Market Overview:

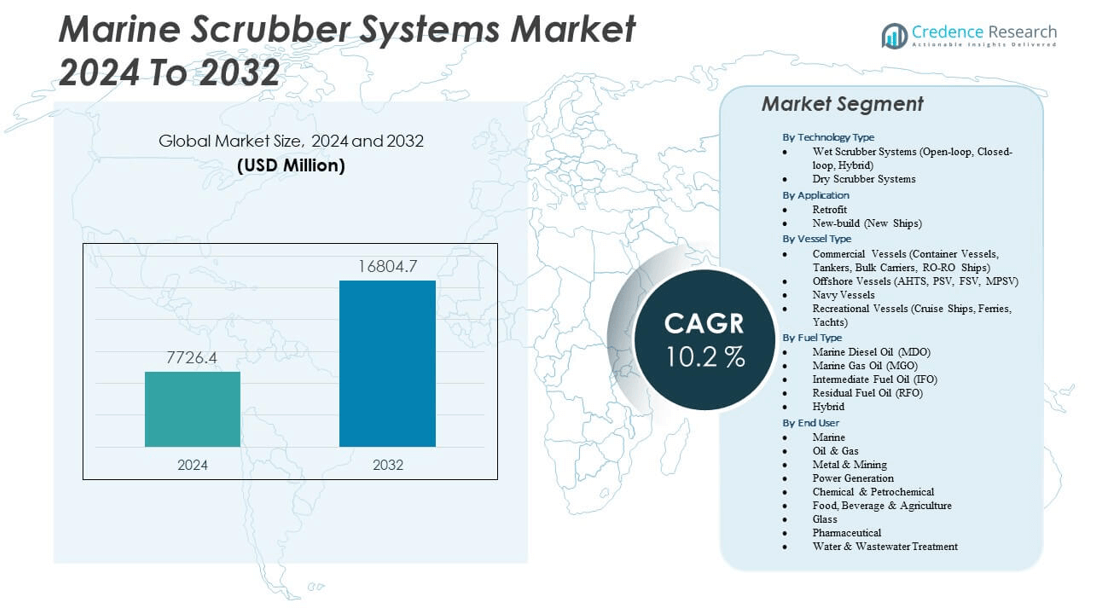

The Marine Scrubber Systems Market is projected to grow from USD 7,726.4 million in 2024 to an estimated USD 16,804.7 million by 2032, with a compound annual growth rate (CAGR) of 10.2% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Marine Scrubber Systems Market Size 2024 |

USD 7,726.4 million |

| Marine Scrubber Systems Market, CAGR |

10.2% |

| Marine Scrubber Systems Market Size 2032 |

USD 16,804.7 million |

The market is expanding due to stricter emission regulations from the International Maritime Organization (IMO) and rising concerns over marine pollution. Shipowners are adopting scrubber systems to comply with sulfur emission limits, avoid penalties, and maintain operational efficiency. Growing fuel cost differentials between high-sulfur and low-sulfur fuels further encourage the installation of scrubbers as a cost-saving solution. Increasing demand for retrofitting vessels and preference for hybrid systems also drive adoption, strengthening the long-term outlook of the market.

Regionally, Europe leads the market due to early adoption of emission-control technologies and strict environmental regulations across the North Sea and Baltic Sea. Asia Pacific is emerging as a high-growth region, supported by large-scale shipbuilding activities in China, South Korea, and Japan. North America also holds a significant share due to the presence of Emission Control Areas (ECAs) and growing fleet modernization efforts. Meanwhile, developing markets in Latin America and the Middle East are slowly gaining momentum, driven by rising trade activities and regional regulatory alignment.

Market Insights:

- The Marine Scrubber Systems Market is projected to grow from USD 7,726.4 million in 2024 to USD 16,804.7 million by 2032, at a CAGR of 10.2%.

- Strict sulfur emission regulations from the International Maritime Organization continue to drive large-scale adoption.

- Rising fuel price differentials between high-sulfur and low-sulfur fuels strengthen the business case for scrubber installations.

- High installation and operational costs remain a key restraint, limiting adoption among small and mid-sized operators.

