Market Overview

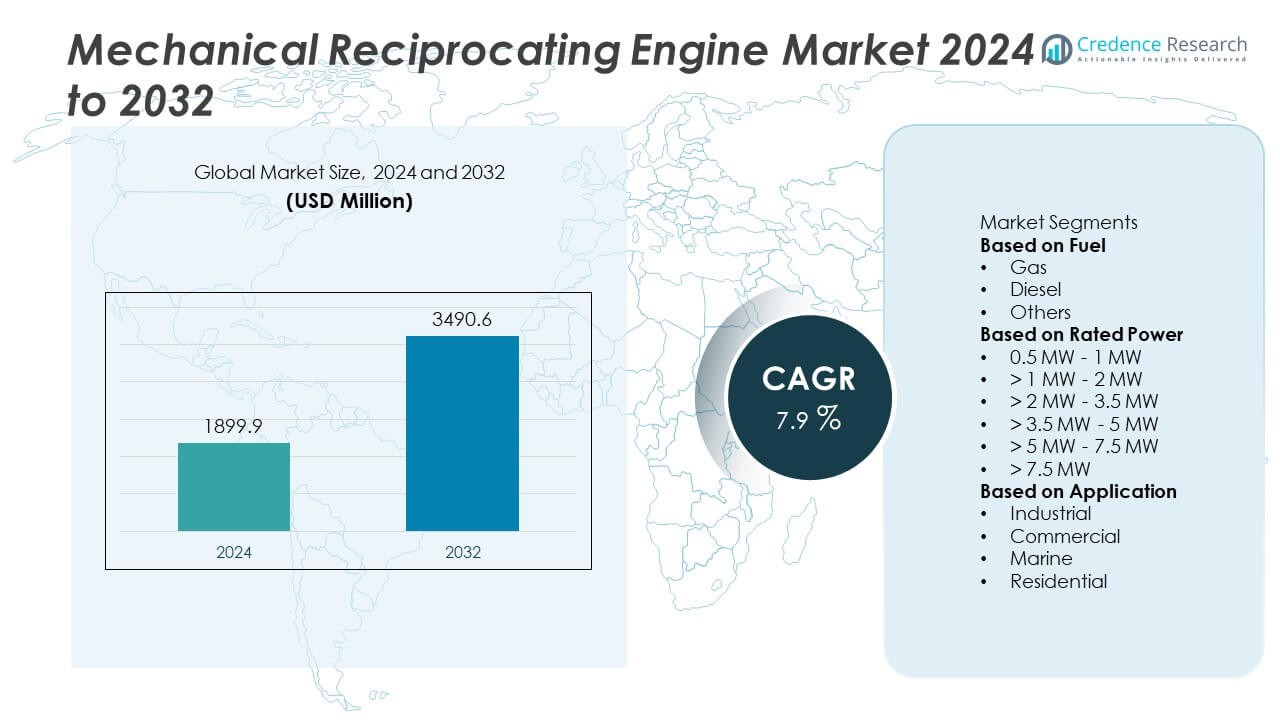

The Mechanical Reciprocating Engine Market was valued at USD 1,899.9 million in 2024 and is projected to reach USD 3,490.6 million by 2032, expanding at a CAGR of 7.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Mechanical Reciprocating Engine Market Size 2024 |

USD 1,899.9 Million |

| Mechanical Reciprocating Engine Market, CAGR |

7.9% |

| Mechanical Reciprocating Engine Market Size 2032 |

USD 3,490.6 Million |

The Mechanical Reciprocating Engine Market advances through rising demand in industrial power generation, marine propulsion, and agricultural equipment, where reliable and flexible power solutions remain essential. Industries adopt these engines for their durability, fuel versatility, and ability to operate in remote or off-grid environments.

