Market Overview

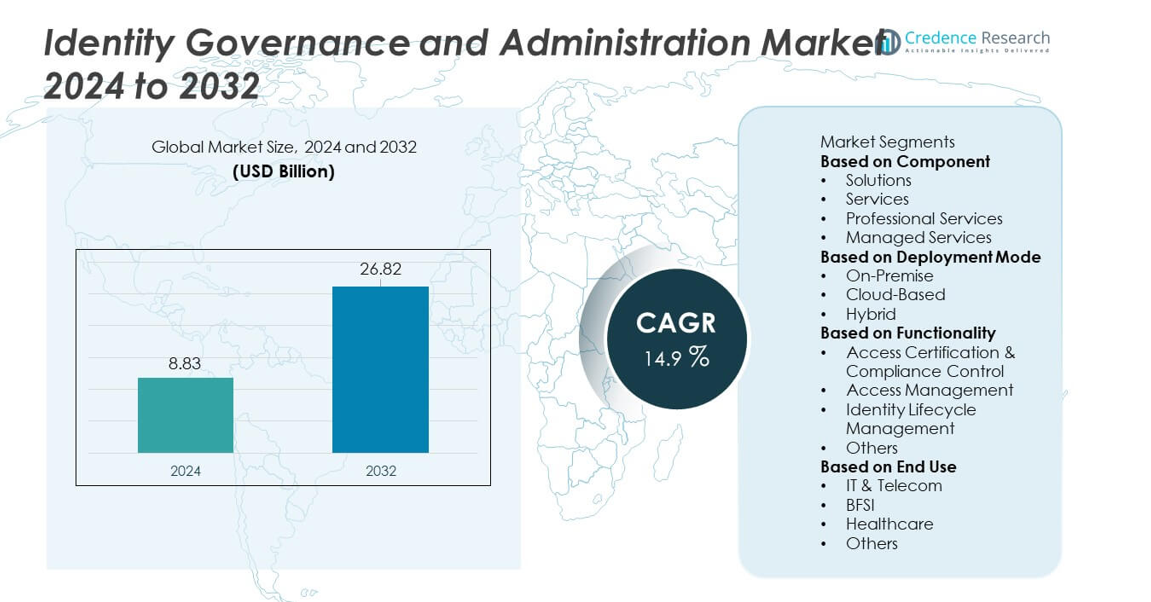

The Identity Governance and Administration (IGA) market reached USD 8.83 billion in 2024 and is projected to grow to USD 26.82 billion by 2032, registering a CAGR of 14.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Identity Governance and Administration Market Size 2024 |

USD 8.83 billion |

| Identity Governance and Administration Market, CAGR |

14.9% |

| Identity Governance and Administration Market Size 2032 |

USD 26.82 billion |

The Identity Governance and Administration market is shaped by leading players such as Microsoft Corporation, Okta, Inc., IBM Corporation, CyberArk Software Ltd., Imprivata, Inc., Oracle Corporation, Amazon Web Services, Inc., Micro Focus International plc, Evidian (Atos SE), and Broadcom Inc. (Symantec), all of which enhance market growth through advanced identity lifecycle tools, automated access governance, and AI-enabled risk analytics. These companies strengthen zero-trust adoption and expand cloud-native IGA capabilities to support hybrid and multi-cloud environments. North America leads the market with a 39% share, followed by Europe at 28%, driven by strict compliance requirements, while Asia Pacific holds a 23% share due to rapid digital transformation and rising cybersecurity investments.

Market Insights

- The Identity Governance and Administration market reached USD 8.83 billion in 2024 and will grow at a CAGR of 14.9% through 2032, supported by rising digitalization and identity security needs.

- Growing compliance pressure and stricter data protection laws drive strong demand for IGA solutions, with the solutions segment holding a 62% share due to high adoption of unified governance platforms.

- AI-enabled identity analytics, automated lifecycle workflows, and cloud-native governance tools shape major market trends as enterprises strengthen zero-trust and hybrid security models.

- Leading players, including Microsoft, IBM, Okta, CyberArk, and AWS, enhance competition through advanced integration capabilities, while high deployment complexity remains a key restraint for smaller organizations.

