Market Overview:

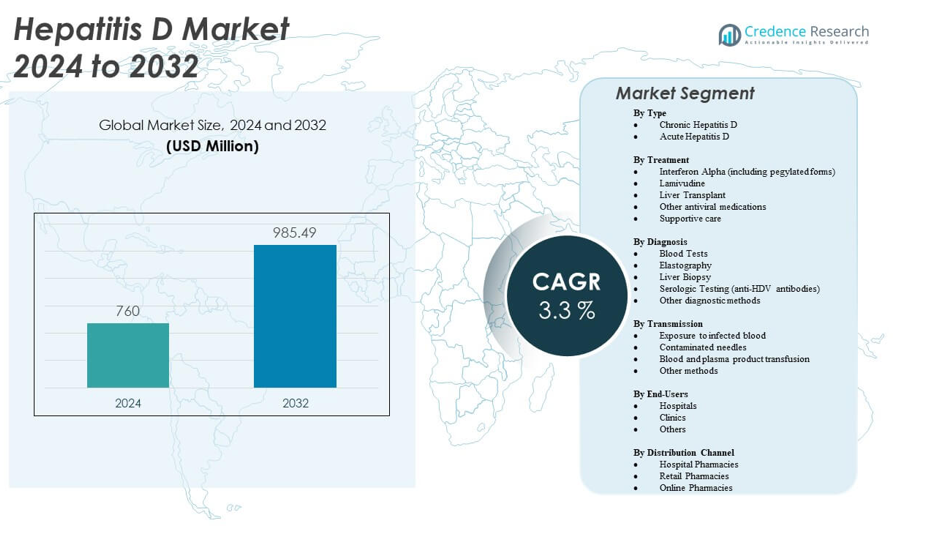

The Hepatitis D Market is projected to grow from USD 760 million in 2024 to an estimated USD 985.49 million by 2032, with a compound annual growth rate (CAGR) of 3.3% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hepatitis D Market Size 2024 |

USD 760 million |

| Hepatitis D Market, CAGR |

3.3% |

| Hepatitis D Market Size 2032 |

USD 985.49 million |

The Hepatitis D Market is driven by the increasing prevalence of Hepatitis B virus (HBV) co-infection, as HDV relies on HBV for replication. Rising awareness of Hepatitis D, improved diagnostic techniques, and advancements in antiviral therapies contribute to the market’s growth. Government initiatives focused on HBV/HDV screening and prevention further propel demand for HDV treatment options, expanding the market potential globally.

North America currently leads the Hepatitis D Market due to its advanced healthcare infrastructure, robust diagnostic capabilities, and high rates of treatment adoption. Europe follows closely, with countries like Germany and the U.K. leading in screening programs. The Asia-Pacific region is emerging as a key growth area, driven by a large HBV carrier population and expanding healthcare access in nations like China and India. These regions show growing awareness and improved diagnostic networks, making them vital for the market’s future expansion.

Market Insights:

- The Hepatitis D Market is projected to grow from USD 760 million in 2024 to an estimated USD 985.49 million by 2032, with a CAGR of 3.3%.

- Increasing prevalence of Hepatitis B co-infection, which drives the demand for Hepatitis D treatments.

- Advancements in diagnostic methods, such as PCR-based tests, have improved early detection, fueling market growth.

- The lack of effective universal treatment options for Hepatitis D continues to limit market expansion.

- Rising awareness campaigns and government initiatives to tackle Hepatitis B/HDV co-infections will support market growth.

- North America leads the market due to strong healthcare infrastructure, with emerging opportunities in Asia-Pacific and Latin America.

- Expanding access to healthcare in regions with high HBV carrier populations will drive market adoption in developing nations.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Increasing Prevalence of Hepatitis B Infection

The Hepatitis D market is significantly driven by the rising prevalence of Hepatitis B virus (HBV) infection, which is a necessary condition for HDV infection. As the primary co-factor for the development of Hepatitis D, the ongoing global burden of HBV increases the risk of Hepatitis D transmission. Countries with high HBV infection rates, particularly in Asia-Pacific and Sub-Saharan Africa, have a larger pool of individuals susceptible to HDV. The efforts in reducing HBV infections indirectly fuel the demand for Hepatitis D diagnostics and treatments, highlighting the direct link between these two viral infections.

- For instance, China’s national HBV vaccination program has resulted in a drastic reduction in HBV prevalence among children under five years old, from 9.67% in 1992 to 0.30% in 2020, according to national survey data summarized in a January 2025 report.