The Mechanical Reciprocating Engine Market demonstrates broad geographical presence, with North America emphasizing oil and gas operations, data center backup systems, and advanced emission-compliant technologies. Europe focuses on sustainable solutions, including biofuel-compatible and hybrid-ready engines, supported by strong demand in marine and district heating applications. Asia-Pacific emerges as the fastest-growing region, where urbanization, agriculture, and marine industries create significant opportunities for compact and high-capacity engines. Latin America and the Middle East & Africa show steady uptake driven by rural electrification, industrial growth, and infrastructure projects. Leading companies shaping the market include Caterpillar Inc., known for large-scale power solutions; Cummins Inc., a global leader in fuel-efficient and emission-compliant designs; Deutz AG, specializing in compact and modular engines for industrial and agricultural equipment; and Kawasaki Heavy Industries, advancing marine and heavy-duty applications. Their diverse strategies and technological innovations strengthen competitiveness across global markets.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Mechanical Reciprocating Engine Market was valued at USD 1,899.9 million in 2024 and is projected to reach USD 3,490.6 million by 2032, expanding at a CAGR of 7.9% during the forecast period.

- Strong demand arises from industrial power generation, marine propulsion, and agricultural machinery, where engines deliver reliable energy supply, high torque, and fuel flexibility to maintain operational stability in critical environments.

- Trends emphasize hybrid and dual-fuel technologies, digital monitoring, predictive maintenance, and modular engine designs, all of which enhance efficiency, sustainability, and versatility across industries and geographies.

- Competitive dynamics feature global leaders such as Caterpillar Inc., Cummins Inc., Deutz AG, and Kawasaki Heavy Industries, who focus on innovation in low-emission designs, hybrid compatibility, and high-performance solutions for industrial and marine segments.

- Market restraints include high operating and maintenance costs, noise and vibration issues in urban settings, and growing competition from alternative power technologies such as turbines, fuel cells, and renewable-based systems.

- Regional analysis shows North America leading with industrial and oil and gas applications, Europe prioritizing sustainable and emission-compliant engines, Asia-Pacific driving rapid growth through urbanization, marine, and agricultural demand, while Latin America and the Middle East & Africa expand steadily through rural electrification and infrastructure investments.

- The market reflects a decisive shift toward sustainability, with increasing investments in biofuel, hydrogen-ready, and eco-friendly reciprocating engines that align with stricter emission regulations and long-term energy transition goals.

Market Drivers

Rising Demand from Industrial Power Generation and Backup Systems

The Mechanical Reciprocating Engine Market gains momentum from its role in industrial power generation and backup systems. Industries rely on these engines to ensure continuous operations during grid failures and fluctuating power supply. Their ability to deliver reliable on-site energy drives adoption across manufacturing plants, refineries, and mining operations. Compact design and lower installation costs further strengthen their presence in distributed generation projects. Companies prioritize engines with higher fuel flexibility to support long-term resilience. It continues to serve critical sectors where uninterrupted operations remain a priority.

- For instance, Cummins Inc. commissioned over 400 units of its QSK95 reciprocating engines in 2024, each delivering 4,200 horsepower, to support continuous backup power for data centers and industrial facilities in North America.

Expansion of Marine and Shipping Applications for Heavy-Duty Engines

Marine and shipping industries drive strong demand in the Mechanical Reciprocating Engine Market due to their heavy-duty power needs. Cargo vessels, fishing boats, and offshore platforms deploy these engines for propulsion and auxiliary power supply. Their high torque output ensures dependable performance in demanding sea conditions. Compliance with maritime emission standards influences innovation in dual-fuel and gas-based variants. Engine makers invest in robust designs that withstand long operating cycles and saltwater exposure. It strengthens market relevance in regions with active shipbuilding and port development.

- For instance, Kawasaki Heavy Industries initiated operation of an 8 MW-class gas engine modified for 30 percent hydrogen mixed-fuel combustion in October 2024, enabling significant CO2 emissions reduction compared to conventional fuel usage.