- Europe holds the largest share of the market due to strong regulatory enforcement across Emission Control Areas.

- Asia-Pacific emerges as a fast-growing region, supported by major shipbuilding activities in China, South Korea, and Japan.

- North America maintains a significant position, driven by compliance within coastal Emission Control Areas and fleet modernization.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Growing enforcement of global emission control regulations by IMO and regional authorities

Regulatory frameworks remain the strongest growth engine for the Marine Scrubber Systems Market. The International Maritime Organization’s sulfur emission limits have pushed shipowners to adopt advanced exhaust cleaning solutions. National authorities in Europe, North America, and Asia Pacific are enforcing stricter regional emission control areas. Compliance requirements have made scrubber adoption an essential operational choice rather than an optional investment. Many shipping firms view scrubbers as cost-effective compliance tools compared with continuous fuel switching. This environment has expanded the demand for hybrid and open-loop scrubbers. It has also prompted fleets across bulk carriers, tankers, and container ships to adopt retrofits. These combined forces strengthen market penetration across existing and newbuild vessels.

- For example, Wärtsilä has delivered more than 800 marine exhaust gas cleaning systems worldwide, with the technology designed to achieve compliance by significantly reducing sulfur oxide emissions in line with IMO regulations.

Rising fuel price differentials between high-sulfur fuel oil and low-sulfur fuel oil

Fuel economics have become a defining factor for scrubber adoption. The cost difference between high-sulfur fuel oil and compliant low-sulfur alternatives remains significant. Scrubbers allow operators to continue using high-sulfur fuel oil while meeting emission requirements. This strategy delivers long-term cost savings for shipping firms operating large fleets. Many shipowners recognize the payback period for scrubber investments as highly attractive. Fuel savings encourage adoption even among mid-sized operators. It has positioned scrubbers as strategic assets to improve profit margins. The Marine Scrubber Systems Market benefits from this direct link between cost efficiency and regulatory compliance.

Expanding retrofitting activities across existing global fleets of shipping companies

Retrofitting vessels with scrubber technology has emerged as a key growth driver. Many shipping companies prioritize retrofitting to comply with current regulations without replacing older vessels. Retrofitting services provide flexibility to meet compliance quickly while extending vessel lifecycles. Shipyards and equipment providers have increased retrofit offerings to meet growing demand. It has created strong opportunities for aftersales support and technical services. The market has witnessed demand from bulk carriers, cruise liners, and container ships. Retrofitting ensures minimal disruption while maintaining efficiency and compliance. The Marine Scrubber Systems Market gains traction as operators pursue practical compliance pathways through retrofits.

Increasing shipbuilding activity in Asia and modernization of global maritime fleets

Growing shipbuilding activity across China, South Korea, and Japan fuels demand for scrubber integration. Many newbuild vessels are being designed with advanced scrubber technology as standard. Integration at the design stage lowers installation costs and ensures efficiency. Global fleet modernization initiatives in Europe and North America are reinforcing this growth. Modern shipping firms invest in fuel-efficient vessels equipped with emission control systems. Shipyards actively market scrubber-ready vessels to meet regulatory expectations worldwide. It has expanded collaboration between shipbuilders, technology providers, and shipping companies. The Marine Scrubber Systems Market advances through this wave of newbuild adoption and modernization projects.

- For instance, Hyundai Heavy Industries secured contracts to build scrubber-fitted Very Large Crude Carriers in 2022, highlighting shipyards’ role in delivering newbuild vessels equipped with exhaust gas cleaning systems to ensure compliance with emission regulations.

Market Trends

Strong preference for hybrid scrubber systems across diversified shipping applications

The Marine Scrubber Systems Market is observing a shift toward hybrid scrubber systems. Hybrid units offer flexibility to operate in both open-loop and closed-loop modes. This dual capability ensures compliance across regions with different discharge restrictions. Shipping companies prefer hybrid systems to reduce operational risks. Flexibility allows operators to manage costs and environmental obligations effectively. Hybrid demand has grown in cruise, container, and bulk carrier segments. Suppliers emphasize hybrid technologies to capture growing adoption. This preference highlights how versatility drives long-term competitiveness.

