| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| India Green Data Center Market Size 2024 |

USD 1,623.11 Million |

| India Green Data Center Market, CAGR |

21.38% |

| India Green Data Center Market Size 2032 |

USD 7,645.97 Million |

Market Overview

The India Green Data Center Market is projected to grow from USD 1,623.11 million in 2024 to an estimated USD 7,645.97 million by 2032, with a compound annual growth rate (CAGR) of 21.38% from 2025 to 2032. This growth is driven by increasing demand for energy-efficient and environmentally sustainable data storage solutions.

Key drivers of this market include the rapid digitalization across industries, which is pushing the demand for data centers with reduced environmental impact. Moreover, government regulations and incentives for green building certifications are encouraging businesses to adopt energy-efficient technologies. The rising emphasis on renewable energy sources, including solar and wind power, for powering data centers is another significant trend. Furthermore, advancements in cooling technologies and energy-efficient designs are enhancing the sustainability of data center operations.

Geographically, the green data center market is expanding rapidly in urban areas of India, with major cities such as Bengaluru, Hyderabad, and Mumbai emerging as key hubs. The growing presence of global tech giants and local enterprises investing in data infrastructure is fueling market growth. Key players in the Indian Green Data Center Market include NTT Ltd., Adani Enterprises, and Netmagic Solutions, which are leading the way in developing energy-efficient data center solutions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The India Green Data Center Market is projected to grow from USD 1,623.11 million in 2024 to USD 7,645.97 million by 2032, with a CAGR of 21.38% from 2025 to 2032.

- The global Green Data Center Market is expected to grow from USD 59,645.02 million in 2024 to USD 239,470.06 million by 2032, at a CAGR of 18.98% from 2025 to 2032.

- The growth is driven by the increasing demand for energy-efficient and environmentally sustainable data storage solutions, with businesses and governments focusing on reducing carbon footprints.

- Government regulations and incentives for green building certifications are encouraging the adoption of energy-efficient technologies and renewable energy sources.

- Advancements in cooling technologies, energy-efficient infrastructure, and the integration of renewable energy are significant drivers of growth in the green data center market.

- High initial investment costs and the complexity of transitioning from traditional data centers to green technologies pose challenges for market growth.

- The market is expanding rapidly in urban areas of India, particularly in cities such as Bengaluru, Hyderabad, and Mumbai, which are emerging as key hubs for green data centers.

- Key players in the market include NTT Ltd., Adani Enterprises, and Netmagic Solutions, who are leading efforts in developing energy-efficient and sustainable data center solutions.

Report Scope

This report segments the India Green Data Center Market as follows:

Market Drivers

Technological Advancements in Data Center Infrastructure

Technological innovations have played a pivotal role in the growth of the green data center market in India. The advent of energy-efficient cooling technologies, such as liquid cooling and free-air cooling, has significantly reduced the power consumption required for temperature regulation within data centers. In addition, server virtualization, software-defined networking (SDN), and the integration of artificial intelligence (AI) in data center operations are optimizing energy usage and resource allocation, thus improving overall efficiency. These advancements allow data centers to handle larger volumes of data while consuming less power, which directly contributes to reducing their carbon footprint. The development of cloud computing platforms and the increasing adoption of hybrid cloud infrastructures have also boosted demand for more sustainable data storage solutions. As more companies transition to cloud services, the need for energy-efficient data centers that minimize environmental impact grows. These innovations not only enable data centers to lower energy costs but also make them more adaptable to future technological developments, driving the expansion of green data centers in India.

Adoption of Renewable Energy Sources

The shift towards renewable energy sources is another critical driver for the growth of the green data center market in India. As the country pushes for a more sustainable future, the adoption of renewable energy, including solar, wind, and hydroelectric power, is becoming increasingly prevalent within the data center sector. India is one of the world’s largest solar power producers, and its government has been making significant investments to increase renewable energy capacity. Many data centers are tapping into these resources to reduce their reliance on conventional grid power, which is typically sourced from fossil fuels and contributes to higher carbon emissions. By incorporating renewable energy, such as solar and wind, data centers can operate with lower environmental impact while reducing their operational costs in the long run. The integration of renewable energy into data centers not only supports India’s national climate goals but also aligns with global sustainability trends. Additionally, green energy-driven data centers benefit from improved corporate social responsibility (CSR) ratings, appealing to environmentally conscious consumers and investors, thus boosting the market for green data centers.