Advancements in Diagnostic Methods

The market benefits from advancements in diagnostic methods for Hepatitis D, which contribute to its early detection. Newer diagnostic technologies, such as advanced PCR-based tests and RNA-based tests, have improved the sensitivity and specificity of HDV detection. These improvements help healthcare providers identify the virus more accurately, even in its early stages, facilitating timely interventions. This shift towards more reliable and efficient testing methods has driven the demand for Hepatitis D diagnostic kits, spurring growth in the market.

- For example, Roche Diagnostics offers the LightMix® Kit Hepatitis D Virus (HDV), which detects HDV genotype 1 from cDNA. It delivers highly specific results by amplifying a 113 bp fragment of the HDV delta antigen gene, providing precise diagnostic capabilities for HDV detection.

Therapeutic Advancements and Drug Development

Hepatitis D treatment options have expanded due to advancements in drug development, significantly impacting the market. The availability of antiviral therapies targeting both HBV and HDV has increased the treatment options available to patients. For instance, the introduction of interferon-free therapies and antiviral drugs designed specifically for HDV has led to more effective treatment regimens. Pharmaceutical companies’ ongoing research efforts to develop more effective and less toxic therapies continue to shape the market, with a growing pipeline of promising drugs.

Government Initiatives and Healthcare Funding

Government policies and healthcare funding play a crucial role in driving the growth of the Hepatitis D market. Increased public health funding has enabled governments to implement widespread HBV and Hepatitis D screening programs. These initiatives, particularly in endemic regions, are aimed at reducing the transmission rates of both diseases and improving treatment access. As the awareness of Hepatitis D grows, governments are allocating more resources towards preventing and treating viral hepatitis, ultimately boosting market growth.

Market Trends:

Integration of Telemedicine in Hepatitis D Management

Telemedicine has emerged as a growing trend in the Hepatitis D market, offering patients more accessible treatment options. The increased use of telehealth services enables patients, especially in rural and underserved areas, to consult specialists and access diagnostic tests remotely. This trend has become more pronounced due to the COVID-19 pandemic, which accelerated the adoption of digital health technologies. It has particularly benefitted patients with chronic conditions like Hepatitis D, who need regular monitoring and consultations but may not have easy access to healthcare facilities.

- For example, Amwell documented over 1.8 million telehealth visits in Q1 2022, showcasing the growing adoption of telemedicine. During the COVID-19 pandemic, video visits became essential, with significant utilization in chronic liver disease management, including hepatitis patients, in large academic hepatology clinics.

Shift Towards Personalized Medicine

There is a growing trend towards personalized medicine in the treatment of Hepatitis D, focusing on tailoring treatment plans based on individual genetic profiles. Personalized approaches help in identifying the most effective therapies for patients, improving treatment outcomes and minimizing adverse effects. This trend is driven by the increasing availability of genomic testing and the understanding of how genetics influence the response to antiviral drugs. Hepatitis D treatment regimens are becoming more customized, leading to improved patient care and outcomes in the long run.

Rise in Vaccine Development for Hepatitis D

Vaccine development for Hepatitis D is a prominent trend shaping the future of the market. Several pharmaceutical companies are working on developing vaccines that not only prevent HBV but also offer protection against Hepatitis D. The global efforts to combat viral hepatitis have shifted towards integrating Hepatitis D into the larger Hepatitis B vaccination programs. These vaccines, once developed, could reduce the incidence of HDV infections significantly, presenting a potential game-changer for the Hepatitis D market by reducing the overall burden of the disease.

- For example, VBI Vaccines, in collaboration with Brii Biosciences, conducted an interim analysis of its Phase 2 trial for BRII-179 (VBI-2601), an HBV immunotherapeutic candidate. The study showed promising immune responses, with enhanced antibody and T-cell activity in patients with chronic HBV infection.

Increased Collaborations and Partnerships in Research

Collaborations between pharmaceutical companies, research institutions, and government agencies are driving innovation in the Hepatitis D market. Partnerships focused on finding new therapeutic options, improving diagnostic techniques, and enhancing prevention strategies are gaining momentum. These collaborations allow for the pooling of resources, knowledge, and expertise, leading to faster advancements in Hepatitis D treatment. The collective efforts of these organizations are accelerating the development of novel therapies and vaccines, which are crucial for the market’s future growth.

Market Challenges Analysis:

Limited Treatment Options and Drug Resistance

One of the main challenges in the Hepatitis D market is the limited availability of effective treatment options. While antiviral therapies have improved, there is still a lack of universal, long-term treatments for Hepatitis D. Many patients experience poor responses to existing therapies, and drug resistance can develop over time, making treatment management more difficult. This challenge results in ongoing efforts to develop new, more effective therapies, but the market remains constrained by these limitations.