Growing emphasis on digital monitoring solutions for enhanced scrubber efficiency

Digitalization is reshaping the operational value of scrubber systems. Smart sensors and advanced monitoring software enable real-time tracking of emissions. Remote data collection supports compliance reporting and maintenance planning. It reduces risks of regulatory fines while enhancing operational transparency. Many suppliers are integrating IoT and AI-driven tools into their scrubber offerings. Automated performance optimization improves system reliability and lifecycle management. Digitalization also attracts fleet operators seeking efficiency beyond compliance. The Marine Scrubber Systems Market is advancing toward connected and intelligent solutions.

Strategic collaborations and mergers among technology providers and shipyards

Partnerships are becoming a defining trend in the scrubber industry. Technology providers and shipyards are collaborating to streamline design and integration. Joint ventures help optimize costs and accelerate adoption in both retrofits and newbuilds. Many companies are entering alliances to enhance market reach and service capability. It has encouraged the development of standardized solutions for global customers. Consolidation improves competitiveness while broadening technical expertise. Shipyards benefit by offering complete compliance-ready packages to shipowners. The Marine Scrubber Systems Market reflects this trend through increased industry consolidation and alliances.

- For example, in February 2022, MAN Energy Solutions signed a cooperation agreement with Hyundai Global Services, part of Hyundai Heavy Industries, to jointly market MAN’s Overridable Power Limitation (OPL) solution, supporting shipowners in meeting EEXI compliance requirements.

Rising demand for lightweight and compact scrubber designs with lower maintenance needs

The market is shifting toward more compact and efficient designs. Space constraints onboard vessels drive demand for smaller yet powerful scrubber systems. Lightweight models reduce fuel consumption and improve installation flexibility. Compact systems also lower maintenance requirements, improving cost efficiency. Many technology developers highlight modular systems that simplify retrofitting. Operators view reduced downtime as a significant advantage. Compact systems suit smaller vessels while remaining attractive to larger operators. The Marine Scrubber Systems Market grows as innovation aligns with efficiency and adaptability needs.

- For instance, Yara Marine Technologies developed an inline SOx scrubber that replaces a ship’s silencer, offering a compact and lightweight design suitable for both retrofits and newbuilds across different vessel types.

Market Challenges Analysis

High installation and operational costs impacting adoption among small and mid-sized operators

Cost remains a critical restraint for widespread scrubber adoption. Initial installation requires high capital investment, making it difficult for smaller operators to justify. Operational costs, including maintenance and consumables, add to long-term burdens. Financing challenges often limit access to advanced systems for regional shipping firms. Many small carriers face uncertainty about achieving payback periods. Market volatility in fuel prices can weaken projected savings from scrubber adoption. Shipowners must carefully assess long-term cost advantages before investment. The Marine Scrubber Systems Market continues to balance cost concerns with compliance needs.

Regulatory uncertainties and increasing scrutiny over washwater discharge practices

Regulatory shifts pose significant challenges for scrubber adoption strategies. Some regions have tightened restrictions on open-loop scrubbers due to washwater discharge concerns. Shipowners face uncertainty in investing heavily in systems that may face future bans. Variations in regional enforcement complicate decision-making for global fleets. Environmental groups continue to pressure regulators to impose stricter limits. Ship operators must remain adaptive to changing compliance requirements. Long-term uncertainty discourages investment among risk-averse companies. The Marine Scrubber Systems Market is shaped by regulatory unpredictability and evolving environmental concerns.

Market Opportunities

Expansion in emerging economies with growing maritime trade and fleet expansion programs

Emerging markets present strong opportunities for future growth. Expanding maritime trade across Asia, Latin America, and the Middle East supports higher demand for scrubbers. Governments are modernizing fleets and adopting stricter regulations to align with global standards. It creates a favorable environment for adoption across regional operators. Local shipyards are partnering with international technology providers to integrate scrubber systems. Market players can capitalize on rising demand through cost-effective solutions. These opportunities expand market penetration and long-term competitiveness. The Marine Scrubber Systems Market is well-positioned to benefit from emerging region adoption.