- Regionally, North America leads with a 39% share, Europe follows with 28%, and Asia Pacific holds 23%, driven by increasing cloud adoption and rising demand for identity risk management across regulated industries.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Component

Solutions lead the Identity Governance and Administration market with a 62% share, driven by growing enterprise demand for unified identity management, automated access provisioning, and real-time compliance monitoring. Organizations adopt advanced IGA solutions to manage rising identity volumes across cloud, mobile, and hybrid environments. Services, including both professional and managed services, continue to grow as enterprises seek support for deployment, integration, and policy optimization. Managed services gain attention for lowering operational burdens and delivering continuous monitoring. Increasing cybersecurity risks and stricter regulatory requirements further push organizations to adopt robust and scalable IGA platforms.

- For instance, Microsoft has introduced the Security Copilot Access Review Agent in Microsoft Entra ID (formerly Azure AD), which uses AI and machine learning to analyze user activity and provide data-driven recommendations to reviewers, thereby accelerating access reviews for large enterprises.

By Deployment Mode

Cloud-based deployment dominates with a 54% share, supported by rapid digital transformation and the shift toward SaaS-based identity management platforms. Enterprises choose cloud IGA for scalability, faster rollout, and lower infrastructure costs. Hybrid deployment gains traction among large organizations that balance on-premise security control with cloud flexibility. On-premise solutions remain relevant for highly regulated sectors needing strict data governance. Rising cloud workloads, remote work expansion, and demand for centralized identity oversight reinforce the dominance of cloud-based IGA deployments across global markets.

- For instance, Oracle Cloud Infrastructure (OCI) Identity and Access Management (IAM) provides enterprise-class identity and access management capabilities, including multifactor authentication (MFA) and single sign-on (SSO), for both Oracle and non-Oracle applications.

By Functionality

Identity lifecycle management leads the segment with a 47% share, driven by the need to automate onboarding, role assignments, privilege adjustments, and deprovisioning across diverse systems. Enterprises focus on reducing manual errors and improving security posture through continuous identity updates. Access management also records strong growth as organizations implement zero-trust models and multi-factor authentication. Access certification and compliance control expand due to tighter audit requirements and data governance mandates. Increasing identity complexity, multi-cloud adoption, and rising insider threats continue to support broad adoption across all IGA functionalities.

Key Growth Drivers

Rising Regulatory Compliance Requirements

Strict global regulations push enterprises to adopt strong Identity Governance and Administration solutions. Frameworks such as GDPR, HIPAA, SOX, and PCI-DSS require tight control over user access, audit readiness, and policy enforcement. Organizations deploy automated identity workflows to reduce compliance risks and maintain consistent privilege management across cloud and on-premise systems. Growing penalties for data misuse and unauthorized access increase adoption of centralized governance tools. As enterprises expand digital operations, regulatory pressure continues to act as a major catalyst for IGA deployment.

- For instance, the broader IBM X-Force threat intelligence team obtains its insights from monitoring over 150 billion security events per day across more than 130 countries.

Expansion of Cloud Adoption and Digital Transformation

Enterprises accelerate cloud migration and modernize IT systems, creating a surge in identity volumes across applications, devices, and hybrid environments. This expansion increases demand for identity lifecycle automation, role-based access models, and unified governance platforms. Cloud-based IGA solutions offer scalability and rapid deployment, supporting fast-growing digital operations. Organizations adopt zero-trust frameworks that require continuous identity validation and real-time access visibility. As multi-cloud ecosystems expand, IGA becomes essential for keeping identities secure, consistent, and compliant.

- For instance, Okta processes more than 19 billion monthly authentication requests across global clients, supporting high-growth cloud environments.

Increasing Cybersecurity Threats and Insider Risks

Rising cyberattacks and insider-driven breaches drive strong demand for automated access governance. Enterprises deploy IGA platforms to control privileged accounts, detect abnormal access behavior, and reduce manual provisioning errors. Identity misuse remains a major entry point for attackers, increasing the need for monitoring and policy-driven access decisions. Automated certification, role optimization, and continuous access reviews enhance security posture. As workforce mobility grows, organizations rely on IGA to ensure secure access across remote teams, third-party vendors, and distributed digital ecosystems.

