Market Overview

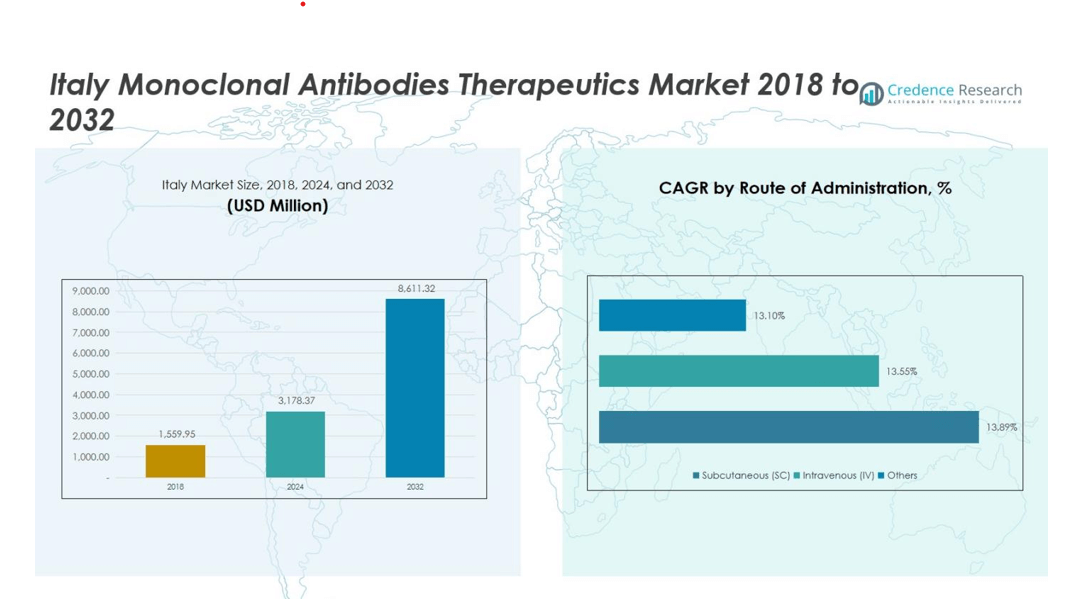

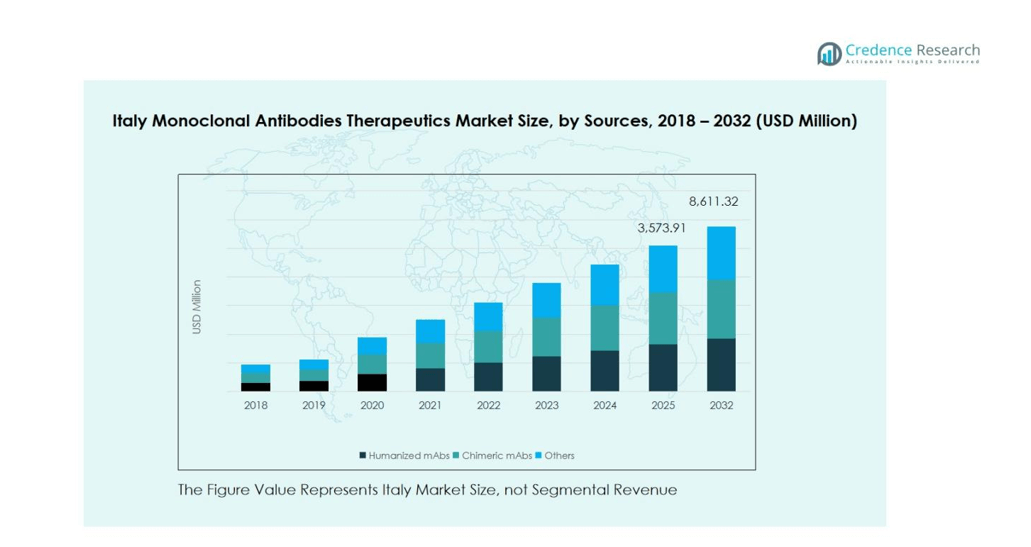

Italy Monoclonal Antibodies Therapeutics Market size was valued at USD 1,559.95 Million in 2018 and grew to USD 3,178.37 Million in 2024. It is anticipated to reach USD 8,611.32 Million by 2032, growing at a CAGR of 13.2% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Italy Monoclonal Antibodies Therapeutics Market Size 2024 |