Rising Demand for Sustainable Solutions in Data Centers

The growing awareness of environmental sustainability is driving the demand for green data centers in India. As the country continues to experience rapid digital transformation across industries such as finance, e-commerce, IT, and telecommunications, the need for data storage, processing, and management solutions has surged. However, this increased demand for data centers also leads to higher energy consumption, contributing significantly to carbon footprints. Consequently, there is a shift towards green data centers, which focus on reducing energy usage and emissions while ensuring efficient and sustainable data storage operations. Green data centers leverage technologies like energy-efficient servers, advanced cooling systems, and renewable energy sources, all of which contribute to lowering operational costs and meeting environmental goals. For instance, Yotta Infrastructure’s data center in Navi Mumbai uses a solar power system generating 10 megawatts annually, reducing carbon emissions equivalent to nearly 20,000 metric tons. This trend is gaining traction as both businesses and governments prioritize reducing their ecological impact. By adopting these solutions, organizations can mitigate their environmental impact and meet regulatory compliance requirements, further driving the green data center market’s growth.

Government Regulations and Incentives for Sustainability

The Indian government has made significant strides in promoting sustainability through various initiatives and regulatory frameworks. Policies like the National Action Plan on Climate Change (NAPCC) and the promotion of renewable energy are fostering an environment conducive to the growth of green technologies, including green data centers. Additionally, the government has introduced several incentives and subsidies to encourage energy-efficient practices within industries, including data storage and management. These initiatives provide tax benefits, rebates, and funding for companies that invest in energy-efficient technologies and green building certifications, which are crucial for the development of green data centers. For instance, under the Energy Conservation Building Code (ECBC), energy-efficient designs in commercial buildings, including data centers, have led to reductions in energy consumption equivalent to tens of thousands of kilowatt-hours per year in facilities like the CtrlS data center in Hyderabad. Furthermore, the government’s push for a digital economy, coupled with its ambitious renewable energy targets, aligns with the green data center market’s expansion. These regulations, combined with the economic benefits of reducing energy consumption, are key drivers that are propelling the adoption of green data centers in India.

Market Trends

Integration of Renewable Energy Sources

One of the most prominent trends in the Indian green data center market is the increasing adoption of renewable energy sources. Data centers in India are increasingly turning to solar, wind, and hydroelectric power to reduce reliance on conventional energy grids. For instance, a data center in Karnataka has installed solar panels capable of generating 1.2 megawatts of clean energy annually, reducing its carbon emissions by approximately 15,000 metric tons per year. As India ramps up its renewable energy capacity, data centers are leveraging these clean energy options to minimize their environmental impact. Major data center providers are also entering into power purchase agreements (PPAs) with renewable energy producers to secure a consistent supply of green energy. This trend not only helps data centers reduce their carbon footprint but also provides a cost-effective way to manage energy consumption in the long term. The integration of renewable energy is aligned with India’s broader sustainability goals, further reinforcing the role of green data centers in meeting national and global climate objectives.

Adoption of Advanced Cooling Solutions

In an effort to optimize energy efficiency, India’s green data centers are increasingly adopting advanced cooling technologies. Cooling systems, which account for a significant portion of data center energy consumption, are being revamped with energy-efficient solutions such as liquid cooling, free-air cooling, and indirect evaporative cooling. For instance, a data center in Tamil Nadu has implemented liquid cooling systems, achieving a 25% reduction in cooling energy consumption compared to traditional air-based methods. By utilizing external air or liquid-based cooling methods, data centers can significantly cut down on the power consumed by traditional air conditioning systems. Additionally, AI-based monitoring systems are being implemented to dynamically adjust cooling needs based on real-time data, further improving energy efficiency. These advanced cooling technologies are not only reducing operational costs but also helping data centers meet stringent environmental regulations and sustainability goals. This trend is expected to become more prevalent as data centers seek to balance the increasing demand for computing power with the need for energy conservation, especially in India’s hot climate.