Key Trends & Opportunities

Growing Integration of AI and Automation in Identity Governance

AI-driven analytics help organizations detect anomalies, optimize access roles, and automate certification workflows. Machine learning enhances identity risk scoring, enabling faster decisions and reducing manual oversight. Intelligent recommendations streamline privilege allocation and identify unnecessary access rights. Vendors invest in advanced automation that simplifies large-scale governance tasks and improves compliance reporting. This trend creates opportunities for predictive identity management and real-time threat response within IGA ecosystems.

- For instance, SailPoint Identity Security Cloud leverages AI and machine learning to provide access recommendations and automate governance processes, helping organizations make more accurate and informed access decisions.

Rising Demand for Unified Identity Platforms in Hybrid Environments

Organizations adopt unified IGA platforms to manage identities across on-premise systems, SaaS applications, and multi-cloud architectures. Centralized dashboards offer better visibility into user privileges and improve governance efficiency. Growing complexity in hybrid environments pushes enterprises to seek seamless integration across directories, HR systems, and security tools. Vendors offering flexible and interoperable platforms gain strong market momentum. Increasing hybrid workforce models further accelerate the need for unified identity governance.

- For instance, CyberArk helps secure over 10,000 global customers, including more than 55% of the Fortune 500 and over 35% of the Global 2000. These organizations leverage CyberArk’s identity security platform to manage and secure access across a mix of environments.

Key Challenges

High Deployment and Integration Complexity

Large enterprises face challenges integrating IGA systems with legacy applications, on-premise architectures, and diverse cloud platforms. Complex identity structures require extensive customization, extending deployment time and cost. Many organizations lack skilled personnel to manage advanced IGA configurations, slowing system adoption. Ensuring smooth synchronization across multiple identity sources remains difficult for IT teams. These complexities often hinder organizations from achieving full automation and governance efficiency.

Rising Costs for Implementation and Long-Term Maintenance

Implementing a comprehensive IGA platform requires significant investment in software, consulting, integration, and ongoing support. Small and mid-sized enterprises often struggle with budget constraints, limiting adoption of advanced governance tools. Continuous updates, compliance audits, and license renewals increase operational expenses. Organizations must invest in skilled resources to maintain identity workflows, access policies, and governance rules. These financial and resource burdens remain key obstacles to widespread IGA adoption.

Regional Analysis

North America

North America leads the Identity Governance and Administration market with a 39% share, driven by strong regulatory frameworks, rapid cloud adoption, and high cybersecurity awareness among enterprises. U.S.-based organizations invest heavily in automated identity lifecycle tools to meet strict compliance standards like HIPAA, SOX, and FedRAMP. The region sees rising demand for cloud-based IGA platforms as businesses support large remote workforces and hybrid IT architectures. Advanced adoption of zero-trust security and growing insider threat concerns strengthen market growth. Major technology vendors and high digital maturity further reinforce North America’s dominant position.

Europe

Europe holds a 28% share, supported by strict enforcement of GDPR and sector-specific regulations that require consistent identity governance and secure access controls. Enterprises across Germany, the UK, and France invest in IGA platforms to manage complex identity structures across cloud and on-premise systems. The region’s strong focus on data privacy accelerates adoption of automated certification workflows and risk-based access policies. Growing digital transformation in financial services, manufacturing, and public sectors enhances demand. Increased awareness of identity-related breaches and rising hybrid environments strengthen Europe’s role in the global IGA market.

Asia Pacific

Asia Pacific commands a 23% share, driven by rapid enterprise digitization, large-scale cloud migration, and growing cybersecurity threats. Companies across China, India, Japan, and Southeast Asia adopt IGA platforms to manage expanding identity volumes and strengthen compliance with evolving data protection laws. The region’s increasing adoption of SaaS applications and hybrid IT models boosts demand for scalable governance solutions. Growth in banking, telecom, and IT services accelerates need for automated access controls and lifecycle management. Rising investments in digital infrastructure and expanding remote work contribute to strong regional momentum.