High Treatment Costs and Accessibility Issues

High treatment costs pose a significant challenge for the Hepatitis D market, particularly in low- and middle-income countries. The cost of newer antiviral drugs and diagnostic tests is often prohibitive for many patients, limiting their access to care. Healthcare systems in these regions may struggle to allocate the necessary funds to provide widespread access to treatments and screening programs. This issue results in an inequitable distribution of resources and hinders the overall effectiveness of global efforts to combat Hepatitis D.

Market Opportunities:

Growth Potential in Emerging Markets

The Hepatitis D market presents significant growth opportunities in emerging markets, especially in regions with high HBV prevalence. Countries in Asia-Pacific, Africa, and Latin America represent untapped markets for Hepatitis D diagnostics and treatments. These regions have large populations affected by HBV, making them prime candidates for expanded Hepatitis D screening and treatment programs. As healthcare infrastructure improves and awareness of Hepatitis D increases, these markets are expected to witness substantial growth.

Focus on Research and Development of Novel Therapies

There is a growing opportunity in the market for companies to invest in research and development of novel therapies for Hepatitis D. The lack of a comprehensive treatment option creates a high demand for innovative antiviral drugs and vaccines. Companies investing in this space have the potential to develop breakthrough treatments that could dominate the market. Continued R&D efforts, coupled with increasing governmental and institutional support, present a strong opportunity for companies to establish leadership in this niche yet crucial market.

Market Segmentation Analysis:

By Type

The Hepatitis D Market is primarily divided into Chronic and Acute Hepatitis D. Chronic Hepatitis D holds the largest market share due to its higher prevalence and ongoing need for management. This type of infection leads to long-term complications, such as liver cirrhosis and hepatocellular carcinoma, which demand continuous monitoring and treatment. Acute Hepatitis D, on the other hand, is less common and typically results in severe illness but is manageable with prompt intervention. The distinct treatment and management requirements of both types drive separate segments within the market.

- For instance, Gilead Sciences published in May 2025 the final data from the Phase 3 MYR301 study of bulevirtide (Hepcludex) for chronic Hepatitis D, confirming that 36% of patients achieved virological suppression (HDV RNA undetectable) after 48 weeks, with durable off-treatment efficacy at 72 weeks.

By Treatment

In the Hepatitis D Market, the primary treatments include Interferon Alpha (including pegylated forms), Lamivudine, liver transplant, other antiviral medications, and supportive care. Interferon Alpha remains the main FDA-approved therapy, with its usage aimed at suppressing HDV replication. Lamivudine and other antiviral drugs contribute to managing the disease by targeting viral replication processes. Liver transplants are increasingly needed due to the progression of liver damage in chronic cases. Supportive care remains essential to managing symptoms and improving quality of life.

By Diagnosis

Diagnosis in the Hepatitis D Market relies on methods such as blood tests, elastography, liver biopsy, serologic testing (anti-HDV antibodies), and other diagnostic techniques. Blood tests and serologic testing are the primary tools for early and accurate detection, while elastography and liver biopsy help assess the extent of liver damage. These diagnostic methods enable clinicians to effectively monitor HDV infection progression and guide treatment plans.

- For example, The Abbott ARCHITECT Anti-HDV IgM/IgG assay, used globally in clinical settings, offers high specificity (99.5%) for serologic HDV antibody detection. It is capable of large-scale, automated throughput on the ARCHITECT platform, providing efficient, high-volume diagnostics for Hepatitis D.

By Transmission

Hepatitis D is predominantly transmitted through exposure to infected blood, contaminated needles, blood, and plasma product transfusions. The main mode of transmission remains direct blood exposure, which is common among intravenous drug users and in healthcare settings with insufficient safety measures. Awareness and prevention measures, such as needle exchange programs and safe blood transfusion practices, remain key factors in controlling transmission.

By End-Users

Hospitals are the primary end-users in the Hepatitis D Market, given their advanced diagnostic and treatment capabilities. Clinics also play a significant role, offering more accessible care options for routine management and monitoring. Other end-users include specialized care centers and research institutions that contribute to diagnosis, treatment, and the development of new therapeutic options.