USD 3,178.37 Million |

| Italy Monoclonal Antibodies Therapeutics Market, CAGR |

13.2% |

| Italy Monoclonal Antibodies Therapeutics Market Size 2032 |

USD 8,611.32 million |

The Italy Monoclonal Antibodies Therapeutics Market is led by key players including F. Hoffmann-La Roche Ltd, Sanofi, AbbVie Inc., Bristol Myers Squibb, Amgen Inc., Eli Lilly and Company, AstraZeneca, Pierre Fabre S.A., Regeneron Pharmaceuticals Inc., and Johnson & Johnson Services, Inc. These companies drive the market through strategic initiatives such as product launches, collaborations, and investment in research and development, focusing on innovative therapies like humanized and bispecific antibodies. Northern Italy emerges as the leading region, capturing 40% of the market due to its robust healthcare infrastructure, concentration of specialty hospitals, and high patient awareness. Central Italy follows with a 25% share, supported by major medical research centers and clinical trial activities. Southern Italy and the islands account for 20% and 15% respectively, reflecting growing adoption of monoclonal antibodies and expanding healthcare access in these regions.

Market Insights

- The Italy Monoclonal Antibodies Therapeutics Market was valued at USD 3,178.37 Million in 2024 and is projected to reach USD 8,611.32 Million by 2032, growing at a CAGR of 13.2%.

- Rising prevalence of cancer, autoimmune, and chronic diseases is driving the demand for monoclonal antibodies, with humanized mAbs holding the largest share of 55% in the sources segment.

- Market trends include the increasing adoption of subcutaneous administration, which accounts for 60% of the route of administration segment, and growing use of biosimilars to improve patient access.

- Competitive players such as F. Hoffmann-La Roche Ltd, Sanofi, AbbVie Inc., and Bristol Myers Squibb are actively investing in R&D, product launches, and collaborations to strengthen their market position.

- Regionally, Northern Italy leads with a 40% market share, followed by Central Italy at 25%, Southern Italy at 20%, and the islands of Sicily and Sardinia at 15%, reflecting strong healthcare infrastructure and patient awareness.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

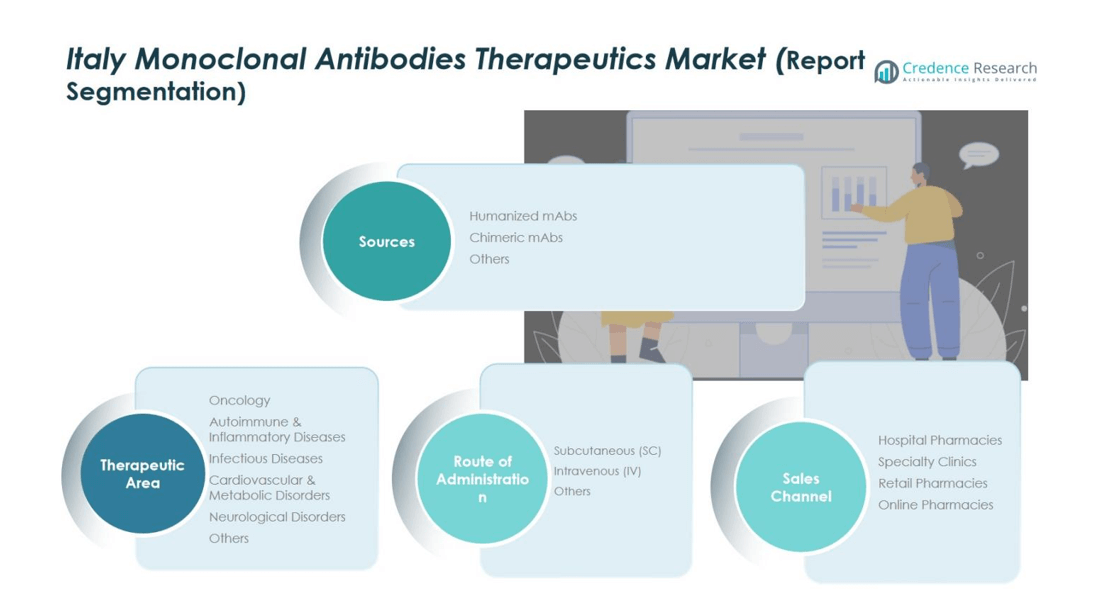

Market Segmentation Analysis:

By Sources:

The Italy Monoclonal Antibodies Therapeutics Market is primarily driven by humanized mAbs, which dominate the sources segment with an estimated market share of 55%. Humanized antibodies are preferred due to their enhanced safety profile, reduced immunogenicity, and broad therapeutic applicability. Chimeric mAbs account for around 30% of the market, supported by their established use in oncology and autoimmune disorders. The remaining 15% comprises other sources, including murine and fully human antibodies. Rising prevalence of chronic and autoimmune diseases, coupled with technological advancements in antibody engineering, continues to fuel the growth of humanized mAbs in Italy.