Latin America

Latin America holds a 6% share, supported by growing digital transformation and increasing adoption of identity security tools across financial services, retail, and public sectors. Brazil and Mexico lead demand as enterprises strengthen governance frameworks to address rising cyber threats and comply with new data protection laws. Cloud adoption continues to expand, driving interest in scalable IGA platforms. Limited identity expertise and budget constraints slow adoption in smaller organizations, but rising awareness of access risks supports steady growth. Investments in secure digital services and government modernization initiatives further drive regional expansion.

Middle East & Africa

The Middle East & Africa region accounts for a 4% share, driven by growing cybersecurity investments and rising adoption of identity governance solutions in banking, oil and gas, and government sectors. GCC countries lead with rapid deployment of cloud-based IGA platforms to support national digital transformation programs. Increasing cyberattacks and insider risks push enterprises to adopt automated access monitoring and certification tools. Regulatory modernization in data privacy strengthens market potential, though adoption remains slower in parts of Africa. Expanding cloud infrastructure and enterprise modernization efforts continue to support gradual growth in the region.

Market Segmentations:

By Component

- Solutions

- Services

- Professional Services

- Managed Services

By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid

By Functionality

- Access Certification & Compliance Control

- Access Management

- Identity Lifecycle Management

- Others

By End Use

- IT & Telecom

- BFSI

- Healthcare

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape features leading companies such as Microsoft Corporation, Okta, Inc., IBM Corporation, CyberArk Software Ltd., Imprivata, Inc., Oracle Corporation, Amazon Web Services, Inc., Micro Focus International plc, Evidian (Atos SE), and Broadcom Inc. (Symantec), all of which shape the Identity Governance and Administration market through advanced security capabilities and strong integration frameworks. These players focus on AI-driven identity analytics, automated access workflows, and unified governance platforms that support both cloud and hybrid environments. Vendors expand partnerships with enterprises to strengthen zero-trust adoption and improve compliance readiness. Continuous R&D enhances identity lifecycle automation, privileged access controls, and risk-based authentication. Many companies also invest in cloud-native IGA solutions that scale with growing identity volumes driven by digital transformation. As cyber threats rise, competition intensifies around real-time monitoring, anomaly detection, and interoperability with broader security ecosystems, reinforcing the market’s innovation-driven growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Microsoft Corporation

- Okta, Inc.

- IBM Corporation

- CyberArk Software Ltd.

- Imprivata, Inc.

- Oracle Corporation

- Amazon Web Services, Inc.

- Micro Focus International plc

- Evidian (Atos SE)

- Broadcom Inc. (Symantec)

Recent Developments

- In February 2025, CyberArk Software Ltd. acquired Zilla Security to integrate AI-powered IGA capabilities into its Identity Security Platform.

- In 2025, IBM Corporation ranks among the top three IAM/IGA providers according to a 2025 buyers’ guide.

- In December 2024, Imprivata, Inc. sold its IGA business to SailPoint and entered into a strategic go-to-market partnership focused on healthcare identity and access management

Report Coverage

The research report offers an in-depth analysis based on Component, Deployment Mode, Functionality, End Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for automated identity lifecycle management will rise as enterprises scale digital operations.

- Cloud-based IGA platforms will gain wider adoption due to flexibility and faster deployment.

- Zero-trust security models will increase reliance on continuous identity verification and access oversight.

- AI-driven identity risk scoring will strengthen real-time threat detection and policy decisions.

- Unified governance platforms will grow as organizations manage identities across hybrid and multi-cloud ecosystems.

- Privileged access governance will expand as insider threats and credential misuse increase.

- Regulatory pressure will drive more enterprises to adopt advanced compliance automation tools.

- Integration of IGA with broader security ecosystems will improve visibility and incident response.

- SMEs will adopt simplified and cost-effective IGA solutions as vendor offerings become more modular.

- Identity governance will shift toward predictive models that reduce manual intervention and enhance security outcomes.