Increase in Modular Data Center Designs

Modular data centers are emerging as a popular trend in the India green data center market due to their scalability, energy efficiency, and lower environmental impact. Unlike traditional, large-scale data centers that require extensive infrastructure and energy consumption, modular data centers are pre-fabricated units that can be quickly deployed and scaled according to demand. These modular units are designed with energy efficiency in mind, incorporating advanced power management systems and cooling technologies to minimize environmental impact. Furthermore, they are built to be highly flexible, allowing operators to add capacity as needed without overbuilding, thus reducing wasted energy. The modular approach also enables data center providers to adopt sustainable practices at a faster pace, with less capital investment. This trend is particularly relevant in India, where demand for data storage and cloud services is growing rapidly but where infrastructure expansion needs to be efficient and environmentally responsible. Modular data centers also enable better resource optimization, which aligns with the push for green operations.

Government Support and Regulatory Frameworks

The Indian government’s increasing focus on environmental sustainability is shaping the growth of the green data center market. Policies and regulations aimed at promoting energy efficiency are encouraging the adoption of green practices in the data center industry. For example, the Indian government is offering tax benefits, subsidies, and other incentives for businesses investing in energy-efficient technologies and infrastructure. Additionally, the government has introduced frameworks such as the Energy Conservation Building Code (ECBC) and the promotion of renewable energy to accelerate the transition towards greener data centers. The government’s push for a digital economy and smart city initiatives is also creating a favorable environment for the growth of green data centers. With regulations emphasizing lower energy consumption and reduced carbon emissions, data center operators are increasingly aligning their operations with these guidelines. As the Indian government continues to prioritize sustainability, the green data center market is expected to benefit from enhanced support, incentives, and regulatory frameworks that promote environmental responsibility. This trend will likely intensify as India seeks to meet its climate targets.

Market Challenges

High Initial Capital Investment

One of the primary challenges facing the India Green Data Center Market is the high initial capital investment required for building energy-efficient and sustainable infrastructure. Green data centers often require advanced technologies such as energy-efficient cooling systems, renewable energy sources, and state-of-the-art monitoring systems, all of which involve significant upfront costs. For many businesses, especially small and medium enterprises (SMEs), the capital required to transition from traditional data centers to green alternatives can be a major barrier. While these investments promise long-term savings through reduced operational costs, the high initial financial commitment can deter companies from adopting green data center solutions. Moreover, the complexity of integrating renewable energy sources such as solar or wind power, along with the need for specialized infrastructure, adds to the overall costs, making it difficult for some businesses to make the shift. As a result, overcoming the challenge of high capital expenditure remains a critical factor for widespread adoption in the market.

Technical Complexity and Transition from Legacy Systems

Another significant challenge in the India Green Data Center Market is the technical complexity involved in transitioning from legacy data centers to green solutions. For instance, many existing data centers rely on outdated infrastructure and technologies that are not optimized for energy efficiency or sustainability. Upgrading these facilities to meet the standards of green data centers can be a complicated and resource-intensive process. This includes the integration of advanced cooling systems, efficient power management solutions, and the incorporation of renewable energy sources. Additionally, organizations may face difficulties in training their workforce to manage and operate these new technologies effectively. The transition often requires a thorough redesign of existing data center operations, which can lead to disruptions in service and potential downtime. Given the technical expertise required for such upgrades and the potential risks involved, many businesses are hesitant to make the leap to greener solutions. This technical complexity adds another layer of challenge to the growth of the India Green Data Center Market.