Increasing innovation in sustainable and energy-efficient scrubber system technologies

Innovation is opening new pathways for adoption. Manufacturers are developing scrubbers with lower energy consumption and eco-friendly designs. Sustainable models address concerns over environmental impacts and discharge issues. Advanced designs reduce water use and improve operational efficiency. Shipowners find value in solutions that balance compliance with sustainability. Research into alternative materials and modular layouts enhances system adaptability. Suppliers investing in R&D can differentiate themselves in a competitive market. The Marine Scrubber Systems Market benefits from continuous innovation that aligns with global decarbonization goals.

Market Segmentation Analysis:

The Marine Scrubber Systems Market is segmented

By technology type into wet scrubber systems and dry scrubber systems. Wet scrubbers, including open-loop, closed-loop, and hybrid variants, dominate demand due to their effectiveness in reducing sulfur emissions across diverse vessel classes. Dry scrubber systems serve niche applications where water use is limited, offering simpler operation but lower adoption compared to wet systems. It benefits from continuous innovation in hybrid scrubbers, which provide operational flexibility across regions with varied regulatory restrictions.

- For instance, Valmet has tested a scrubber combined with a wet electrostatic precipitator on a marine diesel engine and achieved up to 99% reduction in exhaust gas emissions during trials.

By application, the market divides into retrofit and new-build segments. Retrofit solutions lead adoption as shipowners prioritize compliance for existing fleets without investing in replacements. Retrofitting ensures regulatory alignment while extending vessel lifecycles. New-build installations are rising steadily with shipyards integrating scrubber systems at the design stage to optimize cost and efficiency. It reflects a balanced growth pattern where both retrofits and new-builds contribute significantly to overall demand.

By vessel type highlights commercial vessels such as container ships, bulk carriers, tankers, and RO-RO ships as primary adopters. Offshore vessels, including AHTS, PSV, FSV, and MPSV, represent a growing niche due to expanding offshore exploration activity. Navy vessels and recreational vessels such as cruise ships and ferries also deploy scrubbers to meet stringent environmental standards. It demonstrates wide adoption across both industrial and passenger-focused fleets.

By fuel type, the market covers marine diesel oil, marine gas oil, intermediate fuel oil, residual fuel oil, and hybrid categories. Residual fuel oil drives demand for scrubbers given its cost advantage, while hybrid fuels gain attention in modern fleets.

- For example, a lifecycle study conducted by researchers from MIT and Georgia Tech found that scrubbers operating on heavy fuel oil (HFO) delivered a 97% reduction in sulfur dioxide emissions. This performance brings HFO scrubber operations on par with low‑sulfur fuels, effectively supporting compliance with IMO 2020 sulfur limits

By end user, marine remains dominant, while oil and gas, metal and mining, power generation, and other industries adopt scrubber systems for emission control. It reflects the market’s expansion beyond shipping into industrial applications.

Segmentation:

By Technology Type

- Wet Scrubber Systems (Open-loop, Closed-loop, Hybrid)

- Dry Scrubber Systems

By Application

- Retrofit

- New-build (New Ships)

By Vessel Type

- Commercial Vessels (Container Vessels, Tankers, Bulk Carriers, RO-RO Ships)

- Offshore Vessels (AHTS, PSV, FSV, MPSV)

- Navy Vessels

- Recreational Vessels (Cruise Ships, Ferries, Yachts)

By Fuel Type

- Marine Diesel Oil (MDO)

- Marine Gas Oil (MGO)

- Intermediate Fuel Oil (IFO)

- Residual Fuel Oil (RFO)

- Hybrid

By End User

- Marine

- Oil & Gas

- Metal & Mining

- Power Generation

- Chemical & Petrochemical

- Food, Beverage & Agriculture

- Glass

- Pharmaceutical

- Water & Wastewater Treatment

By Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

Europe holds the largest share of the Marine Scrubber Systems Market, accounting for 34% of the global share. The region’s leadership stems from strict sulfur emission regulations enforced in Emission Control Areas across the Baltic Sea and North Sea. Strong adoption by commercial fleets, cruise operators, and container shipping companies drives demand. European shipowners prioritize compliance technologies to maintain competitiveness in regulated waters. Shipyards and retrofit providers across Norway, Germany, and Finland play a critical role in system installations. It benefits from advanced technology development and government-backed sustainability initiatives.

