizing quality and durability sustain demand. Leading manufacturers leverage R&D facilities in the United States and Canada to develop specialized sealing solutions.

Europe

Europe accounts for 27% of the glass to metal seals market, supported by a robust automotive sector, high defense spending, and advanced industrial capabilities. It has a strong presence in precision engineering for medical devices and aerospace applications. Demand is fueled by the shift toward electric mobility and renewable energy infrastructure. The region’s manufacturing excellence enables production of high-reliability seals meeting stringent environmental standards. Investments in smart grid and energy storage projects increase adoption. Germany, France, and the United Kingdom lead innovation in material engineering and seal design.

Asia-Pacific

Asia-Pacific holds 29% share of the glass to metal seals market, driven by rapid industrialization, expanding electronics production, and growing defense programs. It benefits from large-scale semiconductor manufacturing in China, Japan, South Korea, and Taiwan. The automotive sector, particularly electric vehicle production, fuels strong demand for hermetic seals. It also gains from expanding healthcare technology manufacturing in emerging economies. Government-backed infrastructure and energy projects contribute to growth. Regional suppliers compete on both cost efficiency and advanced product features.

Rest of the World

The Rest of the World holds 12% share of the glass to metal seals market, with demand arising from Latin America, the Middle East, and Africa. It sees increasing adoption in oil and gas, power generation, and defense applications. Emerging healthcare infrastructure creates opportunities for medical device integration. It also benefits from renewable energy development in regions investing in solar and wind projects. Limited local manufacturing capacity drives reliance on imports from established producers. Strategic partnerships are expanding to meet sector-specific needs.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Concept Group LLC

- Egide Group

- Emerson Fusite (Emerson Electric Co)

- Hermetic Solutions Group LLC

- Amkor Technology Inc.

- Rosenberger Hochfrequenztechnik GmbH & Co. KG

- Complete Hermetics

- Kyocera

- Dietze Group

- Botou Hi-Tech Electronic Accessories Co. LTD

- AMETEK Inc.

- Electrovac AG

- Palomar Technologies

Competitive Analysis

The glass to metal seals market is characterized by intense competition among global and regional players focusing on innovation, quality, and application-specific solutions. It demands precision engineering and advanced material science capabilities to meet stringent performance standards in aerospace, defense, automotive, medical, and electronics sectors. Leading companies such as AMETEK Inc., Amkor Technology Inc., Botou Hi-Tech Electronic Accessories Co. LTD, Complete Hermetics, Concept Group LLC, Dietze Group, Egide Group, Electrovac AG, Emerson Fusite (Emerson Electric Co), Hermetic Solutions Group LLC, Kyocera, Palomar Technologies, and Rosenberger Hochfrequenztechnik GmbH & Co. KG compete by expanding product portfolios, optimizing manufacturing efficiency, and forming strategic partnerships. It relies on consistent R&D investment to enhance thermal compatibility, corrosion resistance, and miniaturization capabilities. Players differentiate through customization, global supply networks, and compliance with industry-specific regulations. Competitive dynamics are further shaped by the growing demand for seals in emerging sectors such as electric vehicles, renewable energy, and advanced telecommunications.

Recent Developments

- In October 2023, Electro Ceramic Industries completed the acquisition of United Glass to Metal Sealing, Inc., strengthening its portfolio in advanced feedthrough technologies and hermetic headers.

- In May 2025, Electro Ceramic Industries (ECI) expanded its glass-to-metal product line through the acquisition of United Glass to Metal Sealing, Inc., enhancing manufacturing efficiency and adding custom products such as 50-Ohm coaxial feedthroughs for aerospace and defense applications.

- In 2024–2025, Schott AG introduced new hermetic products and its ground-breaking HEATAN technology, expanding its product line in the glass-to-metal seals market.

- In 2023, TE Connectivity introduced a new line of miniaturized glass‑to‑metal seals tailored for medical applications, expanding its footprint in the healthcare sector.

Market Concentration & Characteristics

The glass to metal seals market exhibits a moderate to high level of concentration, with a mix of global leaders and specialized regional players competing on technology, quality, and customization. It is characterized by high entry barriers due to the need for precision engineering, advanced material science expertise, and compliance with stringent industry standards. Established companies leverage strong R&D capabilities, global supply chains, and long-standing relationships with defense, aerospace, automotive, medical, and electronics sectors. It demands consistent innovation to meet evolving requirements for miniaturization, durability, and thermal compatibility. The market’s competitive dynamics are shaped by technological advancements, long qualification cycles for critical applications, and customer preference for proven reliability. Strategic collaborations, product diversification, and regional manufacturing presence strengthen market positioning. It benefits from stable demand across multiple high-value industries, making sustained technological leadership and operational efficiency essential for long-term competitiveness.

Report Coverage

The research report offers an in-depth analysis based on Type, Material, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will rise in aerospace and defense due to increased investment in high-reliability sealing solutions.

- Adoption in electric vehicles will grow with the need for battery safety and sensor protection.

- Medical device integration will expand as healthcare technology advances globally.

- Miniaturized sealing solutions will see higher demand in consumer electronics and IoT devices.

- Renewable energy projects will create new opportunities in high-voltage and environmental protection applications.

- Material innovations will improve thermal compatibility and corrosion resistance in harsh environments.

- Automated manufacturing will enhance production efficiency and consistency in large-scale orders.

- Strategic partnerships between manufacturers and OEMs will strengthen supply chain resilience.

- Emerging markets will contribute more through industrialization and infrastructure development.

- Regulatory compliance will drive adoption of advanced sealing technologies in safety-critical applications.