- For instance, Evusheld (tixagevimab-cilgavimab), another humanized monoclonal antibody combination by AstraZeneca, was approved in Italy for pre-exposure prophylaxis of COVID-19 in immunocompromised individuals, demonstrating a 77% reduction in the risk of infection compared to placebo in clinical studies.

By Therapeutic Area:

Oncology emerges as the dominant therapeutic area in Italy, capturing a market share of 50%, driven by the rising incidence of cancers and increasing adoption of targeted immunotherapies. Autoimmune and inflammatory diseases hold around 20% of the market, reflecting the growing demand for precision treatments. Infectious diseases, cardiovascular and metabolic disorders, and neurological disorders collectively account for the remaining 30%. Expanding clinical trials, government support for biologics, and rising patient awareness are key factors accelerating growth across therapeutic areas, with oncology leading due to its high unmet medical needs and favorable reimbursement policies.

By Route of Administration:

Subcutaneous (SC) administration dominates the market with a share of 60%, owing to its convenience, patient compliance, and suitability for self-administration. Intravenous (IV) formulations account for roughly 35%, primarily used in hospital settings for complex therapies requiring controlled dosing. Other routes, including intramuscular and alternative delivery systems, cover the remaining 5%. The growth of SC administration is further driven by technological innovations in prefilled syringes and auto-injectors, alongside the increasing preference for home-based therapies and outpatient care, which reduce hospital visits and healthcare costs in Italy.

- For instance, SCHOTT Pharma offers ready-to-use prefillable glass and polymer syringes designed to improve patient safety, reduce contamination, and support homecare use.

Growth Drivers

Rising Prevalence of Chronic and Autoimmune Diseases

The growing incidence of chronic and autoimmune diseases in Italy, including cancer, rheumatoid arthritis, and multiple sclerosis, is a significant driver of the monoclonal antibodies therapeutics market. Patients increasingly require targeted and personalized therapies, and mAbs offer precision treatment with reduced side effects. Hospitals and specialty clinics are witnessing higher demand for biologics, particularly humanized and chimeric antibodies. Government initiatives promoting advanced therapies and reimbursement frameworks further facilitate patient access, fueling steady growth in monoclonal antibody adoption across the country.

- For instance, during the Omicron wave of the COVID-19 pandemic, Italian patients with inborn errors of immunity treated with monoclonal antibodies such as sotrovimab showed a significantly lower risk of hospitalization (OR 0.14, 95% CI 0.045–0.436, p < 0.001) and reduced disease severity, particularly when administered early in infection.

Technological Advancements in Antibody Engineering

Innovations in antibody engineering, such as bispecific antibodies, antibody-drug conjugates, and humanization techniques, are accelerating market growth. These advancements improve efficacy, safety, and stability, attracting higher adoption among clinicians and patients. Italian biotechnology firms and multinational companies are investing heavily in research and development to expand the therapeutic potential of mAbs, particularly in oncology and autoimmune diseases. The increasing use of precision medicine and clinical trials evaluating novel formulations enhances treatment outcomes and reinforces the role of monoclonal antibodies as a leading therapeutic option.

- For instance, BL-B01D1, a bispecific antibody-drug conjugate (ADC) targeting EGFR and HER3 developed by SystImmune, showed a 63.2% objective response rate in patients with EGFR-mutated non-small cell lung cancer during Phase I trials, highlighting its potential to overcome multidrug resistance.

Expansion of Home-Based and Outpatient Therapies

The shift toward home-based and outpatient treatments is driving demand for convenient administration routes, especially subcutaneous monoclonal antibodies. Prefilled syringes, auto-injectors, and patient-friendly delivery systems enable self-administration, improving compliance and reducing hospital visits. Italian healthcare providers are increasingly integrating these solutions into chronic disease management programs. This trend aligns with cost containment initiatives and rising patient preference for minimally invasive treatments, strengthening market adoption and supporting the broader expansion of monoclonal antibodies beyond traditional hospital settings.