By Distribution Channel

The distribution channels in the Hepatitis D Market include hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies are the most prevalent distribution point due to their direct connection with patient care and treatment regimens. Retail pharmacies offer convenience for patients requiring regular medication refills. The rise of online pharmacies has further expanded access, allowing patients to conveniently order medications from home.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Segmentation:

By Type

- Chronic Hepatitis D

- Acute Hepatitis D

By Treatment

- Interferon Alpha (including pegylated forms)

- Lamivudine

- Liver Transplant

- Other antiviral medications

- Supportive care

By Diagnosis

- Blood Tests

- Elastography

- Liver Biopsy

- Serologic Testing (anti‑HDV antibodies)

- Other diagnostic methods

By Transmission

- Exposure to infected blood

- Contaminated needles

- Blood and plasma product transfusion

- Other methods

By End‑Users

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America dominates the Hepatitis D Market with a 26.8% share in 2024, thanks to strong healthcare infrastructure, high awareness of HBV/HDV co‑infections and early access to novel therapies. The U.S. market holds the bulk of this regional share, driven by proactive screening programs, specialised hepatology centres and reimbursement policies favouring HDV treatment. High healthcare spending and clinical trial activity reinforce North America’s position, enabling rapid adoption of diagnostics and interventions tailored to HDV.

Europe contributes approximately 24.7% of the market in 2024, supported by mature healthcare systems and increasing HBV/HDV co‑infection awareness. Countries such as Germany, the U.K., France and Italy lead in screening programmes, guidelines and therapeutic uptake. The presence of strong research networks, regional regulatory alignment and growing clinical activity in Eastern Europe further bolster Europe’s significance in the market landscape.

Asia‑Pacific accounts for roughly 22.3% of the market in 2024 and emerging nations within this region are gaining momentum due to a high prevalence of HBV, improving healthcare access and rising diagnostic capability. China, India and Mongolia particularly stand out for their disease burden and investment in public‑health efforts. While the regional share is lower than North America and Europe now, the growth rate prospects remain strong, positioning Asia‑Pacific as a critical growth front in the global market.

Key Player Analysis:

- Gilead Sciences, Inc.

- Eiger BioPharmaceuticals, Inc.

- Janssen Pharmaceuticals, Inc.

- Vir Biotechnology, Inc.

- Antios Therapeutics, Inc.

- PharmaEssentia Corporation

- Hepion Pharmaceuticals, Inc.

- BIOSIDUS S.A.

- Hoffmann-La Roche Ltd.

- Zydus Lifesciences

- Rhein-Minapharm

- PROBIOMED S.A. de C.V.

- 3SBio Group

- Apotex Corp.

- Viatris

Competitive Analysis:

The competitive landscape of the Hepatitis D Market features a blend of large pharmaceutical firms and biotech entrants advancing HDV‑specific therapies. Key players such as Gilead Sciences, Inc., GSK plc and Janssen Pharmaceuticals, Inc. lead with strategic pipelines targeting HDV viral replication, entry inhibition and RNA‑based approaches. Smaller firms and biotech companies complement the field by focusing on novel mechanisms, combination therapies and underserved geographies. It engages firms in partnerships, acquisitions and licensing deals to enhance their HDV portfolios. It contends with limited treatment options, high development cost and regulatory complexity, which yields opportunities for differentiation through innovation and geographic expansion. Firms with robust diagnostic‑to‑treatment capabilities gain competitive advantage in this evolving market.

Recent Developments:

- In September 2025, Bluejay Therapeutics enrolled the first patient in their global Phase 3 AZURE-2 trial assessing the antibody brelovitug for Hepatitis D treatment, marking a critical step in advancing this novel therapy in late-stage clinical development.

- In May 2025, Gilead Sciences, Inc. announced final results from its Phase 3 MYR301 study. The data showed that patients with chronic hepatitis D who received long‑term treatment with the entry‑inhibitor Bulevirtide sustained undetectable HDV RNA levels for nearly two years after stopping therapy.

Report Coverage:

The research report offers an in-depth analysis based on Type, Treatment, Diagnosis, Transmission, End Users and Distribution Channel. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Ongoing advancements in diagnostics will improve early detection, driving market growth.

- Continued innovation in antiviral therapies and personalized medicine will shape treatment paradigms.

- Governments’ increased focus on HBV and HDV co-infection awareness will drive screening programs.

- Growing demand for liver transplants will spur medical infrastructure investment and related services.

- Emerging economies will see increased market adoption as healthcare access improves.

- Expansion of telemedicine and remote healthcare solutions will increase patient access to care.

- Strategic collaborations between biopharmaceutical companies and research institutions will foster innovation.

- Increased funding for hepatitis research will accelerate drug discovery and clinical trials.

- The growing focus on sustainable and affordable treatment options will open new market opportunities.

- Public health initiatives targeting prevention and treatment will contribute to market expansion.