Growing Preference in Agricultural and Construction Equipment Utilization

The Mechanical Reciprocating Engine Market benefits from extensive use in agricultural machinery and construction equipment. Tractors, harvesters, and irrigation systems employ these engines for dependable field operations. Excavators, loaders, and drilling rigs require consistent power for extended working hours. Their ease of maintenance and long operational life encourage widespread adoption among rural and infrastructure development projects. Manufacturers design engines with higher efficiency to minimize fuel consumption in large-scale farming. It maintains a strong foothold in economies with expanding agricultural output and infrastructure growth.

Integration of Fuel Efficiency and Emission Reduction Technologies

Advances in engine design reinforce the Mechanical Reciprocating Engine Market through fuel efficiency and emission reduction. Governments enforce stricter emission standards that push manufacturers toward cleaner technologies. Incorporation of turbocharging, direct fuel injection, and advanced cooling systems improves performance while reducing environmental footprint. Hybrid-ready and dual-fuel models broaden their application scope across multiple industries. These developments enhance competitiveness against alternative power solutions. It ensures long-term market growth while aligning with sustainability objectives.

Market Trends

Adoption of Hybrid and Dual-Fuel Engine Technologies Across Industries

The Mechanical Reciprocating Engine Market advances through the introduction of hybrid and dual-fuel systems. Industries prefer engines that operate on both conventional and cleaner fuels to reduce operational risks. This flexibility supports compliance with emission standards and ensures efficiency across variable supply conditions. Manufacturers introduce gas-based models that lower carbon output without compromising power density. Integration of hybrid features enables smoother transitions between fuel sources. It positions reciprocating engines as adaptable solutions in energy-intensive industries.

- For instance, Wärtsilä delivered four 34DF dual-fuel reciprocating engines to a 38 MW power plant in Myanmar. These engines are designed to run on both gas and liquid fuels, offering flexibility and efficiency.

Integration of Digital Monitoring and Predictive Maintenance Solutions

Engine manufacturers incorporate digital tools to enhance performance in the Mechanical Reciprocating Engine Market. Remote monitoring platforms allow operators to track real-time data on vibration, pressure, and fuel usage. Predictive maintenance reduces downtime by identifying potential failures before disruptions occur. These systems improve lifecycle management and reduce costs associated with unplanned repairs. Companies deploy cloud-based analytics to streamline engine operations across distributed sites. It creates new opportunities for advanced service offerings in the sector.

- For instance, Caterpillar introduced its Cat Remote Asset Monitoring system in 2024, which tracks over 1.2 million data points daily across reciprocating engine fleets worldwide, enabling predictive maintenance that extends overhaul intervals.

Shift Toward Compact and Modular Engine Designs for Versatile Use

The Mechanical Reciprocating Engine Market witnesses demand for compact and modular designs that suit diverse environments. Compact engines meet the requirements of portable power generation, agricultural equipment, and small marine vessels. Modular systems allow customization to specific power ratings, enhancing flexibility for industrial operators. Manufacturers focus on reducing weight without sacrificing durability or efficiency. Improved space utilization makes these engines suitable for urban infrastructure projects and off-grid installations. It expands their relevance in emerging economies where versatile energy solutions are essential.

Emphasis on Low-Emission and Sustainable Power Alternatives

Sustainability trends shape innovation in the Mechanical Reciprocating Engine Market through low-emission solutions. Governments impose stricter emission norms that encourage investment in cleaner combustion technologies. Biofuel-compatible engines gain traction in regions with strong renewable energy adoption. Companies explore hydrogen-ready engines to align with future energy transition pathways. Stricter fuel regulations in marine and transportation sectors accelerate deployment of eco-friendly variants. It reinforces the market’s alignment with global sustainability objectives.

Market Challenges Analysis

Rising Competition from Alternative Power Technologies and Stringent Regulations

The Mechanical Reciprocating Engine Market faces competition from alternative technologies such as gas turbines, fuel cells, and renewable-based power systems. These substitutes often deliver higher efficiency and align more easily with evolving sustainability targets. Governments impose stricter emission standards that increase compliance costs for engine manufacturers. Companies must invest heavily in research to modify designs and incorporate advanced emission control systems. High regulatory pressure limits the speed of adoption in certain regions. It forces manufacturers to balance innovation with cost control while remaining competitive against emerging technologies.