Market Opportunities

Growing Demand for Cloud Computing and Digital Transformation

The rapid digital transformation across various industries in India is creating significant opportunities for the green data center market. As businesses increasingly move to the cloud and adopt data-driven solutions, the demand for data storage, processing, and management is skyrocketing. This surge in demand is being met with a shift towards more sustainable data center practices, providing ample growth potential for green data centers. With the rise of industries such as e-commerce, finance, healthcare, and telecommunications, there is an increasing need for energy-efficient and environmentally responsible data storage solutions. Green data centers that offer scalable, energy-efficient, and renewable energy-powered solutions are well-positioned to capitalize on this trend. Additionally, with India’s focus on reducing its carbon footprint and meeting its renewable energy targets, companies adopting green data centers will not only align with regulatory guidelines but also gain a competitive edge in the market. This growing demand for cloud-based services, coupled with a heightened emphasis on sustainability, represents a strong market opportunity for green data centers in India.

Government Incentives and Sustainability Mandates

India’s government is actively promoting sustainability through various incentives, subsidies, and regulatory frameworks aimed at encouraging the adoption of energy-efficient technologies. These government initiatives are creating a favorable environment for the green data center market, providing financial support for companies investing in sustainable infrastructure. Programs such as tax rebates, subsidies for renewable energy adoption, and regulations that mandate energy efficiency standards are helping to accelerate the development of green data centers. Additionally, India’s growing focus on digital infrastructure, smart cities, and renewable energy targets further bolsters the demand for green data centers. These regulatory drivers present a significant market opportunity for operators to expand their sustainable operations, offering a competitive advantage in both the local and global markets as India continues to prioritize its environmental goals.

Market Segmentation Analysis

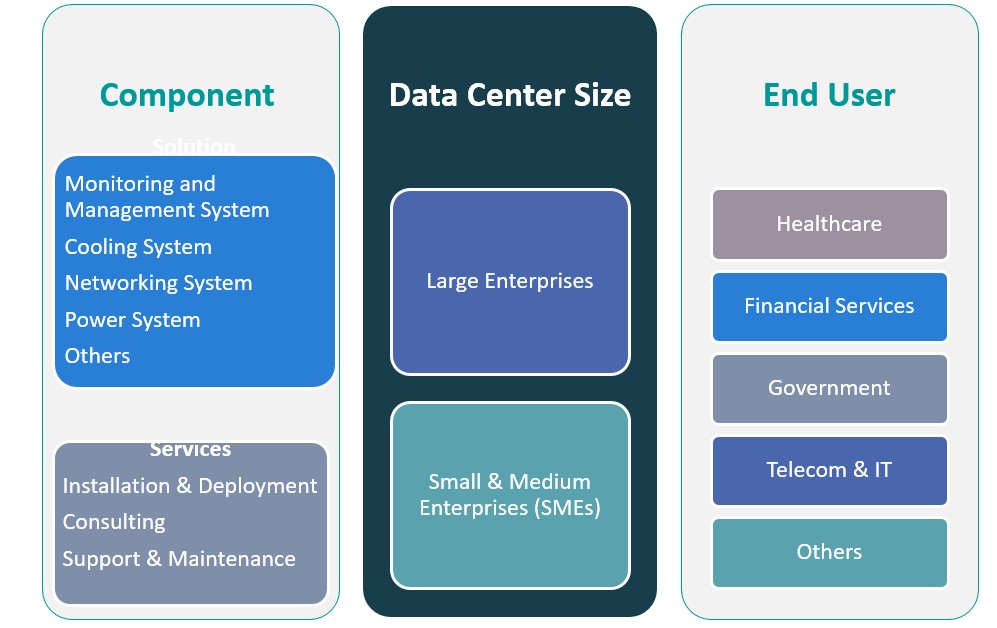

By Component

The India Green Data Center Market is segmented by components into solutions and services. The solutions segment includes critical infrastructure systems such as monitoring and management systems, cooling systems, networking systems, and power systems, all of which play essential roles in ensuring the efficiency and sustainability of data center operations. Among these, cooling systems are crucial, as they account for a significant portion of energy consumption in traditional data centers. Advanced cooling systems, such as liquid and free-air cooling, are becoming increasingly prevalent as they offer substantial energy savings. Monitoring and management systems are also vital for optimizing energy usage and ensuring that data centers meet environmental standards. Networking systems and power systems are key for the overall performance and efficiency of the data center, with a focus on reducing power consumption and increasing uptime. The services segment consists of installation & deployment, consulting, and support & maintenance, which are integral to the functioning of green data centers. These services ensure that data centers are efficiently deployed, maintain high operational standards, and continue to optimize energy usage throughout their lifecycle.