Asia-Pacific represents 30% of the market, driven by its dominant shipbuilding industry and large commercial fleet base. China, South Korea, and Japan lead new-build integration of scrubber systems, aligning with global emission standards. Rising maritime trade, combined with growing exports from emerging economies, strengthens adoption. Regional shipyards are increasingly collaborating with technology providers to offer scrubber-ready vessels. Offshore vessel deployment also contributes to regional growth with expanding exploration activity. The Marine Scrubber Systems Market grows strongly here due to a mix of regulatory enforcement and cost-focused operational strategies.

North America holds 18% of the market, supported by strict regulations within Emission Control Areas along both coasts. Strong demand arises from container vessels, tankers, and cruise ships operating in U.S. and Canadian waters. Latin America contributes 8%, supported by expanding maritime trade in Brazil, Mexico, and Chile. The Middle East & Africa together account for 10%, with adoption concentrated in major shipping hubs and oil-exporting nations. Regional growth here is tied to rising fleet modernization efforts and trade expansion. It demonstrates steady potential across developing markets seeking compliance and operational cost efficiency.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Alfa Laval AB

- Wärtsilä Oyj Abp

- Yara Marine Technologies AS

- Mitsubishi Heavy Industries, Ltd.

- Ecospray Technologies S.r.l.

- Clean Marine AS

- CR Ocean Engineering LLC

- VDL AEC Maritime B.V.

- LiqTech Holding A/S

- Langh Tech Oy Ab

- PureteQ A/S

- Saacke GmbH

- Pacific Green Technologies

Competitive Analysis:

The Marine Scrubber Systems Market features strong competition among global and regional players focusing on technology innovation, cost efficiency, and regulatory compliance. Leading companies emphasize hybrid scrubber systems to address varied emission standards across geographies. Strategic partnerships between shipyards and technology providers strengthen market presence by integrating solutions during new-build projects. Retrofitting services remain a key area where companies compete through flexible installation models and aftersales support. Firms invest in digital monitoring tools and compact designs to differentiate offerings. It benefits from continuous R&D as companies aim to balance performance, sustainability, and operational cost reduction. The Marine Scrubber Systems Market is characterized by consolidation, with mergers and alliances enabling wider service coverage and stronger technical expertise.

Recent Developments:

- In June 2025, TORM completed full acquisition of ME Production.TORM acquired the remaining 25% of ME Production, gaining full ownership of the scrubber systems provider. They now further support innovation and reinforce their footprint within the Marine Scrubber Systems Market.

- In May 2024, LiqTech International entered a strategic partnership with Franman

LiqTech formed an agreement with Franman for the latter to market LiqTech’s marine scrubber water treatment solutions in Greece. This move boosts the Marine Scrubber Systems Market presence in the world’s largest ship-owning nation.

Report Coverage:

The research report offers an in-depth analysis based on Technology Type, Application, Vessel Type, Fuel Type and End User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Marine Scrubber Systems Market will expand with stricter global sulfur emission regulations driving compliance adoption.

- Hybrid scrubber systems will gain strong traction due to flexibility across diverse regional operating environments.

- Retrofitting activities will remain a critical growth area as shipowners seek cost-efficient compliance for older fleets.

- New-build installations will rise steadily as shipyards integrate scrubbers at the design stage to enhance efficiency.

- Digital monitoring and IoT-enabled systems will strengthen operational transparency and improve regulatory reporting accuracy.

- Compact and modular scrubber designs will appeal to operators seeking efficient installation and reduced maintenance needs.

- Emerging economies will present new opportunities through expanding maritime trade and stricter environmental alignment.

- Strategic alliances between technology providers and shipyards will accelerate technology integration and global market reach.

- Innovation in sustainable water treatment and filtration technologies will address concerns over washwater discharge.

- The market will remain highly competitive, with continuous R&D and consolidation shaping long-term industry leadership.