Key Trends and Opportunities

Growth of Targeted Oncology Therapies

Oncology remains the dominant therapeutic area, with increasing investment in targeted therapies such as immune checkpoint inhibitors and bispecific antibodies. Italian hospitals and research centers are actively participating in clinical trials, expanding access to novel cancer treatments. Personalized therapy protocols based on genetic and molecular profiling are gaining traction, allowing clinicians to select the most effective monoclonal antibodies for individual patients. This trend is driving innovation, expanding therapeutic applications, and reinforcing Italy’s position as a key market for oncology-focused biologics.

- For instance, Rottapharm Biotech conducted a phase I/II clinical trial at the National Cancer Institute in Milan combining the EP4 antagonist vorbipiprant with the anti-PD-1 antibody balstilimab, demonstrating promising safety and disease control in metastatic gastrointestinal cancers

Increasing Adoption of Biosimilars

The introduction of biosimilar monoclonal antibodies presents significant growth opportunities in Italy, as cost-effective alternatives improve patient access. Biosimilars allow healthcare systems to manage high treatment costs without compromising efficacy, encouraging wider adoption across hospital and retail pharmacies. Italian regulatory bodies are streamlining approvals for biosimilars, and physician awareness of their safety and effectiveness is increasing. This creates potential for expanded market penetration, particularly in high-demand therapeutic areas like oncology and autoimmune disorders, while stimulating competition and innovation among key market players.

- For instance, Celltrion’s biosimilar infliximab products Remsima and Inflectra have been licensed in Italy since 2015 across multiple autoimmune indications, improving treatment affordability and access

Key Challenges

High Treatment Costs and Reimbursement Limitations

Despite their therapeutic benefits, monoclonal antibodies remain expensive, limiting accessibility for many patients. Reimbursement policies in Italy vary by region and therapy, creating disparities in treatment availability. The high cost of biologics also imposes financial pressure on healthcare systems, particularly for chronic disease management. These factors can slow adoption rates, especially for new or complex therapies. Companies must navigate pricing strategies, reimbursement negotiations, and patient assistance programs to ensure widespread market access and sustain growth in this cost-sensitive environment.

Risk of Immunogenicity and Adverse Effects

Monoclonal antibody therapies can induce immunogenic responses, including infusion reactions or antibody neutralization, which pose safety concerns for patients. Clinicians must carefully monitor dosing and administration, particularly with intravenous therapies, to mitigate adverse effects. Such risks may impact patient compliance and limit use in certain populations. Italian healthcare providers emphasize safety protocols and post-marketing surveillance, but potential adverse events remain a challenge that could slow market expansion, increase liability concerns, and necessitate ongoing investment in research to enhance antibody safety profiles.

Regional Analysis

Northern Italy

Northern Italy holds a significant share of the monoclonal antibodies therapeutics market, accounting for 40% of the overall market. The region benefits from a high concentration of specialty hospitals, research centers, and biopharmaceutical manufacturing facilities. The rising prevalence of chronic diseases, particularly oncology and autoimmune disorders, drives demand for advanced therapies. Additionally, strong healthcare infrastructure, government support, and high patient awareness contribute to the widespread adoption of monoclonal antibodies. Key hospitals and clinics in cities like Milan and Turin are increasingly utilizing humanized and subcutaneous therapies, reinforcing Northern Italy as the dominant regional market in the country.

Central Italy

Central Italy accounts for 25% of the monoclonal antibodies therapeutics market, supported by the presence of major medical research institutes and hospitals in cities like Rome and Florence. The region demonstrates strong adoption of both intravenous and subcutaneous administration routes, particularly for oncology and autoimmune treatments. Government-led health programs and increasing patient preference for targeted therapies contribute to steady growth. Investments in clinical trials and collaborations with multinational biopharmaceutical companies are accelerating access to novel biologics. Central Italy’s growing healthcare infrastructure and rising disease prevalence make it a key contributor to Italy’s overall monoclonal antibodies market.

Southern Italy

Southern Italy contributes 20% to the overall monoclonal antibodies therapeutics market, driven by increasing awareness of biologic treatments and expanding healthcare access in urban centers such as Naples and Bari. The rising incidence of cancer and autoimmune diseases, coupled with the adoption of cost-effective biosimilars, is fueling market growth. Hospital pharmacies and specialty clinics are key distribution channels, and the demand for subcutaneous therapies is increasing due to patient convenience. Despite slower infrastructure development compared to Northern Italy, government initiatives and regional healthcare programs are enhancing the adoption of monoclonal antibodies, positioning Southern Italy as a growing regional market.