By Data Center Type

The India Green Data Center Market is also segmented by data center type into large enterprises and small & medium enterprises (SMEs). Large enterprises, which typically require substantial data storage and processing capabilities, are the dominant segment. These organizations are increasingly adopting green data centers due to the need to manage vast amounts of data while adhering to sustainability regulations. Large enterprises often invest in state-of-the-art infrastructure and advanced technologies, including renewable energy sources and energy-efficient cooling systems, making them key drivers of the green data center market. SMEs, on the other hand, are gradually adopting green data center solutions as well, driven by the increasing need for digital transformation and scalability. While their demand for data center capacity may be smaller compared to large enterprises, SMEs are nonetheless significant participants in the market, especially with the rise of cloud-based solutions and affordable green data center options tailored to their needs.

Segments

Based on Component

- Solution

- Monitoring and Management System

- Cooling System

- Networking System

- Power System

- Others

- Services

- Installation & Deployment

- Consulting

- Support & Maintenance

Based on Data Center Type

- Large Enterprises

- Small & Medium Enterprises (SMEs)

Based on End User

- Healthcare

- Financial Services

- Government

- Telecom & IT

- Others

Based on Region

- North India

- South India

- West India

- East India

Regional Analysis

South India (40%)

South India is the dominant region in the green data center market, holding a market share of approximately 40%. This region is home to major IT hubs, including cities like Bengaluru, Chennai, and Hyderabad, which are known for their well-established IT infrastructure and high concentration of both large enterprises and small & medium enterprises (SMEs). South India also benefits from a favorable climate, which aids in the adoption of energy-efficient cooling technologies. Furthermore, the region’s push towards renewable energy adoption and sustainability initiatives supports the growth of green data centers. The presence of large tech companies such as Infosys, Wipro, and Tata Consultancy Services, which are committed to sustainability, further bolsters the demand for green data center solutions in this region.

West India (30%)

West India follows with a significant market share of around 30%. The region, particularly cities like Mumbai and Pune, hosts several financial institutions, telecom companies, and e-commerce giants. These sectors are heavy consumers of data center services due to their large-scale data processing requirements. The growing demand for cloud services, data analytics, and digital transformation initiatives in the telecom and IT sectors is driving the adoption of green data centers in West India. Additionally, Mumbai’s strategic location as a financial and commercial hub makes it a key player in the green data center market. The region’s government initiatives promoting energy-efficient infrastructure and renewable energy integration are also contributing to the growth of sustainable data center operations.

Key players

- eStruxture

- Digital Realty

- Q9 Networks

- Hydro-Québec

- Leaseweb

Competitive Analysis

The India Green Data Center Market is competitive, with both local and global players striving to capitalize on the growing demand for energy-efficient data storage solutions. eStruxture focuses on offering scalable and sustainable data center services, with a strong emphasis on renewable energy and energy-efficient infrastructure. Digital Realty, a global leader, brings extensive experience in building and operating green data centers, leveraging its global presence and sustainability initiatives to offer innovative solutions. Q9 Networks is a significant player in North America but is expanding its green data center capabilities globally, including in India, focusing on high-performance and eco-friendly infrastructure. Hydro-Québec stands out with its focus on utilizing hydroelectric power for data center operations, making it a key player in the renewable-powered data center space. Leaseweb is known for its cost-effective solutions combined with energy-efficient technologies, making it a prominent player in the competitive landscape of green data centers. These companies’ strategic focus on sustainability and renewable energy integration positions them as strong competitors in the Indian market.

Recent Developments

- In December 2023, Vertiv acquired CoolTera Ltd., a provider of liquid cooling infrastructure solutions. This acquisition strengthens Vertiv’s capabilities in high-density compute cooling, aligning with the industry’s shift towards energy-efficient data center technologies.