High Operating Costs and Technical Limitations in Large-Scale Applications

Operational challenges remain significant in the Mechanical Reciprocating Engine Market due to high fuel consumption and maintenance requirements. Engines require frequent servicing of pistons, valves, and cooling systems, leading to increased downtime. Large-scale installations often encounter cost inefficiencies compared with alternative generation methods. Rising fuel prices create further strain on industrial users who depend on consistent power supply. Noise and vibration concerns restrict deployment in urban and sensitive environments. It underscores the need for advanced design improvements to overcome technical and cost barriers in critical applications.

Market Opportunities

Expansion in Decentralized Power Generation and Rural Electrification Projects

The Mechanical Reciprocating Engine Market holds opportunities in decentralized power generation and rural electrification initiatives. Governments and private operators invest in distributed systems to address power gaps in remote regions. Engines provide reliable, standalone solutions where grid connectivity remains limited or inconsistent. Their adaptability to multiple fuel sources supports continuous energy access in diverse conditions. Demand from microgrids, community power plants, and rural industries increases potential growth avenues. It strengthens the role of reciprocating engines as vital contributors to energy security in underserved areas.

Innovation in Biofuel and Hydrogen-Compatible Engine Technologies

Advances in alternative fuel compatibility open significant opportunities in the Mechanical Reciprocating Engine Market. Manufacturers develop engines capable of running on biofuels, synthetic fuels, and hydrogen blends to meet clean energy targets. This transition aligns with global sustainability agendas and reduces dependence on conventional fuels. Research collaborations with energy firms accelerate the adoption of hybrid-ready and eco-friendly models. Industries such as marine, transport, and agriculture create demand for engines that meet low-carbon objectives without sacrificing reliability. It positions reciprocating engines as future-ready solutions in the evolving energy landscape.

Market Segmentation Analysis:

By Fuel

The Mechanical Reciprocating Engine Market segments by fuel into diesel, natural gas, dual-fuel, and others. Diesel engines maintain wide adoption due to their durability, high torque output, and suitability for heavy-duty operations in marine, mining, and industrial environments. Natural gas variants gain momentum with lower emissions and reduced operational costs, making them attractive for utilities and distributed generation projects. Dual-fuel models provide flexibility to switch between diesel and gas, ensuring operational continuity where fuel supply fluctuates. Manufacturers focus on biofuel and hydrogen compatibility to align with clean energy initiatives. It diversifies the fuel portfolio and supports adoption in regions with varying resource availability.

- For instance, MAN Energy Solutions delivered twelve 51/60DF dual-fuel reciprocating engines in 2024 for a power project in Bangladesh, each rated at 18.9 MW, providing a combined output of more than 225 MW with the ability to operate on both natural gas and liquid fuels.

By Rated Power

The Mechanical Reciprocating Engine Market divides by rated power into below 1 MW, 1–5 MW, and above 5 MW segments. Engines below 1 MW dominate smaller applications such as agricultural machinery, construction equipment, and localized power systems. The 1–5 MW range serves mid-sized industrial plants, district energy systems, and backup power facilities that demand reliable capacity. Engines above 5 MW play a critical role in large marine vessels, offshore platforms, and utility-scale projects requiring high resilience. Rising investments in distributed generation drive demand for modular engines across multiple capacity ranges. It strengthens the market’s adaptability to diverse operational scales.

- For instance, Wärtsilä supplied five Wärtsilä 34SG gas-fired engines to a generating facility in the Czech Republic in November 2024. The new engines are intended to provide reliable power and are an integral part of the facility’s generating capacity.