Islands (Sicily and Sardinia)

The islands of Sicily and Sardinia account for 15% of the Italy monoclonal antibodies therapeutics market. Market growth is supported by improving healthcare infrastructure, increasing patient awareness, and regional government programs promoting access to biologics. Oncology and autoimmune disease treatments are the primary drivers, with subcutaneous administration gaining popularity for outpatient care. Hospital pharmacies and specialty clinics remain the main distribution channels, while limited access to large urban centers slows widespread adoption compared to mainland regions. Continued investment in healthcare facilities and partnerships with pharmaceutical companies are expected to strengthen the islands’ contribution to the overall market.

Market Segmentations:

By Sources

- Humanized mAbs

- Chimeric mAbs

- Others

By Therapeutic Area

- Oncology

- Autoimmune & Inflammatory Diseases

- Infectious Diseases

- Cardiovascular & Metabolic Disorders

- Neurological Disorders

- Others

By Route of Administration

- Subcutaneous (SC)

- Intravenous (IV)

- Others

By Sales Channel

- Hospital Pharmacies

- Specialty Clinics

- Retail Pharmacies

- Online Pharmacies

By Region

- Northern Italy

- Central Italy

- Southern Italy

- Islands

Competitive Landscape

The competitive landscape of the Italy Monoclonal Antibodies Therapeutics Market is dominated by key players such as F. Hoffmann-La Roche Ltd, Sanofi, AbbVie Inc., Bristol Myers Squibb, and Amgen Inc. Companies are actively focusing on strategic initiatives, including product launches, collaborations, and R&D investments, to strengthen their market position. Innovation in humanized and bispecific antibodies, along with the development of biosimilars, is driving competition. Market players are expanding subcutaneous and intravenous formulations to enhance patient compliance and accessibility. Additionally, partnerships with Italian hospitals and specialty clinics facilitate clinical trials and real-world adoption of therapies. Companies are also leveraging pricing strategies and patient assistance programs to overcome cost barriers. Overall, the market remains highly dynamic, with leading players investing in advanced therapies and expanding distribution channels to capture the growing demand for monoclonal antibodies across Italy.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Hoffmann-La Roche Ltd

- Sanofi

- AbbVie Inc.

- Bristol Myers Squibb Company

- Pierre Fabre S.A

- AstraZeneca

- Amgen Inc.

- Eli Lilly and Company

- Regeneron Pharmaceuticals Inc.

- Johnson & Johnson Services, Inc.

Recent Developments

- In October 2025, Orion Corporation (Finland) secured an exclusive commercial license from Abzena (UK) for a monoclonal antibody targeting a cancer with high unmet clinical need, strengthening Orion’s oncology drug development pipeline.

- In October 2025, Novo Nordisk (Denmark) acquired development and commercialization rights from Omeros Corporation (USA) for the monoclonal antibody asset zaltenibart, aimed at treating paroxysmal nocturnal hemoglobinuria, a rare blood disorder.

- In October 2025, Lupin’s subsidiary Nanomi (Netherlands) signed a definitive agreement to acquire VISUfarma (Netherlands), a portfolio company of GHO Capital Partners, to strengthen Lupin’s European operations and expand its global presence

Report Coverage

The research report offers an in-depth analysis based on Sources, Therapeutic Area, Route of Administration, Sales Channel and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Italy monoclonal antibodies therapeutics market is expected to continue growing due to increasing prevalence of cancer and autoimmune diseases.

- Expansion of biosimilar adoption will improve patient access and drive market penetration across hospitals and clinics.

- Advances in antibody engineering, including bispecific antibodies and antibody-drug conjugates, will create new treatment opportunities.

- Subcutaneous administration will gain preference for home-based and outpatient therapies, enhancing patient convenience and compliance.

- Oncology will remain the dominant therapeutic area, supported by clinical trials and targeted therapy adoption.

- Investment in research and development by key players will accelerate the launch of innovative therapies.

- Regional healthcare programs and infrastructure development in Southern Italy and islands will enhance market growth.

- Increasing physician awareness and patient education will drive acceptance of monoclonal antibody treatments.

- Collaborations between biopharmaceutical companies and Italian healthcare providers will expand therapeutic reach.

- Regulatory support for advanced therapies and reimbursement schemes will facilitate sustainable market growth.