- In July 2024, Huawei unveiled three green data center facility solutions at the Global Smart Data Center Summit. These include the AeroTurbo fans, IceCube polymer heat exchangers, and iCooling AI energy efficiency cooling solutions, designed to optimize cooling efficiency and reduce energy consumption.

- In May 2024, Microsoft launched its first hyperscale cloud data center region in Mexico, located in Querétaro. This facility aims to provide scalable, highly available, and resilient cloud services, supporting digital transformation and sustainable innovation in the region.

- In June 2024, HPE partnered with Danfoss to introduce the HPE IT Sustainability Services – Data Center Heat Recovery. This turnkey heat recovery module helps organizations manage and repurpose excess heat, contributing to more sustainable IT infrastructures.

- In November 2024, Google announced a partnership with SB Energy Global to supply 942 MW of renewable energy to power its data center operations in Texas. This initiative supports Google’s commitment to operate on carbon-free energy and aligns with its sustainability goals.

- In January 2025, AWS announced plans to invest approximately $11 billion in Georgia to expand its infrastructure, supporting cloud computing and AI technologies. This investment is expected to create at least 550 new high-skilled jobs and enhance the state’s digital innovation capabilities.

- In May 2024, IBM announced a partnership with Schneider Electric to develop and deploy energy-efficient data center solutions, focusing on reducing carbon emissions and improving operational efficiency.

Market Concentration and Characteristics

The India Green Data Center Market exhibits a moderate level of market concentration, with a few key players dominating the landscape while also providing opportunities for smaller entrants. Major global data center providers such as Digital Realty and Leaseweb are expanding their operations in India, capitalizing on the growing demand for sustainable and energy-efficient data solutions. At the same time, regional players and smaller firms are also emerging, offering specialized green data center services tailored to local requirements. The market is characterized by rapid technological advancements, particularly in energy-efficient cooling systems, renewable energy integration, and modular data center designs. Additionally, government regulations and incentives are shaping the competitive environment, encouraging players to adopt greener practices. The overall trend is a move towards sustainable infrastructure, where both large enterprises and SMEs are increasingly investing in green data center solutions to meet digitalization demands while adhering to environmental goals.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Component, Data Center Type, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- As India continues its digital transformation, the demand for green data centers is expected to grow significantly. Businesses will increasingly prioritize energy-efficient, eco-friendly solutions to meet sustainability targets and reduce carbon footprints.

- Government policies will continue to encourage the adoption of green data centers through subsidies, tax incentives, and sustainability mandates. These efforts will drive the transition towards renewable energy and energy-efficient infrastructure.

- The adoption of renewable energy sources, including solar and wind, will become more widespread in the data center sector. By tapping into India’s growing renewable energy capacity, data centers can reduce their reliance on fossil fuels and decrease their environmental impact.

- Innovative cooling technologies, such as liquid and free-air cooling, will become more prevalent, reducing energy consumption. These advancements will optimize operational efficiency and minimize the environmental footprint of data centers.

- Modular data centers will gain traction due to their scalability and energy efficiency. These units will allow businesses to quickly expand their operations while maintaining sustainable and energy-efficient practices.

- Artificial intelligence (AI) and automation will be used to optimize energy consumption and resource allocation. These technologies will enhance the performance and sustainability of data centers by enabling real-time monitoring and adaptive energy management.

- Energy efficiency will remain a key focus for green data centers. Operators will increasingly invest in optimizing power usage effectiveness (PUE) and enhancing operational efficiency to minimize both energy consumption and operational costs.

- As cloud services and edge computing continue to grow, green data centers will play a vital role in supporting these technologies. The expansion of these services will drive demand for energy-efficient data center infrastructure across the country.

- There will be a continued regional expansion in India, with a strong focus on emerging cities outside major tech hubs. This will open up new opportunities for green data centers to cater to the growing demand for digital infrastructure across various sectors.

- Collaboration between technology companies, renewable energy providers, and government agencies will be essential to accelerating the development of green data centers. These partnerships will foster innovation, investment, and the widespread adoption of sustainable practices across the market.