By Application

The Mechanical Reciprocating Engine Market categorizes by application into power generation, marine, oil and gas, industrial, and others. Power generation remains a core segment, where engines support grid stability and serve as prime or standby power in industrial clusters. Marine applications expand due to cargo vessels, fishing fleets, and offshore platforms relying on robust engine performance. The oil and gas sector uses reciprocating engines for compression, pumping, and on-site energy supply in upstream and midstream operations. Industrial users integrate engines for continuous operations in mining, chemicals, and manufacturing plants. It reinforces the market’s role as a versatile power solution across varied sectors.

Segments:

Based on Fuel

Based on Rated Power

- 0.5 MW – 1 MW

- > 1 MW – 2 MW

- > 2 MW – 3.5 MW

- > 3.5 MW – 5 MW

- > 5 MW – 7.5 MW

- > 7.5 MW

Based on Application

- Industrial

- Commercial

- Marine

- Residential

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for 28% share of the Mechanical Reciprocating Engine Market, supported by strong adoption across industrial power generation, oil and gas, and marine sectors. The United States dominates the region with its extensive deployment of engines in shale gas operations, refineries, and backup systems for data centers. Canada adds momentum through investments in distributed power plants, mining projects, and maritime activities in coastal provinces. The region benefits from well-developed infrastructure and advanced service networks that ensure high engine performance and reliability. Stricter emission regulations under the Environmental Protection Agency drive continuous innovation in cleaner and dual-fuel technologies. It reinforces North America’s role as a mature and stable contributor to global demand.

Europe

Europe represents 24% share of the Mechanical Reciprocating Engine Market, characterized by its emphasis on sustainability and compliance with stringent emission norms. Countries such as Germany, the UK, and France focus on biofuel-compatible and hybrid-ready engines to meet EU climate directives. Marine demand remains strong in Norway, the Netherlands, and Greece, where reciprocating engines support both commercial shipping and offshore platforms. District heating and combined heat and power (CHP) systems further drive adoption in industrial and urban centers. The market benefits from established manufacturers with expertise in modular and compact designs that address both industrial and residential power needs. It strengthens Europe’s position as a hub for advanced and eco-friendly engine technologies.

Asia-Pacific

Asia-Pacific leads with 32% share of the Mechanical Reciprocating Engine Market, driven by large-scale adoption across China, India, Japan, and Southeast Asian nations. Rapid urbanization, infrastructure expansion, and growing energy demand fuel investments in decentralized and backup power solutions. Marine and shipping industries in China, South Korea, and Singapore generate strong demand for high-capacity engines. Agricultural reliance in India and Indonesia ensures sustained need for compact, fuel-efficient reciprocating engines. Governments promote renewable and hybrid-compatible technologies to reduce dependence on conventional fuels while addressing carbon emissions. It establishes Asia-Pacific as the fastest-growing region with diverse opportunities across industrial, marine, and rural sectors.

Latin America

Latin America captures 8% share of the Mechanical Reciprocating Engine Market, with Brazil, Mexico, and Argentina emerging as primary contributors. Industrial expansion and oil and gas activities drive adoption, particularly in upstream exploration and distributed power generation. Marine applications in coastal economies such as Chile and Peru also contribute to regional growth. Agricultural machinery powered by reciprocating engines remains a key driver in rural economies across the continent. Governments promote localized manufacturing and service facilities to reduce reliance on imports. It highlights Latin America’s gradual but steady integration of reciprocating engines into both industrial and agricultural applications.

Middle East & Africa

The Middle East & Africa accounts for 8% share of the Mechanical Reciprocating Engine Market, supported by oil and gas operations, power generation, and infrastructure projects. Gulf countries such as Saudi Arabia, the UAE, and Qatar utilize reciprocating engines for upstream and midstream oil activities. Africa shows rising adoption in distributed energy projects, particularly in Nigeria, South Africa, and Kenya, where engines power off-grid and rural electrification programs. Harsh climatic conditions and fuel supply challenges encourage demand for durable and fuel-flexible designs. Marine demand also emerges along African coasts, supported by fishing and transport industries. It establishes the region as a growth-oriented market with increasing reliance on reciprocating engines for energy stability.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The Mechanical Reciprocating Engine Market features strong competition among global and regional manufacturers that focus on performance, fuel efficiency, and compliance with emission norms. Leading players such as Caterpillar Inc., Cummins Inc., Deutz AG, Doosan Corporation, AB Volvo Penta, Kawasaki Heavy Industries, General Electric, J C Bamford Excavators, Escorts Limited, and Fairbanks Morse Engine shape the industry landscape with diversified product portfolios and strategic investments. Caterpillar emphasizes large-scale engines for industrial and marine sectors, supported by advanced emission-control technologies. Cummins strengthens its position with fuel-efficient and dual-fuel engines designed for both stationary and mobile applications. Deutz AG specializes in compact and modular designs suited for agriculture and construction equipment, while Doosan Corporation leverages its expertise in power generation and heavy machinery. AB Volvo Penta focuses on marine propulsion and industrial applications with sustainable and hybrid-ready solutions. Kawasaki Heavy Industries expands in shipping and heavy-duty equipment through high-capacity engines, while General Electric integrates advanced reciprocating engines into energy systems with digital monitoring features. J C Bamford Excavators and Escorts Limited support demand in agricultural and construction equipment, offering reliable and cost-efficient designs, whereas Fairbanks Morse Engine maintains strength in defense, marine, and critical infrastructure. The competitive environment reflects innovation, regulatory compliance, and strong service networks that sustain long-term market presence.

Recent Developments

- In May 2025, Cummins highlighted its European Master Rebuild Centre’s capabilities in remanufacturing engines to like-new standards, offering strong total-life support.

- In February 2025, GE Aerospace certification of its advanced Catalyst turboprop engine reflects its broader propulsion innovation efforts.

- In December 2024, Deutz agreed to acquire a 50% stake in HJS Emission Technology to enhance its expertise in clean and efficient combustion engine technology; the closing is expected in early 2025.

- In October 2024, the Kawasaki unveiled the world’s first hydrogen combustion technology for large gas engines that operate without CO₂ emissions.

- In August 2024, Caterpillar initiated a USD 725 million expansion of its Large Engine Center in Lafayette, Indiana to boost production capacity—particularly for engines and aftermarket parts driven by data center growth.

Market Concentration & Characteristics

The Mechanical Reciprocating Engine Market reflects a moderately concentrated structure where a group of global manufacturers dominate supply with advanced product portfolios and strong service networks. Leading players invest in research to improve fuel efficiency, emission control, and hybrid readiness, creating a high barrier for smaller entrants. It exhibits characteristics of technology-driven competition, where compliance with environmental standards and demand for fuel flexibility define growth opportunities. The market shows wide application diversity, spanning industrial power generation, marine propulsion, oil and gas, agriculture, and construction, which sustains steady demand across regions. It demonstrates resilience through adaptability to multiple fuel types, including diesel, natural gas, biofuels, and hydrogen, ensuring relevance during energy transitions. Strong aftersales service, predictive maintenance support, and digital monitoring systems remain critical differentiators, reinforcing brand loyalty and long-term adoption. It balances innovation with operational reliability, reflecting a blend of established expertise and evolving sustainability goals.

Report Coverage

The research report offers an in-depth analysis based on Fuel, Rated Power, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand through increasing adoption in decentralized and distributed power generation projects.

- Demand will grow in marine propulsion where dual-fuel and hybrid-ready engines support emission compliance.

- Agricultural and construction sectors will continue to rely on compact and durable reciprocating engines.

- Digital monitoring and predictive maintenance will become standard features to improve operational efficiency.

- Biofuel and hydrogen-compatible designs will gain wider acceptance under stricter emission regulations.

- Engine manufacturers will focus on modular and lightweight structures to meet diverse application needs.

- Service-based models and remanufacturing programs will strengthen customer retention and lifecycle value.

- Competition with alternative technologies such as turbines and fuel cells will push faster innovation.

- Asia-Pacific will remain the fastest-growing region with demand from industrialization and infrastructure projects.

- Long-term market direction will align with global sustainability goals through cleaner combustion solutions.